On the one hand: a lot of this is probably generic clickfarm rage bait designed to generate engagement $ by shit-stirring on a hot issue

On the other: this is such an obvious and easy win for foreign intelligence services that it’s almost self-evident they’re behind some of it

Arizona’s largest utility is proposing a 45% electricity-rate increase for data centers and a 14.5% hike for households. No one is happy. https://t.co/MCZ7OJUG6L

Arizona's biggest utility, APS, wants a 45% rate hike on data centers and ~14.5% on households and everyone is pissed!

Latest example in the battleground of who pays for the AI power build-out. APS calls it out as paying for growth vs. Microsoft claiming it already covers its own upgrades and wants to build its own generation.

APS is connecting 4,000+ MW of new large load with another 19,000 MW queued, >2x current system peak.

The AG Kris Mayes claims the hike of even 45% won't cover the cost and wants residential hikes limited to near 3%.

Core local concern is if AI development slows down, households amortize infrastructure built for load that never showed and have been burned on prior RE cycles.

This is why utilities are making tech companies sign 20 year take or pays if they want a lot of power!

$NVDA CEO: Software isn't dead

"And we're working with so many companies: Cadence and CrowdStrike, and also Palantir, SAP, and ServiceNow. People always said, 'Jensen, the agents are going to disrupt these markets.' I said completely the opposite. And you can now see it. Agents are going to create the largest opportunity ever for my partners and friends."

The data center industry is being rewritten in real time.

On the latest @NomadFuturist Podcast, Peter Gross explores AI-driven infrastructure, power strain, and why the industry is facing a structural reset — not gradual change.

🎧 Listen: https://t.co/aHMC1DG6EV

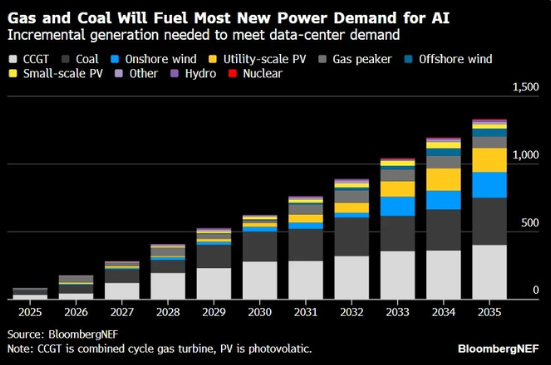

🚨BloombergNEF just dropped a reality check on AI's power needs: Gas and coal will fuel most new generation for data centers through 2035.

No green fairy dust here, just hard numbers on incremental generation required. CCGT and coal dominate the stacked bars, renewables and nuclear barely move the needle.

AI will run on natural gas and coal for the foreseeable future.

But here’s where the rubber meets the (slow-moving) regulatory road:

Where do all the CCGTs come from?

•Major manufacturers (GE Vernova, Siemens Energy, Mitsubishi) are booked solid with 4–5+ year backlogs. GE alone is at ~100 GW and growing; new orders are already slipping into 2029–2030.

•Data-center hyperscalers are paying non-refundable deposits years in advance just to hold a slot. Supply chain can’t scale fast enough.

Where does all that new coal generation come from?

•U.S. permitting and EPA rules have made new coal plants virtually impossible for over a decade.

•Strict emissions standards, carbon-capture mandates that don’t exist at scale, endless lawsuits, and local opposition = de facto moratorium. Retirements continue while new builds are DOA.

Can the U.S. compete with China in the AI race without a sea change in permitting & policy?

•China added the equivalent of the entire U.S. power grid in just four years, including massive new coal and gas capacity with lightning-fast approvals.

•Beijing’s “AI-Energy” strategy treats power as national security. America’s grid is aging, interconnection queues are years long, and bureaucracy is the real bottleneck.

•Without radical permitting reform, China is structurally positioned to pull ahead on the energy foundation that powers AI compute.

The BNEF chart doesn’t lie. The question is whether U.S. policy will let us actually build what the chart demands.

As always, Energy reality trumps green rhetoric. AI supremacy depends on it.

#AI #DataCenters #CCGT #NaturalGas #Coal #energyreality

Homebuyer demand remained near record lows to close out April.

With Reventure's buyer demand index downshifting to 9/100 this month.

For comparison: a 50/100 is "normal", and the current readings are near the lowest on record.

Suggesting that the spring 2026 season will continue to be a difficult one for sellers and buyers.

Lower prices is the quickest and fastest way out of this prolonged housing depression. Markets where prices have fallen are seeing an improvement in demand; everywhere else is still stagnating.

