@BetterIRR Two key positives: SuperCom replaced the incumbent provider after 20+ years, and just like Sweden's contract expanded from $17M to a potential $75M, Norway's opportunity has grown from $1.8M to a potential $6.1M

@CapstackCapital It's strange because you know the investment thesis in detail,and you've also, in a way, helped spread the word about it.I already have a significant position in SPCB. I'd like to own more, then I remind myself that it's an illiquid nano-cap that's still unknown to most investors

@LocodlDividendo Me cuesta trabajo entender cómo alguien puede llevar 50 acciones en cartera, dominar cada una de ellas al detalle, seguir sus resultados trimestrales y anuales, sus competidores, los múltiplos de sus competidores, riesgos y ventajas de cada una de ellas, etc.

Another insider purchase at Comstock $LODE

Director (Pei Steven Yu-Tsung) at Comstock Inc. $LODE purchased $1.02M (3rd largest purchase, out of 3).

This increased their listed holdings by 15%.

3 other insiders also purchased the stock in the last 30 days.

$SPCB project value ranges from $17M to $75M published budget with upside reflecting potential expansion of # offenders monitored, add. capabilities such as alcohol monitoring, PureOne GPS solution & Pure Officer mobile device for supervising officers.

https://t.co/OdVnOMoDqs

$SPCB is confirming a major bull case that its EU contracts are much larger than the reported figures. A large positive discrepancy applies to Germany as well.

https://t.co/ZNGYKQsk2y

@ASESOREFA Buscando la lógica del Mercado, creo que està descontando que ese crecimiento no va a ser sostenible en el tiempo y anticipa una desaceleración, tanto por demanda como por aparición de competidores como Amazon y Google que han desarollado sus propias TPU, Procesadores, etc.

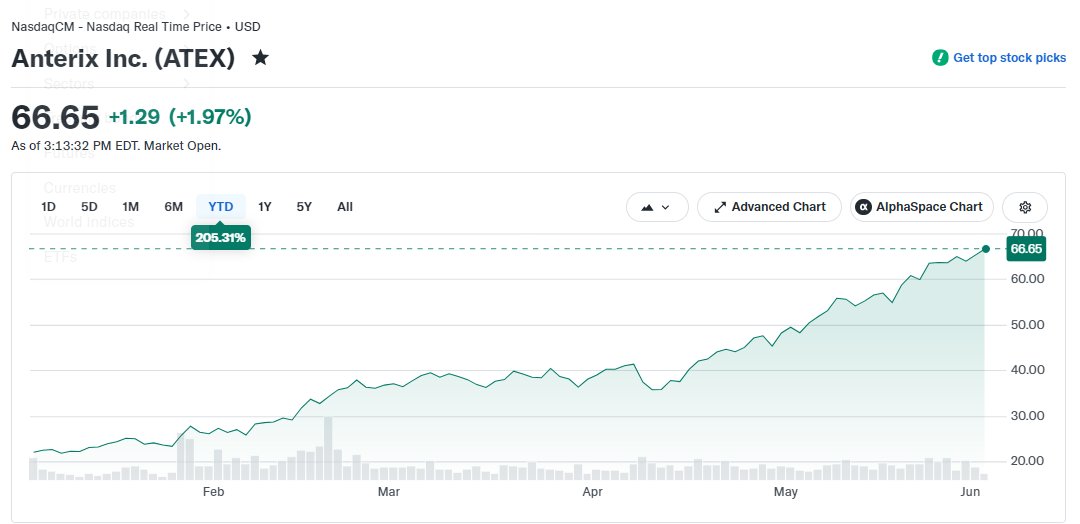

@dan_tmt It has been one of the most asymmetric investments I’ve ever seen. The rally has been significant, yet it still remains cheap. The company itself has valued the spectrum at between $2 billion and $7 billion, and just a week ago it was trading at only 0.44 usd/MHz-POP.

🚨 La mayoría de la gente juega al Monopoly de la vida… pero nunca compra propiedades ni activos que generen ingresos.

Solo pasa por la casilla de salida, cobra 200 euros, paga al banco (o al rico de turno) y reza por no caer en la cárcel.

@jbegno1 Lo preocupante de esto es que el Loco tiene unos 55K seguidores en X, lo que demuestra la escasa cultura financiera que existe en la comunidad hispanohablante (aunque la inmensa mayoría de sus seguidores son españoles). Este hombre transmite una visión equívoca de la inversión.

$LE at $10. Oaktree and Ares paid $300M cash for half the brand IP last week. Add ~$50M in net cash and the assets alone exceed the $311M market cap.

The operating business, $1.3B in revenue at record 49% gross margins, is implied below zero.

LE also holds an exchange right on its JV stake. If WHP ever IPOs or sells, LE converts at a 13x contractual floor. That floor alone values LE's half at $292.5M against a $311M market cap. No expiry.

The current price requires 86% odds of the worst outcome. I put it at 10%.

Anterix Inc $ATEX operates as a highly specialized wireless spectrum landlord that holds a federally protected monopoly over the 900 MHz band for utility-grade private broadband networks. A recent landmark FCC ruling expanded their spectrum capacity to 10 MHz, effectively doubling the bandwidth and pushing the theoretical valuation of their nationwide asset portfolio as high as $7 billion. The business is also expanding beyond critical electric grid modernization into the massive direct-to-device satellite communications market through strategic technical partnerships with Qualcomm and Lynk Global. With the stock currently trading at a steep discount to its underlying spectrum value and private infrastructure funds hunting for long-term cash flows, will Wall Street recognize this hidden monopoly before a lucrative buyout takes it private?

@BetterIRR Outstanding execution. Management has delivered every milestone on time and transformed Vodafone Spain. One of the best management teams I've seen.

$ATEX - Top Holding Equity Small Caps FI

Pudiera parecer que Anterix está subiendo mucho pero sigue cotizando a 0,45x MHP-POP cuando el management te está dando un rango de valoración $2,5bn-$7bn, es decir, 0,8x MHP-POP a 2,2x MHP-POP.

Si damos por bueno el rango bajo del management, el múltiplo aún debe casi duplicar😀

No tengo nada más que decir...