Can’t believe Nike got Ja shipped right to Portland them shoes goin so crazy them folks said you ain’t fuckin this shit up for us NO MORE nigga bring ya ass to headquarters

@breakpoint67 Don’t take no more breaks bro me and the family counting on you every night for tennis picks 🎾 we win some we lose some but your a goat. 🐐

Tennis Picks 6/22 🎾

1 unit each unless otherwise noted

Atmane ML +111 (Novig)

Ugo Carabelli ML +240 (ProphetX)

Draper ML +110 (Bet365)

Collignon / JM Cerundolo u21.5 games -122 (Kalshi)

Choinski ML +223 (Novig)

Quinn -2.5 games spread -127 (Novig)

Struff ML +138 (Novig)

Elon just created 4,400 millionaires in a single day.

400 of them are now worth over $100 million.

These aren't VCs. They're SpaceX employees, and the list includes welders, technicians, and cafeteria staff, because for two decades the company paid every level of the workforce in stock instead of higher salaries.

Juan Hernandez immigrated from Mexico and took a $28 an hour contractor welding job in 2015. He says he didn't even know what SpaceX was. The company gave him a $10,000 equity grant and let him buy more shares through payroll deductions. That stake is now worth $880,000.

Trevor Hise's parents wanted him to take a stable job at General Electric. He picked SpaceX instead, stayed 12 years, and accumulated over 100,000 shares. At the $135 listing price that's $13.5 million. He's 37 and semiretired. His words: "The magnitude of this has been ridiculous."

The most telling detail came before the listing. Over 100 employees quietly banded together and negotiated a group wealth management deal covering up to $5 billion, because none of them had ever needed a wealth manager before.

Software IPOs have minted millionaires for 30 years. This is the first one where the money went to the factory floor.

I’ve been asked by many to create one comprehensive post explaining how to prepare for @SpaceX’s IPO if you use one of the brokerages listed in SpaceX’s S-1 filing to allocate IPO shares to retail investors. Here it is:

Fidelity:

1) $500,000 minimum account balance required to participate (including IRAs, individual, etc, but excluding 401k).

2) Enter an indication of interest. The indication of interest provides Fidelity with the maximum number of shares a customer is interested in purchasing.

3) Confirm your indication of interest shares on Fidelity's website after the registration statement has been declared effective and the offering has priced, which is typically after 7 PM ET on the night of pricing. Indications of interest may not be confirmed prior to the registration statement being declared effective and the offering pricing established. By confirming your indication of interest, you are placing an order to buy shares at the offering price. If you do not confirm your indication of interest, you will not be eligible for an allocation of shares.

4) Allocation of shares will occur on the morning following pricing and is usually complete before 9:30 AM ET. An alert will be sent once allocations are complete, and you can check your account to determine whether you were allocated shares. If you receive an allocation of shares, you must have adequate funds available to settle the purchase in the settlement date which is typically the trade date plus one business day.

5) You may increase your indication of interest up through the close of the indication of interest period. You may decrease or cancel an indication of interest until share allocation takes place. Once share allocation takes place, your indication may not be canceled or modified.

Charles Schwab:

1) $100,000 minimum account balance required to participate (including IRAs, individual, etc, but excluding 401k).

2) On Schwab's website, under the Trade tab, select the IPO page to view the Calendar of Offerings, a list of upcoming IPOs. Once the IPO offering window opens (expected first week of June), investors will have the ability to submit a Conditional Offer to Purchase (COTP), also known as an Indication of Interest, from this page.

3) During an IPO's open COTP window, select Start COTP to review offering details and the preliminary prospectus. Then select the green button to proceed to the Eligibility Questionnaire, which is required to confirm investors meet eligibility criteria and are not restricted (per FINRA rules) from participating. After completing the questionnaire, you'll be able to indicate how many shares you're interested in purchasing based on the price range provided. Select Confirm to submit the COTP.

