We are combining:

• Global payment acceptance

• Native multi currency business accounts

• Instant internal settlement

• Treasury and FX control

• Automated reconciliation

• Developer first APIs

• Platform and marketplace infrastructure

• Payments and banking integrated into one system.

• Built for cross border operators.

Our community should not have to fear being debanked or worry whether a legitimate transaction will be delayed or denied. Access to financial infrastructure should not feel fragile.

https://t.co/AgpHklc2hy

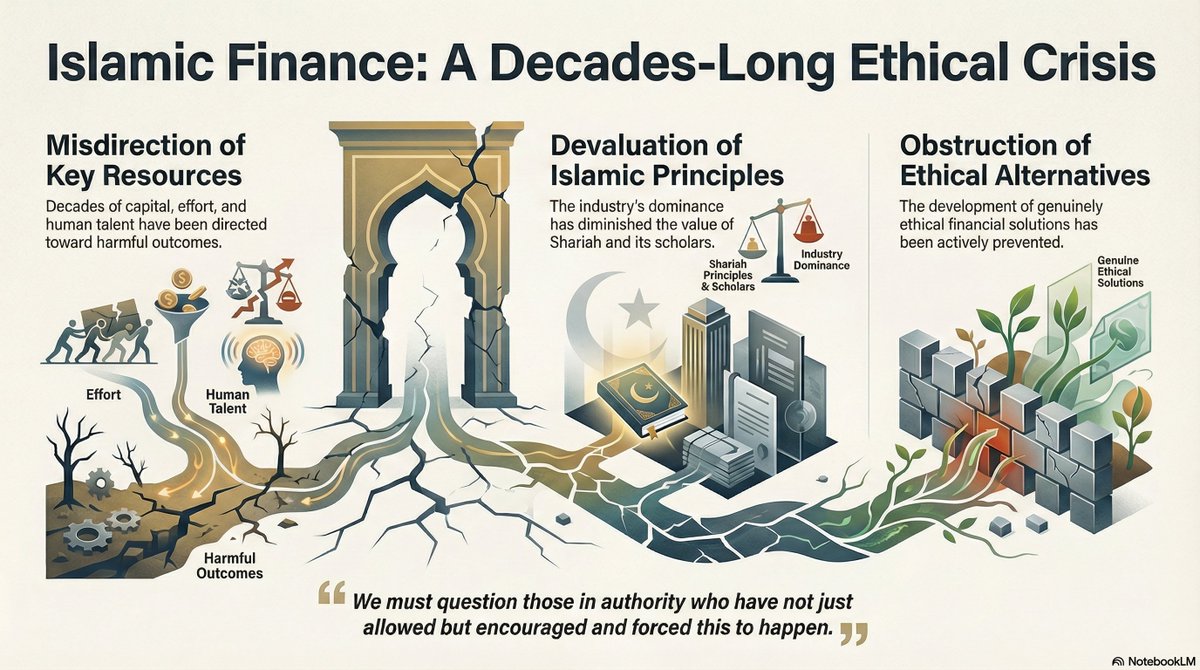

Part 4/4 Islamic banking is not a compromise with Riba. It IS Riba — industrialised, licensed, and Shariah-approved

Series - Why Islamic banks Lend instead of invest - The Economics They Don't Want You to See. - From an Insider who built this machine

BEGINNING

In the previous parts we have observed the following:

Islamic banks are subject to stringent regulatory requirements, such as Basel 3, which requires banks manage the risks that they enter into by taking certain measures. A key measure is that the bank must allocate sufficient regulatory capital to meet the risk of adverse events, such as their customers (borrowers) failing to repay loans, and other assets of theirs falling in value (or being illiquid such that they cannot effectively be utilised in emergency scenarios)

The consequences of these regulations mean that lending is far more efficient than actually buying an asset or making an investment. The latter two attract much higher risk weightings, meaning they are less efficient for the Islamic bank.

With the addition of credit creation, this inefficiency is now longer just impractical, it is downright impossible. Credit creation can be utilised for lending and not for investing or buying assets. As such, the Islamic banks can deliver 30x more loans than a single investment of the same size, and when it comes to residential property, it can make over 40x more profit with the same capital outlay (cash and regulatory capital) than buying a property outright,

Islamic banks obtain a banking license that permits them to lend whilst putting the deposits at risk. It is this activity that requires a banking license (as defined by the Bank of England) and the following activities do NOT require a banking license:

- The taking of deposits

- The provision of loans (look at the proliferation of nob bank credit providers in the market).

