🚨 Early $GOOGL & $META investor Roger McNamee:

“AI is not a small bubble. It’s a humongous bubble.”

“$1.4T has already been spent trying to build a general-purpose technology, which will never happen.”

“OpenAI, Anthropic, Meta, Google, Microsoft, Amazon & SpaceX are all competing for the same 2 spots in the AI marketplace.”

“There is no moat. They all have the same technology and are competing for the same customer.”

“How do you think that’s going to end?”

His full investment thesis:👇

🚨 Peter Thiel, co-founder of $PLTR:

“Stop focusing on $META, OpenAI & Anthropic.”

“The only company making money in the AI race is $NVDA.”

“Everyone else is losing money.”

Investors are looking in the wrong place.

$WDH

A Chinese scam?

Or one of the cheapest profitable AI growth companies in the market?

This isn’t another cash-burning China story.

Watch for volume and keep eyes, not my favorite setup but an interesting one.

It’s becoming an AI-native insurance and healthcare platform.

And I still believe many of those are only getting started.

Now I’m watching $WDH.

Look at $LMND, $OSCR, $HUIZ, and even $PLTR for the blueprint.

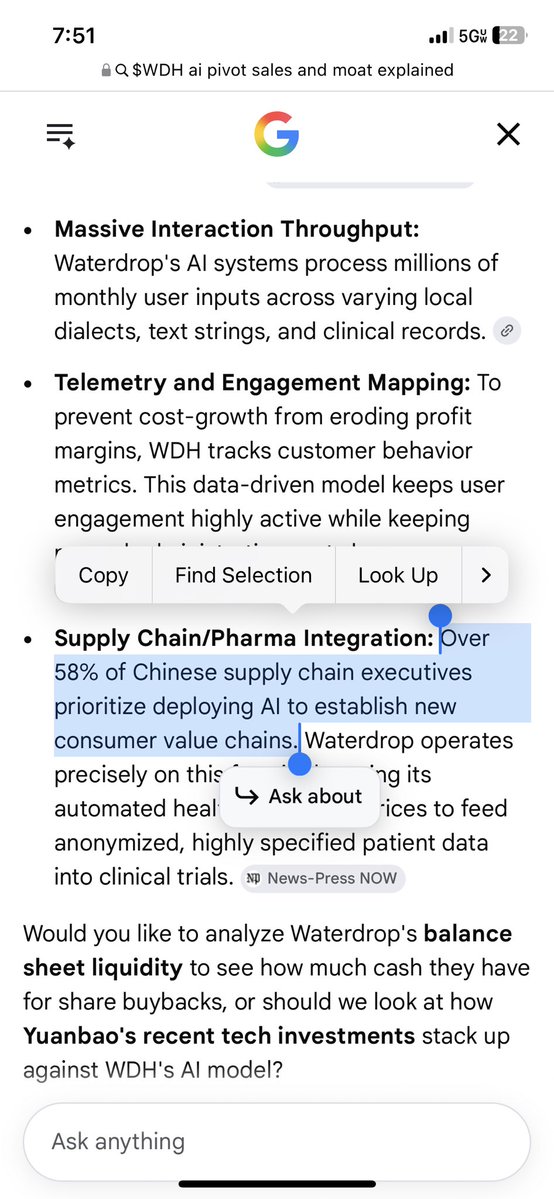

Unlike traditional insurers that carry underwriting risk, Waterdrop operates an asset-light AI-powered insurance marketplace, technical services platform, medical crowdfunding ecosystem, and digital clinical trials network.

Every customer strengthens the data.

Every interaction improves the AI.

Every product expands the ecosystem.

Its business is built around:

• AI-powered insurance marketplace

• Technical services for insurers

• Medical crowdfunding

• Digital clinical trial recruitment

• AI underwriting & risk analytics

This creates multiple recurring revenue streams while requiring far less capital than traditional insurance carriers.

The AI opportunity may be even bigger.

Management is transforming Waterdrop into an AI-native company.