4) After the COTP has been submitted, regularly monitor the IPO page, which will indicate the Status of Your Conditional Offers to Purchase (COTPs), the expected pricing date, and current pricing status, plus any changes in the prospectus. When the IPO has been priced, you will affirm your COTP. You must affirm your COTP once the effective price is established in order to be eligible to purchase shares. To do so, select Affirm Now to review and finalize the share quantity.

Robinhood:

1) There's no minimum account size requirement, but you must have enough buying power to cover your requested shares if you are allocated any. You must have an individual brokerage account. Retirement, custodial, and multiple investing accounts are not eligible for IPO Access.

2) Make sure IPO Access is enabled in your Robinhood app. Turn on your IPO notifications so that Robinhood notifies you when the SpaceX IPO comes online.

3) Request Shares: Once the IPO is announced and available, you can request shares through the app or website. This is a request for IPO shares. By placing a conditional offer to buy (COB), you’re asking for the opportunity to purchase a quantity of shares at the IPO price. An investor may place, edit, or cancel a COB after the initial price range is published and before the confirmation period ends.

4) Allocation is random and not guaranteed. The number of shares you request factors into how many you actually get, but it doesn’t affect the likelihood that you’ll get any allocation. You may get all, some, or none of the IPO shares you request.

E*Trade:

1) E*TRADE does not publicly list a specific minimum account size required to participate in IPOs, but contact them to double check. That said, allocation priority for “hot” IPOs may still favor larger or more active accounts in practice, even if there’s no official minimum balance requirement.

2) Be a U.S. resident, have an active E*TRADE account (Individual, Joint and IRAs are all eligible) and complete the investor profile questionnaire.

3) Sign up for IPO alerts.

4) Submit a conditional offer to buy ("COB"). As part of this submission, you specify the number of shares and the maximum price you are willing to pay per share. COBs can only be submitted via the New Issue Center. A COB may be submitted once an offering is listed as "open" up until the status is changed to "closed." COBs that have already been submitted may be amended or cancelled after an offering is "closed" up until the status is changed to "allocate." At this point, no further changes may be made to a COB and you are bound by the terms of your COB. If there is no material change in an offering, customers will not need to reconfirm their COBs. If you have submitted a conditional offer, you must have available buying power to cover the full amount of your conditional offer in the account through which you submitted the conditional offer.

5) Shares are allocated to eligible accounts as a proportion, or percentage, of the size of their COB. The percentage is based primarily on the number of shares provided to E*TRADE for sale to its customers and the size of the overall demand for shares from E*TRADE's customers. Given the expected high demand for this offering and the limited availability of shares available for sale to E*TRADE customers, many COBs may not be allocated shares (according to E*Trade). Additionally, in many instances, allocations will be significantly smaller than the size of shares requested in a customer's COB.

6) E*TRADE makes its allocations after the pricing of the overall offering but before the stock begins trading. E*TRADE will inform customers via alert or email whether they have been allocated shares. Any allocation should be reflected in the relevant customer account once that allocation has been processed by E*TRADE.

Sofi:

1) There is no minimum account balance/size requirement. Have an active Self-Directed Invest account.

2) Go to the “IPO Investing” section in the app or website

3) Select the IPO

4) Complete the IPO suitability questionnaire

5) Submit an “Indication of Interest” (IOI), which is basically a non-binding request for shares.

6) When the IPO is officially priced, SoFi will notify you to confirm your order.

NOTE: Don’t be surprised if you receive fewer IPO shares than you requested, or none at all. Demand for the limited number of IPO shares available to retail investors will likely be extremely high, and each participating brokerage will only receive a limited allocation of shares to distribute to retail investors.

