(Assistam primeiramente o video do último post!) Agora, assistam este, após Scaramucci descobrir que seu novo cônjuge não era exatamente aquilo que ele antecipava (sendo que boa parte do trabalho de um gestor de FoF é, uh, implementar due diligence...). Impagável. Como a Bloomberg ainda quer dar moral pra esse cara?

Para quem não conhece Scaramucci, gestor do fund of funds Skybridge, que cresceu agressivamente com pico de AUM perto de US$ 10bn ~10 anos atrás (com bom marketing pois Scaramucci tbm é do "show biz" e, por exemplo, foi host de Wall Street Week), ele tbm é notório por ter ficado apenas 10d na administração Trump 1 (será que vem daí o ressentimento? 🤔). Mas deixemos Scaramucci falar por si mesmo, primeiramente aqui, elogiando o fraudador SBF e comemorando o "casamento" do Skybridge com a FTX 🤦♂️):

I talk to people on Wall Street every day. I have heard some belly aching about the President from time to time, but I have literally not once heard a single person say they regret voting for Trump or, "gee, if only Kamala had won, we would be so much better off." Bloomberg News laments any of the advances our country is making for fear that they might reflect well on the @POTUS and all their news is reported through a lens of severe TDS.

https://t.co/lfhFvWfb7X

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time.

He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha.

He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life."

He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett.

But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them.

Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does.

Enjoy!

Timestamps:

0:00 Intro

1:00 The Kindest Thing

13:19 Trading vs. Investing

17:33 Lessons from Warren Buffet

22:24 The Existential Risks of AI

29:54 The Nature of Trading

31:46 Bitcoin

35:55 Bubbles

42:08 A Day in the Life of PTJ

46:00 Information Overload

47:07 Passion for Markets

50:49 The Robin Hood Foundation

54:18 The Workless World

56:03 Journalism

1:00:00 Principal Components of a Great Life

1:05:06 Kill Them With Kindness

@burrytracker "[You want] three qualities: integrity, intelligence, and energy. [If you] don’t have the first, the other two will kill you" - Warren Buffett

If Sam Bankman-Fried did nothing illegal, he might have been the best VC in history

What SBF bought vs. what it's worth today:

• Cursor: ~$200K → ~$3B (+1,499,900%)

• Anthropic: ~$499M → $82.3B (+16,400%)

• SpaceX: ~$200M → ~$15B (+7,400%)

• Solana: ~$189M → $5.1B (+2,600%)

• Robinhood: $612.5M → $4.9B (+700%)

• Genesis Digital: $1.17B → $3.5B (+200%)

Had he done nothing wrong, he'd have an estimated worth of $114,000,000,000 today

Instead he's tweeting from Federal Correctional Institution

STANLEY DRUCKENMILLER: “I JUST DON’T CARE WHAT I PAID FOR A STOCK. IT’S ABSOLUTELY IRRELEVANT.”

“If the reason I bought a stock is no longer the case, I don’t care if I bought it at 60 and it’s 50. I have no emotion whatsoever.”

“There’s resistance at certain prices because a bunch of people bought at 60, it went down, and they’ve been waiting 3 or 4 years for it to get back. Meanwhile they could’ve been in something else going up the whole time.”

His friends and fellow investors say he’s “entirely unemotional.” His response: “Yes. I’m told that’s true.”

Is that the key to his success?

“I think it’s a big part of it. Being open-minded and having humility. The only reason you can change your mind is if you’re not arrogant about a position.”

📊 Chart of the Day 📊

Changing rates and inflation expectations affect energy importers the most.

❌ Europe, the U.K., and Japan are energy importers and face larger downside growth risks.

✅ Canada and Australia should benefit from their net energy export status.

@PIMCO

https://t.co/tn0VMxKIaA

‼️ Competent central bankers should not be raising rates as economies plunge into supply shocks. Yet Australia has just hiked rates while facing mounting shortages of distillates, food, and other essential goods. ‼️

The academics running the world’s leading central banks…the Fed, ECB, BOE, and others…need to pause their singular focus on inflation and recognize the broader reality: tightening policy in the middle of supply-driven stress amplifies global problems and pushes us further into recession.

