$RKLB - Clear Street's Note From This Morning...

Launch Opportunity Expanding: The recent grounding of Blue Origin’s (private) New Glenn further tightens an already constrained launch market.

Infrastructure Advantage: The industry faces overloaded U.S. federal launch ranges even if more rocket hardware enters the market, reinforcing RKLB’s strategic advantage with its three-pad platform.

Core Business Nearing Profitability: Excluding Neutron R&D, the combined Electron and Space Systems segments are approaching adjusted EBITDA profitability

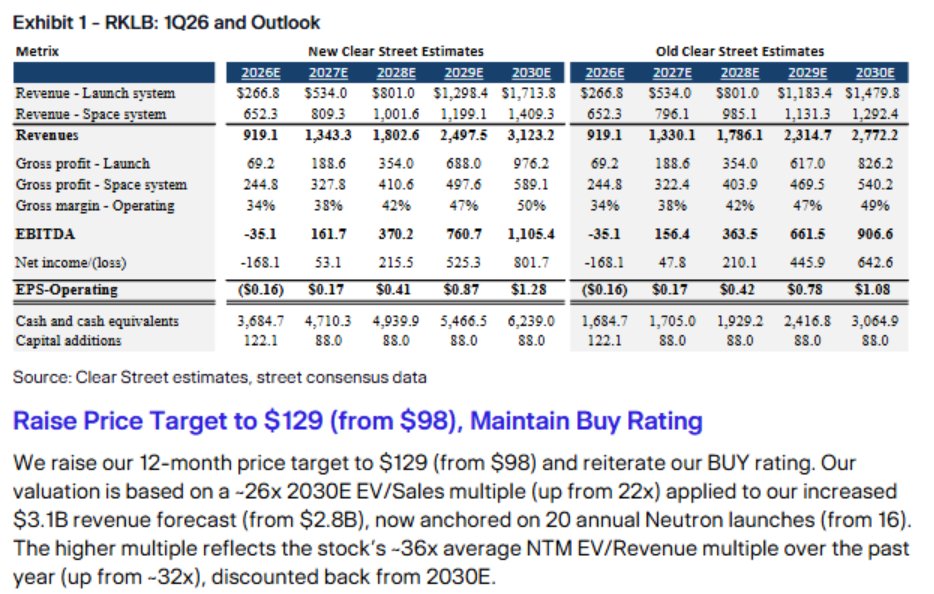

We raise our 12-month price target to $129 (from $98) and reiterate our BUY rating. Our valuation is based on a ~26x 2030E EV/Sales multiple (up from 22x) applied to our increased $3.1B revenue forecast (from $2.8B), now anchored on 20 annual Neutron launches (from 16).

The higher multiple reflects the stock’s ~36x average NTM EV/Revenue multiple over the past year (up from ~32x), discounted back from 2030E

$ASTS - By Bloomberg’s estimates and Goldman’s 2030 Starlink forecasts for 2030, the street is currently estimating AST capturing only 2% of the D2D market….?

Seems like a re-rating much higher is in store for AST if they can execute on launch in the coming 6-12 months! 🧩

$ASTS - Goldman sees Starlink revenue going from $4.2B in 2025 to $144B by 2030!

Bloomberg has AST revenues estimates jumping from $70M in 2025 to $3.3B by 2030 which seems ultra conservative

AST is one of the best asymmetric set-ups in the market today…😎

$ASTS - Goldman sees Starlink revenue going from $4.2B in 2025 to $144B by 2030!

Bloomberg has AST revenues estimates jumping from $70M in 2025 to $3.3B by 2030 which seems ultra conservative

AST is one of the best asymmetric set-ups in the market today…😎

GOLDMAN SEES SPACEX AI REVENUE EXPLODING TO $322B BY 2030

Goldman Sachs projects SpaceX AI revenue rising from $3.2B in 2025 to $322B by 2030, a ~100x increase, forming the core justification for its $1.78T IPO valuation. Total revenue is forecast to reach $474B, with Starlink at $144B and rockets at $8.3B.

AI segment growth is tied to aggressive market assumptions despite current losses and execution concerns around xAI. Overall EBITDA is seen surging to $352B by 2030.

@endurancetest $ASTS has partnered with over 60 MNO’s with access to over 3B customers. Plus we’ll have multiple constellations for govt’s as well. It’s not just about the consumer

$RKLB - Stifel maintains 𝐁𝐮𝐲 on 𝐑𝐨𝐜𝐤𝐞𝐭 𝐋𝐚𝐛, 𝐫𝐚𝐢𝐬𝐞𝐬 𝐏𝐓 𝐭𝐨 $𝟏𝟑𝟐 from $110

Analyst highlights Rocket Lab's strong execution, revenue momentum, and expanding backlog, with Neutron execution seen as key to valuation upside.

$RKLB - Clear Street analyst Greg Pendy raised the firm's price target on Rocket Lab to $129 from $98 and keeps a Buy rating on the shares.

Rocket Lab is positioned for increasingly accelerating growth through 2030, benefiting from industry-wide launch under supply that is expanding backlog opportunities, the analyst tells investors in a research note. The firm added that the company has an advantage in infrastructure, and that its core business is nearing profitability.

Space ETFs are exploding in popularity:

Total assets under management (AUM) in space-themed ETFs has surpassed $5 billion for the first time in history.

Since the start of 2026, space ETF AUM has more than DOUBLED.

Over the last year, this figure has surged by over +900%.

Meanwhile, the Space Innovators ETF, $NASA, launched on March 30th, has grown its AUM to a record $2.6 billion.

Over this period, the fund price has surged +50%, including a +37% increase in May alone.

This comes as $NASA is one of the few investment vehicles available to retail investors that offers exposure to SpaceX, which currently accounts for 7.5% of the fund.

Retail is ready for the SpaceX IPO.