2.3x EV/FCF for a digitally inflecting deep-value security group with recurring cybersecurity growth and substantial underlying real-property value:

- Cost optimized

- Billionaire shareholder

- Unique cross-selling opportunity

My first Substack writeup:

https://t.co/UYBD6rTPhH

@evfcfaddict Welcome back aboard, Andy! Besides the great Biz growth, I think the Ponta Pass can turn out quite valuable for the established Security business.

One Danish investor I admire uses a simple formula for estimating future returns:

Earnings growth + share buybacks + dividends.

No forecasts. No market timing. No complex models.

Simple enough to understand. Powerful enough to help him build nearly 400M.

@david_katunaric Good article, David. What makes this stock even more compelling is that it's led by an ex Morgan Stanley person. It's rare to see stewardship of this caliber at a company of this size. Been a position of mine through some time, although of smaller scale.

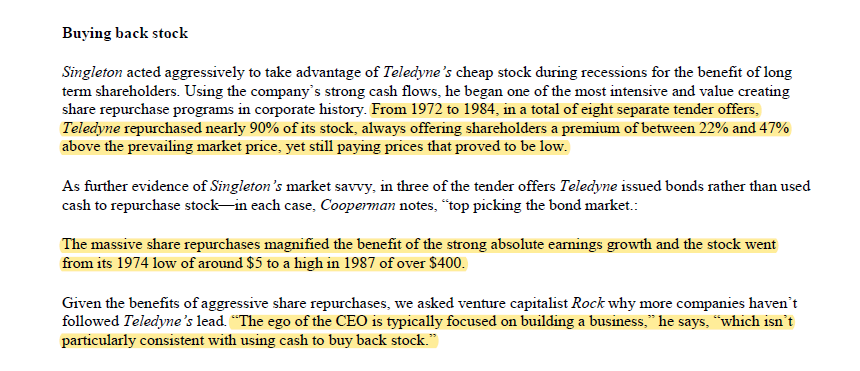

Every public company CEO should study Henry Singleton.

1961–1969: used Teledyne's nosebleed P/E as currency to roll up ~130 companies.

1972–1984: when the multiple collapsed, retired 90% of the share count across 8 tender offers.

Result: 20.4% CAGR from 1963–1990 vs. 8% for the S&P.

Reversing your capital allocation policy 180 degrees when valuation flips is the part nobody copies.

Issuing stock when it's expensive and retiring it when it's cheap sounds obvious. Almost no CEO actually does it.

Entravision $EVC math is pretty simple:

Media assets don't earn much, but thanks to the spectrum & FCC dereg, there's a realistic path to $500m of value

Meanwhile, Smadex, against the full $800m EV, is priced at a fraction of peers and growing faster.

Value guys afraid to buy because "they missed it" and widow of the former CEO has been selling

But there's zero street coverage and the growth guys barely know this exists (yet)

Very bullish on this one. The company is currently in its quiet period and should report in less than a month.

Most importantly, management confirmed the core part of the thesis: accounting treatment is materially understating the company’s true owner earnings.

Cash offer for $PAY.BR stands at 7.38 EUR per share.

Shares worth far far more.

Currently trading for 8.15 EUR

My original thesis mapped this all out and seems to be playing out as I thought. See link in bio if you want to read.

If you are a share holder, please help fight the existing low offer of 7.38 per share.

I have just voted mine here:

https://t.co/Olk0M9iIL8

The WhatsApp group is now projecting over 50% of free float is voting against the offer! But not everyone has added a screenshot of their shares to the website yet.

Please add your shares to the group.

This is my mental model for how $EVC gets to a $100 share price, which on 96.4 million shares outstanding is a $10 billion market capitalization, against the $760 million market cap it trades at today, which is a 13x move from here, which I am aware sounds insane, which I am aware sounds like I have been mainlining something that is not legal in most states, which I am aware is the kind of price target that gets you blocked on FinTwit and quietly removed from group chats. I get it. The stock is $7.89. The company has spent most of the last twelve months trading between $1.81 and $4. The TelevisaUnivision affiliation has to be renewed in December. The legacy media business is shrinking. On the surface, calling for a 13x is the kind of thing a person types at 2 a.m. and deletes at 9 a.m. But if you actually do the math — if you actually look at the segment-level economics, the industry tailwind, the supply curve of new mobile games, the operating leverage of a programmatic DSP at scale, and what comparable AdTech businesses trade at when the market finally figures out what they are — the path is not crazy. The path is arithmetic. What follows is the arithmetic.

