Andrew Mckee는 2026년 3월부터 이미 $sive Photonics의 부문장이 아니었다.

아래 기사는 2026년 3월에 뜬 2개의 기사인데,

두 기사 모두에 'Alex McCann, Managing Director for Sivers' Photonics business' 라고 써있음.

즉, Andrew Mckee는 그냥 $sive 직원인 거..

I currently hold shares in the million range, so not quite sure what’s with these accusations.

Since I believe $SIVE is one of the most important laser companies in the next optical shift… and has immense TAM expansion potential with IP acquisition.

Nasdaq listing is coming up… volume ramp is coming up… I think I’m fine and know what I’m holding

Everyone's panicking about $SIVE "the head of Sivers Photonics selling his entire position."

I find it unreal the amount of manipulation the retail investor has been facing the past two weeks.

I checked the primary sources. The story falls apart.

1. Andrew McKee wasn't the division head anymore.

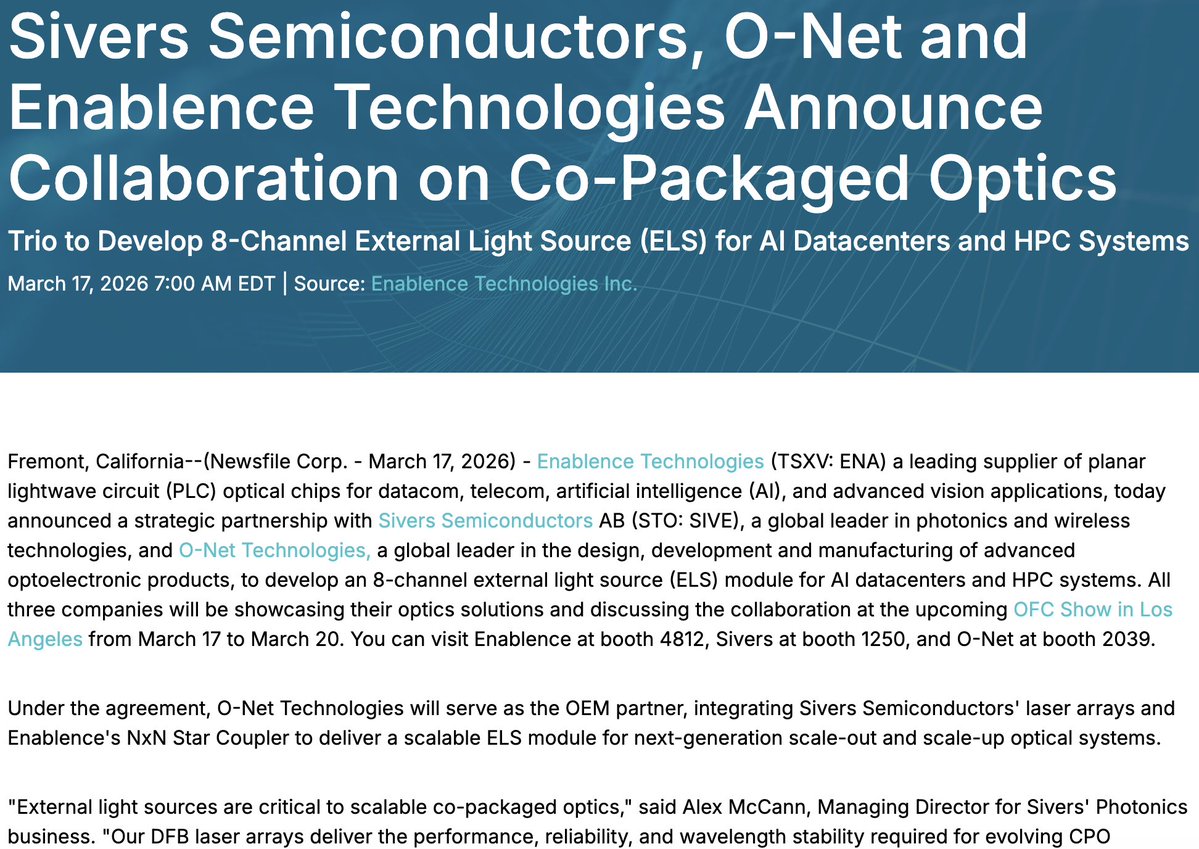

Andrew McKee was replaced as MD Photonics by Alex McCann confirmed by name in Sivers' own press releases since March 2026 (the LiDAR announcement, the O-Net/Enablence ELS deal, and the Jabil 1.6T collaboration).

McKee’s sells his position (half in Q1, rest in Q2) line up with a completed leadership transition standard for a long-time exec stepping back, not a current division head dumping ahead of disaster.

