This is wild. And it's exactly why SpaceX IPOs in 3 days.

SpaceX just unveiled AI1: one computer rack strapped to a 230-foot solar wing, with a plan to fly a million of them. On its face it reads as a satellite reveal. Read the timing and it's a pitch deck.

The company prices June 11 at a $1.75 trillion valuation, raising $75 billion, already two times oversubscribed. Rockets and Starlink don't get you to $1.75T. Orbital AI compute might.

Here's the bridge. That 150 kW is roughly a single NVIDIA GB300 rack, nothing special sitting on the ground. The spec that actually matters is 70 kW per ton.

On Earth, the constraint on AI is power. You build next to a substation and wait years in an interconnection queue for the utility to hang enough transformers. The megawatts are the bottleneck, not the chips.

At 600 km that goes away. Sunlight is constant and free, the 230-foot wing is the power plant, and it ships attached to the rack. The only new problem is heat, which is why the thing is almost entirely panel.

So the whole bet collapses to one number that has nothing to do with AI: the cost of putting a kilogram into orbit. Get Starship cheap enough and a watt of solar compute in space underprices a watt trapped behind a transformer queue on the ground.

That's the story they're selling 3 days before pricing: they own the only rocket cheap enough to turn free sunlight into the cheapest compute on Earth, and nobody else can copy it.

A million satellites is 150 gigawatts of compute that never touches a power grid. That's the actual IPO.

Atlassian's revenue: $1.79 billion last quarter

Atlassian's move: fire the engineer who built their infrastructure

his move: post a 38-minute breakdown of every system he built, free for anyone to copy

what he revealed:

> Envoy proxy instead of enterprise load balancers

> sidecar architecture for auth, logging, rate limits

> DynamoDB + SQS for async provisioning

> Packer + SaltStack for automated VM deployments at scale

Atlassian charges per employee across 350,000 customers

this guy just handed you the enterprise playbook for free

save this

Shopify CEO Tobi Lutke explains Goodhart’s law and why he doesn’t like KPIs or OKRs

“Goodhart’s law is real. The moment a metric becomes a goal, it’s no longer a useful metric… No metric by itself is a complete heuristic for a complex business. There’s a million different tensions in a company, and you can’t keep all of them in harmony by optimizing for one thing.”

For this reason, Shopify doesn’t use KPIs or OKRs. But as Tobi explains, this doesn’t mean they don’t value data and metrics.

“We are extremely data informed. We have invested enormous amounts of money and time into systems that give us basically everything at our fingertips… But what Shopify attempts to do is just not over-fit for what’s quantifiable.”

People love optimizing for highly-quantifiable things because there’s immediate gratification that comes from seeing a number go up. But Tobi thinks that the most important aspects of a product are rarely quantifiable:

“The overlap of the most valuable things you can do with a product and the things that happen to be fully quantifiable are like maybe 20%. Which leaves 80% of a value space unaddressable by the people who only look at quantifiable things.”

He continues:

“Shopify is comfortable with unquantifiable things like taste, quality, passion, love, hate… The sort of deep satisfaction that a craftsperson feels when they’ve done a job well is actually a better proxy if you allow it to be.”

They then have robust analytics systems that tell the company if something’s wrong or a new rollout breaks something.

“We think about it as a cockpit for a pilot. The decisions are still made by pilots, and we think this leads to better results… I think there needs to be more acceptance in business of unquantifiable things… And then metrics take a support function.”

Source: @lennysan (Feb 2025)

Let's talk about $UBER because it's been on my mind alot recently... I'm assuming others are also debating these questions in their spare time 😏

Last weekend I took a Waymo and it was a wonderful experience so it's fair to say I'm a big believer in robotaxis as the future of ridesharing.

Right now it feels like Waymo is the leader in robotaxis but they only have ~3,000 cars (ie AVs) on the road doing ~500,000 rides per week.

Tesla might be next but they have less than 150 cars (ie cybercabs) on the road doing less than 1,500 rides per week.