Smadex is a demand-side platform for mobile gaming ads, sitting inside a Spanish-language television company called Entravision Communications, which trades on the NYSE under the ticker EVC at $7.89, with a market capitalization of $760 million, against trailing twelve-month revenue of $448 million, against a Q1 2026 print of $197 million in a single quarter, against an Advertising Technology segment that grew 204% year-over-year, against a segment operating profit that went from $6 million to $34 million in twelve months, which is what programmatic operating leverage looks like the first time it shows up in the consolidated P&L of a company that nobody who covers programmatic has ever heard of.

The reason nobody who covers programmatic has ever heard of it is that EVC is covered by the people who cover Hispanic broadcasters. The people who cover Hispanic broadcasters are modeling political ad cycles and the TelevisaUnivision affiliation renewal in December 2026. They are not modeling mobile gaming user acquisition spend. The people who cover mobile gaming user acquisition spend are modeling AppLovin at $130 billion and Unity at whatever Unity is at this week and they have a Bloomberg screen that does not surface a $760 million broadcaster when they search for DSPs.

This is the entire setup. A real business inside a wrong label.

In Q1 of 2026 the App Store received 235,800 new app submissions, which was up 84% year-over-year, after declining 48% from 2016 to 2024. April 2026 was up 104%. The cause is vibe coding. The cause is that Claude Code and Cursor and Replit and Lovable made it possible for someone with no engineering background to build a mobile game over a weekend, and 600,000 people did it last year, and more are doing it this year, and the line on the chart goes up and to the right at an angle that the public forecasts for in-game advertising — which were built when app supply was still declining — have not absorbed yet.

A mobile game built in a weekend has zero organic distribution. There are two million apps on iOS. The algorithm does not surface unknown SKUs. The only way a new game finds a player is paid user acquisition. Paid user acquisition flows through demand-side platforms. Smadex is a demand-side platform.

My model spits out $4.4 billion of revenue by 2031 at 26% operating margins generating $750 million of free cash flow, which discounts back at 12.5% to roughly $10.6 billion of equity value, which is roughly $110 per share on 96.4 million shares outstanding. The 40% sustained growth assumption I'm using is below the 60% advertiser growth rate that the mobile gaming ad industry was already running before vibe coding happened. The 26% margin assumption I'm using is less than half of what AppLovin runs at scale. Neither input is heroic. The model breaks only if Smadex stops growing, which is the binary the current $7.89 print is implicitly assuming.

The path is in three stages. Q2 and Q3 of 2026 confirm the trajectory and the stock re-rates from broadcaster to AdTech-with-a-media-tail and trades at $15 to $25. Margin expansion shows up in 2027 and 2028 and the first sell-side analyst writes the standalone Smadex valuation note and the stock trades at $35 to $55. By 2029 to 2031 Smadex is a $2 to $4 billion revenue business inside a public shell with a legacy media stub and either it gets spun and re-rated to AdTech multiples or AppLovin or Unity or a private equity sponsor takes it out at a control premium and the stock trades at $75 to $110.

The dependencies are four. Smadex maintains 30%+ growth through 2030, which is well below the 204% it just printed. Operating leverage continues to behave like operating leverage, which it is already doing. Vibe-coded apps spend on user acquisition, which the 60% pre-existing advertiser growth rate suggests is the path of least resistance. And management surfaces the value, which is the squishiest of the four and the one where a spin announcement or a separation or even consistent segment-level reporting collapses the holding company discount on its own.

EVC is going to print another quarter in August of 2026 and it is going to be a number that does not fit the broadcaster taxonomy and the screens are going to start picking it up under a different label, and by the second half of 2027 a sell-side analyst at a mid-tier shop initiates coverage with a Smadex sum-of-the-parts and the stock is at $30, and by 2029 a banker at a boutique pitches the spin to management and management says they are evaluating strategic alternatives, and by 2031 the deal closes or it does not need to because the market has already done the math, and the stock is at $110, and the consultant who flew to Burbank in 2019 to pitch them on a programmatic strategy and got served coffee and a polite no is now divorced and works at a Chipotle, and Michael Christenson buys a boat.

@Aktieprenoren@InvesteringsM If you like Truecaller, I recommend also having a look at Japanese Tobila. They should be on track to generate almost entire EV in FCF over the next couple of years.

$EVC Wow!

ATS 204% growth and operating profit was $34.3 million for first quarter 2026, compared to operating profit of $6.5 million for first quarter 2025!