Excited to FINALLY release toughest+most rewarding paper I've worked on...

….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)...

Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯

🧵

…a formal but ad hoc version of Tâtonnement was born…

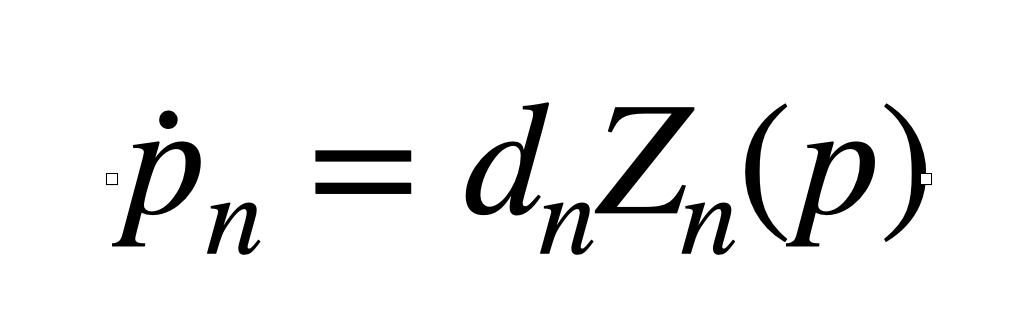

Samuelson put down a differential equation that says:

"prices in market n go up (dot p>0) if there is excess demand Zn(p)>0 in that market at some speed dn"

For researchers interested in U.S. banking and finance, we are sharing a new data resource!

It contains information on bank balance sheets, bank runs, and bank failures from the 19th century to the present:

Genuinely curious: where did all the geopolitical experts go who were absolutely certain back in April that the US and Iran would have a second shootout?

Terence Tao spent a year at the Institute for Advanced Study - no teaching, no random events of committees, just unlimited time to think. But after a few months, he ran out of ideas.

Terence thinks that mathematicians and scientists need a certain level of randomness and inefficiency to come up with new ideas.

Petrodollars! Nothing produces more heated discussion and, in my experience, less insight. Myths trump facts, because the actual data is a bit obscure --

But here is the most important thing to know. Before the Hormuz crisis, the flow of petrodollars had more or less dried up

1/many

Is the Phillips curve useful to make sense of inflation?

A.W.H. Phillips first postulated a negative empirical correlation between inflation and the level of economic activity. Looking at inflation in 2021-24---up and down---versus measures of unemployment---roughly unchanged---shows little correlation. Has the Phillips curve failed, yet again? No, it did not.

Friedman and Phelps, almost 50 years ago, clarified that this correlation should only hold keeping expected inflation fixed. Almost every account of how firms choose prices or bargain wages with their workers predicts that expectations would show up in a Philips curve. Moreover, those models of behavior further add that increases in marginal costs (supply shocks) would further shift out this relation. The empirical Phillips curve has for many decades meant a negative relation between inflation and real activity, controlling for expected inflation and supply shocks.

The left figure below shows on the vertical axis inflation, after controlling for expected inflation---mean and disagreement from a household survey---and for supply shocks---gas prices and global supply pressures. The horizontal axis shows a measure of slack in the labor market---the log of the ratio of unemployment to job vacancies. The Phillips curve held nicely and steadily throughout.

A criticism of that figure is that its is looking in the rear view mirror: the measure of supply shocks and the measure of slack were developed in the last few years and the data has been revised. The right figure does instead an out-of sample exercise. Estimate a regression of inflation on (i) expected inflation, (ii) the difference between the unemployment rate and the CBO estimate of its non-cyclical component, and (iii) the PCE energy price index. Do it on data pre-pandemic: 1984Q1-2020Q1. Using that estimated equation, predict inflation in real time from then onwards using the data releases available at the time of the forecast. The Phillips curve was a pretty good predictor of inflation throughout.

The Phillips curve was stable during the inflation surge, and it predicted well the movements in inflation, with expectations playing a key role in those predictions.

Notes: it is important to include the right measure of expectations to understand inflation-activity dynamics at a business-cycle frequency: the short-horizon expectations of households and firms. (For instance, the long-horizon expectations from professionals, or the expectations from models in policy institutions, as in my previous two posts, are the wrong measure.)

Sources:

(i) Section 3 in Reis "Why Did Inflation Rise and Fall in 2021-24? Channels and Evidence from Expectations"

(ii) The simple exercise on the left figure is inspired on the analysis of Bernanke and Blanchard “What Caused the US Pandemic-Era Inflation?”

(iii) The simple exercise on the right figure is inspired on @jadhazell "Comment" in the NBER macro annual 2025, which in turn built on Beaudry, Hou, and Portier "The Dominant Role of Expectations and Broad-Based Supply Shocks in Driving Inflation"

How much did public deficits contribute to the inflation surge of 2021-24?