Already deployed:

• AI Insurance Expert

• https://t.co/U3QbObGrQV underwriting assistant

• Claw Copilot CRM

• AI-powered risk screening

• Intelligent recommendations

• 75+ LLM patent applications

• 100+ AI-related patents

Unlike many AI stories…

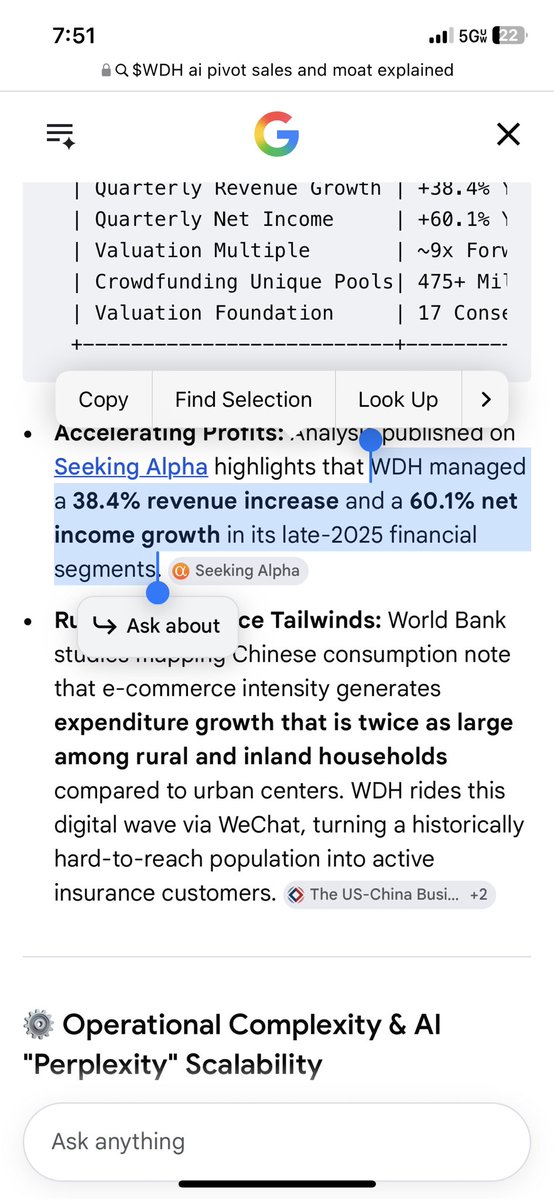

Management is already producing measurable results.

• AI Insurance Expert increased facilitated premiums 17.7% QoQ.

• AI generated roughly RMB 87M of incremental insurance premiums in Q1 alone.

• Technical services revenue exploded as AI underwriting, CRM, and analytics adoption accelerated.

This isn’t experimental AI.

It’s already driving revenue growth.

The moat may be even larger.

Waterdrop has quietly built one of China’s largest healthcare data ecosystems.

Current platform scale:

• 494M cumulative donors

• RMB 73.5B raised

• 3.75M patients helped

• 243+ pharma & CRO partners

• 15,500+ patients matched across 1,700+ clinical trials

That creates proprietary healthcare and insurance data that becomes more valuable as AI improves.

Global demand continues accelerating.

China remains one of the world’s largest underinsured markets.

Long-term tailwinds include:

• Aging population

• Rising healthcare costs

• Low insurance penetration

• Rapid digital insurance adoption

• AI-driven underwriting

• Expanding biotech & clinical trial demand

Growth has accelerated dramatically.

Recent results:

• FY2025 Revenue: ~$569M (+~50%)

• FY2025 Net Income: ~$81M

• Q1 2026 Revenue: +64.8%

• Insurance Revenue: +74.1%

• 17 consecutive profitable quarters

• ~$400M+ cash & short-term investments

Shareholders continue getting rewarded.

• ~$120M returned through buybacks

• Cash dividend

• Enterprise value remains remarkably low after adjusting for cash

One screen that caught my attention:

$PLTR

$CELH

$WDH

All currently meet:

• Revenue growth above 50%

• Gross margins above 50%

• Positive EBITDA

• Positive EBIT

• Operating income growth above 50%

• Gross profit growth above 90%

• Revenue above $600M

• Current assets above $700M

• Profit margins above 5%

• Less than 30% above 52-week lows

Upcoming catalysts:

• AI rollout across every business

• Technical services expansion

• Insurance penetration growth

• Clinical trial platform expansion

• Additional pharma partnerships

• Continued buybacks & dividends

• 2026 earnings acceleration

The risks are obvious.

China ADR sentiment.

Regulation.

Currency.

Competition.

Marketing ROI.

But if execution continues and sentiment toward Chinese equities improves…

Sometimes the market prices a company like it’s going out of business.

$WDH is acting like it’s just getting started.