To track the demand metrics in your market, download our app and search your ZIP: https://t.co/pLvj026xCj

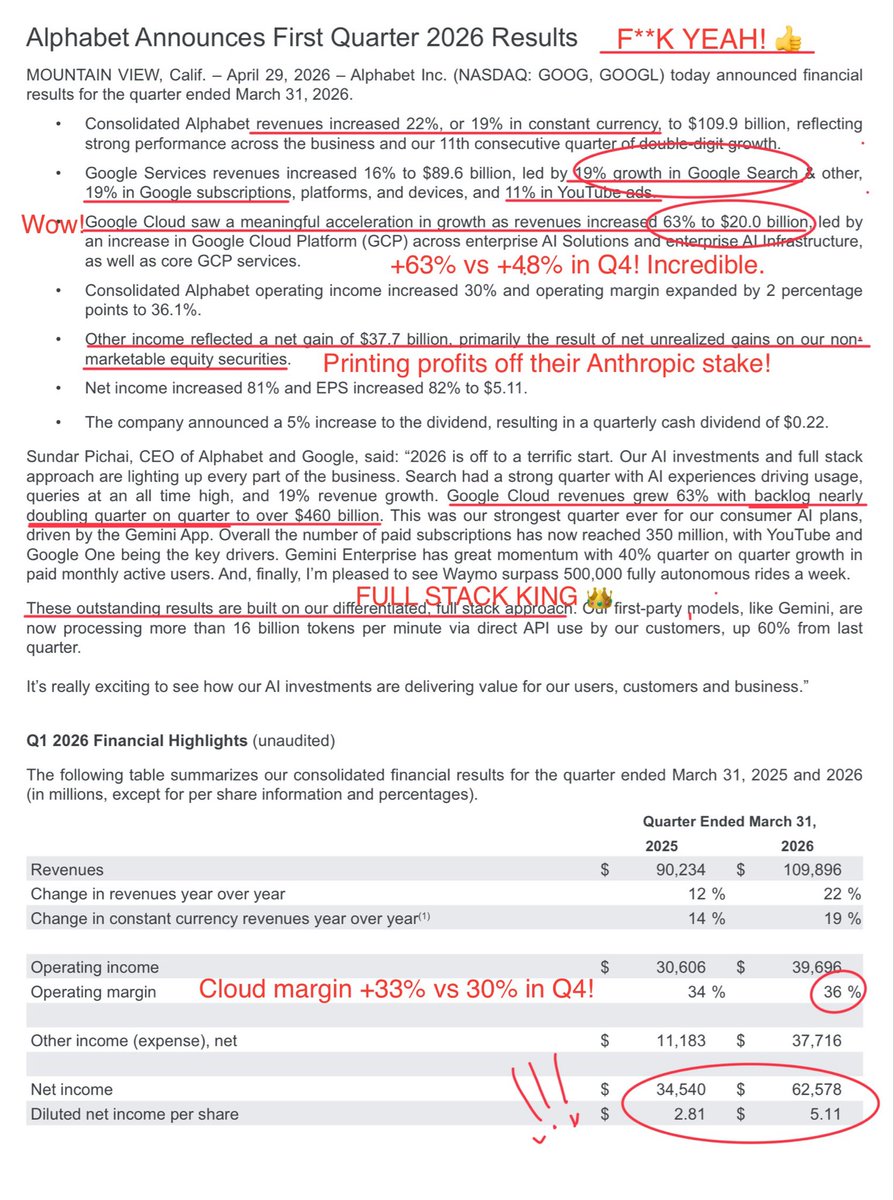

The $GOOG numbers were absolutely MIND-BLOWING.

Revenue +22%. Cloud +63% (WTF???) up from +48% in Q4, with record margin at 33% despite huge capex. Search accelerated yet again to +19%. The opposite of dead! Total Op margin at 36.1% (+200bps) = staying lean!

Just STUNNING. 🤯

$META CFO ups the capex:

"We anticipate 2026 capital expenditures, including principal payments on finance leases, to be in the range of $125-145 billion, increased from our prior range of $115-135 billion. This reflects our expectations for higher component pricing this year and, to a lesser extent, additional data center costs to support future year capacity."

