The two sectors where we're likely seeing the biggest hits from AI (in terms of jobs) - Tech and Finance - continued to shed jobs in May.

Tech payrolls have been falling since November 2022 and Finance payrolls have been falling since last May

Amazon just made it possible for any founder to plug into the same logistics network that delivers a package to your door the next day.

That's not a small thing.

Amazon Supply Chain Services, ASCS, is now open to businesses of all sizes. Freight, distribution, fulfillment, parcel shipping. The same infrastructure that powers Amazon's own marketplace is now available to you as a service.

Procter and Gamble, 3M, Lands' End, and American Eagle Outfitters are already signed up. These are not scrappy startups testing the waters. These are massive operators who understand what world-class logistics actually costs to build.

Here's what most people are missing though. This isn't just a story about physical products getting cheaper to ship.

It's about AI agents entering the physical world.

We're already seeing agents that can purchase using Stripe. Now those same agents can tap into Amazon's logistics network to move, store, and deliver real goods. The agentic economy isn't just digital anymore. It's touching atoms.

FedEx and UPS stocks dropped on this news. The market understood the implications immediately.

For founders, the barrier to launching a physical product just got meaningfully lower. You don't need to build warehouses. You don't need to negotiate freight contracts. You just plug in.

The question is: what physical product have you been putting off building because the logistics felt too hard?

@ChrisCamillo@Rewkang It didn’t seem like you. Just wanted to let you know half the podcast is an advertisement for his fund. And pomp bought some. The fund owns a lot of the same companies you do but at a 300% premium.

@IsomorphicLabs Would love to see @IsomorphicLabs open their next round to the public. Let the retail community invest, support the innovation, and be a part of the journey.

