VVV is up 9x YTD

The market's found its newest obsession: uncensored AI inference

Everyone's hunting for the next VVV

Here are 5 beta plays worth watching (plus 2 for the degens):

i am a huge proponent of privacy $ZEC and recently:

- shared the desci narrative

- caught onto $ONDO with a 2x

- money/credit markets like $AAVE $AERO $MORPHO

- $HYPE has been the strongest thesis along with several ai companies given their similar verticalization approach

there are alpha to some early projects which you should also explore

👇

1) @SeismicSys

privacy-first blockchain with normal ethereum developer experience. developers can build private apps without learning a totally new language or stack. most privacy chains require special tooling, new languages, or complex cryptography. Seismic tries to make privacy feel like normal Solidity/EVM development.

- $17M total raised (latest $10M led by @a16z crypto + @polychain + others in late 2025).

- testnet live since early 2025 (faucet + devnet activities ongoing, community is farming for potential airdrop).

- partners like @brookwellapp already routing stablecoin flows.

- narrative fit is perfect (privacy + real fintech adoption).

- this has the strongest VC signal in the list.

2) @tmrwfinance

creator lending against future AdSense revenue. youtubers and digital creators can borrow based on expected future income. Karat is more like banking for creators. Spotter buys catalog rights. Tomorrow uses a lending model, so creators can get capital without selling ownership of their content.

- very early/stealthier than the rest.

- part of @base ecosystem cohorts.

- fits creator economy + RWA lending narrative but less public traction/funding visible yet.

- underdog play vs bigger tokenized credit names.

3) @lightconexyz

trade the impact of events, not just whether events happen. it answers: “what happens to ETH/BTC/SOL if this event occurs?” prediction markets trade probability. options trade price movement but not clean event-specific outcomes. lightcone creates state-based assets, so users can hedge very specific scenarios directly.

- product site live.

- still pre-token/early.

- volves prediction market narrative into something more useful for hedging real outcomes.

- low competition in this exact flavor.

4) @techdollarhq

borrow against private tech shares without selling them. Employees or early investors in companies like AI labs or frontier tech firms can access liquidity while keeping upside. we recently saw @OpenAI employees sold $6.6b of equity and instead of selling, they can get a loan. Forge and EquityBee mostly focus on secondary sales or option financing. TechDollar focuses on lending against private equity, closer to margin lending for private startup shares.

- product page live with waitlist + clear borrower thesis (frontier tech conviction without forced exits).

- bridges TradFi private equity illiquidity with crypto-style credit.

- no big funding announced yet but clean positioning in the private shares as collateral narrative.

5) @agra_gg

secondary market for tokenized private credit. it lets holders exit before maturity instead of being stuck until redemption. most tokenized credit platforms only solve issuance. Agra solves liquidity. Its yield-based orderbook also fits bonds better than normal AMMs or price-based trading.

- beta live on Ethereum right now with real markets like Anemoy/Apollo credit fund and others.

- tokenized private credit is one of the hottest RWA sub-narratives ($14B+ already in the space).

- first-mover liquidity layer here is real product alpha.

6) @OrnnExchange

commoditizes GPU access. it treats compute like oil or electricity: a scarce resource that should be priced, traded, and accessed efficiently. most GPU projects are just marketplaces. Ornn’s bigger idea is that GPU compute becomes a financialized commodity layer for the AI economy.

- $5.7M seed (oct 2025).

- index already on Bloomberg Terminal.

- live spot pricing + derivatives coming.

- perfect AI infra narrative, compute as the new oil.

- regulated U.S. venue angle is big for institutions.

7) @numoforex

fx infrastructure for frontier markets that gives currency hedging tools to markets where normal fx products are missing or too expensive. most fx platforms serve large institutions or developed markets. Numo targets the places where fx risk is most painful but least served.

- product live with actual markets and volume.

- zero-fee on/off-ramps.

- targets painful real-world FX risk in underserved markets.

- one of the few actually shipping frontier FX infra.

8) @meanwhile

bitcoin-native life insurance. it connects long-term $BTC holding with long-term financial planning. most bitcoin products are trading, lending, or custody. Meanwhile treats btc as a long-duration savings asset, closer to insurance and retirement planning.

- massive $82M raise (oct 2025).

- first and only licensed BTC-native insurance carrier.

- huge signal for BTC as serious savings vehicle beyond trading/lending.

- institutional partner push incoming.

9) @merit_systems

from builder reputation to AI-agent commerce. it started by tracking and rewarding open-source contribution, then moved toward payments/commerce for agents. most reputation systems are static badges. their newer direction is more dynamic: enabling AI agents to transact, earn, and interact economically.