For our international friends, keep in mind that @SpaceX said in their S-1 filing that allocations will also be made to retail investors by the underwriters, which include:

• Goldman Sachs

• Morgan Stanley

• Bank of America

• Citigroup

• J.P. Morgan

• Barclays

• Deutsche Bank Securities

• RBC Capital Markets

• UBS Investment Bank

• Wells Fargo Securities

• Allen & Company

• Cantor

• Needham & Company

• Raymond James

• Societe Generale

• Stifel

• William Blair

• BTG Pactual

• ING

• Macquarie Capital

• Mirae Asset Securities

• Mizuho

• Santander

so you can try reaching out to one of these places if you have assets with them and you may be able to request an allocation of some shares. I've already seen that happen with some Goldman Sachs clients.

Lastly, and I stated this in a previous post, @SpaceX specifically stated in their S-1 filing that any purchase of their Class A common stock in this offering through these platforms will be at the same IPO price, and at the same time, as any other purchases in this offering, including purchases by institutions and other large investors, which means any retail investors that are lucky enough to get allocated some SpaceX IPO shares will pay the same price as the big guys. This will likely be the largest retail IPO share allocation in history, by far.

If you have more questions, reach out directly to your brokerage and/or bank. And no, this post wasn't written by AI lol.

Not financial advice.

WTA predictions for Roland Garros day 3

Siniakova ML vs Waltert

Mboko ML vs Bartunkova

Jovic ML vs Eala

Liu ML vs Uchijima

Sabalenka 2-0 sets vs Bouzas-Maneiro

Osaka ML vs Siegemund

Ann Li ML vs Zhang

Coco Gauff ML vs Townsend

Ruzic +1.5sets vs Krueger

Kalinskaya ML vs Boisson

Join my free telegram for live picks and more analysis (link in my bio)

Let’s go🎾💪🏼

#tennis #wta #rolandgarros #frenchopen #picks #predictions #apuestas #parlay

Welcome everyone, I just joined X.

For the past 4 months, I’ve been sharing tennis analysis and betting picks on Telegram, building a strong and consistent track record.

Current run: 32/39 winning picks 🎯

If you love sports and you’re into tennis insights, stats, and value bets, you’re in the right place.

I have more than 30 years of experience competing and coaching tennis at a high level. I will provide you a lot of valuable information in the tennis world and share my analysis and picks.

More to come✅

Some predictions:

• $IREN becomes a $100B+ company after fully monetizing its 5GW

• $SOFI becomes the financial backbone of the next generation

• $LMND becomes the largest insurance company in the world

• $HIMS offers the most valuable subscription product in the world

• $META smart glasses replace the iPhone

Your credit score is not actually a real score

It's a probability rating that 3 private companies invented in 1989 to sell to banks for $1 each

You never agreed to it. You can't audit it. They don't owe you an explanation. And it controls roughly half a million dollars of your life

Here's what FICO and the credit bureaus don't say out loud:

FICO is not a government agency. It's a publicly traded company (NYSE: FICO) called Fair Isaac Corporation. They generated $1.7 billion in revenue in 2024 selling credit scoring algorithms to banks. Their stock trades at $1,800+/share. Their CEO made $14.5M last year

VantageScore is the competing private algorithm, owned jointly by Equifax, Experian, and TransUnion. They generate revenue selling scores to banks that don't use FICO. Combined revenue: roughly $400M annually

Neither company is regulated by the federal government. Neither is required to disclose how their algorithm calculates your score. Neither owes you anything. They're private vendors selling probability models to bank customers, and you are the inventory they're scoring

What FICO actually is:

A predictive model designed to estimate one specific outcome: the probability that you will go 90+ days delinquent on a credit obligation in the next 24 months

That's it. That's the entire purpose. Your "credit score" is just a number between 300 and 850 representing how likely a bank thinks you are to miss a payment

The model is built using regression analysis on millions of historical credit files. FICO finds patterns: people with X traits default at Y rate. They assign weights to traits. They produce a score

What's actually in your score (FICO's stated weights):