$CLF: The Most Asymmetric Setup in the AI Power Trade

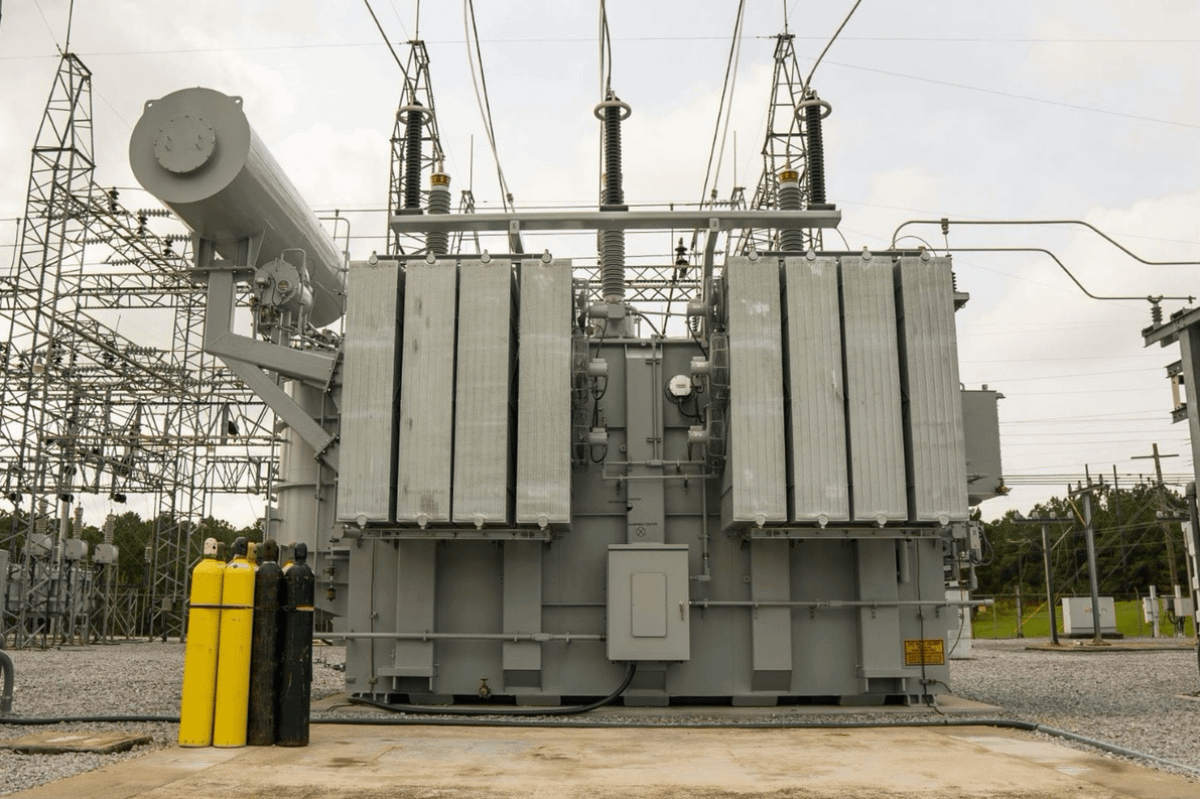

Cleveland-Cliffs is the only name in the AI Power complex that hasn't re-rated. PWR, GEV, ETN, HUBB, VRT — all multi-baggers off the data center buildout. CLF is still trading like a busted 2022 cyclical despite owning the only domestic GOES asset in the United States, a transformer plant ramping this half, and 1GW+ of powered industrial land sitting on the balance sheet at effectively zero implied value.

The Q1 2026 print and call last week was the cleanest setup on this name in two years.

The earnings cadence is now visible

Goncalves was unusually direct: Q1 was the trough, Q2 will be the best quarter in nearly two years, and Q3 will be "much better than Q2" with maximum operating leverage. The mechanics back it up:

- Pricing lag has extended from ~1 month to ~2 months as order books fill. Translation — current spot strength flows through later, not today. ASPs already +$55/ton QoQ in Q1, guided +$60/ton again in Q2.

- The $80M energy hit from February's gas price spike was a one-timer. Removed in Q2.

- Final ArcelorMittal slab shipments completed in Q1 (175k tons, drag now done). The annualized EBITDA tailwind from contract termination starts flowing in full.

- Q2 outages add ~$15/ton on cost; Q3 is outage-light. That's the operating leverage quarter.

- Working capital release: AR built ~$130M in Q1 as March shipments accelerated. Q2 collections + higher EBITDA = "major cash collection quarter."

If HRC pricing simply holds and management executes guidance, Q3 is the print where 2026 consensus EPS resets meaningfully higher. The street is still anchored to Q4 2025 trough numbers.

Tariffs are now structural, not tactical

Imports are at the lowest level since 2009. Section 232 sits at 50% across the top 10 importing countries — Canada, Brazil, Mexico, Korea, Japan, Germany, all at 50%. Total flat-rolled imports running ~340k tons/month, less than half the 2024 average of 750k.

The kicker most are missing: distribution transformers were just added to the derivative product tariff list. That's a direct tailwind to the Weirton transformer plant ramp and an indirect tailwind to Butler Works GOES output, because it walls off the domestic market from imported finished transformers. Goncalves called it out explicitly — "exactly the right outcome."

This isn't a tariff trade in the cyclical sense. It's a regime change. Melted-and-poured + 50% Section 232 + derivative enforcement is structural protection for the only fully integrated US flat-rolled producer with domestic ore feed.

The GOES/DPA leg is still a free option

The April 20 Section 303 Defense Production Act determination explicitly named "electrical core steel" as essential to national defense. CLF is the only domestic producer. Butler Works expansion on track for 2028. Middletown Works affirmed. DOE EDF (formerly LPO) financing now opens up — and Section 1706 authority expires September 30, 2026, which forces deployment of capital into qualifying projects.

GOES + transformers is ~7% of revenue today. The ramp pushes that into low double digits over 12–24 months. None of it is in consensus. The market is pricing CLF as a leveraged auto cyclical. The DPA exposure, the Weirton commissioning, the Butler expansion — all sit on top of the base case for free.