$UBER currently has 1.5M human drivers (just in the US) but nothing in terms of robotaxis other than partnerships with Waymo and AVride (owned by $NBIS) however both options are very limited... Austin & Atlanta for Waymo... and Dallas for AVride. I do think it's possible that Waymo dumps $UBER in the future and just uses their own app in every market... however I could be wrong and maybe it goes the other way because $UBER does have 200M global customers which is massive distribution for any AV ridesharing service that wants scale.

fwiw, $UBER currently does 200-250M rides per week which is 400-500x more than Waymo... however Waymo just raised capital at $126B valuation while $UBER currently trades at $153B valuation. I know some people think Waymo will be the winner but kind of crazy it's already worth 80% of $UBER with just 3,000 cars on the road vs $UBER with 1.5M US drivers and another 4M+ drivers outside the US.

Over the past ~12 months $UBER has announced 15+ partnerships with different brands and OEMs including Lucid, Rivian, Nissan, Pony, Zoox, Nuro, Oro, WeRide, Baidu, Wayve, Volkswagon, May Mobility, Momenta, Mercedes and probably a few more that I'm forgetting about.

I don't think we need to debate that $UBER already has massive distribution but my question is around these 15+ partnerships. Sure it's lots of constant PR which might sound good but we have very limited details... which of these AV companies has technology that is good enough to compete and scale?

Putting tens or hundreds of thousands of AVs on the road in the coming years will be extremely expensive and capital intensive. I'm sure Baidu and Mercedes could handle the upfront capex but I don't know about these other brands. So who is covering the capex? the brand? uber? or do they split it?

With the capex in mind, what does the rev share look like for these partnerships? Will it be the same across the board or does every partnership have different economics? For instance, let's say https://t.co/oX9xZje9Hh can't afford the upfront capex themselves, do they split it with $UBER? or does $UBER cover 2/3 of the capex but then they own 80% of the rev share?

Let's say Baidu and Mercedes can afford the capex themselves and they want to go that route... does that mean $UBER just handles distribution & logistics but only gets to keep 1/3 of the rev share?

Obviously I'm just making up numbers and scenarios because we don't have much else to go on.

Would you prefer $UBER stay asset light and just collect a 1/3 toll like they do now? or do you want $UBER to leverage up the balance sheet to become asset heavy in order to get a bigger rev share % ?

and here comes the monkey wrench in all of this... what if $UBER enables anyone with an AV (similar to what $TSLA might do)... to put their car onto the $UBER network in order to generate some extra income while they're working, sleeping or just not using the car? This would allow $UBER to stay asset light and maybe collect a higher % of the rev share since the car owner might be very happy just collecting 40% of the revenues since it's extra income for them not including the accelerated depreciation.

I'd love to know how others are thinking about this... especially $UBER shareholders... what do you think is the right business/economics model going forward? and do you want them in the capex business in order to get a bigger rev share?

I am very curious to see how this all plays out in the coming years.

NFA.

DYOR.

**We have a tiny $UBER position at @FirstWaveFund because I think the valuation is attractive when you consider 200M customers with the potential to be the robotaxi leader... but I still have lots of concerns about what their strategy looks like going forward and what % of the ridesharing market they lose to Waymo and Tesla and if the TAM can grow big enough for all three companies to be winners? Best case for $UBER is the TAM keeps growing and even as they lose market share the economics for robotaxis are meaningfullly better than a human focused ridesharing network.

Elon Musk explains his 5-step algorithm for solving any problem:

"The most common mistake of smart engineers is to optimize a thing that should not exist."

"I have this very basic first principles algorithm that I run as a mantra."

Elon breaks it down:

Step 1: Question the requirements.

"Make the requirements less dumb. The requirements are always dumb to some degree, no matter how smart the person who gave you those requirements. You have to start there, because otherwise you could get the perfect answer to the wrong question."

Step 2: Try to delete it.