Payment history: 35%

Amounts owed (utilization): 30%

Length of credit history: 15%

Credit mix (types of accounts): 10%

New credit (recent inquiries): 10%

But the actual calculation is a black box. FICO doesn't publish the exact formula. They publish the categories. The weights inside those categories are proprietary. The interactions between variables are proprietary

You also have at least 9 different FICO scores. They're not interchangeable:

FICO 8 (most commonly used for credit card applications)

FICO 9 (newer version, treats medical debt differently)

FICO 10 (current version)

FICO 10T (incorporates trended data)

FICO Auto Score 8/9/10 (auto lender variant)

FICO Bankcard Score 8/9 (credit card variant)

FICO Mortgage Score (mortgage lender variant, uses FICO 2/4/5 depending on bureau)

When you check your credit score on Credit Karma, you're seeing a VantageScore (not a FICO score). When you check it on your Chase app, you're seeing FICO Bankcard Score 8. When a mortgage lender pulls your credit, they're seeing FICO 2 (Experian), FICO 4 (TransUnion), and FICO 5 (Equifax)

These can differ by 30-80 points for the same person on the same day. The score you see on the app and the score the bank sees are often not the same number

Why this matters:

The 0% APR business card stack covered in funding posts requires a 720+ FICO score. Which FICO score? The bank's. Which bank's? Depends on the bank. Chase pulls FICO Bankcard Score 8 from Experian. Amex pulls FICO 8 from Experian or TransUnion depending on state. Capital One pulls FICO 8 from TransUnion mainly

If you have 740 on Credit Karma (a VantageScore) but 695 on FICO Bankcard 8 (the Chase version), you might think you qualify but get denied. The number you've been tracking isn't the number the bank is reading

How to actually monitor what banks see:

Pull your real FICO scores from myFICO. com ($29/month for all 28 FICO variants, or $9.95/month for basic 3 FICO scores)

Pull free monthly FICO scores from your existing credit cards (Chase, Discover, Capital One, Bank of America all offer free FICO 8 scores to cardholders)

Pull free official credit reports at annualcreditreport. com (weekly access now, used to be annual, expanded in 2023)

These are the real numbers. Credit Karma and similar free services are useful for monitoring trends but should not be used to predict approval decisions

The deeper truth:

Your credit "score" doesn't actually exist as a static number. It's a calculation that happens at the moment a bank pulls your file. Different banks pull different scores. The score changes based on which FICO variant they use, which bureau they pull from, and what day they pull

You don't have one credit score. You have somewhere between 28 and 56 different credit scores depending on how you count. The number on your favorite credit monitoring app is one of them. The number that decides whether you get the $50K Chase Ink approval is a different one

The implication for the dispute and repair process:

When you dispute items off your credit report, you're affecting the underlying data that ALL FICO models pull from. Improvements show up in every score. If you delete a collection from your Experian report, every FICO score that pulls Experian improves: FICO 8, FICO 9, FICO 10, FICO Bankcard 8, FICO Auto 8, FICO Mortgage 2

This is why dispute work is more valuable than people realize. You're not improving "one score." You're improving the entire family of scores that every lender in America pulls

The score game is rigged in one specific way:

It's a private system controlled by 4 publicly traded companies (FICO, Equifax, Experian, TransUnion) that collectively generate $20+ billion a year selling your data and your scoring against your data. You are the product. You don't get to opt out. Your only leverage is the FCRA, which lets you force corrections to the underlying data

The bureaus want you to believe your score is accurate, immutable, and meaningful. It's none of those things. It's a probability rating that 4 private companies sell to banks, and the underlying data is wrong about 25% of the time, and the wrong data costs you the half-million-dollar lifetime differential mentioned in the previous post

Stop treating your credit score like a report card. It's a price tag set by an algorithm you didn't agree to. The only legal way to negotiate that price is to fix the data feeding the algorithm

(i fix credit in 30-90 days. link in bio)

🚨The Fed just said AI is breaking the economy in three different ways.