The aluminum trade is happening in real time

This was the most underappreciated part of the call. Goncalves: "In my long career in this business, I have never seen so much momentum in substituting aluminum with steel."

Catalysts converging — domestic aluminum plant fire took out ~40% of US automotive aluminum sheet supply, Strait of Hormuz affecting ~8–9% of global aluminum output, Iran strikes hit Iran's largest aluminum plant, aluminum at 4-year highs. Cliffs has proven steel substitution on fenders and other previously aluminum-only parts using the same OEM stamping equipment. New Carlisle EGL line restarted to handle the volume. Toyota Quality Excellence Award in February.

Mix-up, share-up, volume-up — all at once, all flowing to the highest-margin auto book.

The hidden asset: 1GW+ of powered land

Buried on slide 8 of the deck. CLF is sitting on more than 1 gigawatt of idled, powered industrial land — sites with grid interconnect, water access, and infrastructure already in place. $425M of asset sales under contract or closed (~$70M received), management guiding $50M Q2, $100M Q3, balance Q4. 100% of proceeds going to debt paydown.

In a world where hyperscalers are paying premium for any site with utility-scale power and interconnect, this is pure data center optionality embedded in the equity at zero implied value. Watch the buyer profile on the remaining contracts.

The chart: 50 SMA reclaim is the trigger

Daily setup is now genuinely constructive. $CLF reclaimed the 50 SMA at $9.43 and is now sitting at $10.51 with the 50 SMA starting to flatten and curl up. 200 SMA at $11.44 is the next clear target. Above $11.44, the path opens to $14–15 (the late-2025 highs) where the bullish consensus PTs cluster.

The recovery off the March-April lows around $8 has the right shape — higher lows on rising volume, with the April 20 post-earnings response ripping the stock from sub-$9 to $9.96 intraday. The market is starting to front-run the Q2 inflection.

The line in the sand is the 50 SMA at ~$9.43. As long as daily closes hold above it, the structure stays bullish and the path of least resistance is up toward the 200 SMA. Lose $9.43 on a daily close and the setup resets.

Weekly context: the post-2022 base from $7 to $15 is now four years deep. Long-duration accumulation at deep cyclical lows tends to resolve to the upside when the macro inflects — and the macro just inflected via tariffs, DPA, and the auto recovery hitting at the same time.

Setting up the trade

Three independent bullish legs stacking on top of each other:

1. Tariff regime + slab contract end + working capital release = visible Q2/Q3 earnings inflection

2. Aluminum-to-steel substitution = mix and share gains in the highest-margin auto book

3. GOES/DPA + 1GW powered land = free options the market isn't paying for

Sell-side PT cluster of $11.86–$15 implies 13–43% upside on consensus alone. If Q2 prints clean and Q3 confirms the operating leverage, consensus migrates to the high end of that range. The DPA leg layered on top is what gets you to $16–18 over 12–18 months as the GOES/transformer revenue mix moves toward double digits.

Above the 50 SMA is the trade. Below it, you wait.

$CLF has to be the most overlooked stocks in the market

Sure it has a huge chunk of debt but

1. Trades under book value even at depressed valuations ( it should be trading at a premium because it’s metered land)( as in date Center’s can avoid years of sitting idle waiting to get power)

2. Its factories are already energized. As an aluminum factory it has a boatload of power

3. fills the void for the current transformer shortage. (fabricate the base material for them)

4. Trades are a massive discount for replacement cost of factories.

These guys will either see massive margin expansion from premiums for it’s raw material being it’s in high demand

Or it’s energized Land being it skips years of idle time for data centers

At these levels, I believe it offers a really favorable risk to reward

Disclaimer I’m long

Half of America's AI data centers planned for 2026 are delayed or cancelled. They're waiting on transformers. I build chemical plants. Transformer prices have tripled in the last four years. Lead times are 2 to 4 years. Each new plant we build competes with AI data centers for the same grid equipment. Every large power transformer in America runs on grain-oriented electrical steel. It's made by rolling iron and silicon together until their crystals align in one direction. No other alloy works at utility scale and only one US company makes it: Cleveland-Cliffs. The average large power transformer on the grid is 38 years old. Service life is 40. Amazon, Google, Meta, and Microsoft committed $650 billion to AI infrastructure this year. Nvidia's most expensive GPU is useless without a transformer.