A popular argument notes that inflation rose in the US by almost as much as in other OECD countries. Yet, the US had a large fiscal stimulus in 2021 that most other countries did not. Therefore, the US fiscal stimulus did not contribute to the inflation surge. Is that right? No, it is not.

To inspect this claim, you can use expectations data. By virtue of its mandate, the IMF is one of the best forecasters of fiscal variables and all economists pay attention to them. The IMF also forecasts inflation; during 2021-24, it was as right or as wrong as other institutions or surveys.

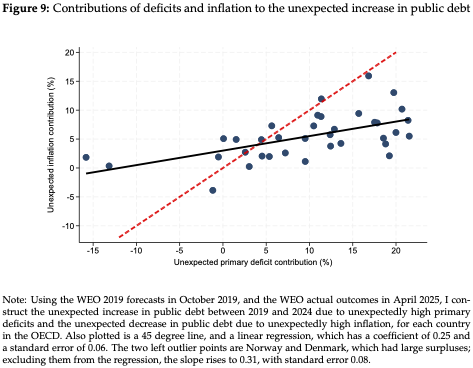

Start from the IMF's forecasts in October of 2019 for the next 5 years of how much public debt would grow and what would be fiscal deficits, interest rates, inflation, and growth rates. Then look at the IMF April 2025 reports of those actual variables. Subtract one from the other and you have how much of the unexpected increase in public debt was due to unexpectedly high deficits, unexpectedly high interest rates, unexpectedly low growth rates and unexpectedly high inflation.

The plot compares the unexpected high deficits with the unexpected high inflation terms for OECD countries, using the common units of their impact on the public debt.

For countries that ran higher unexpected fiscal deficits, inflation was also unexpectedly higher.

Some countries had their stimulus early, others only later. Somer larger, other smaller. Some had more, others less inflation. The accounts of the government let you consistently sum these differences over the 5 years to look beyond timings and to use consistent units. Thinking in terms of surprises and using expectations data allows you to compare countries with very different fiscal trajectories.

More generally, in all models and theories of inflation, including fiscal account, expectations are crucial. Using expectations data to inspect them is very informative.

Note: as with the initial claim, the plot is a correlation, not a causal statement.

Sources:

(i) Section 4 in Reis "Why Did Inflation Rise and Fall in 2021-24? Channels and Evidence from Expectations"

(ii) This simple exercise is inspired on the analysis of Barro and Bianchi “Fiscal Influences on Inflation in OECD Countries, 2020-23.”

BREAKING: Claude can now research like a Stanford PhD student.

Here are 9 insane Claude prompts that turn 40+ research papers into structured literature reviews, knowledge maps, and research gaps in minutes (Save this)

Day 5 of #Iran vs. U.S./Israel conflict (focus on Iranian strategic narrative):

🔹There is growing concern in Iran that decapitation has become a continuing war strategy rather than a one-off strike. Iranian sources believe Washington and Tel Aviv may attempt to target the heads of Iran’s government branches or members of the interim leadership council.

🔹This fear extends to whoever becomes the next Supreme Leader, with Iranian commentators referencing the precedent of Hezbollah, where Nasrallah’s successor was reportedly targeted shortly after assuming leadership.

🔹Israeli and U.S. strikes have continued across western and central Iran, including in cities such as Shiraz, Khorramabad, Kermanshah, Qom, Ahvaz, and Tabriz, with western regions and the capital remaining the primary focus.

🔹At the same time, Iranian sources acknowledges that several missile bases have been hit, including installations near Kermanshah. Damage to access points and infrastructure may be affecting the tempo of missile launches.

🔹The decline in Iranian missile strikes on Israel therefore appears linked both to operational constraints caused by Israeli air dominance and to Iran’s possible effort to conserve its remaining arsenal.

🔹Instead, Iran appears to be still prioritizing strikes on U.S. interests and regional energy infrastructure, aiming to raise the cost of the war for Washington and its regional partners.

🔹Iranian missiles have reportedly targeted additional THAAD early warning radars, including systems in Jordan following earlier strikes in Qatar and the UAE.

🔹If accurate, these attacks suggest a strategy aimed at degrading the regional missile-defense architecture that helps protect both U.S. bases and Israel.

🔹Iranian sources also claim that communications and radar infrastructure at several U.S. bases – including facilities in Bahrain, Qatar, Kuwait, Saudi Arabia, and the UAE – have been damaged.

🔹The objective appears to be disrupting command-and-control systems and weakening coordination between U.S. and Israeli air-defense networks.

🔹At the same time, Iranian air defenses appear to have had greater success targeting Israeli reconnaissance drones, including additional Hermes 900 systems.

🔹Some analysts suggest that improvements in Iran’s short-range air-defense network may be responsible for these successes, even though long-range systems remain degraded.

