I hate to admit this, but I completely agree with the IMF on this one.

I know that this may sound heavily counterintuitive. In all my political analysis on this platform, I have consistently pointed out that the IMF and the World Bank do not give out loans to genuinely help developing countries. They lend strictly to control the economies of developing nations, force privatization, and forcefully open local markets for the massive global multinationals financing these exact institutions.

However, I have done my deep research on this highly secretive Abu Dhabi loan scheme that the Nigerian government is presently considering, and what I found is deeply troubling and borderline treasonous.

First, it is crucially important to emphasize that this is the first time Nigeria, in all its long, painful history of borrowing to build infrastructure, is ever seriously considering a Total Return Swap (TRS) loan.

Historically, Nigeria has always restricted its sovereign borrowing to Eurobonds, bilateral government-to-government loans(with China), Paris Club concessional debt, standard World Bank infrastructure facilities, or traditional commercial syndicated loans.

Not only has Nigeria never tried a Total Return Swap loan in the past, but other African nations have actively, aggressively avoided this financial death trap entirely. In fact, the only two African nations to have even foolishly attempted to engage in a Total Return Swap loan are Senegal and Angola, and in both tragic cases, the macroeconomic aftershocks have been devastatingly brutal.

First, I see Nigerians making the erroneous and highly emotional argument that the IMF is strictly against this loan simply because they do not want us borrowing from China or the Middle East. This is a massive because the toxic TRS loan that Angola eventually took was actually structured through an American bank, JPMorgan, and the IMF still criticized it heavily, publicly, and relentlessly. Secondly, even though the bank Nigeria currently intends to borrow this money from may proudly bear an Arabic name, the underlying operational and structural plumbing of global finance rigidly dictates that it is absolutely impossible for the UAE to directly lend billions of dollars to Nigeria without the direct involvement, backend infrastructure, dollar liquidity, and clearing systems of major American banks. So Wall Street still gets to comfortably eat from this toxic loan, even though it is geographically originating from the Middle East.

Secondly, it is incredibly easy to understand why the Tinubu Administration is pushing so aggressively to lock in this loan. Recall that a strong rumor was circulating last month that the World Bank had permanently terminated an $800 million loan to the Nigerian government. Well, the truth is that it was actually the Tinubu Administration that urgently requested the World Bank terminate the loan because the harsh conditions were simply too much to swallow politically. The World Bank arrogantly demanded that Tinubu impose even more taxes on electricity and hike tariffs which would effectively raise the suffocating cost of survival for Nigerian businesses, which Tinubu respectfully declined because the tax burden was already provoking mass anger.

So right now, it is highly probable that Tinubu is quietly running to Abu Dhabi to collect a massive, strings-free loan that will definitely not come with painful Structural Adjustment Programmes that would force him to devalue the Naira further, remove more subsidies, or hit Nigerians with heavier, crippling taxes.

This is highly understandable from a purely selfish political calculus. General elections are exactly seven short months away, and the frustrated, hungry, and exhausted Nigerian population could violently rebel against him at the ballot box. So obviously, another punishing World Bank loan is completely off the table for now if the President intends to comfortably return to Aso Rock come 2027.

This is exactly why they have desperately chosen this Total Return Swap loan. This is because Abu Dhabi does not care a single bit about the junk credit ratings of Nigeria, they do not care about structural adjustment programmes, they will not demand Nigeria cuts funding for healthcare, slashes education budgets, eliminates remaining agricultural subsidies, privatizes critical national assets, or forces mass layoffs in the civil service just to qualify for this cash. However, this loan comes with a very strict, highly predatory condition that every single Nigerian should be deeply concerned about, violently reject, and aggressively demand the government immediately withdraw their application for.

First, to even qualify for this $5 billion loan, the Nigerian government must physically hand over sovereign government bonds worth over 133% of this loan, which translates to a staggering ₦6.6 Trillion, directly to the UAE. These Treasury Bills are binding debts that the Nigerian government has legally promised to pay out to creditors, and Abu Dhabi will instantly sell off these bills to the international market to secure their ₦6.6 trillion. These new global buyers will effectively be holding Nigeria's sovereign debt hostage. These private, faceless investors will eventually turn to the Central Bank of Nigeria and violently demand to be paid the interest (coupons) and the massive face value of those bonds. The Nigerian government is now legally, permanently obligated to pay out ₦6.6 trillion of our bleeding taxpayers' money to these aggressive private bondholders.