This was not in any public statement. It came directly from the April 28-29 FOMC minutes.

THE FIRST WAY IS INFLATION.

The Fed's own members said that strong AI investment spending is pushing up input costs across multiple industries. Every company building or using AI infrastructure is paying more for power, equipment, and services, and those costs are being passed down the supply chain.

The Fed flagged this as a direct contributor to core inflation that is separate from energy prices and tariffs. AI was supposed to reduce costs across the economy. The Fed is now saying it is adding to them.

THE SECOND WAY IS THE PRIVATE CREDIT MARKET.

Software companies that borrowed money from private credit funds are quietly deferring their interest payments using payment-in-kind arrangements, where instead of paying cash interest they just add it to the loan balance. The Fed flagged this specifically in Q4 2025 and Q1 2026.

The reason investors are pulling money out of these funds is that they believe AI will destroy the business models of the software companies inside them. Private credit funds saw net outflows in Q1 2026 specifically because of AI disruption fears. Blue Owl, one of the largest private credit managers in the world with $36 billion in its flagship fund, was forced to cap redemptions after investors tried to pull 21.9% of the fund in a single quarter.

Its technology-focused fund saw 40.7% of investors request their money back in the same period. Blue Owl halted redemptions entirely, sold $1.4 billion in loan assets, and Blackstone, Apollo, Ares, and KKR all fell 5 to 6% the same day.

The $1.8 trillion private credit market is cracking from the inside and the Fed confirmed in these minutes that AI disruption fears are the reason why.

THE THIRD WAY IS JOBS.

Multiple Fed members said that business contacts are already telling them they plan to delay or reduce hiring specifically because of AI adoption. This is not a future risk.

Companies are making those decisions right now, before AI has fully arrived, and the Fed internally flagged it as a risk that could push unemployment sharply higher very quickly.

The Fed held rates unchanged. But for the first time, their internal minutes show AI is no longer just an economic opportunity they are monitoring. It is now a source of inflation, a credit market risk, and a hiring slowdown, all at the same time.