🔹On the proxy front, Iraqi armed groups have continued attacks on U.S. bases, even after heavy U.S.-Israeli strikes on PMF positions in Anbar, Diyala, and Samawah.

🔹Hezbollah has also continued its operations, including missile and drone attacks against Israeli targets in northern Israel and the Golan Heights.

🔹The Houthis, meanwhile, remain largely outside the conflict. Some Iranian sources claim they are being deliberately held in reserve as a deterrent against Saudi Arabia or the UAE joining the war.

🔹Energy warfare remains central to Iran’s strategy. QatarEnergy has declared force majeure and halted LNG production following attacks on energy infrastructure.

🔹These disruptions are reinforcing Iran’s effort to sustain pressure on global energy markets, particularly given uncertainty about how long the Strait of Hormuz can remain closed.

🔹At the same time, the war has begun to generate secondary instability across the region, including protests in Pakistan and Bahrain in response to the killing of Khamenei and the ongoing conflict.

🔹Within Iran itself, supporters of the Islamic Republic have continued to organize demonstrations calling for retaliation and resistance.

🔹Authorities are also warning against internal dissent. The chief justice has stated that any actions aligning with U.S. or Israeli objectives will be treated as wartime collaboration.

🔹Iran’s leadership is simultaneously attempting to reassure Gulf countries. President Pezeshkian and parliamentary speaker Qalibaf have emphasized that Iranian strikes are directed at U.S. forces rather than host states.

🔹Iranian officials have also reaffirmed commitment to the China-brokered 2023 Beijing agreement with Saudi Arabia, signaling an effort to prevent Gulf states from joining the conflict.

🔹China has reportedly dispatched a special envoy to the region to explore mediation options, reflecting Beijing’s concern over disruptions to energy flows through the Strait of Hormuz.

🔹Meanwhile, the Kurdish issue is emerging as a major security concern for Tehran. Kurdish insurgent groups have recently formed a broader coalition, raising fears that they could be used as ground forces against the Islamic Republic.

🔹Tehran has reportedly warned KRG officials that if Kurdish groups launch attacks from Iraqi Kurdistan, Tehran could directly target the Kurdistan Regional Government itself.

🔹The war has also produced a potentially dangerous incident involving Turkey. A missile launched from Iran was intercepted by a NATO air-defense system over Hatay while reportedly heading toward the U.S. base at Incirlik.

🔹Although the intention remains unclear, one interpretation is that Iran’s decentralized missile-launch structure may increase the risk of accidental escalation or uncoordinated moves.

🔹International monitoring agencies have also assessed damage near Iranian nuclear facilities. Satellite imagery shows limited damage near the Isfahan site, but the IAEA reports that no nuclear material has been affected.

🔹Concerns remain particularly high around the Bushehr nuclear power plant, where Russian personnel operate the facility and where nearby explosions have been reported.

🔹Inside Iran, discussions have also begun about the country’s future nuclear policy after Khamenei. Some argue that the war demonstrates the need for a nuclear deterrent and that the next Supreme Leader my move toward that direction.

🔹The Assembly of Experts continues deliberations on selecting a new Supreme Leader.

🔹Overall, the fifth day of the war suggests a continuation of existing patterns rather than a dramatic shift: sustained Israeli air operations inside Iran, Iranian efforts to impose costs on U.S. interests and regional energy markets, and a widening regional and proxy dimension to the conflict.

🔹The trajectory of the conflict increasingly resembles a prolonged regional confrontation in which both sides are attempting to reshape the strategic balance over time rather than achieve rapid military victory.

I spent time in Shenzhen last year and when I saw Merz come back from China saying Germans need to work more I immediately knew what broke his brain because I lived the exact same cognitive shock

my first week in Huaqiangbei I burned through 4 prototype iterations of a motor controller board for less than a thousand bucks total, back home a friend was working on something similar and spent over 12 thousand for a single revision that took almost two months to arrive

when you live that contrast in your own hands with your own project something permanently shifts in how you see the world and it goes way deeper than speed & cost

what Shenzhen actually built is a collective learning organism, imagine 20 PCB fabs 15 injection mold shops 30 component distributors and a hundred firmware freelancers all within a 2km radius, looks insanely redundant from the outside until you realize redundancy is actually information density in disguise

I watched this firsthand with an injection mold supplier I was working with, this guy had seen a hundred founders iterate similar thermal designs over 6 months so he proactively modified his tooling before I even opened my mouth, he knew what I needed before I knew what I needed, the intelligence lives in the relationships between the nodes and it compounds daily

the west thinks about manufacturing as a cost center you optimize by centralizing…