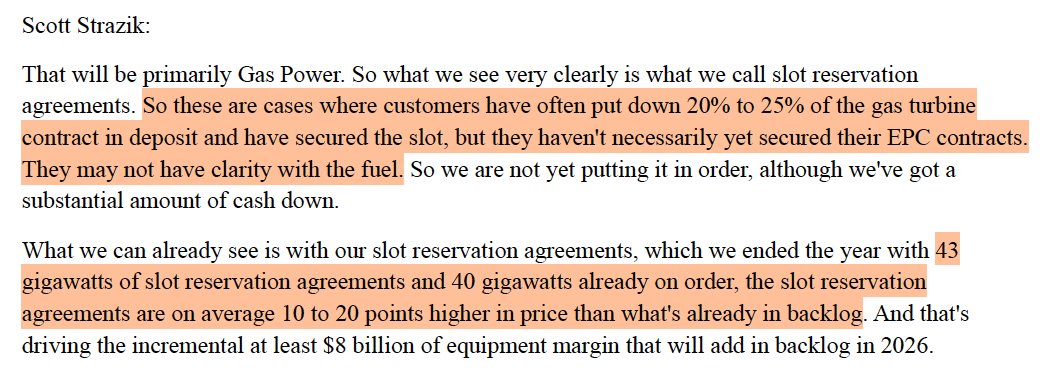

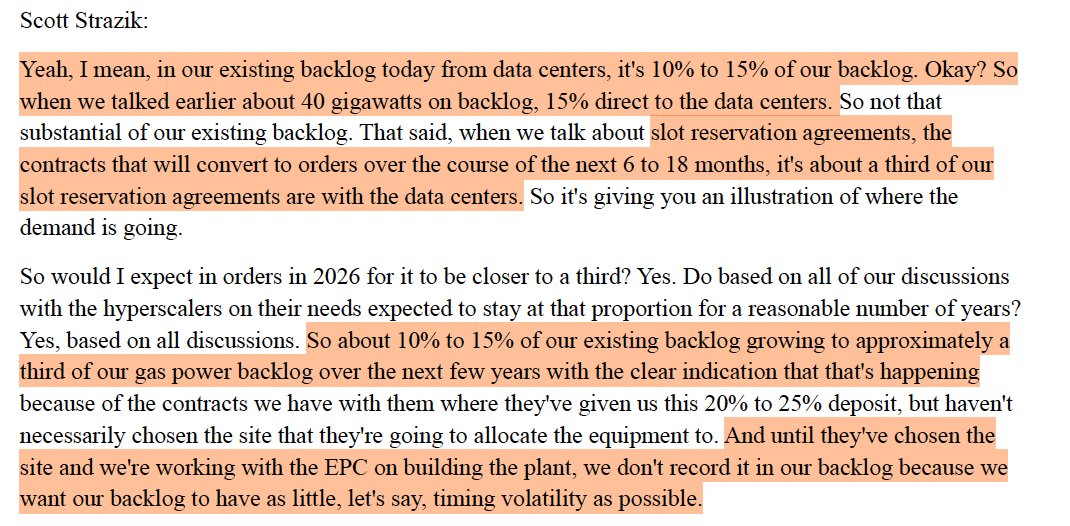

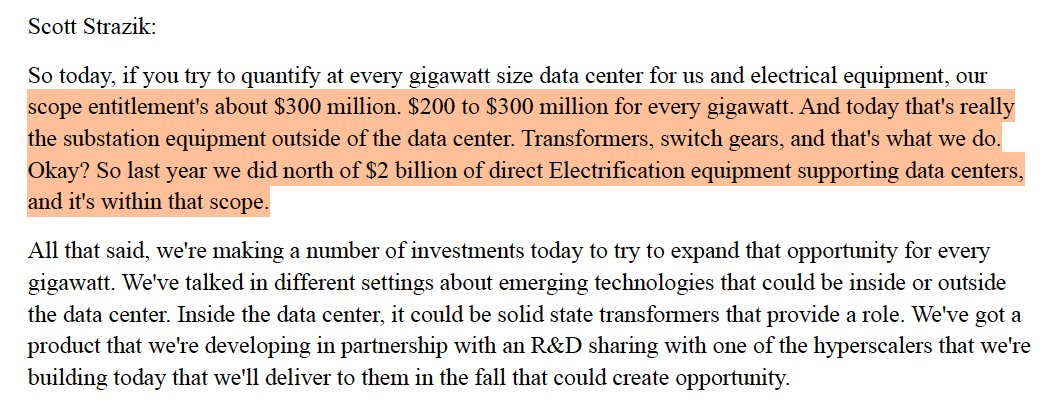

Interesting numbers here in this interview of GE Vernova's CEO on gas turbine reservations >> orders

- Ended 2025 with 43 GW of "slot reservations" (33% direct to data centers), 40 GW already on order (15% direct to data centers)

- Customers putting down 20-25% deposits on reservations but don't have EPC/fuel secured (next bottleneck!) so not yet 'orders'

- Reservations now through to 2031! Can't get shipped though until 2029, shipping 4 GW/quarter

- Converting from Reservation to Order taking 6-18 months because of EPC/fuel issues

- GE can build 20 GW/yr simple cycle now, up to 24 GW/yr by 2028, adding more shifts + capacity in SC plant, France

- Note 24GW/yr simple cycle could theoretically equate to about 35 GW of NGCC/yr from GEV alone

- 50% of gas commitments are in the U.S.

- GEV also doing great business outside of turbines on switchgear, transformers, substation equipment - $200-300M for every 1 GW of data center load just on that