"Try to delete the part or the process step entirely. If you're not forced to put back at least 10% of what you delete, you're not deleting enough. Most people feel like they've succeeded if they haven't been forced to put things back in. But actually they haven't, they've been overly conservative and left things in that shouldn't be there."

Step 3: Optimize or simplify.

"The most common mistake of smart engineers is to optimize a thing that should not exist. So you don't optimize until after you've tried to delete."

Step 4: Speed it up.

"Any given thing can be done faster than you think. But you shouldn't speed things up until you've tried to delete it and optimize it otherwise, you're speeding up something that shouldn't exist."

Step 5: Automate.

"And then the fifth thing is to automate it."

Elon explains why the order matters:

"I've gone backwards so many times where I've automated something, sped it up, simplified it, and then deleted it. I got tired of doing that. So that's why I have this mantra."

Nvidia CEO Jensen Huang just revealed the “five-layer” model of what AI is dependent upon…

These 5 layers include:

1. Energy ~ $NBIS, $IREN, $CIFR, $OKLO

2. Chips ~ $NVDA, $AMD, $TSM, $AVGO

3. Cloud Infrastructure ~ $AMZN, $MSFT, $GOOGL, $CRWV

4. Models ~ $META, $ORCL

5. Applications ~ $PLTR, $TSLA

All these names will see generational upside in 2026 as AI continues to expand rapidly.

Save this for later…

In August I wrote a thesis I never published. The funds I was warning were key Crossover Research clients, so I stayed quiet. Since then, 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗺𝘂𝗹𝘁𝗶𝗽𝗹𝗲𝘀 𝗮𝗿𝗲 𝗱𝗼𝘄𝗻 𝟱𝟬%+. Salesforce $CRM, ServiceNow $NOW, Adobe $ADBE, Workday $WDAY all off 40% from highs. Thomson Reuters $TRI dropped 16% in a single session on the Anthropic legal agent launch. The SaaSpocalypse arrived. So here's the follow-up. Not commentary on what happened, but where I think this goes next.

Most vertical SaaS companies aren't underperforming because their software is bad. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲𝘆 𝗻𝗲𝘃𝗲𝗿 𝗯𝘂𝗶𝗹𝘁 𝘁𝗵𝗲 𝘀𝗲𝗰𝗼𝗻𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀. And the first business is under attack. For twenty years, one of the biggest SaaS moats was engineering complexity: deep technical talent, long roadmaps, compounding codebases that were genuinely hard to replicate. 𝗔𝗜 𝘂𝗽𝗲𝗻𝗱𝗲𝗱 𝘁𝗵𝗮𝘁 𝗮𝗹𝗺𝗼𝘀𝘁 𝗼𝘃𝗲𝗿𝗻𝗶𝗴𝗵𝘁.

Product development is democratizing to operators with no code background but strong product vision. Look at Anthropic: they've built the engine and are shipping lookalike products at a cadence that would have taken a legacy SaaS vendor three years of roadmap, with a fraction of the headcount. That pace can kill legacy businesses overnight.

𝗜𝗳 𝘁𝗵𝗲 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗺𝗼𝗮𝘁 𝗶𝘀 𝗴𝗼𝗻𝗲, 𝗳𝗼𝘂𝗿 𝗺𝗼𝗮𝘁𝘀 𝗿𝗲𝗺𝗮𝗶𝗻: 𝗱𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻, 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮, 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄 𝗯𝗿𝗲𝗮𝗱𝘁𝗵, 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗶𝗼𝗻. The first three are moats the company builds. The fourth is a moat the company captures, and it's the one most resistant to AI disruption.

𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗰𝗼𝗺𝗽𝗹𝗲𝘅𝗶𝘁𝘆 𝗰𝗿𝗲𝗮𝘁𝗲𝘀 𝘀𝘄𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝗰𝗼𝘀𝘁𝘀 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗲 𝗻𝗼𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗱𝗼 𝘄𝗶𝘁𝗵 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗾𝘂𝗮𝗹𝗶𝘁𝘆. Once a vendor is embedded in a compliance workflow, ripping them out means re-attesting, re-auditing, and re-certifying every downstream process. The buyer isn't paying for software, they're paying for the accumulated paper trail. Tyler Technologies ($TYL) is the clearest version of the pattern. State and local government software across courts, public safety, assessment, and ERP. Every module is married to statutory process, FIPS, CJIS, audit trails, and procurement cycles that take years. TYL is down 42% TTM and 2026 guidance came in soft, but the moat didn't break. Revenue still compounded, and government procurement runs on five-year cycles, not five-week news cycles. Veeva is the sharper version. Revenue up 16% in FY26, Q4 beat, the stock still down 25%. The market is selling execution, not weakness. Guidewire in P&C insurance, where regulatory filings and rate approvals anchor the stack, sits in the same setup: still compounding ARR, still winning cloud conversions, multiple reset anyway. Same pattern across all three: multiples compressed, fundamentals intact. The moat is the regulatory surface area itself, and it compounds because the rules get more complex, not less.

𝗜 𝘄𝗮𝘀 𝗹𝗼𝗻𝗴 𝗣𝗮𝗹𝗮𝗻𝘁𝗶𝗿 𝗮𝘁 $𝟭𝟯 (read that here: https://t.co/0N0oIX8N87). 𝗡𝗼𝘁 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗺𝗼𝗱𝗲𝗹 𝗼𝗿 𝘁𝗵𝗲 𝘁𝗼𝗼𝗹𝗶𝗻𝗴. 𝗕𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗼𝗻𝘁𝗼𝗹𝗼𝗴𝘆. Palantir is the proprietary-data version of the regulatory thesis. Once Palantir sits between the customer and their own data, ripping it out means rebuilding the data model from scratch. Snowflake and Databricks never had that entrenchment layer. AIP bootcamps then turned the data moat into a distribution moat: 660 bootcamps in a single quarter, 94% y/y US customer deal growth, bookings at 1.9x sales. Own the data, ship functional AI on top of it, let the GTM compound. Every vertical incumbent has a version of this available. The question is whether they'll build it before a challenger does.

But regulatory insulation is necessary, not sufficient. Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade.

𝗧𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗳𝗼𝗿𝗺𝘂𝗹𝗮 𝗶𝘀 𝗱𝗮𝘁𝗮 𝗼𝗿 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝘀𝘂𝗿𝗳𝗮𝗰𝗲 𝗮𝗿𝗲𝗮 𝗽𝗹𝘂𝘀 𝗳𝘂𝗻𝗰𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜, 𝗻𝗼𝘁 𝗼𝗻𝗲 𝗼𝗿 𝘁𝗵𝗲 𝗼𝘁𝗵𝗲𝗿. Look at why Claude is winning. Anthropic isn't competing on model benchmarks, they're competing on functional workflow. Building for the user, not the leaderboard. That's the playbook vertical incumbents need to run. Take the moat you already have, whether it's regulatory or data-entrenchment, layer genuine workflow AI on top, and the challenger can't catch you. The vendors that do both win the decade. The ones that rely on inertia alone get caught. The ones that ship AI without an anchor get commoditized. You need both.

𝗧𝗵𝗲 𝗯𝘂𝘆𝗲𝗿 𝗶𝘀 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗵𝗶𝘀 𝗽𝗹𝗮𝗶𝗻𝗹𝘆. A study we ran with Battery Ventures on AI adoption in the Office of the CFO (https://t.co/xBEMSF8Y72) surveyed 129 finance leaders at companies from $50M to $5B+ in revenue. 77% said they want to uplevel existing systems with AI from new vendors that layer onto existing systems. Only 15% want to replace their current system of record with an AI-native platform. The incumbent wins if they ship AI. The AI-native challenger wins only if the incumbent doesn't.

