43 stocks will move from the small-cap Russell 2,000 into the large-cap Russell 1,000 after the close tomorrow. The 25 largest stocks in the index are up 260% over the last year.

Needless to say, the Russell 2K is going to look and act a lot different in the 2nd half. $IWM

JPM: "Many tokens consumed in the future may not come from frontier models but from smaller open models that are up to the tasks. Amazon now offers a half-dozen open models at a fraction of frontier pricing, and NVIDIA is teaming up with Dell, Lenovo and HP to make PCs designed with AI agents. While OpenAI and Anthropic compete with their own smaller models (e.g., Claude Haiku and GPT-5.4-mini), these models aren't competitive vs the efficient frontier right now. That frontier shown as the green zone below is dominated by China (DeepSeek, MiniMax, Xiaomi, Alibaba) and only includes a modest presence from US models including one from xAI (Grok) and one from NVIDIA (Nemotron). Consider the following: Claude Opus 4.8 costs $3,700 to run the Artificial Analysis Intelligence Index task set for a score of 56, while DeepSeek V4 Pro (Max) scores at 44 for just $186, which is ~20x cheaper. TLDR; you don’t need frontier level intelligence for everything, and if you do, https://t.co/JdwoOcImCh’s GLM 5.2 appears competitive with top tier Anthropic and OpenAI models."

This gets to the pricing power challenge I dissected in my December report on "GenAI & Productivity" (https://t.co/kEx5Z4BJH7). The commodification of models will come not only from frontier model competition, but enterprises seeking cost control via cheaper, narrower use-case models. This implication has been abundantly clear as I research my upcoming report on "The Medical Innovation Inflection." Whether it's drug discovery, devices, or care delivery, health care stakeholders are looking at a variety of pathways to AI deployment including DIY capabilities trained on proprietary data and SaaS capabilities built with domain expertise.

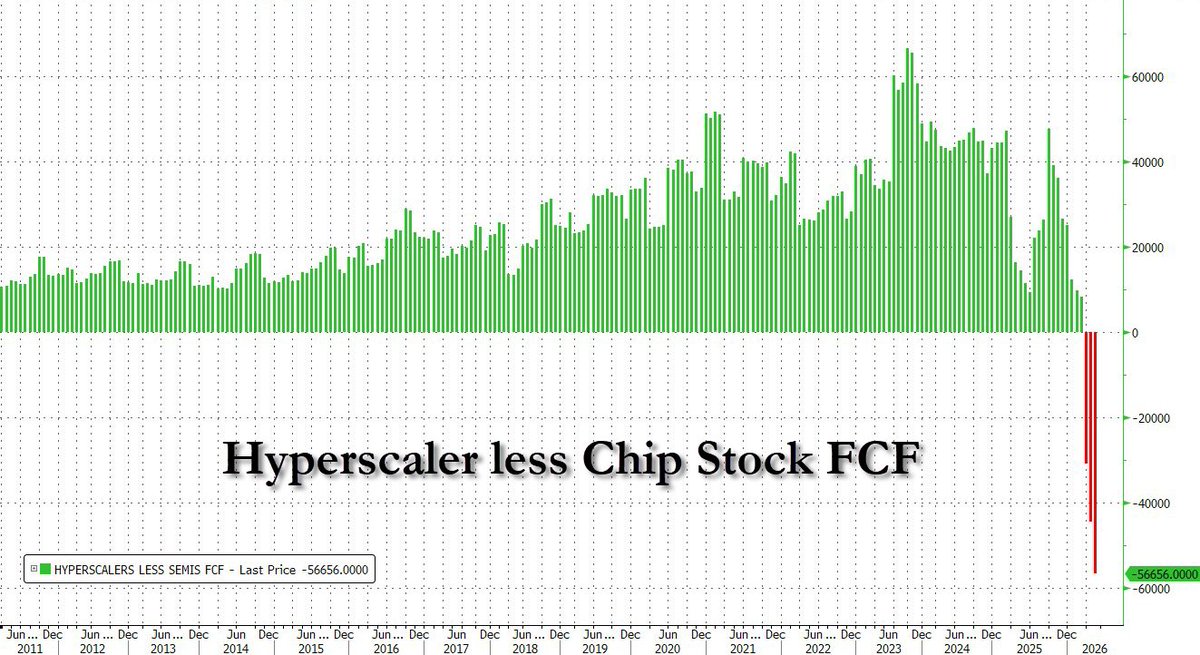

I continue to believe that enterprise spending is the most viable path for hyperscalers to recoup AI CAPEX. Of course, enterprises will spend as little as possible to realize AI-driven revenue growth alongside margin expansion. It's far too early to know where that tug-of-war lands, but the ongoing progression of increasing buildout costs alongside expanding enterprise AI optionality suggests the market continues to underestimate the pricing power challenges hyperscalers face.