Not financial advice. Always do your own research.

$ALIT

I have the daughter at work with me today, so the DD isn’t as deep.

Still…

Go look at the weekly volume.

Worth watching. Not my favorite but keep eyes

The recent reverse split grabbed attention, but the volume isn’t just split-related. Institutional activity has started picking up while the business continues working through a turnaround.

This isn’t a momentum stock.

It’s a beaten-down enterprise software company trading as a turnaround with meaningful AI optionality.

Alight isn’t competing with $ORCL, $WDAY, $ADP, or $PAYX.

It’s helping power them.

Alight provides cloud-based benefits administration, healthcare navigation, wealth management, leave administration, and HR solutions for many of the world’s largest employers through its Alight Worklife platform.

This is one of the largest pure-play benefits administration companies globally.

The company remains financially solid despite slower sales.

• Q1 2026 revenue: $534M.

• Approximately $2.25B annual revenue.

• 93% recurring revenue ($498M in Q1).

• Nearly $2B of contracted recurring revenue.

• Operating cash flow: $79M.

• Free cash flow: $53M (+20% YoY).

• More than $500M liquidity.

• Adjusted EBITDA: $104M.

The top 400 enterprise customers now represent over 90% of recurring revenue, giving management a concentrated opportunity to drive renewals, upsells, and wallet share.

Revenue has been flat to slightly lower.

Cash flow hasn’t.

This is becoming a margin expansion story rather than a hyper-growth story.

AI is becoming the biggest catalyst.

Alight’s proprietary LumenAI platform is rolling out across healthcare, wealth, leave, and benefits administration to automate complex workflows, personalize employee experiences, improve compliance, and reduce administrative costs.

The company also expanded its partnership with $IBM to integrate watsonx AI directly into the Alight Worklife platform.

Early enterprise prototypes demonstrated productivity improvements exceeding 90% on targeted workflows.

Third-party validation also matters.

Alight’s Healthcare Navigation platform was independently validated to deliver approximately $296M in claims savings for employer customers.

That’s a powerful sales tool.

Large employers care about ROI.

Not hype.

Alight also serves over 30 million employees and family members across many of the world’s largest organizations, creating one of the deepest proprietary benefits and workforce data sets in the industry.

The long-term opportunity continues growing.

AI-driven HR.

Healthcare cost management.

Benefits outsourcing.

Retirement administration.

Leave management.

Employee engagement.

Compliance automation.

Digital healthcare navigation.

Every one of these trends increases demand for outsourced, technology-enabled HR platforms.

Its niche is becoming more valuable as labor shortages, healthcare complexity, and AI automation accelerate globally.

Unlike many enterprise software names burning cash…

Alight is generating meaningful free cash flow while investing in AI.

Valuation also stands out.

Despite generating roughly $2.25B in annual sales, ALIT trades at only a fraction of revenue compared to many enterprise software peers.

The market continues assigning a discounted multiple because revenue growth has stalled.

If recurring revenue stabilizes while margins continue expanding, operating leverage could become significant.

This isn’t an AI infrastructure company.

It’s AI-enabled enterprise software with one of the highest recurring revenue mixes in the industry.

Sometimes the market overlooks mature businesses quietly improving profitability while embedding AI across mission-critical workflows.

Those can become some of the most overlooked turnaround opportunities.

$SPT

-60% past year but volume expansions seen.

Is this the farmers market? No.

DONT MISS THIS SAAS.

A premium SaaS company trading like the market has already given up on it.

Sprout Social is one of the most interesting beaten-down software names I’m watching.

This is a ~$500M market cap company generating nearly $500M in annual revenue.

A niche AI-powered social intelligence platform with enterprise customers, recurring revenue, improving margins, and a massive opportunity to become the intelligence layer behind how brands understand customers.

Now I’m watching $SPT.

Look at $BRZE, $FRSH, $PD, $PCOR, and even $CRM for the blueprint.

Unlike broad enterprise software companies, Sprout Social is a pure-play social intelligence and management platform.

Tied to Open Ai, Anthropic, and $RDDT

It helps brands publish content, manage conversations, analyze performance, monitor trends, understand sentiment, and turn billions of social signals into actionable business intelligence.

The company sits in a very specific niche:

Social media management + social customer experience + AI-powered consumer intelligence.

Sprout’s goal is becoming the intelligence layer between brands and billions of online conversations.

