“Understanding both the power of compound interest and the difficulty of getting it is the heart and soul of understanding a lot of things.”

— Charlie Munger

⚡️BREAKING

Trump to Fox News on Iranian attacks on Israel:

"What I would suggest to Iran: You've shot your missiles, that's enough. Get back to the table and make a deal"

Alexander Zverev wins the French Open! It's his 1st career major title in his 41st Major appearance.

Only Goran Ivanisevic (48 appearances) needed more attempts among men in the Open Era before winning his 1st major title 🎾

.@intel and @GreenstoneBio are working together to speed up the development of new medicine, combining state of the art human genetics and biology from Greenstone with advanced computing platforms from Intel. This work will allow rapid drug discovery at lower cost. This combination of human biology and AI computing will shape the future of biomedicine in the coming years. I’m amazed by the work my longtime friend Dr. @Joseph_C_Wu and his team are doing, and we are excited about the potential of this partnership.

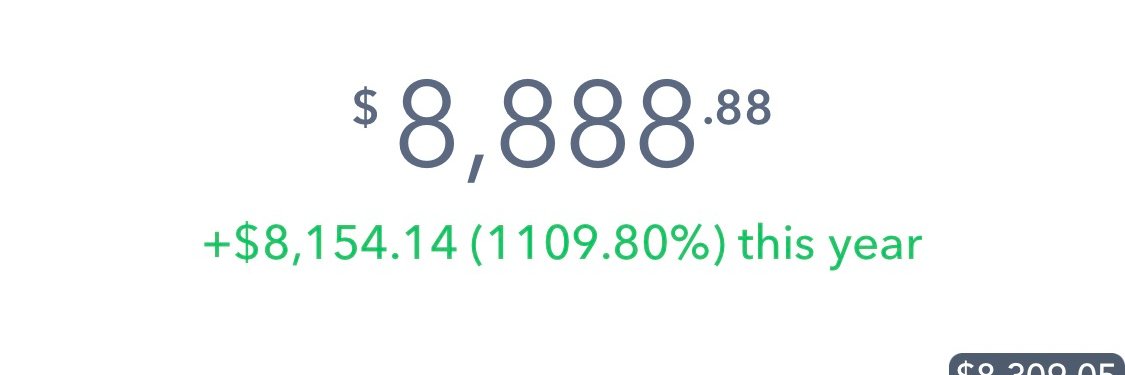

$AAOI will be one of those stocks that is completely obvious like $SNDK - it goes up 5,000% and you are wondering what spell was cast on you to not buy it.

Im long $AAOI till the foreseeable.

$CIFR CEO Tyler Page says the company may generate its own power on-site to move faster on AI data center demand.

Hyperscalers need power faster and Cipher may be able to “tap the pipeline” instead of waiting years on the grid.

Paul Tudor Jones opens a fireside chat with Druckenmiller by admitting one of his biggest mistakes:

"after the crash of '87, i was so worried about debt to GDP that it caused me to be short the stock market for the entire decade of the nineties."

an entire decade. one of the greatest bull markets in history. and one of the greatest traders alive sat short through the whole thing because of a macro obsession.

then Druckenmiller adds his own version:

"the one rule i had for thirty years of trading was never let my obsession with the debt interfere with my trading. because it never had market impact."

"and then i looked at the numbers and i threw out my playbook."

two of the best macro traders ever, both admitting that the hardest part of their career has been separating what they believe should happen from what the market actually does. until the math finally forces you to act.

Coatue's Thomas Laffont on a "Power Law Paradox": a business valued between $100B and $1T (a "Centacorn") has a higher statistical likelihood (31%) of multiplying its value by 10x compared to smaller, earlier-stage unicorns (8%).

Chief AI Officer Alex Wang is subtly confirming that $META's previous AI paradigm failed, and they are executing a strategic shift to close their ecosystem, capture personal data, and build a regulatory moat.

For the last few years, Meta’s entire strategy was to open-source frontier-level models like Llama 2 and 3 to commoditize the foundational layer. Now that Meta is building highly lucrative Personal Agents, they are keeping their best tech proprietary.

$ASML is bringing Elon Musk into a closed-door employee conference to discuss the $55B $TSLA and $SPCX Terafab project.

Terafab would target leading-edge 2nm chips for AI, robotics and space compute.

In 12 to 18 months the world will understand how this cross section of $INTC 18A fundamentally changes the semiconductor landscape forever.

$INTC has caught up to and possibly overtaken $TSM on leading edge logic in 5 years - it should have taken a decade.

$TSM has a real competitor and it's monopoly position is breached. The #Taiwan Silicon Shield has a hole in it.

Congratulations to every engineer @Intel@Intel_Foundry - you changed history.

Sure, #1 thing is toxic financing structure/float dynamics.

Best example is current Neoclouds landscape:

- $IREN is basically trash, since they have $6,000,000,000 ATMs and virtually infinite dilution, likely selling into every rally (structural overhang)

- While $NBIS is now YTD 153%+, from optimal structures (eg. $NVDA direct funding, mix of convertibles, etc.).

- On the other hand, $CRWV has endless debt interest given they took out high interest rate loans to finance GPUs.

It's extremely nuanced, but you need to take a look at the float dynamics.

If they're legitimately a good company, then it might be a good idea to go long after all the existing holders get diluted to oblivion.

But if you care about your equity appreciation, it's a good idea to stay far away from toxic financing structures or toxic overhang (eg. debt interest, that eats away at a company FCF long term)

With smaller companies, they have this all the time, like

$SLNH, where there's new $500m ATMs on a $250m MC.

Or like $BKKT where there's endless dilution to fund executive pay.

With these companies you're basically transferring your money over to the company while influencers talk about them. So those are red flags.

With many software names like $SNAP, they mask stock-based compensation with profitability. So while the company optically looks profitable, you'll likely see the value of your equity decrease due to dilution.

There's endless types of these share structures you need to look when screening ideas.