The signal shows up in our VoC data too. In regulated verticals, mission criticality scores cluster above 9, and NPS doesn't track satisfaction, it tracks switching friction. Customers will tell you the product is mediocre and still score it 9 on "would not switch" because the compliance team vetoes any alternative. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝘁𝘂𝗿𝗲 𝗼𝗳 𝗮 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲-𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗻𝗱𝗼𝗿, 𝗮𝘀 𝗹𝗼𝗻𝗴 𝗮𝘀 𝘁𝗵𝗮𝘁 𝘃𝗲𝗻𝗱𝗼𝗿 𝗶𝘀 𝗮𝗰𝘁𝗶𝘃𝗲𝗹𝘆 𝘀𝗵𝗶𝗽𝗽𝗶𝗻𝗴 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝘁𝗵𝗲 𝗔𝗜 𝗰𝘂𝗿𝘃𝗲.

Which brings us back to the second business for everyone outside the regulated or data-entrenched moat. Seat ARR got them to $100M. But with the shift to agentic workforce structures, partial human capital replacement, and pricing pressure compressing margins, the traditional SaaS model has to transform fast. The next $500M comes from monetizing the installed base: marketplace rake on demand they generate for their own customers, capital products underwritten by their own transaction data, supplier monetization, brand partnerships, group buying. The assets are already sitting there. Captive SMB audience. Proprietary transaction and behavioral data. A distribution pipe (the UI itself) that delivers new products at near-zero CAC.

𝗪𝗵𝗮𝘁'𝘀 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 𝗶𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘄𝗶𝗹𝗹. Monetizing the installed base requires a different org than the one that got you to scale. Different GTM, P&L optics, and talent. Founders and boards under-invest because year one looks worse before it looks better, and public markets punish any SaaS multiple that starts to look like fintech or marketplace. So the second business never ships. The round prices in the optionality. The multiple compresses. The exit underwhelms.

𝗧𝗵𝗿𝗲𝗲 𝗱𝗶𝗹𝗶𝗴𝗲𝗻𝗰𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴:

𝟭. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗰𝗼𝗺𝗲𝘀 𝗳𝗿𝗼𝗺 𝘀𝗼𝘂𝗿𝗰𝗲𝘀 𝗼𝘁𝗵𝗲𝗿 𝘁𝗵𝗮𝗻 𝘀𝘂𝗯𝘀𝗰𝗿𝗶𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗽𝗿𝗼𝗰𝗲𝘀𝘀𝗶𝗻𝗴? Under 5%, they haven't started. 10 to 20%, thesis is live. Over 20%, it's working.

𝟮. 𝗛𝗼𝘄 𝗵𝗮𝗿𝗱 𝘄𝗼𝘂𝗹𝗱 𝗶𝘁 𝗯𝗲 𝘁𝗼 𝗿𝗲𝗰𝗿𝗲𝗮𝘁𝗲 𝘁𝗵𝗶𝘀 𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗮𝘁𝗰𝗵 𝘄𝗶𝘁𝗵 𝗔𝗜 𝘁𝗼𝗱𝗮𝘆? If a well-funded team with Claude and six engineers could rebuild the functional product in nine months, the software isn't the moat. The moat has to live somewhere else: proprietary data, a network, integrations, or regulatory surface area the challenger can't clear. If you can't point to at least one, you're underwriting a melting ice cube.

𝟯. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗯𝘂𝘆𝗲𝗿'𝘀 𝘀𝘁𝗶𝗰𝗸𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆, 𝗮𝗻𝗱 𝘄𝗵𝗶𝗰𝗵 𝘄𝗮𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗿𝘂𝗹𝗲 𝘀𝗲𝘁 𝗺𝗼𝘃𝗶𝗻𝗴? A regulatory moat evaporates if the regulation simplifies. Underwrite the direction of travel, not just the current state.

𝗔𝗻𝗱 𝘁𝗵𝗲 𝗰𝗹𝗼𝗰𝗸 𝗶𝘀 𝘁𝗶𝗴𝗵𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲. Retention in enterprise SaaS has largely been defined by the pain of systems replacement, not genuine moat. If the stickiness isn't backed by proprietary data, a harvesting flywheel, or regulatory surface area, those vendors are about to get disrupted. Pure seat-based pricing is dying unless vendors embrace agent-seat models, and LLM providers have been subsidizing the market on token cost, with recent pricing shifts signaling cash reserves aren't infinite.