So, my question is McCann has been Managing director since March. Why do we have Andrew McKee as MD in the headlines and that he sold all his shares. What's his part in the company now?? Scumbags.

2. Look who actually runs photonics now.

Alex McCann helped execute Dialog Semiconductor's $6B sale to Renesas, was COO of Linear Technology through its $14B sale to Analog Devices, and is currently a Semiconductor Partner at Alexa Capital an M&A advisory firm.

3. The board changes fit the same pattern.

Founding investors Erik Fallström and Keith Halsey and retiring Vice Chairman Tomas Duffy stepped off. In came Joakim Nideborn Ericsson's former Head of M&A as Vice Chairman, plus Helena Svancar (international expansion).

Early founder capital out. Scale-and-transaction operators in. Right as a 700M SEK raise funds the HVM ramp.

4. Now consider the source of the bear case.

Nearly every bearish claim traces back to ONE source:

Ningi Research. Who is Ningi?

An anonymous short seller no office, no named team, no track record page. Germany's BaFin previously criticized them for publishing anonymous investment advice. Their disclaimer openly states they may close their short position immediately after publishing, without telling anyone.

Their record is mixed, not elite. Their biggest Swedish target before this Sinch, also accused of "suspicious accounting" initially dropped, then finished UP 17% after the company rebutted them point by point. Oddity Tech rejected their report as "demonstrable factual inaccuracies." Arbor Realty called their work "false and inflammatory."

And their SIVE accounting claim? It centers on a restatement Sivers had already disclosed and explained on April 24 five weeks BEFORE Ningi's June 1 report. They reframed pre-disclosed information as a scandal.

They're short SIVE. They profit when it falls. Every post is bearish by design.

I know a lot of $SIVE investors were panicking on X today. I hope they now can realize that a lot of people are against this stock for no reason. The amount of BS headlines I've been seeing just to manipulate the price action of the stock is crazy. I hope the retail investors get to take advantage of this current dip.

Let's See What's Ahead 😉

Big Big Big S/O to @Sofigoodboy for the article link.

Nothing like an internal $META memo getting published.

Showing AI ramping as usual:

- LTAs signed with Samsung and $SNDK for memory

- LTAs signed with Sumitomo Electric for fiber optics

- Expected to deploy 7GW compute infra this year, and doubling in 2027.

- as much as $145B capex spend this year

“It plans to launch a chip about every six months through 2027”

$NBIS Co-Founder Roman Chernin just spoke.

- On AI growth: We think the most growth is still ahead of us. The reason: AI adoption is still just taking off. Most cases still need to be solved. From technology perspective we only just now seeing the model being capable to solve enterprise problems. We only see now the what it can do in the business.

- On demand: The huge part part is coming from a limited number of the players (read Hyperscalers). Between 50/70% of the total demand. He calls $META and $GOOGL by name. The other 30% are smaller labs who build specialised models but we also see product companies (enterprises). They start from the application and are now starting to build their own models.

- On enterprise demand: Not much enterprise demand with 2 exceptions: -1 Revolut for example: they are digital by native and very technical, they invest very much in AI and grow very hard, others in this category Booking and Shopify. -2. fintec companies like janestreet also do a lot in AI. But if we put these 2 aside, the real enterprise adoption has not really started yet.

- On the layers: First layer is physical infrastructure, bare metal, we have a few customers who only want this layer. Second layer is cloud. This is the layer where most of the current demand is sitting. Any lab or team that does some training, they want to have reliable infrastructure but want the development to do themselves. Third layer that Nebius build is the infrastructure. Most enterprises just want to build applications on top of this layer. Revolut for example, most enterprises want to outsource this layer. They don’t need to own the infrastructure, they just want to build their apps on top.

- On paying for valuation: Nebius builds a product integrated downstack and upstack. They control the hardware and control the software. New consumption will come on the new layer. Enterprises don’t want to be an expert. They just want to use the tokens without locked by choosing which models. A platform that will choose which model is good for that outcome. Enterprises don’t want to pay for tokens or hardware but for the outcome. Users don’t care about how many hours of gpu they used or how many tokens.

- On deepseek: it creates a lot of panic in public markets but it’s really creating the next wave of development.

- On open source models: The open source models are catching up to some level and can already solve a lot of problems. Think about enterprise, you have very specific tasks in a specific environment. It’s an unlocking factor, how trainable are this models. The industry is figuring out how to tune the models, if they can, the adoption will start. Open source is the start but in the end you have post trained models that bring the value of the very specific knowledge of this specific enterprise. You get similar results somilar cheaper but often you have better results bacause you can inject your info safely.