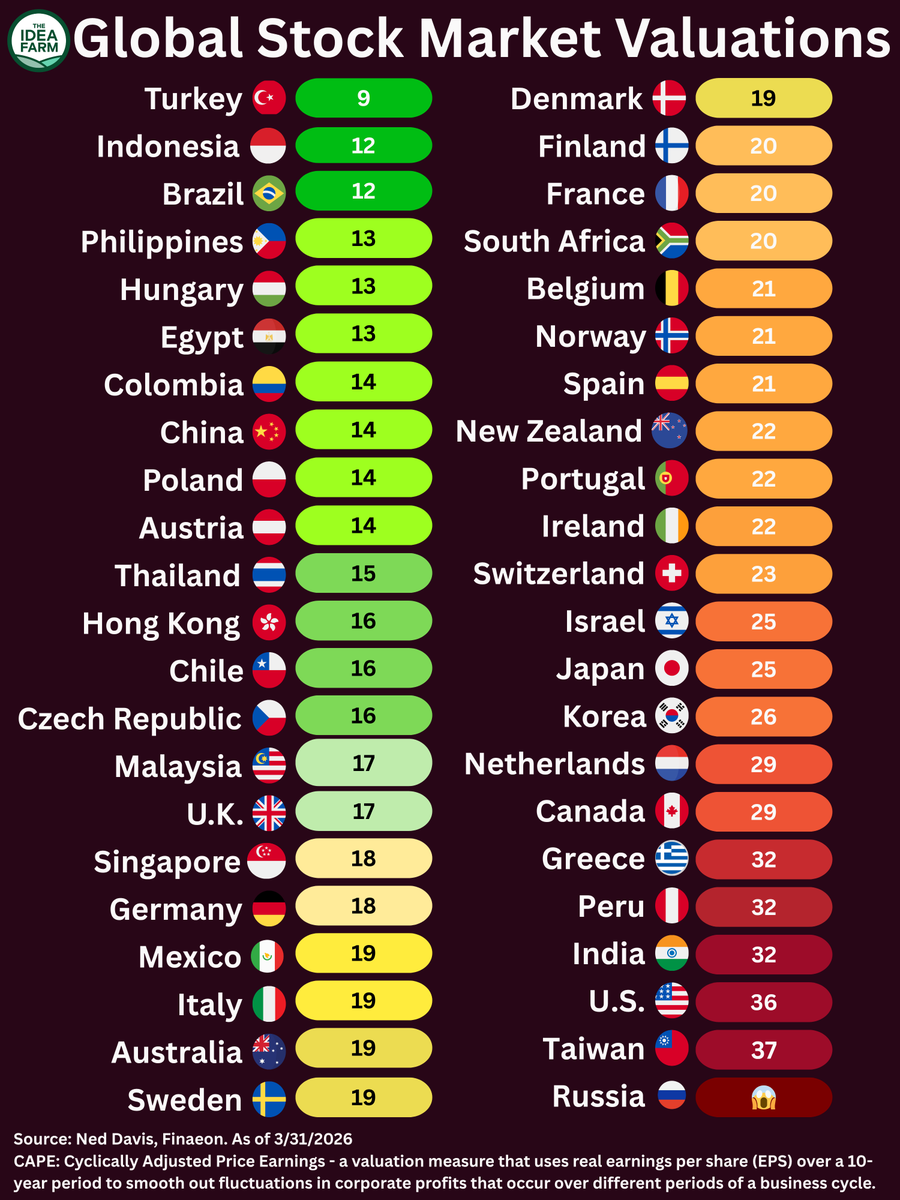

O critério utilizado para mapear esta "distribuição global de valor", em mercados desenvolvidos, foi empresas com: (1) valuation menor que valor patrimonial (P/B); (2) valuation menor que 10x lucro (P/E); (3) capitalização superior a usd 100mm

Deep value stocks are not equally distributed globally: Europe today accounts for 1/3 of the global opportunity set. Japan is 1/4, South Korea is 15%, EM 18% and the US & Canada only 11%.

My information consumption is now 1/4 X, 1/4 podcast interviews of the smartest practitioners, 1/4 talking to the leading AI models, and 1/4 reading old books. The opportunity cost of anything else is far too high, and rising daily.