𝗛𝗲𝗿𝗲'𝘀 𝘁𝗵𝗲 𝘂𝗻𝗱𝗲𝗿𝗮𝗽𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗲𝗱 𝗽𝗼𝗶𝗻𝘁: 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘄𝗼𝗿𝘀𝗲 𝗴𝗿𝗼𝘀𝘀 𝗺𝗮𝗿𝗴𝗶𝗻𝘀 𝘁𝗵𝗮𝗻 𝗦𝗮𝗮𝗦 𝗶𝗻𝗰𝘂𝗺𝗯𝗲𝗻𝘁𝘀, 𝗻𝗼𝘁 𝗯𝗲𝘁𝘁𝗲𝗿. Inference costs haven't collapsed, and burning VC cash to subsidize unit economics is a bridge, not a business model. The incumbents should be winning on P&L. They're losing on product velocity and AI-readiness. That's a solvable problem if the board has the will to ship. Vendors without a second business, without a data moat, and without regulatory insulation will still lose, despite having better margins than their AI-native challengers. Customers switch on features and speed, not on unit economics.

𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗿𝘁𝗶𝗰𝗮𝗹𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝗹𝗮𝘀𝘁 𝘀𝗮𝗳𝗲 𝗵𝗮𝗿𝗯𝗼𝗿, 𝗮𝗻𝗱 𝗼𝗻𝗹𝘆 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝗱𝗮𝘁𝗮 𝗯𝗿𝗲𝗮𝗱𝘁𝗵 𝗮𝗻𝗱 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲. Everywhere else, the premium is about to get competed away. Any fund underwriting vertical SaaS exposure right now should be asking the second-business question before the next check clears. DM me, email me [email protected], or let's chat about your portfolio/underwriting process (https://t.co/muMNtk6ssk).

https://t.co/ElZm7vjalx

Photonics is the trade of the decade

We got in early.

The AI bottleneck keeps moving.

First it was compute → $NVDA won

Then memory → $MU and SK Hynix ran

Now it’s interconnects

Moving data between chips at AI speed.

Copper is done.

Light is next.

We positioned across the photonics stack before the crowd showed up, from materials to lasers to foundries to transceivers.

Here’s what I’m holding:

$SIVE / $SIVEF

The one nobody was watching.

Now confirmed as a laser supplier for 1.6T transceivers going into hyperscaler data centers. Tied into next-gen architectures.

NASDAQ listing plans just hit. Institutions starting to move in.

Feels like the last undiscovered chokepoint.

$AAOI

Fully vertically integrated transceivers and even makes its own lasers.

Serious hyperscaler demand already showing up.

April 30 earnings = big moment.

$AXTI

This is upstream.

Indium Phosphide = critical for AI lasers.

No InP → no lasers

No lasers → no photonics

No photonics → no scaling

Most overlooked part of the chain.

$COHR

Picks and shovels.

Scaling advanced InP wafers. Backed and booked out years.

Positioned across multiple optical growth areas.

$LITE

Could be sold out through 2028.

Massive growth, strong backlog, already landing early CPO orders.

Watch this closely; it’s a signal stock.

$SOI

Quiet monopoly.

Every silicon photonics chip needs SOI wafers.

Huge IP moat. Market still catching on.

$TSEM

Key foundry for silicon photonics.

Scaling capacity hard with long-term demand locked in.

Critical piece of the ecosystem.

$SMSN.L

Only one doing memory + logic + packaging + photonics.

As AI scales, full-stack players win.

Still cheap vs peers.

$EWY

Memory is the other bottleneck.

SK Hynix leading HBM. Demand not slowing.

This gives broad Korea semi exposure.

This isn’t hype. It’s physics.