TRIGGER ALERT

On a podcast yesterday $WULF CFO admitted to getting triggered by this "model".

It's worth reading his full response:

"You just triggered something, so I'm going to go there on this. I just saw, Jim Chanos, who when I was growing up in finance, he was a king. I started in the business in 2000 and he was around and one of the early short-sellers. He just put out some nonsense on us last night. I read it and I was like, you're an idiot. And by the way, if you want to be short our stock god bless you, but at least call me up so I can tell you what you're doing wrong in your model because it literally is nonsense.

And so one of the things he did on the model, which has triggered this, is that he's modeling maintenance capex of $1-1.5M/MW. On an annual basis! I looked at his model and he has $8B D&A on a $4.4B build.

Hey genius! The last time I checked the tax code you can only depreciate about 80%, not even the full amount. [The asset] costs us $4.4B, about 80% is depreciable. So, where the hell are you coming up with $8b of D&A? And I think it's because he's assuming another $1-1.5M of maintenance capex. Which by the way is ridiculous.

So, let's just level set on that point: I build the shell the and the power and water to the rack. I don't do anything else, that's it. So, to your question, what happens if the technology changes, that's my tenant's issue. It's their rack that they put together with their integrator: Dell, Supermicro idk. I provide power and water for 99.999% of the time. What about maintenance capex? If the technology changes in 3-5 years that's on the tenant. I'm still providing electricity and water.

You're telling me on a $10M per MW data center build, I am going to spend $1-1.5M/MW on maintenance capex, oh and by the way I hope he listens to this.

Jim, pick up the phone and call me bro. My phone number is out there or you can email me.

But stuff like this, it reminds me: back in Bitcoin mining days I had a NY Times reporter reached out to me who wanted to do a story on our facility at Lake Mariner. I got on the phone and what I found was an ignorant person who didnt want to understand why they were wrong about what they were reporting. They literally didn't care that what they were writing was wrong; they just wanted to sell eyeballs.

Which basically is what Jim Chanos just did, and I lost all respect. This was a guy I held in high regard. You're wasting my time and just trying to sell eyeballs and that kind of stuff really bothers me, so sorry to get triggered on it. If you want to learn something, pick up the phone and call me."

$WULF +11% this morning

$IREN: Nvidia DSX OS

Thanks to @TheTechInvest for posting this clip of RAISE Summit. Starting at 9:10, Nvidia and Mirantis representatives talk about how $IREN will be the first adopter of Nvidia DSX OS which is an Open Source AI Cloud Platform with Nvidia Orchestration made available through integrating Nvidia APIs.

This seems to signal that $IREN's SW1 Campus is going to be the first Nvidia DSX site serving enterprises and possibly sovereign compute.

Open source will be open source of the whole stack from the Nemotron Model down to the Orchestration layer. People ask why I'm with IREN being mediocre at software, well it's because Nvidia will have DSX OS.

🚨BREAKING🚨

Are you the next hyperscaler?

$IREN CCO Kent Draper

It’s absolutely attainable. We have built that foundation.

*Nearly 6GW gives you just a glimpse of the big picture and the insane potential for this $$15B company.

RAISE Day 1 Summary $IREN:

‣ Horizon 1 handover confirmed 19th July

‣ Commisioning H2

‣ MSFT very happy with IREN so far, very hands off. Great partners.

‣ IREN on call with NVDA basically everyday

‣ Deals signed today are even better than 2 months ago.

‣ Pre payments sweetspot now between 25-40 roughly. Some even offering 100%

‣ IREN GB300 NVIDIA EXEMPLAR Cloud certified. Likely announced next week. Only THREE have this right now.

‣ IREN selected with small number for VERA rubin for testing VERY SOON. Unofficially late EOY mass production. Likely early 2027

‣ H5-H6, Sweetwater 1 Vera Rubin

‣ Mirantis deal closing this month is the aim

‣ Semi conductor shortage micron $MU seeing into 2031

h/t: @FinGigawatt

https://t.co/Rx84G8EYzc

$META will invest about $10B to build its first data center in Canada, a 1GW facility in Sturgeon County, Alberta, largely powered by natural gas. The project is expected to need 3,000 construction workers and create 300 full-time jobs.