So why $CLF? I have seen tons of posts on X about bottlenecks in the AI cycle, and I believe that $CLF is the next major bottleneck.

$CLF is a vertically-integrated flat-rolled steel producer. They mostly make steel for cars. Boring, right?

Enter Grain-Oriented Electrical Steel (GOES)- a critical aspect of building a transformer. Without GOES, there is no transformer. The need for transformers is only going to continue growing because of data centers.

It is safe to say the AI cycle relies on GOES. Now, guess who is the only producer of GOES in the US? $CLF.

This company is going to be critical for the ever-expanding AI industry, and currently they are being priced as an automotive steel company. I believe they are a massive bottleneck for building data centers and will see massive growth in the future.

NFA

$CLF is the most overlooked AI trade on the board.

Hyperscalers have $650B of 2026 capex ready to deploy. 45% of planned US data center capacity is already delayed or cancelled.

Not because of GPUs. Transformers.

And every large power transformer in America needs grain-oriented electrical steel (GOES).

$CLF (Cleveland-Cliffs) is the ONLY domestic producer at commercial scale.

• Transformer demand +119% since 2019

• Lead times up to 5 years

• Section 232 tariffs on imports

• DOE 2027 rules force GOES-spec

• ~$4B market cap

Priced as a steel cyclical. Positioned as a grid monopoly.

Re-rate is a matter of when, not if.

The key topic going into tomorrow’s $TSLA We, Robot event is Robotaxi timing.

Looking back over the last decade, Elon has commented ~20 times on the timing of FSD/Robotaxi availability. His average prediction suggested the tech will be ready in less than 2 years.

Needless to say, investors will take any timing commentary with a grain of salt. The one positive scenario would be if Elon indicates commercialization of the rideshare network will begin in less than a year. The reason this would be viewed as positive is “less than a year” is close enough that many investors would believe Elon.

My prediction: Elon announces an initial robotaxi city that will begin by the end of 2025.

If you’re curious, here’s some of Elon’s commentary over the past decade:

• 2014 (October): Musk predicted Tesla would have complete autonomy within six years (by 2020).

• 2015 (December): Musk reiterated that complete autonomy would be achieved in two years (by 2017).

• 2016 (October): Musk declared autonomous driving was a "solved problem" and said it was less than two years away.

• 2016 (October): He predicted that Tesla robotaxis would be operational by 2020.

• 2016 (October): Musk predicted that a Tesla vehicle would drive itself from Los Angeles to New York without driver intervention by the end of 2017.

• 2017 (April): Musk admitted autonomy was proving to be "harder than we thought." and predicted full autonomy was close, estimating Level 4 autonomy (fully autonomous in most situations) by 2019.

• 2017 (October): Musk predicted feature-complete full self-driving would be ready by 2019.

• 2018 (February): Musk reaffirmed FSD capabilities available within 3 to 6 months and adjusted the LA to NYC drive timeline to end of 2018.

• 2019 (April): At Tesla’s Autonomy Day event, Musk predicted that Tesla would have over 1 million robotaxis on the road by the end of 2020.

• 2019 (October): Musk predicted that Tesla's FSD would be "feature complete" by the end of 2019, meaning drivers could "go hands-free and just look out the window," regulatory approval still seen as a barrier.

• 2020 (January): Musk reiterated that Tesla would launch the Tesla Network robotaxi fleet by the end of 2020, later saying it would happen in some markets but required regulatory approval.

• 2020 (July): Musk stated during Tesla's Q2 earnings call that full autonomy was “very close” and that Tesla was undergoing a significant rewrite of its FSD software. He predicted that FSD would be feature complete by the end of 2020.

