New research finds that the anchoring of medium-term inflation expectations during the pandemic inflation surge weakened more for firms in the manufacturing sector, consistent with the sharp rise in goods-price inflation in 2021. https://t.co/KO46WdwCjl

The first meeting of new Fed Chair Kevin Warsh made clear that we are entering a new -- or old -- era of Fed communication without forward guidance.

Ehsan Khoman, Economist at the BlackRock Investment Institute, shares his key takeaways in this #SpecialMarketTake.

Ladies and gentlemen, the private credit market explained, in two charts.

Left: distribution of private ratings. Vast majority of B and below.

Right: private ratings severely underestimate default risk for ratings... of B and below.

Thanks for listening to my TED talk.

Companies that raced to put AI tools in the hands of their workers are starting to rein in their use, as the cost of deploying the technology at scale begins to test corporate budgets. https://t.co/Dr2rwpEBlc

There's a difference between not telling markets your next move and not telling them how you make decisions at all.

Kevin Warsh, at his first meeting as Fed chair, did both.

Warsh got high marks for planting a flag on the Fed's 2% inflation target and for shearing the policy statement of jargon that had become a recitation of the obvious.

But he also stretched his objection to forward guidance into something broader, using it to sidestep questions about how the committee reasons toward a decision.

"It matters to have some sense of how this committee is thinking about how it goes about conducting this business," said JPMorgan's Michael Feroli.

Jeffrey Rosenberg, portfolio manager of the systematic multi-strategy fund at BlackRock, reacts to the Federal Reserve's decision to keep rates unchanged and says there's a risk of overplaying the flattening yield curve https://t.co/tT5BnZxpL3

Very hawkish dot plot.

Nine out of 18 officials have at least one hike this year (and six of those 9 have *multiple hikes*).

Only one person has a cut this year, and one participant (presumably Warsh) didn't submit an SEP

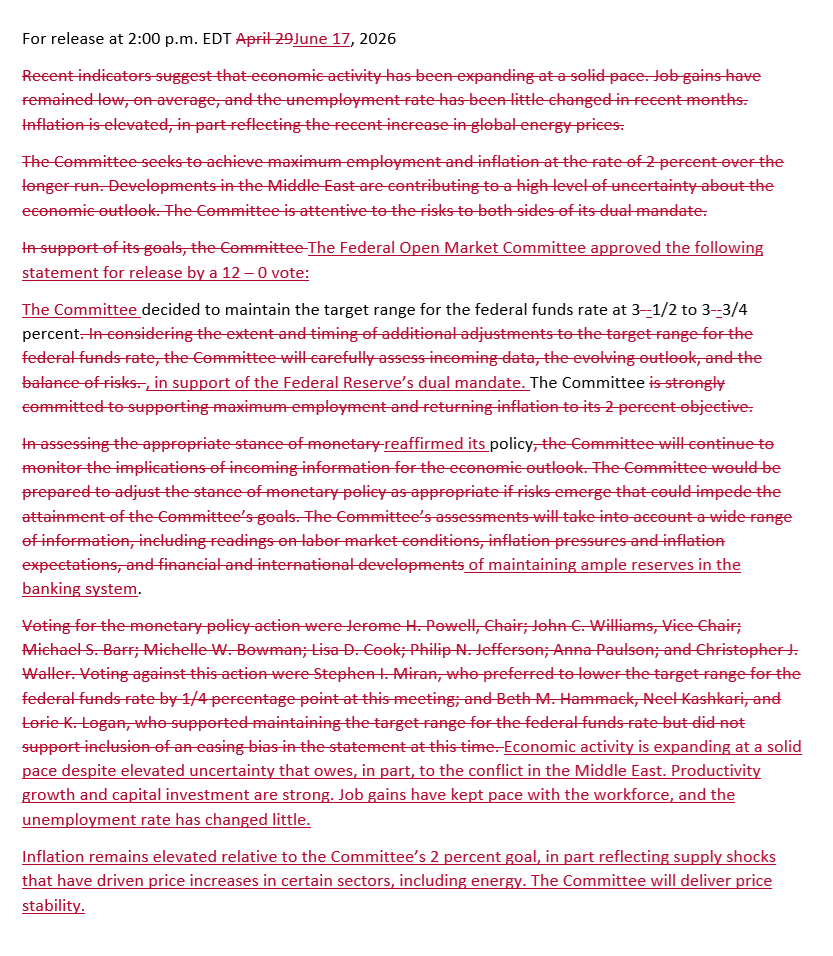

The statement gets a complete writethru from top to bottom, much shorter

⚠️ The risk is not a rate hike, it’s a hawkish dot-plot shift.

Kevin Warsh’s first FOMC decision as Fed Chair on June 17 could force markets to reprice 3 key risks:

1. Dot plot shift toward no cuts

The March SEP median showed one 2026 cut, but the dots could shift toward no cuts and a higher-for-longer rate path.

2. End of RMPs / T-bill purchases

The Fed’s reserve management purchases have slowed, while Q3 Treasury issuance is set to rise sharply.

3. Less forward guidance

If Warsh gives fewer policy signals, markets may lose a key anchor, increasing volatility.

Follow MacroMicro and watch the June 17 Fed decision closely to spot market risk signals early: https://t.co/qzFH4Pyjh2

Kevin Warsh’s Federal Reserve will need to raise interest rates by the end of 2026 to tame the burst of inflation sparked by Donald Trump’s Iran war, leading economists said as he prepares for his first meeting as chair. https://t.co/thaG0fDxqh

#AI is expected to not only replace roles but also spark new industries and entirely new job categories — a trend that has already begun to show signs of taking hold- chart @GoldmanSachs

Global capital markets are incredibly hot:

Companies have raised a record $4.7 trillion in equity, corporate debt, and bank loans so far this year.

This marks the 3rd consecutive annual increase for this point of the year.

Total capital raised is also running ~$500 billion above the 2021 post-pandemic financing boom.

The surge has been driven primarily by technology companies seeking to fund AI spending, alongside record debt issuance to finance AI infrastructure.

Furthermore, investment-grade private credit issuance is not included in these figures, despite playing an increasingly important role in financing data centers, semiconductors, and power plants supporting the AI buildout.

Investors are pouring money into AI an unprecedented pace.

𝐔𝐒 𝐦𝐚𝐫𝐤𝐞𝐭𝐬: 𝐰𝐡𝐞𝐫𝐞 𝐥𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲, 𝐥𝐨𝐧𝐠𝐞𝐯𝐢𝐭𝐲, 𝐚𝐧𝐝 𝐦𝐚𝐫𝐠𝐢𝐧𝐬 𝐚𝐥𝐥 𝐫𝐡𝐲𝐦𝐞.

🇺🇸US dominance in global markets is structural, not cyclical: Scale + liquidity + profitability = the long arc of US outperformance.

NYSE liquidity runs $71B/day, out‑trading Tokyo 1.7×, Hong Kong 2.7×, London 10×.

150 years of equity data show the US compounding at 9.9%, outpacing every major market in recorded history.

EPS growth since 2003: US 21.2% CAGR vs World 14.2%.

Operating margins: US 16%, consistently above DM peers (World 14.7%, Europe 12.6%, Japan 9.5%).

#investments #productivity #Growth