Learn more about Sage Road Research here: https://t.co/Wgwz2xnvR6. Interested in subscribing? Message me.

JPM link: https://t.co/P8hiu8swMI

Goldman Sachs: "So far this year, US-listed levered ETF trading volumes are running 50% higher than the first six months of 2025’s record pace…this breaks down to roughly $45 billion /day in volume, turning over 30% of complex AUM…"

🇺🇸 Recession

The probability of US recession in 12 months, calculated from the yield curve, stands at 12.5%, tilting the narrative toward continued expansion. This cycle still has room to run

👉 https://t.co/m11iBkSWhc

#yieldcurve#economy#GDP#growth#economics#recession

Market makers remain in negative gamma.

Under these conditions, market makers in the options space will be forced to trade with the market, amplifying moves in both directions rather than cushioning them.

Microsoft, the third largest Tech stock in the S&P 500, is down by 26.5% in the first half of 2026. If that held here, it would be the worst semi-annual performance since the second half of 2008

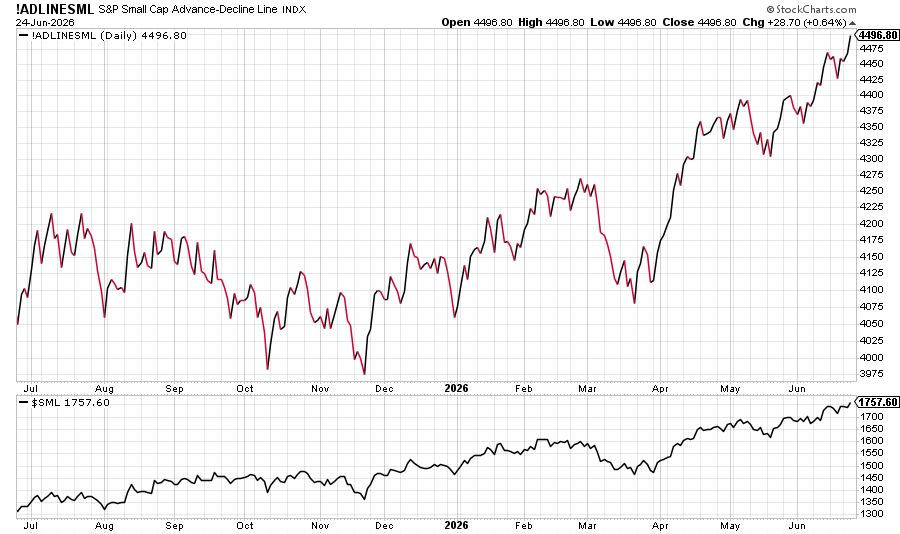

Small caps (the S&P 600) closed at their highest level in history today.

Also, the small cap advance/decline line did as well. File this one under not bearish.

US technology stocks are driving historic market gains:

The MSCI USA Momentum Factor ETF, $MTUM, has surged +38.2% year-to-date, more than 4 times the S&P 500’s equal-weighted index gain of +9.2%.

The fund’s top holdings include Micron, $MU, Intel, $INTC, AMD, $AMD, and Broadcom, $AVGO.

As a result, the $MTUM to S&P 500 equal-weighted index ratio has risen to a record ~172.

This ratio has surged +75.0% since early 2023, as momentum stocks have materially outperformed the average stock.

This metric also now stands 14.7% above the 2020 pandemic recovery peak.

Meanwhile, the MSCI US Momentum Index to MSCI US Index ratio has surged +24% over the last quarter, the largest quarterly outperformance on record, surpassing the 2000 Dot-Com bubble high of +21%.

The momentum trade is leaving the rest of the market behind.

.@Gallup: "The most common way Americans say they have gotten their news in the past seven days is from social media (54%), followed by news websites or apps (44%)."