China accidentally built a distributed neural network of manufacturing intelligence where knowledge diffuses horizontally across thousands of agents faster than any single western company can process internally

so when Merz comes back and says we need to work a bit more I think he saw the problem but COMPLETELY misdiagnosed the solution, telling Germans to work harder is like telling a horse to gallop faster when the other side built a combustion engine

the gap is ARCHITECTURAL

it’s ecosystem density, you need a custom connector in Shenzhen you walk 200 meters, in Munich you send an email and wait 3 weeks

it’s iteration speed, parallel search vs sequential optimization at the system level, it’s risk tolerance, Chinese founders ship something broken on Monday fix it Tuesday ship again Wednesday while European companies are still in the approval phase for the pilot program of the feasibility study…

and Merz only saw the surface, what he missed is the tier 2 cities like Hefei Chengdu Wuhan replicating the Shenzhen model at scale right now

BYD going from irrelevant to outselling every european automaker combined in roughly 5 years, Huawei building its own 7nm chip under maximum sanctions when every analyst said it was physically impossible & behind all of that a government that treats advanced manufacturing as an existential national priority while europe debates whether AI needs another ethics committee

I think what we’re watching is the most asymmetric economic competition in modern history and most western leaders are still framing it as a productivity problem when it’s actually an ontological one

Europe & America are optimizing variables that China stopped tracking years ago meanwhile China is compounding on dimensions the west has no framework to even measure

Merz at least had the courage to name

it out loud and I respect that genuinely but working a bit more inside a broken architecture just means you arrive at the wrong destination slightly faster

#Iran Let us debunk some myths before social media starts to go crazy:

1) Iran has never been able to close the Strait of Hormuz. Furthermore, almost 80% of the traffic goes to China, Iran's largest partner. It would shoot itself in the foot.

This is what we got

And yes it made it within an hour, using "fast" mode in Claude Code Opus 4.6 + Grok-4.1-Fast + GPT-5-mini + Gemini-3-Flash + Codex-Mini. The API cost for Claude Code alone (at 50% discount currently) was $50. (Use API to track costs in this case; in general we are running multiple 20x Max subscriptions)

Again, we are running an autonomous generation pipeline, not human verification pipeline yet. I want to document all failures transparently too in real time, not report them ex post. (Interestingly I have never seen so many null effects papers!) I understand and respect if people disagree on this point. In fact, I have been hesitant to even post this. But have come to the conclusion that, on net, it's better to share the progress of the project transparently.

https://t.co/WJJEJen3XT

On today’s episode of what will AI replace and cause a violent selloff in: Transportation / Logistics companies

$RXO, $CHRW, $EXPD and others are getting absolutely smoked without any news.

Yesterday was CRE brokers, Tuesday was financial advisors, Monday was insurance brokers, and again everyday is SAAS. Sell it all

Super interesting!

"How Do Central Bank Governor Turnovers Affect Uncertainty and Lending Globally?" by Kristle Romero Cortés and Mandeep Singh.

"This paper studies how predictable transitions in central bank leadership generate uncertainty about the future policy environment and shape the international allocation of bank credit. Exploiting the institutional timing of fixed-term central bank governor appointments, we show that cross-border loan volumes increase by approximately $90 million, while total lending remains broadly unchanged. ...These findings highlight governor turnovers as a distinct source of economic policy uncertainty with global credit implications."

https://t.co/KRd1nWu9KT

Our interview with the two authors is also highly recommended. For instance, their perspective on the Powell-to-Warsh transition:

“From the perspective of our paper, what matters most is not the eventual policy outcome but the period of uncertainty surrounding the Powell-to-Warsh transition. Even now, while the successor is now known, markets and banks are still trying to understand how Warsh will behave in practice, how independent he will be, how he will communicate, and how closely he will align with the administration. That uncertainty can influence financial decisions before any policy change actually occurs.”

The full interview can be found here:

https://t.co/2CldL6Zajb

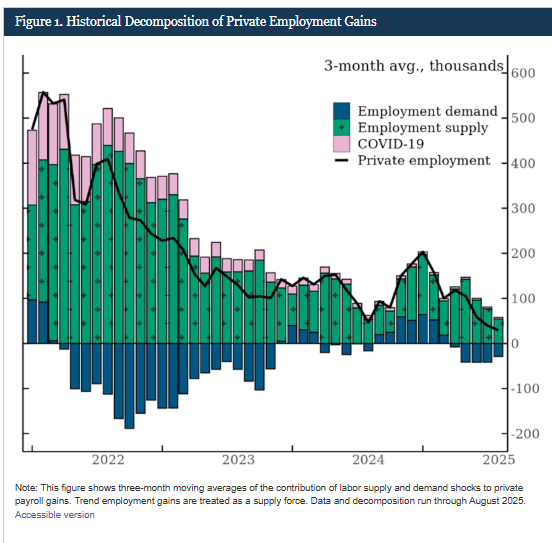

new Fed analysis blames the slowdown in US employment mostly on supply - i.e weak labour force growth.

Not the AI/productivity fairy

https://t.co/dK3GFt0bmF