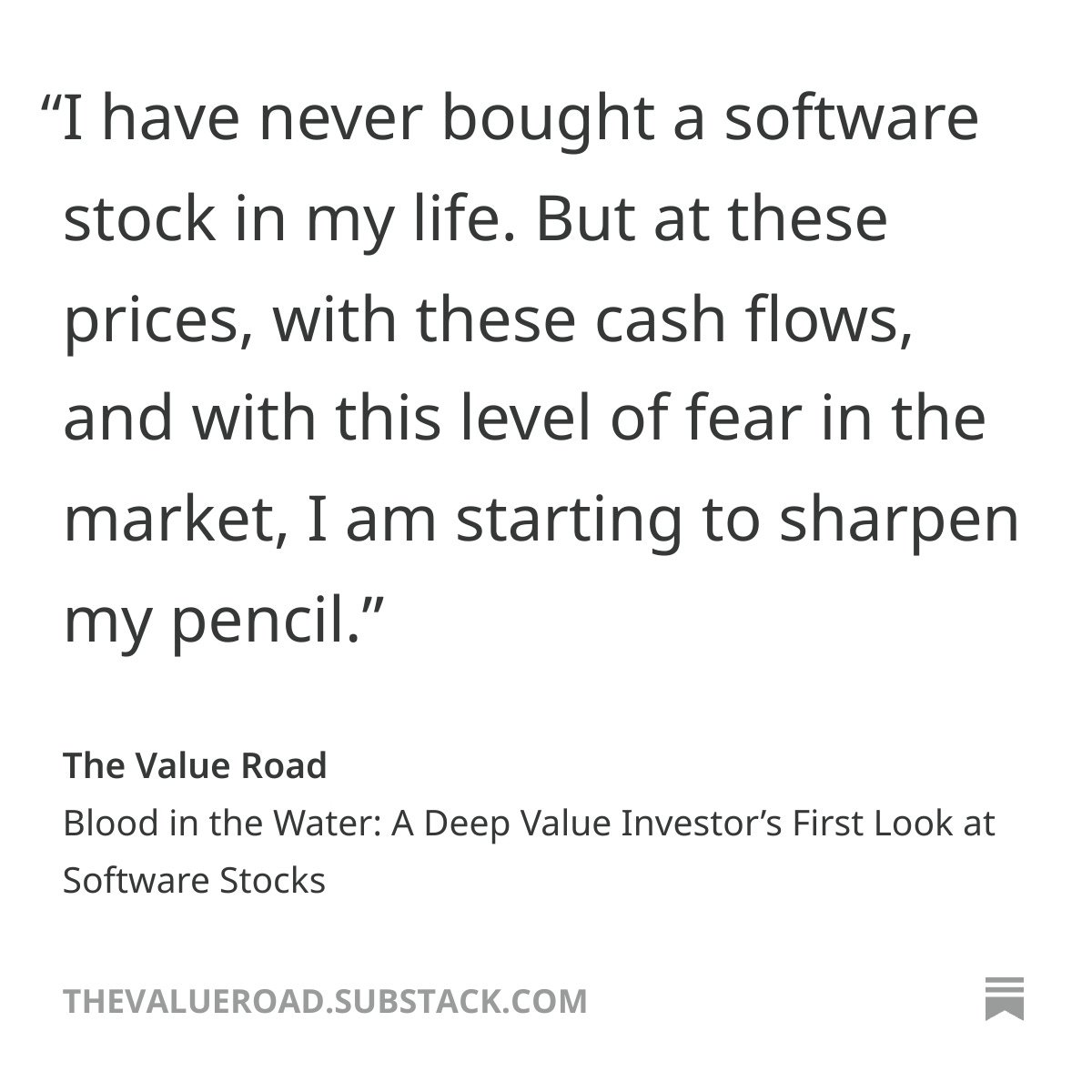

Bons pontos. Claro, um dos catches é se as empresas de software [will be] “declining 5% a year” apenas. Pessoalmente (RTR) tomo bastante cuidado com falling knives... Mas o post lembra o Warren, qdo jovem: “Vou lhes dizer como se fica rico. Fechem as portas. Sejam medrosos quando os outros forem gananciosos. Sejam gananciosos quando os outros forem medrosos.”

I've spent years buying ugly, cheap, unloved microcaps. Never once touched a software stock. They were always way too expensive. No margin of safety. I'd look at 40x revenue multiples and move on.

For the first time in my career, I'm paying attention.

AI fears have absolutely cratered software stocks. The narrative flipped overnight from "every software company is an AI beneficiary" to "every software company is an AI victim." Multiples that were 15-20x revenue are now 4-6x. Some lower. Names down 50-70% from highs.

I'll be honest, the bears have a point. AI is taking a blowtorch to the traditional software moat. Switching costs, network effects, integration complexity, all diminished. I'm not going to pretend otherwise.

But a narrower moat does not mean zero terminal value.

There's a long, profitable history of buying melting ice cubes. Tobacco stocks in the early 2000s. Newspapers at the trough. Print directories. Everyone priced them for death. The ones that managed the decline intelligently made their investors a fortune. If you pay 3x free cash flow for a business declining 5% a year, you do very well for a very long time.

These software companies are still generating enormous free cash flow. Enterprise customers don't rip out systems they spent years and tens of millions implementing because a startup showed a good demo. That's not how procurement works.

And here's what the market is really missing, these aren't buggy whip manufacturers. They're software companies. They have the engineers, the data, the domain expertise, and the distribution to adopt AI faster than anyone. AI doesn't just threaten them. It lets them cut costs and expand margins dramatically.

A startup can build a great product. But getting past enterprise security reviews, procurement teams, and support requirements? That takes the distribution infrastructure incumbents spent decades building.

For years software was wildly overvalued. Now it's priced like every customer churns next quarter and cash flow goes to zero. The truth is in the middle. It always is.

When a deep value microcap guy starts sharpening his pencil on software stocks, either I've lost my mind or the prices have finally come to me.

I'm betting it's the latter.