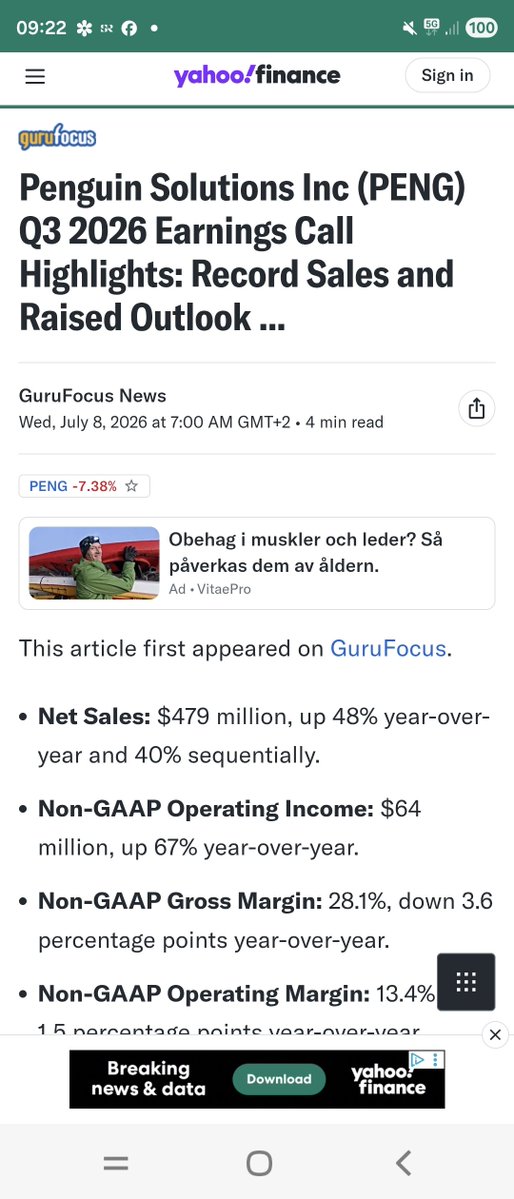

$PENG earnings blowout is critical evidence confirming that the AI super cycle is shifting from a speculative infrastructure build to a sustainable deployment and optimization phase.

Ayar Labs is the CPO connection that could take $SIVE from $1B to $5 to $7.5B market cap on its own.

I'll explain.

Ayar Labs makes a product called the SuperNova. It is a light source module that powers their optical engine inside AI datacenters. Every single SuperNova unit contains Sivers laser arrays inside it.

Think of it like this. Ayar makes the lamp. $SIVE makes the bulb that goes inside every single lamp they ship.

Now here is where it gets interesting.

Some Wall Street CPO models assume only a few dozen external light sources per rack.

$JBL already built a single box housing 64 SuperNova modules. That is 64 Sivers laser modules inside one box that fits in a server rack.

Then at Computex 2026 Ayar and Wiwynn demonstrated a rack-scale AI architecture supporting up to 512 SuperNova light source assemblies per rack.

If these rack-scale architectures move into hyperscale production, analysts may need to revisit their assumptions around external light source density entirely.

Now the math on how we get to $5 to $7.5B.

Assuming approximately $60 to $65 of Sivers laser content per SuperNova assembly, large scale deployment could translate into hundreds of millions of dollars of annual laser revenue over time.

If Ayar alone ultimately generated roughly $500M of annual revenue for Sivers, and the market valued that business at 10 to 15 times sales, that implies a potential valuation of approximately $5 to $7.5B.

This is one scenario showing how powerful the Ayar relationship could become if CPO adoption reaches scale.

$SIVE sits at roughly $1B today.

From one connection. Not $GFS. Not $AAPL. Not $POET.

Just Ayar.

When I first started investing in robotics, I searched X and YouTube for Humanoid Robotics experts and @GoingBallistic5’s content kept popping up

Scott is an encyclopedia on all facets of the space and has been an instrumental player in the space for 40+ years. Follow him unless you’re afraid of learning too much

The $MU memory cycle is over and the bubble is popping.

At least that's what the market is pricing after a 25% crash in two weeks. There's just one problem: the "bubble" is sold out for the next two years.

Two weeks ago $MU printed one of the greatest quarters in semiconductor history: $41B in revenue, up 345% YoY, 85% margins, and guidance for $50B next quarter. The stock made new ATHs at 1259... then gave back 300 points on cycle fears.

But this isn't the old Micron; 16 take or pay contracts with binding price floors and $22B in customer deposits mean customers pay whether they take delivery or not. Management says margins at FLOOR pricing would still exceed past peak margins. Bears are trading the 2018 playbook against a company that rewrote the rules.

The chart is now backtesting the exact zone that launched the last leg. 966 was the breakout level; $MU sits just under it at 938 with monthly support at 810 below. Reclaim 966 and hold, and 1100 comes fast. Thru 1100 and the ATH retest at 1259 is in play. Break 1259 and the 1500 melt up thesis is fully alive again.

