@TheStalwart There's the legitimate contention of why wealth & income are the sole determinants of who is supposedly sophisticated enough to invest in private cos vs the reality of adverse selection that anyone who just qualifies would not be getting the OpenAIs/SpaceXs but cast-offs

@Brad_Setser Or visualized another way by Bloomberg Intelligence.

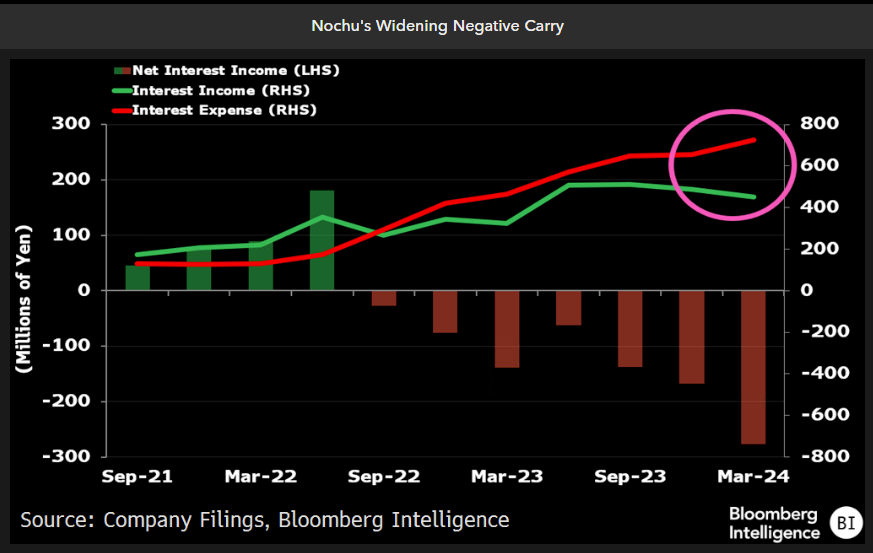

Seems Nochu's particular dependence on repo and XCCY to funds its $ and € trades is driving most of this pressure vs. say a Mitsubishi UFJ who has a cheaper and stable source of $ funding https://t.co/0oETQz6RN6

@hsri07 This is the general trend I was seeing for recoveries in the HY space but admittedly not current (and would be curious to see updated figures here as well)

@the_red_deer@k2_nft But do see a more drawn out corporate deleveraging cycle than that transmits to consumers and in that way more a recession amplifier than immediate 2008 implosion of any sort. Always happy to discuss the merits of that https://t.co/Xumh1WdiGi

@the_red_deer@k2_nft Agree. Key difference being the lower amounts of additional external leverage in the system and where most of the risk is being concentrated (more broadly across insurers vs. G-SIB banks) https://t.co/iDrS0d3X9e

@tyillc@SheilaBair2013 Hear you, but expanding agency data collection on private funds only requires agency rulemaking which can be done now vs. data being available to public requiring amendments passed in Congress (though agree that should one day happen)

@SheilaBair2013@RealBankReform Aw, thanks Sheila! Could be worth including in future editions of "Princess Persephone Loses the Castle"? (Beware the Trickster Lender!)😆

@Stimpyz1@GrandTokamak When you have such blatant capital charge arbitrage and are surprised insurance company portfolio allocation then looks like this

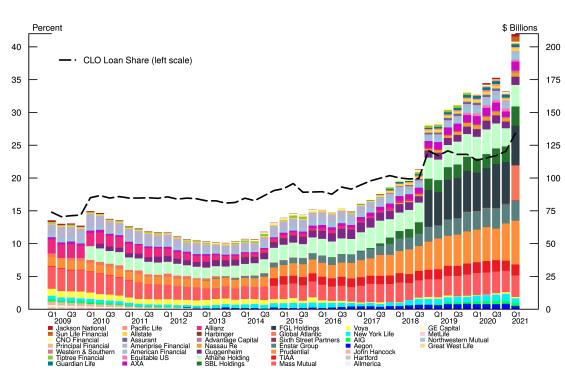

@Brad_Setser And to your original point, most its ~$451bn portfolio looks to be USD https://t.co/Mjrbmyv9id