This is not even the scariest part of this suicidal deal. Another strict, unforgiving obligation of this toxic loan is the terrifying "Margin Call." You see, since these Treasury Bills are heavily priced in Naira, their global value will violently fluctuate depending on how our fragile exchange rate changes. If the Strait of Hormuz is permanently reopened, for example, the global price of oil per barrel will drastically plummet below the $100 mark. This will definitely, immediately impact our Naira value since it will rapidly dry up the vital US dollars flowing into Nigeria, given that 90% of our foreign reserves are entirely dependent on crude oil exports. This means significantly fewer dollars will now be coming into the country, which will trigger massive dollar scarcity. Basic, elementary economics dictates that we should automatically expect the Naira to violently crash to ₦1,600, ₦1,800, or even ₦2,000 per dollar. If this nightmare happens, let us assume the Naira falls by 40%. Then the underlying value of the Nigerian treasury bills issued to the UAE would effectively crash in value by 40 percent. In response, they will instantly issue an aggressive margin call to Nigeria, legally forcing the CBN to immediately, unconditionally transfer $2.6 billion in raw cash directly to the UAE just to keep the loan position open.

Now, pay attention: this massive amount does not even settle the outstanding principal loan, it does not settle the mounting interest on the loan, it is simply a punitive penalty fee that Nigeria must bleed out just to keep the contract active. Nigeria would either have to raid our already depleted foreign reserves (which are supposed to be strictly used to defend the Naira, pay for imports, and secure national stability) just to keep a useless loan position open. If Nigeria does not want to send scarce dollars to the UAE, Nigeria would be contractually forced to issue and blindly pledge an additional ₦2.64 trillion in brand new Treasury bills. Instead of having ₦6.6 trillion in national debt held hostage by a foreign bank, Nigeria would suddenly have ₦9.24 trillion totally locked up. If Nigeria eventually defaults, the amount of national debt the UAE bank can maliciously dump onto the fragile local market violently increases from ₦6.6 trillion to over ₦9.2 trillion, and this would absolutely, mathematically guarantee a total domestic financial collapse.

Look at the tragic case of Angola, for example. Just four very short months after collecting this exact type of toxic loan from JPMorgan, their local currency violently crashed, legally forcing Angola to urgently scrape together and send $200 million in raw cash directly to the American bank, and despite this massive financial bleeding, they eventually defaulted on the entire loan anyway.

This is exactly what every Nigerian desperately needs to understand. Tinubu is not actively avoiding the IMF and the World Bank because his administration has suddenly decided to act sovereign, stand tall, and look for a genuinely better, more respectful lender. This administration is directly, purely avoiding the World Bank because their specific loan will come with heavier taxes, painful structural reforms, and massive public backlash since a highly contested election is dangerously close. But now, this desperate administration is blindly grabbing onto a far more dangerous, explosive, and financially lethal loan that has the direct capacity to cripple our entire economy, destroy our currency, and bankrupt our future faster than the World Bank or IMF could ever possibly dream of.

The society of Nigerian accountants needs to urgently study the complex terms of this toxic loan, hold emergency press conferences, and issue a strongly worded statement to condemn it in its strongest possible terms. The lawyers need to immediately download these predatory loan agreements, study the fine print, dissect the hidden clauses, expose the draconian arbitration terms, file urgent injunctions in federal courts, drag the Finance Minister to the National Assembly, and forcefully petition international financial watchdogs. We, as an exhausted people, need to finally wake up, get angry, and do something concrete, as this is a catastrophic decision that will violently affect our daily lives, our businesses, and our children. Yes, an election is coming, but the election is not tomorrow, the election is not next month, the election is in exactly 7 months, and by then, this financial death warrant would be permanently signed, sealed, and firmly delivered. The House of Assembly will obviously, spinelessly approve these loans without reading a single page because their privileged children, their wealthy families, and their unborn grandchildren will obviously never be affected by the brutal terms of this financial slavery. But we, the ordinary, hardworking, and highly taxed Nigerians, will be the ones totally crushed to the absolute ground when this house of cards inevitably crashes.

Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐️

Dialysis is draining man, I'm literally on my knees. I need medication refill and food to get by. If you can spare something please help a brother. My number is 09098539701, 08079468065. Thank you. 🙏🏿

“The t£rrorists need all the money they’re getting from k+dnapping. It’s not like they are living luxurious lives. The government is putting too much pressure on them so they need money to finance their war machines.” – Sheikh Gumi

NGX vs Ecobank: A ₦627 Billion Market Cap Discrepancy Investors Cannot Ignore

So, I was discussing with the TG members during our usual Sunday session, something we have consistently hosted every Sunday since 2021, free of charge. One of the topics we discussed was why continuous dilution should never be ignored when building long-term positions in companies. As we started breaking down the banking sector, we got to @GroupEcobank. We noticed major discrepancies in the reporting of its outstanding shares compared to what @ngxgrp currently displays on its platform, which, ideally, should be the go-to and most reliable source for investors.