- shift to agent economy is perfectly timed with AI agent hype.

- live tools (AgentCash, Poncho, directories).

- enables permissionless agent-to-agent commerce.

- narrative tailwind is massive.

10) @StreetFDN

tokenizing startup equity. it builds standards and infrastructure to make private startup shares easier to issue, manage, and transfer. equity tokenization usually focuses on public stocks, funds, or bonds. Street targets startup equity, which is illiquid, paperwork-heavy, and structurally hard to access.

- claims 150+ startups tokenized.

- solves paperwork + access issues in VC equity.

- fits the broader equity tokenization wave (SPV wrappers are the current compliant path).

- early mover on actual startup (not public stock) side.

Weekly|Why Memory / CPU Rally Accelerated and Outperformed Optics, $SMTC & $AMD Deep Dive, $DDOG , $APP , $LITE , $COHR , $PLTR , $NET , $RKLB , $RDW

A week dominated by tons of earnings reports and a relentless rally in AI semis, especially memory and CPU stocks. As our long-term readers would recall, we have consistently highlighted the “mis-positioning” by many US funds, which significantly underweight semi/hardware while overweighting software/internet, and, more importantly, they are starting to adjust. This was confirmed by Coatue’s latest presentation, in which they disclosed that Semis + Infra’s long exposure % jumped to 58% as of late, up from 35% at the beginning of the year. This is at the expense of Software, Internet + Other exposure decreased materially.

Meanwhile, Altimeter’s Brad Gerstner openly justified the valuation of memory stocks and said he will be on a podcast with the Micron CEO in a few weeks to discuss how the shortage could last until 2028/29 or even longer, suggesting a material shift in his fund’s positioning, too. We sense that the attitude change by these two reputable US TMT funds has ignited FOMO among other investors, including both HFs and LOs, thereby accelerating stock moves lately.

Under this assumption, we think the performance gap between memory/CPU and optics is explanatory. For these funds that missed out on the AI semi rally largely since 2023, MU/SNDK and INTC/AMD are at least names they have known for years, compared to LITE/COHR, which were smaller in market cap and more difficult to understand from a technology perspective. Moreover, MU/SNDK’s lower valuation multiples on paper are a big help. We believe the LTA announcement during SNDK earnings gave the funds we mentioned above a major reason to chase the names here. The market is starting to discuss that once LTAs exceed 50% of the mix, the stock can no longer be viewed as cyclical. We are increasingly hearing investors benchmarking NAND valuation to HDD at 8-10x FCF. You’ll probably recall the LTA Report we published—the first in-depth LTA Report in the market —which laid out the case for why this LTA cycle is different from previous ones.

https://t.co/nxvthwLFRu

In general we have been long in all three AI beneficiary segments and would suggest investors exercise caution in names that are going vertical in the near term, while paying closer attention to other areas that are being neglected. On the Premium Research side, we published an SMTC initiation and an AMD deep dive, among others, validating our conviction in all these segments. Please contact [email protected] for more information.

This Week’s Reports

Review|DDOG 1Q26: Big Guidance Upside Surprise, No Growth Cliff Concern Anymore. We were bullish into the event but earnings were even stronger than our higher-than-consensus estimates. 1Q26 met expectations but the real story was the guide — 2Q26 +30% YoY (implying ~35% with the typical 5pt beat) and FY26 raised to 26-27% (low-to-mid 30s on actuals), effectively retiring the 2H OpenAI cliff narrative. Two new hyperscaler AI training wins reinforce DDOG’s tech moat over in-house and OTel alternatives.

https://t.co/pjOtMF4vUs

https://t.co/HSr0wf8Fr2

Review|APP 1Q26: Management Guides E-commerce to ~20% of US Revenue, +25% QoQ. Revenue +59% YoY in line; the more important read is the explicit 2Q26 guide of e-commerce +25% QoQ with April marking a record month — exactly tracking our Preview’s +23% bogey. With European GA in June and CTV emerging as a first-time upside contributor, the e-commerce ramp is clearly inflecting and gaming shows no deceleration.

https://t.co/Ee8T7RwSSP

https://t.co/CKrwHCHlLD

Review|RDW 1Q26: Headline Miss, Clean Margins, Prime Optionality. Revenue grew 58% YoY but missed by 7%, with after-hours weakness driven by the $350M ATM rather than the print itself; underneath, GM expanded to 26.6%, backlog hit a record $498M, and book-to-bill was 1.92x. Andromeda (~$6B opportunity), Golden Dome (VLEO/GEO prime), and Lunar Power Grid reframe RDW from components supplier toward space infrastructure prime — the dilution is buying optionality, not survival.

https://t.co/WjK5P4x7R2

Selected Premium Report Snapshot

...