HBM4 Is the Inflection

$MU was just approved as an HBM4 supplier for $NVDA's Vera Rubin platform with shipments starting this half. HBM4 revenue already crossed $1B and the ramp is moving 2x faster than HBM3E did. Micron now sees the HBM market topping $100B by 2027 (a year earlier than projected). First wafers from its new $9.3B Japan fab came off the line on July 4, and fresh supply deals with Ford and GM keep widening the demand base.

Trade Ideas

$MU above 966

Swing Trade: MU 8/21 1500C

Day Trade: MU 7/10 1000C

The market is pricing the death of the old memory cycle. It hasn't noticed the new one has a floor under it. When it does, the reclaim will be violent.

$IREN at @RaiseSummit

Kent Draper: 3 layers of AI compute

1. Physical Infrastructure

2. Compute

3. Software & Services

Layers 1 and 2 are the key foundation, without those, your ceiling is capped.

I have been pounding the table on the superior model of a bottom-up approach.

@kentpdraper confirms that @IREN_Ltd sees it the same.

Having a strong foundation of land, power, grid connections, substations, owned GPUs, network core buildings, and storage, will unlock the amount of GPU hours that can be monetized up the stack.

It's very simple: with an abundance of physical infrastructure and chips — software is the layer that can be added when needed.

The foundation of the thesis rests on physical assets and power being scarce, and those are the limiting factors in your ability to grow faster than peers.

$AAPL and $AVGO announced a $30B+ multiyear deal for custom silicon and wireless technology used across Apple products.

The deal includes more than 15B U.S.-made chips and a $1.5B Broadcom investment to expand its Colorado facility.

AI infra/neocloud selloff summarized:

> Bloomberg floated the idea of $META selling excess compute

> Retail sells off neocloud & AI infra

(Names like $NBIS, $IREN, $CIFR, $WULF, and many others take a huge hit)

> Institutions start buying tech & AI stocks at the fastest pace since last October

(Most definitely because they realize $META has absolutely zero excess compute)

> $META & Bloomberg does damage control and starts to change their narrative

IMO, in the coming days:

> We start to bottom out

> Institutions got in at lows

> And retail regrets selling

![matthew_sigel's tweet photo. TRIGGER ALERT

On a podcast yesterday $WULF CFO admitted to getting triggered by this "model".

It's worth reading his full response:

"You just triggered something, so I'm going to go there on this. I just saw, Jim Chanos, who when I was growing up in finance, he was a king. I started in the business in 2000 and he was around and one of the early short-sellers. He just put out some nonsense on us last night. I read it and I was like, you're an idiot. And by the way, if you want to be short our stock god bless you, but at least call me up so I can tell you what you're doing wrong in your model because it literally is nonsense.

And so one of the things he did on the model, which has triggered this, is that he's modeling maintenance capex of $1-1.5M/MW. On an annual basis! I looked at his model and he has $8B D&A on a $4.4B build.

Hey genius! The last time I checked the tax code you can only depreciate about 80%, not even the full amount. [The asset] costs us $4.4B, about 80% is depreciable. So, where the hell are you coming up with $8b of D&A? And I think it's because he's assuming another $1-1.5M of maintenance capex. Which by the way is ridiculous.

So, let's just level set on that point: I build the shell the and the power and water to the rack. I don't do anything else, that's it. So, to your question, what happens if the technology changes, that's my tenant's issue. It's their rack that they put together with their integrator: Dell, Supermicro idk. I provide power and water for 99.999% of the time. What about maintenance capex? If the technology changes in 3-5 years that's on the tenant. I'm still providing electricity and water.

You're telling me on a $10M per MW data center build, I am going to spend $1-1.5M/MW on maintenance capex, oh and by the way I hope he listens to this.

Jim, pick up the phone and call me bro. My phone number is out there or you can email me.

But stuff like this, it reminds me: back in Bitcoin mining days I had a NY Times reporter reached out to me who wanted to do a story on our facility at Lake Mariner. I got on the phone and what I found was an ignorant person who didnt want to understand why they were wrong about what they were reporting. They literally didn't care that what they were writing was wrong; they just wanted to sell eyeballs.

Which basically is what Jim Chanos just did, and I lost all respect. This was a guy I held in high regard. You're wasting my time and just trying to sell eyeballs and that kind of stuff really bothers me, so sorry to get triggered on it. If you want to learn something, pick up the phone and call me."

$WULF +11% this morning](https://pbs.twimg.com/media/HMtdEEnXQAECHmz.png)