- The buying of assets, such as property, commodity, Palm Oil, or milk cartons

- The holding, and selling of such assets

- Investments into any financial assets

So, if an entity goes through the process of obtaining a (Islamic) banking license, then it will be intending to lend money whilst putting deposits at risk.

And the process of obtaining a banking license is not something you wake up and decide. It is a long onerous and expensive process.

For example, in the UK, Revolut obtained its banking license in 2024, and it took their application 3 years to be accepted, and at the time they had 9 million customers in the UK and group revenue of over £2bn.

As noted in FinTech Weekly:

“A full UK banking licence would grant Revolut access to the domestic lending market, enabling it to deploy customer deposits for loans and other credit products. Such a move could introduce new competition to established high-street banks, particularly in digital consumer finance.

However, without the licence, Revolut’s capacity to operate as a traditional bank remains limited. The company continues to function as a hybrid platform that combines payments, foreign exchange, and investment services under its existing permissions.”

So, we have an Islamic bank, that has undertaken the serious, lengthy and expensive process of obtaining a banking license, the primary benefit of which is it can now lend money.

There is also another benefit of a banking license, which is that it can engage in credit creation, a right that is given to private banks and to no other entity on the planet. (This is, in fact a monstrous right that they have, and is the source of much of the financial slavery we experience today).

Islamic banks also have this right to effect lending via credit creation. And that is WHY they obtained a banking license in the first place.

The result is that for an Islamic bank to buy a real asset, instead of lending, it must accept making 1/40th of the profit it can make via lending. This decision is suicide.

If they did not have a banking license, and instead actually purchased property, and made investments, such as is the activity of a huge portion of the global investment market, then they would not be subject to such comparisons, They would utilise real capital, make real investments and be forced to deliver efficiencies to ensure their investments are profitable. All of these are good things, and especially so in Islamic Finance.

So, we must conclude, that the fact that Islamic banks have decided to obtain a banking license means they have already worked all of this out and decided that lending is the way to go.

Now, of course, lending money and making profit on it is Riba. So they cannot do that.

But they must utilse credit creation to benefit from this 40x profit leverage, so what do they do? What they do is very simple.

They utlise simple Shariah contracts such as buying and selling to instead replicate this lending, This provides the required façade to enable some scholars to provide Shariah approval and thus the activity of the bank is now Shariah compliant.

My position is that the robust and intellectually honest application of Shariah to these trading activities of an Islamic bank would result in this Shariah compliance being removed.

So, we now have a clear presentation of the battlefield:

- An Islamic bank has a banking license and thus must lend to benfit from this 40x profit leverage

- An Islamic bank cannot be seen to be lending money as this results in Riba

- Islamic banks thus engage in buying and selling to replicate the effect of lending (thus gaining access to this 40x profit leverage) whilst demonstrating that their activities are simply buying and selling and thus Shariah compliant

If the above was true, we would see certain outcomes be clear:

- When an Islamic bank is engaging in trading, the outcome would be the same as a loan

- Any sales activities that result in the bank taking risks on the underlying assets must then be tweaked such that any asset risk is removed For example:

- The bank will buy and then immediately sell an asset

- The bank takes no risk on the delivery or performance of this asset

- The bank will only buy the asset once the immediate sale of it is contractually certain

- When the bank buys assest (cash out) it will pay immediately and when it sells an asset (cash in) it will sell it on deferred repayments to replicate the required loan

- The sale to the customer (to effect the loan repayments) will be a function of the loan size, the repayment time, and the market interest rates (just like a regular loan)

In market practice we see every one of these outcomes, all the time, every time.

And this is all deemed as Shariah compliant because basic rules of sale contracts are followed. But the rules around combinations of sales contracts are ignored. It si this combination that results in the loan and Riba, not an isolated sales transaction in itself.

So the Islamic banks now apply themselves to present these sales transactions as standalone, isolated sales transactions, and not structued as a combination of 2, 3, or 4 circular sales transactions.