• 2020 (October): Tesla released a limited beta of supervised FSD to some customers, marking a key step forward but still requiring driver supervision.

• 2021 (July): Musk predicted that FSD would likely be “widely available” by the end of 2021, acknowledging that the development of full autonomy was proving more difficult than anticipated.

• 2022 (May): During Tesla's Q1 earnings call, Musk stated that achieving full autonomy remained Tesla’s "number one priority." He admitted that solving full self-driving was "one of the hardest problems ever."

• 2022 (June): Musk said in a Twitter discussion that he expected FSD Beta to be "feature-complete" globally by the end of 2022, but acknowledged that regulatory approval remained a significant hurdle.

• 2023 (February): Tesla expanded its supervised FSD Beta to all customers in North America.

• 2024 (April): Robotaxi Unveiling event was scheduled for August.

• 2024 (July): August event was delayed.

• 2024 (July): Robotaxi event for October 10, 2024, with Musk claiming it would be “one for the history books.”

• 2024 (October): More to come tomorrow.

Today is not only Tesla's earnings call, it's also the 7 year anniversary of Tesla Autonomy Day 2019.

Elon, very confidently, claimed they'd have 1 million robotaxis by 2020 and if you need a geofence area, you don't have real self-driving.

Full video:

https://t.co/MS5vyAW6Dz

@SawyerMerritt They only have 1,023 robotaxis WeRide

They only have 1,446 robotaxis https://t.co/KUc8oN3JKY

They only have over 1,000 robotaxis Baidu Apollo Go

They only have 3,000 robotaxis Waymo

Two days ago, Anthropic cut off third-party harnesses from using Claude subscriptions — not surprising. Three days ago, MiMo launched its Token Plan — a design I spent real time on, and what I believe is a serious attempt at getting compute allocation and agent harness development right. Putting these two things together, some thoughts:

1. Claude Code's subscription is a beautifully designed system for balanced compute allocation. My guess — it doesn't make money, possibly bleeds it, unless their API margins are 10-20x, which I doubt. I can't rigorously calculate the losses from third-party harnesses plugging in, but I've looked at OpenClaw's context management up close — it's bad. Within a single user query, it fires off rounds of low-value tool calls as separate API requests, each carrying a long context window (often >100K tokens) — wasteful even with cache hits, and in extreme cases driving up cache miss rates for other queries. The actual request count per query ends up several times higher than Claude Code's own framework. Translated to API pricing, the real cost is probably tens of times the subscription price. That's not a gap — that's a crater.

2. Third-party harnesses like OpenClaw/OpenCode can still call Claude via API — they just can't ride on subscriptions anymore. Short term, these agent users will feel the pain, costs jumping easily tens of times. But that pressure is exactly what pushes these harnesses to improve context management, maximize prompt cache hit rates to reuse processed context, cut wasteful token burn. Pain eventually converts to engineering discipline.

3. I'd urge LLM companies not to blindly race to the bottom on pricing before figuring out how to price a coding plan without hemorrhaging money. Selling tokens dirt cheap while leaving the door wide open to third-party harnesses looks nice to users, but it's a trap — the same trap Anthropic just walked out of. The deeper problem: if users burn their attention on low-quality agent harnesses, highly unstable and slow inference services, and models downgraded to cut costs, only to find they still can't get anything done — that's not a healthy cycle for user experience or retention.

4. On MiMo Token Plan — it supports third-party harnesses, billed by token quota, same logic as Claude's newly launched extra usage packages. Because what we're going for is long-term stable delivery of high-quality models and services — not getting you to impulse-pay and then abandon ship.

The bigger picture: global compute capacity can't keep up with the token demand agents are creating. The real way forward isn't cheaper tokens — it's co-evolution. "More token-efficient agent harnesses" × "more powerful and efficient models." Anthropic's move, whether they intended it or not, is pushing the entire ecosystem — open source and closed source alike — in that direction. That's probably a good thing. The Agent era doesn't belong to whoever burns the most compute. It belongs to whoever uses it wisely.