Its main competitors include:

$SPT vs $SPKL (Sprinklr), Hootsuite, Khoros, Brandwatch, Meltwater, Emplifi, Buffer, and other social SaaS platforms.

But Sprout occupies a unique position.

It is not trying to be the cheapest option.

It is not trying to become a massive all-in-one CX platform.

It is focused on being the premium, easy-to-use intelligence platform for brands that need enterprise-level insights without enterprise complexity.

The biggest opportunity is AI.

Sprout is building AI into the entire platform through Trellis.

Trellis is designed as an AI agent that can analyze social conversations, identify trends, understand sentiment, surface competitive intelligence, and help teams make faster decisions.

This turns Sprout from a social scheduling tool into a real-time business intelligence platform.

The future opportunity:

Every company will need to understand:

• What customers are saying

• Why sentiment is changing

• What trends are emerging

• How competitors are performing

• How AI-generated content is impacting brands

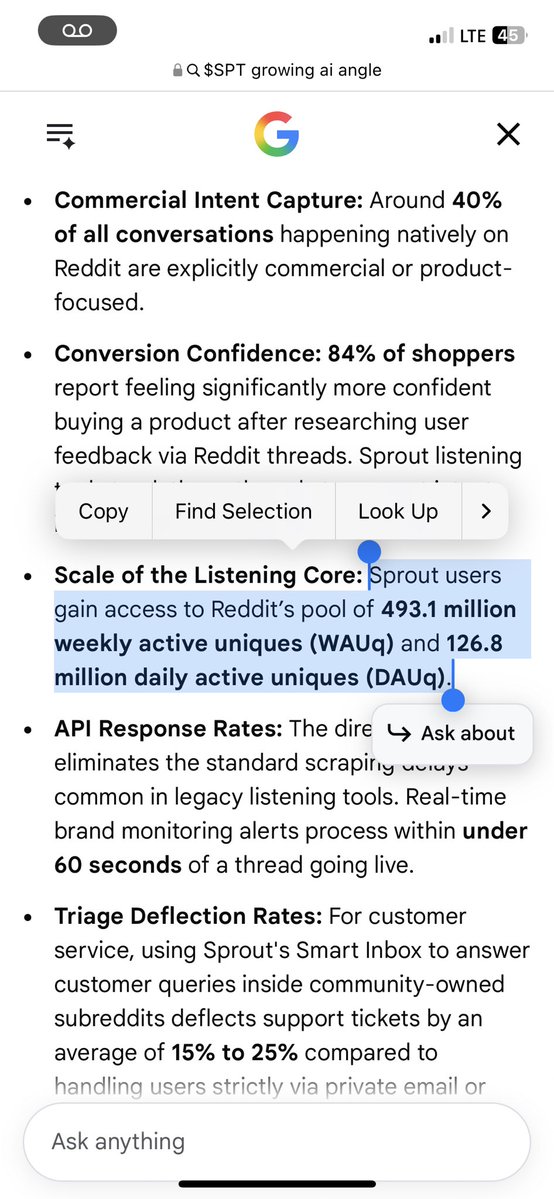

Social data is becoming one of the largest real-time datasets in the world.

The numbers:

• Market cap: ~$500M

• FY2025 Revenue: ~$457.5M (+13% YoY)

• Q1 2026 Revenue: ~$121.5M (+11% YoY)

• Subscription revenue: ~$453M annually

• Gross margins: ~77-80%

• ARR continues expanding

• ~30,000 brands using the platform

The most important growth signal:

Enterprise customers continue expanding.

Customers generating:

• $30K+ ARR: 3,803 customers (+13% YoY)

• $50K+ ARR: 2,022 customers (+18% YoY)

The $30K+ ARR customer base now drives the majority of subscription revenue.

This matters because SaaS companies re-rate when customers expand usage, contracts get larger, and revenue becomes more predictable.

Sprout is increasingly moving toward larger, higher-value enterprise relationships.

The company is also showing improving operating leverage.

Recent trends:

• Non-GAAP operating margins improving

• Operating expenses growing slower than revenue

• Strong gross margins

• Improving free cash flow profile

• Continued focus on efficiency

The valuation is where this gets interesting.

Comparable SaaS companies:

$BRZE: ~$3B market cap

$FRSH: ~$3B market cap

$PD: multi-billion market cap

$PCOR: ~$6B+ market cap

Sprout:

~$500M market cap.