AI isn’t just about compute anymore.

It’s about moving data.

And the shift from copper to light is happening now.

Institutions are just starting to figure it out.

Shoutout to the leaders in the space on X.

I have got most of my education from them.

They are a must follow in the space

@crux_capital_@PhotonCap@damnang2@aleabitoreddit@ParadisLabs@jukan05

The execution layer gets all the attention. But the design conditions underneath it are the interesting, human part.

@tobi and I get into it on the latest Context episode. We talk about my path from politics to @Shopify COO, invisible work, and why T-shaped people are becoming X-shaped.

Highlights:

1:09 - A Nonstandard Career Path

5:12 - White House Transition Lessons

8:40 - T-Shaped vs X-Shaped People

10:18 - Fluid Intelligence and Agency

13:31 - Rethinking HR as Talent

15:26 - Flex Wallet and Boomerangs

17:04 - Building Systems and Teams

19:38 - AI-Assisted Small Teams

22:01 - The Social Coefficient

24:52 - Dead vs Alive Companies

27:20 - Incentives and AI Usage

29:49 - Our Relationship with Data

36:29 - Shopify's Position with AI

40:02 - Anthropomorphizing AI

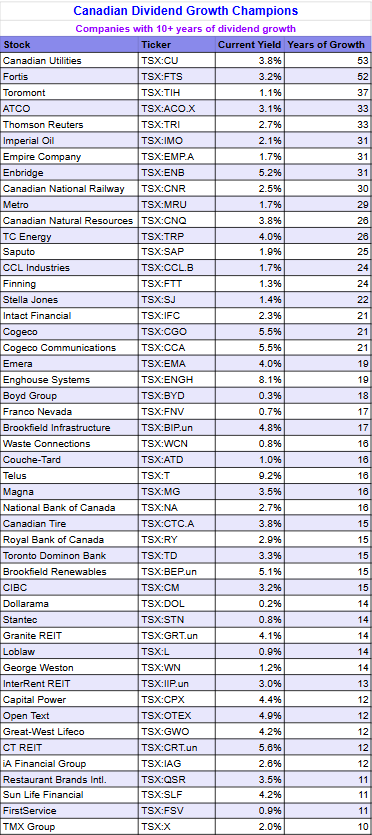

An updated list of the 49 stocks on the TSX that have increased their dividends at least 10 years in a row.

An excellent hunting ground for quality Canadian companies, IMO.

I don't understand why people don't use CLAUDE for stock trading.

It analyzes charts, digests earnings reports, and spots trends in seconds.

Here are 16 prompts to turn it into your personal hedge fund analyst:

James Liang is a Chinese billionaire who pays his employees 50K for every baby they make, who is launching a 1 Billion fund to pay PHD students to have children, here’s why…

James is the cofounder of https://t.co/fgLx7FDZQ7 worth $50B, he was also a prodigy academic who started college at 15, got a PHD at Stanford and then became a professor at China's top university PKU. He straddles not just the active and the contemplative life but elite circles across US and China.

Sitting at this unique intersection helped him articulate his most important idea: that demography is one of the most overlooked factors that impact innovation. The problem with an aging population is not just the financial strain on pensions but a cultural, technological stagnation that will suffocate any creative act. Gerontocracies (rule by the old) result in sterile, hierarchical, and unimaginative futures. If humanity is going to continue innovating, humanity needs to stay young. James believes offering money alone can significantly fix the problem and is putting his money where his mouth is.

In this interview, you will learn about the coming population collapse from one of the world’s foremost demography experts and what to do about it from one of the world’s most resourceful entrepreneurs.

Timestamps:

2:02 Paying Employees to Have Babies

3:09 Low Fertility Kills Innovation

11:05 The Young Want Merit. The Old Want Hierarchy

15:42 Small Population = Little Innovation

33:50 Why a CEO Left for Academia

48:33 Humanity Craves Novelty

55:14 True Innovation Creates Heritage

1:16:32 AI Won’t Lead Innovation