Detailed Report

https://t.co/OYSa2YyJGv

The Hoot Oracle has spoken.

My egg aligned: BRICK

The oracle has not chosen you, but your alignment is still sealed. The egg remembers.

Will the oracle choose you? Claim your Hoot alignment → https://t.co/JGxmWVsbXx

By @uhootdotart

Gonna share my 2026 hedging thesis (long tweet warning)

I call it: how to get paid even if crypto bleeds and tech beta starts vomiting into year end.

Strictly my personal opinion. All info below are based on PUBLIC sources. Not financial advice, DYOR

With crypto potentially facing another 20-40% drawdown into year-end, I’m increasingly convinced that select oil and tanker equities are one of the cleaner hedges right now.

AND NO, this isn't another tweet about gambling long or short on crude.

The play is shareholder yield: dividends, supplemental dividends, and buybacks, backed by strong free cash flow, manageable leverage, and real asset exposure. Sized right, the basket could return 20-30% cash this year.

My thesis is not “which oil stock does 2x or 5x.”

It’s defensive: these companies are generating exceptional cash in the current freight and energy setup. Many run with low single-digit net debt to EBITDA, and select names can deliver double-digit shareholder yield through 2026 if rates stay firm.

That’s real cash flow while crypto chops, and honestly I’d rather have that than be all-in into tech growth names that offer zero yield buffer when risk assets correct.

Buying now can still qualify you for upcoming quarterly dividends, but you need to own shares before the official ex-date. Make sure you check share buyback policies too, because that’s where the real combo comes from: dividends + buybacks + potential share price gains.

ALSO AN IMPORTANT TAX NOTE everyone should know:

> US taxpayers: want the lower qualified-dividend tax rate instead of getting cooked at ordinary income rates? Usually you need to hold shares unhedged for 61+ days within the 121-day window around the ex-date.

> Non-US investors: normal US dividends can get hit with a 30% withholding tax slap. BUT many tanker names are foreign-domiciled, so the tax haircut can be much lighter. Don’t be lazy though, check domicile, broker, and local tax before celebrating.

The near-term dividend window is worth watching, but I’m separating confirmed declarations from forecasted ex-dates.