So, I decided to do a deeper dive.

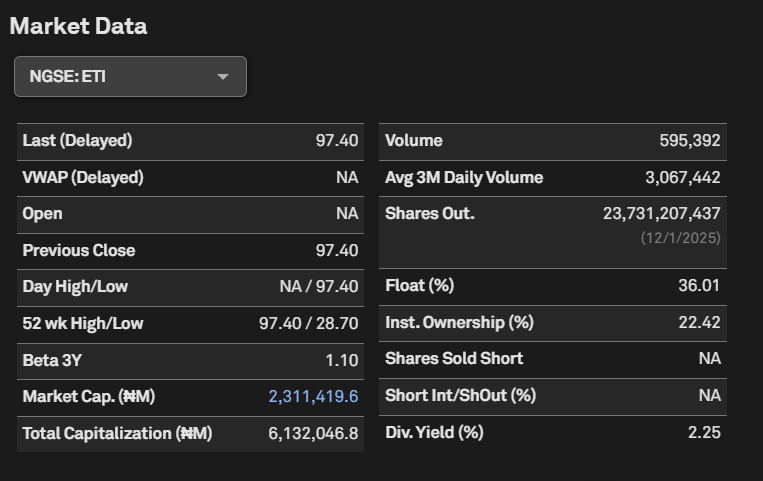

The first screenshot is from the @ngxgrp platform, which currently shows Ecobank’s total outstanding shares at 18,155,073,977. Multiplying that by Friday’s closing price of ₦97.4/share gives a market capitalization of ₦1,768,304,205,359.80.

The second screenshot is from S&P Capital IQ, which reports Ecobank’s outstanding shares at 23,731,207,437 shares. Interestingly, the last update there was dated 1 December 2025. Using the same closing price of ₦97.4/share gives a market capitalization of ₦2,311,419,604,363.80.

The final screenshot is extracted directly from Ecobank’s Q1 2026 financial statement under Note 14, page 29. The company itself reported outstanding shares of 24,592,619,000 shares. Multiplying this by ₦97.4/share gives a market capitalization of ₦2,395,321,090,600. What shocked me even more was that the same outstanding shares figure was also reported in Q1 2025.

Now, today is a weekend, so I do not currently have access to the Bloomberg Terminal to cross-check further, but working with these three data points raises serious questions.

So, who exactly should investors believe here?

Personally, I would naturally rely on the company’s own financial statements because they are the primary source, and I should know their actual outstanding shares.

NGXGROUP Market Cap for ETI = ₦1,768,304,205,359.80

Ecobank Q1 2026 Financial Statement Market Cap = ₦2,395,321,090,600

Difference = ₦627,016,885,240.20

That difference is highly material and honestly quite alarming.

Even if we compare S&P Capital IQ with Ecobank’s reported figures, we still get a discrepancy of about ₦83.9 billion, which remains very material. Meaning even S&P Capital IQ appears to be underreporting Ecobank’s market capitalization.

Now, this becomes a serious issue if @ngxgrp is not accurately reporting something as fundamental as outstanding shares. Market capitalization is one of the most basic valuation metrics investors rely on daily. If discrepancies of this magnitude exist, then it raises broader questions around data integrity and market transparency.

What does this mean for the future of our market if basic company information is either underreported or overstated? This is 2026; these are issues we should have moved past long ago. It honestly breaks my heart because these were part of the same structural issues that contributed to market inefficiencies during the 2007/2008 era.

And Ecobank is not even the only example. Even @ngxgrp previously had issues with the reporting of its own outstanding shares at some point (although I do not know if that has now been rectified).

This is why I always encourage investors to scrutinize everything. It is not just about making money. It is also about ensuring our market institutions uphold accuracy, transparency, and investor confidence.

I drop my pen here.

Dear @WorldBankGroup

STOP GIVING NIGERIA FRESH LOANS!

STOP GIVING NIGERIA FRESH LOANS!

STOP GIVING NIGERIA FRESH LOANS!

STOP GIVING NIGERIA FRESH LOANS!

STOP GIVING NIGERIA FRESH LOANS!

You already approved a whopping total of $9.35 billion in loans & credits between June 2023 & May 2026 for the BAT administration

Enough is enough! Add your voice & repost this until The World Bank does the needful. 💔💔

Minimum wage cannot do full tank but your president is seeking reelection and he is the favorite to win. Nigerians are very comfortable with bad governance.

Highlights from the Inaugural #FSDHInvestorsConference2026

Stronger markets are built on confidence, liquidity, and participation.

At FSDH Capital, we’re focused on turning insight into action by guiding capital to support sustainable growth.

#CapitalMarkets#CoCreatingTheFuture