When we play games with Shariah, I have seen that something happens. It forces us to encounter anomalies and plain impossibilities. Because our Shariah is never intended to be used to justify lending and Riba, and when we force this, the reality then forces outcomes that are plain impossible. It is these outcomes that everyone must lie about, or plain hide from scholars. For example:

- When the banks conduct a Tawarruq transaction, which is a sequence of sales transactions, we end up having to claim that a commodity broker, with £5mn is buying and selling commodity worth £1bn in a single transaction

- We have a commodity / Tawarruq exchange in Malaysia that is selling $25tn of commodity a year, when only $2bn max of that commodity exists, and the Shariah requirement is that the commodity must be delivered to the buyer if requested

- We have billions of dollars of Islamic loans being effected by the buying and selling of commodities that nobody every wants, like platinum, timber, copper, palm oil and milk cartons

- Whenever an Islamic bank sells something it is replicating the repayment of a loan with interest, so that sales prices is deferred, repaid in the future, and benchmarked to interest rates, just like a loan demands

- When an Islamic bank sells something, it has to buy it first, but it will have cast iron guarantees, BEFORE it buys the item, that it will be onsold immediately to the customer

- The Sukuk market, which comprises 25% of the global $4tn Islamic finance industry, is built on the apparent investment into assets, but all risk of asset ownership is systematically removed, piece by piece, so what is left is a bond which is Riba (I have written a whole book about this and made a 2 hour video about a single Sukuk issuance showing all this complex trickery works in practice)

- A Malaysian professor from INCIEF analysed 900 Sukuk issuances over 15 years and found precisely ZERO retain asset risk and performance, and all deliver bond performance, which is Riba

- We have a multi trillion business built on organised commodity sales to deliver Riba and supported, in a 250 page policy document, by a simple statement that sales transactions are permitted in Shariah, and quoting one verse from the Quran

- We have Islamic banks whose balance sheets are comprised between 95-99% (assets and liabilities) of interest rate instruments, not sales and investments

This is utter madness.

This is diabolical

We have systemically chosen Riba as our foundation (Islamic banking) and we have consistently, and relentlessly, delivered Riba via the guise of Shariah compliance, and we have built an army of scholars who fight to approve it and preserve it.

We are wholly lost.

We are wholly to blame.

In this part 4/4, I was meant to also address solutions, but our descent into madness prevents that. I will write a part 5/4 that looks at solutions and what the way forward must look like.

I have played a big role in building this monster, this abomination, and this is part of my public penance, my tawbah, and my duty to expose what I know. I have blame here, and do not seek to avoid it. I face it full on and ask for forgiveness.

My only aim is to lighten my scales on the Day and be a servant of Allah swt.

May Allah swt forgive us

Part 5/4 to follow - the way forward out of this diabolical mess

I was absolutely thrilled that Binance had moved in Islamic finance. This was supposed to be a massive moment for the space.

Then I found something deeply wrong tucked away in their FAQ:

These new shariah staking products are their same old LST tokens (BNSOL and WBETH). Just with a new frontend.

Boss - Muslims are TIRED of the grift. Just repackaging the same foods and finances and slapping a halal label is not the way. We’ve seen this game played time and time again. We saw it in TradFi with banks. We saw it in halal food sector. And we’ve even already seen it in crypto (Islamic Coin, Bybit Halal Portfolio, etc.).

And you know what happened?

100s of millions of Muslims have learned to completely distrust incumbents and build their own.

There’s a reason the TradFI Islamic finance market is $4T at best. Have you thought about that number considering that Muslims are ~25% of the global population? It should at least be like $10T which is less than 10% of the total financial market.

So why is it so small? The reason is because Muslims don’t trust it. We’ve seen the grift so many times we built a collective immunity to relying on these repackaged products.

In the short term, you might see big growth. But in the long term you lose Muslim trust and shoot yourself in the foot.

It's not too late and there IS a better way. Binance if you can hear me, I want you to win long term.

Work with a team that’s examined the entire staking process forensically and carefully. That’s built and refined a truly shariah compliant product from the ground-up. No shortcuts. No easy stamps. And has all their research public.

Binance, ByBit or whoever: we’re ready to help you win massively and for the long term. Just reach out to us.

a lot of folks hate on what we’re doing.

many of those haters know us in our personal lives. they know how dedicated we are to studies, to teaching, and to our families.

they just don’t know that we’re the ones behind these handles.

#BTC

Nice bounce so far as uptrend remains intact

Clear, close, confirm above the 10 SMA at $105k and likely have our new higher low and should see a push to new all time highs next

@ZHoubba Our "Liquid Staking Token" that auto-stakes SOL halal for you

And will soon power halal looping & leveraging so you can get 2.5X leverage on SOL and ~25% APY

https://t.co/808Ik7xOZv