The upside case is the market begins viewing it as an AI-enabled social intelligence platform with enterprise expansion.

The AI opportunity could become the catalyst.

But the setup is interesting.

$SPT may be one of the more underfollowed ways to invest in AI-powered customer intelligence, social analytics, and enterprise SaaS recovery.

That combination is worth watching.

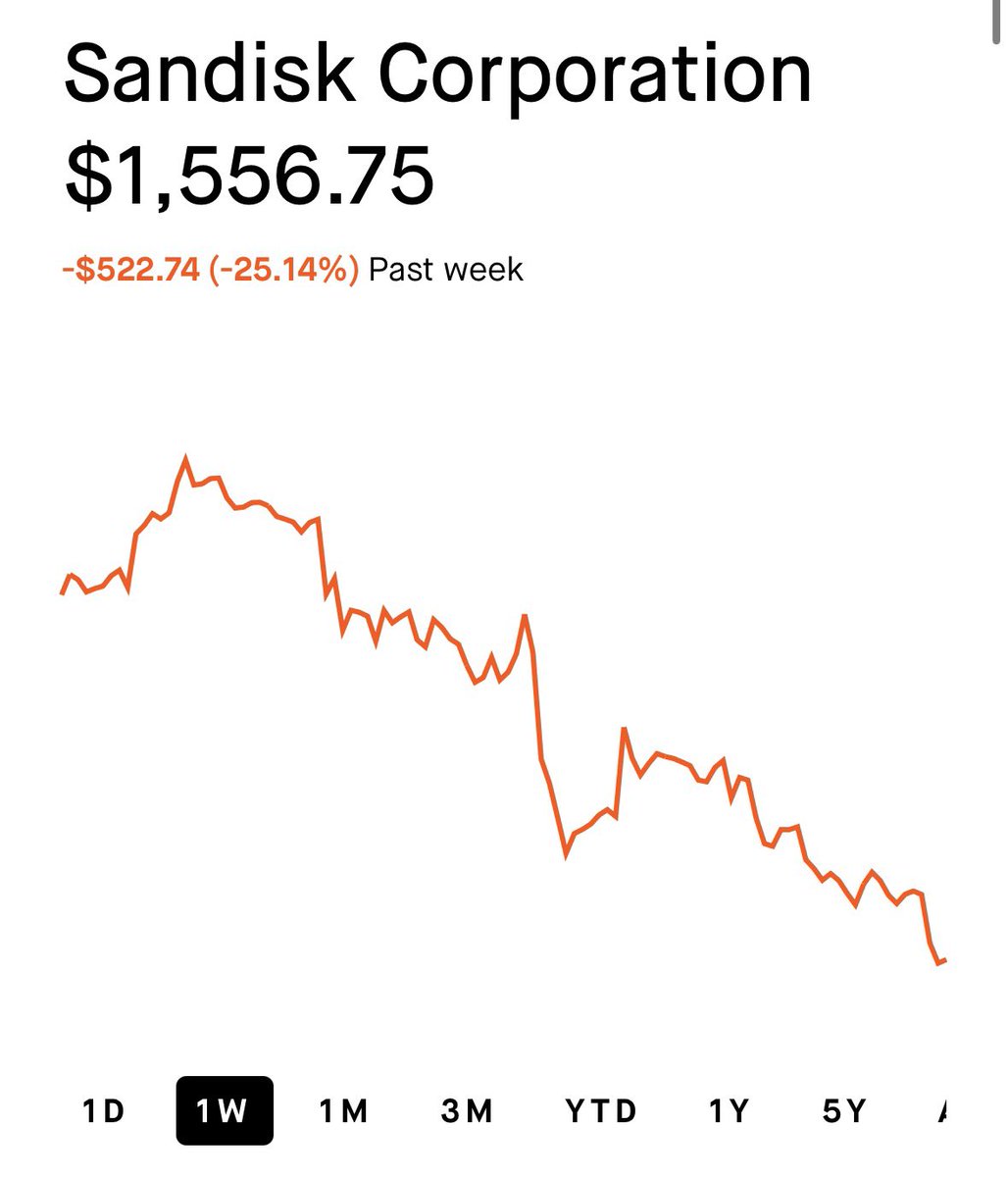

Memory stocks are going thru the biggest bubble we will see in our lifetime for them. A stock like Micron is just one of many. The party is NOT over yet, but when it does end… AND IT WILL… the mess to clean up will be gigantic.