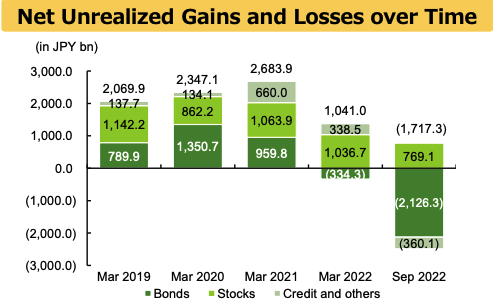

Will say though I was taken aback by their -$13.3bn mark-to-market unrealized losses thru Sept vs. March 2020 👀

@Brad_Setser Yup, underwater on most of its CLO senior tranche (chart is spread) book at this point but I think understanding has always been these were going to be held to maturity given the size of the holdings relative to their liquidity

@Brad_Setser Right. Wondering moreso if TIC is capturing the non-bank/private fund lending to Chinese firms at all since they aren't technically securities and I don't believe have any registered/depository-linked intermediaries between them (unless the custodian is?)

@macrodelics Plenty of issues from downgrades and lower post-default recoveries that will be rough for equity/mezz (not to mention mark-to-market losses across the board) holders but don't have the same level of additional external leverage vs. 2007 https://t.co/2171OO0Ah0

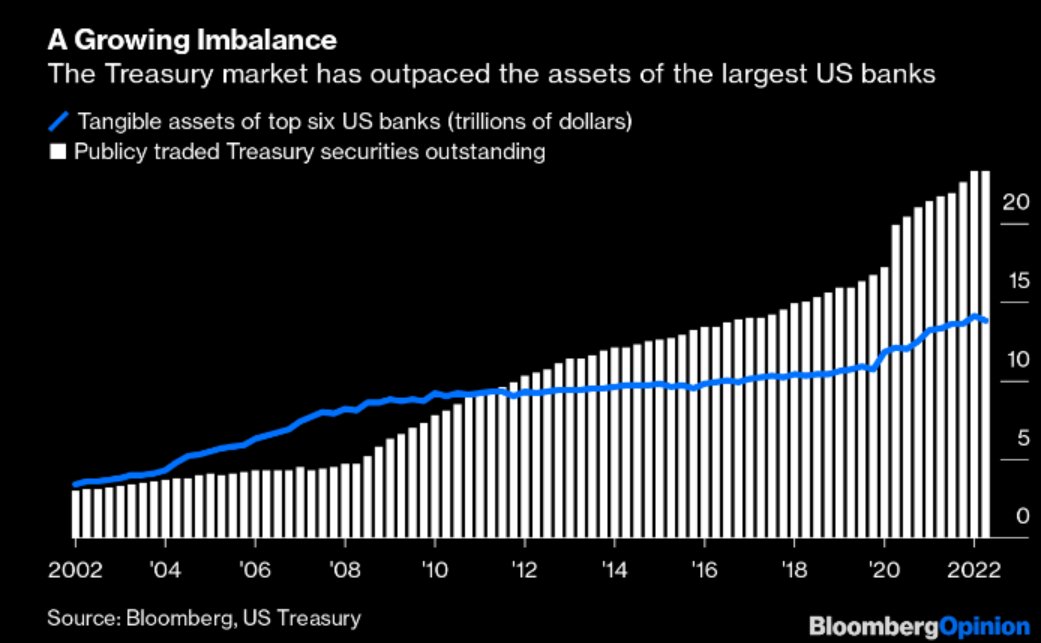

@Brad_Setser Especially as domestically the Treasury market is growing more dependent on mutual funds/insurance cos/hedge funds whose exact involvement in the market isn't always clear from the current available data (re: March 2020) vs. the primary dealers/bank holding companies