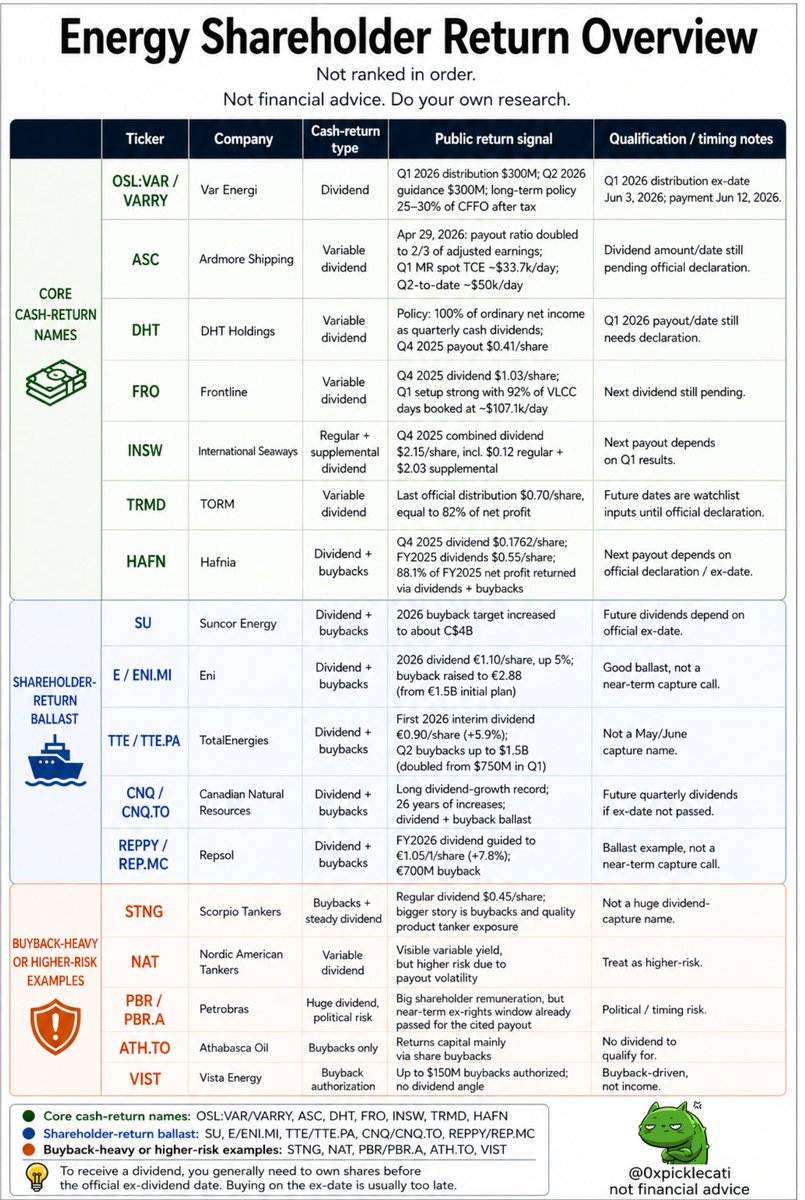

Confirmed/recent shareholder-return updates:

> ASC announced on april 29 (literally yesterday) that it is doubling its payout ratio to two-thirds of adjusted earnings, effective Q1 2026. Q1 MR spot TCE was around 33.7k/day, and Q2-to-date was around 50k/day. Dividend amount/date still needs official declaration.

> Var Energi (OSL:VAR/VARRY) has a confirmed 300M Q1 2026 distribution payable June 12, with another 300M guided for Q2.

> Eni (E/ENI.MI) confirmed a 2026 dividend of €1.10/share and raised its buyback plan by about 90% to €2.8B.

> TTE raised its first 2026 interim dividend by 5.9% to €0.90/share and doubled Q2 buybacks to $1.5B. Not a May/June capture name, but good shareholder-return ballast.

For the tanker watchlist:

> DHT has one of the cleanest payout formulas: 100% of ordinary net income as quarterly cash dividends. Q1 payout/date still needs declaration.

> TRMD’s last official distribution was $0.70/share. Any May dates floating around are watchlist inputs until TORM officially declares.

> FRO paid $1.03/share for Q4, and Q1 looks strong with VLCC days booked around 107.1k/day. But the next dividend is still pending.

> INSW’s most recent payout was $2.15/share combined ($0.12 regular + $2.03 supplemental) for Q4 2025. Next payout depends on Q1 results.

> HAFN (product/chemical tankers) raised its latest quarterly dividend to $0.1762/share and is seeking a new 10% buyback mandate at the 2026 AGM. Next payout pending.

> STNG is more buyback + quality product tanker exposure than a huge dividend-capture name.

> NAT has visible variable yield, but I’d treat it as higher risk.

The basket has 4 buckets:

Variable/formula-based tanker payouts: ASC, DHT, TRMD, HAFN, FRO, INSW, NAT

(highest dividend torque in the basket, but also the most variable)

Product tanker buyback discipline: STNG

(still shipping exposure, but more buyback + quality operator than huge dividend capture)

Big energy shareholder-return ballast: SU, TTE, E/ENI.MI, CNQ, REPYY/REP.MC, OSL:VAR/VARRY

(less sexy, but more grown-up hedge: dividends, buybacks, scale, and balance sheet durability)

Buyback/growth oil names: VIST, ATH. TO

(not dividend names, but buybacks can still create shareholder yield without sending you a cash dividend)

see the table below for the full visual overview with qualification/timing notes on every name (including higher-risk examples like PBR)

IMPORTANT: this is not a free dividend glitch.

Stocks often adjust down around the ex-date, sometimes more than the dividend itself. variable dividends can disappear if rates collapse. Buybacks only matter if management buys at sane prices.

So, the setup I like: own cash-return machines while the market is still underpricing how long energy cash flow can stay strong.

Why this hedge over the usual alternatives:

> tech stocks: still risk-on beta, no yield buffer

> bonds: help in recession, messy if inflation/oil risk stays sticky

> cash: safe but real returns are unexciting

> long dated puts: clean hedge, expensive theta bleed if timing is wrong

The tanker angle is different because strong Q1/Q2 cash flow can come back as dividends, supplemental dividends and buybacks. (not fixed, but in the right rate environment, cash returns fast)

Even if Hormuz reopens tomorrow, the system doesn't reset overnight:

> inventories still need to rebuild

> refined products can stay tight

> trade routes can stay inefficient

> Q1 cash flow already happened

> Q2 rates are the next thing to watch

Crypto for asymmetric growth, oil-linked yield for cash flow ballast. I don't need every hedge to 5x, sometimes the boring trade just keeps paying you while crypto does whatever crypto does.