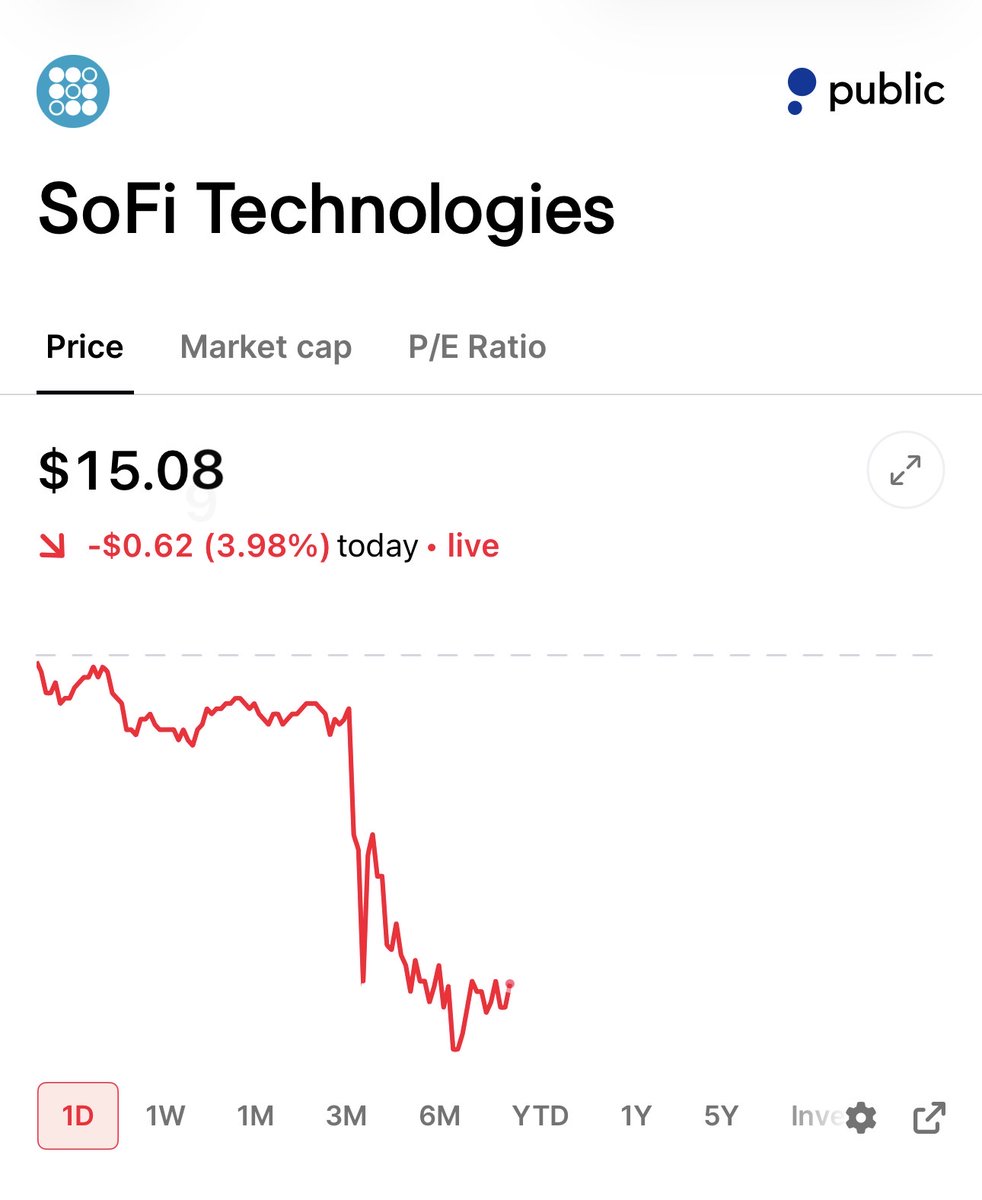

You could buy 100 shares of $SOFI right now for ~$1,508

Or you could buy the $15 call LEAP expiring January 2028 for ~$550

Directional exposure to 100 shares. ~63% less capital. Over 612 days of runway.

The trade:

Strike: $15

Expiration: January 21, 2028

Premium: ~$5.50 per contract

Breakeven: $20.50

If $SOFI hits $25, this LEAP returns ~82%

If $SOFI hits $30, this LEAP returns ~173%

If $SOFI hits $40, this LEAP returns ~355%

Buying 100 shares at $15.04 and watching it hit $50 is a ~232% return. The LEAP returns ~536% on roughly a third of the capital.

Why I like the setup:

- Q1 2026 adjusted net revenue up 41% YoY to $1.09B

- Adjusted EBITDA up 62% YoY to $340M with a 31% margin

- Members up 35% YoY to 14.7M

- Products up 39% YoY to 22.2M

- Total loan originations hit a record $12.2B, up 68% YoY

- Financial Services revenue up 41% YoY to $428.5M

- Deposits grew $2.7B in the quarter to $40.2B

- Management maintained 2026 guidance for ~$4.655B in adjusted net revenue, ~$1.6B in adjusted EBITDA, and ~$0.60 adjusted EPS

The max you can lose on a LEAP is the entire premium you paid. In this case, that's ~$550 per contract. LEAPs are leveraged and can lose value quickly if the stock drops or stays flat. Only size this so you're comfortable losing all of it.

Note: LEAPs are one tool inside a broader portfolio. Owning shares is always the primary use of capital. This is a selective add-on for high-conviction moments when conditions align.

NFA DYOR

@barkmeta Here’s the part that y’all are forgetting…. it’s fucking ugly…. And screams I want a broke ass version of the real thing, because I need validation from a brand.