I want to post my predictions for 2ish years horizon.

AI stock bubble collapses due to fundamentals not working out with the assets prices. Overleveraged and overdebted market will go down in a massive correction by the like of 2008.

Most AI companies will burn, although some will survive. Specifically, cloud providers, chip makers are among the likely to survive. Inference companies like Anthropic and OpenAI are likely to be bailed out by gov and to default otherwise. Companies sitting in the API level will default.

Enshittification of the internet will reduce although it will still be above pre-llm era.

AI will be most used in niche scenarios like support chat bots, on device helpers (like Apple does), and specific needs like medical imaging. All of that to be mostly powered by open source or at least on-device models. On-device LLM will be default LLM in general.

People would still use AI for coding but not all people and certainly not for all purposes. Software professions would be recognized to be human-first. Even more so with artistic professions.

The most advanced models will be expensive and realistically available only for governments, research institutions, and other elite use. Both due to price tag and secrecy concerns.

AI exposure in education will continue to worsen the education quality of graduating students. In mitigation attempt, Universities and schools will be switching to almost only inclass paper assesments.

Nicolai Tangen, CEO of Norges Bank Investment Management pressed IBM CEO Arvind Krishna directly on whether AI is a bubble (Save this).

And Krishna responded with what has become known inside financial circles as the $8 trillion math problem.

A single gigawatt of AI data center capacity filled with accelerators, liquid cooling, and power infrastructure costs roughly $60 to $80 billion to build and populate.

The industry has committed to more than 100 gigawatts of buildout globally.

That is $6 to $8 trillion in capital expenditure and because AI grade hardware depreciates on a five-year cycle, that entire sum must be effectively replaced and refreshed every five years.

To service the interest on $8 trillion in capital at a conservative 10% borrowing rate, the AI ecosystem would need to generate approximately $800 billion in annual profit, a number that currently exceeds the combined net income of every large technology company in the world.

Goldman Sachs estimates $7.6 trillion in aggregate AI CapEx between 2026 and 2031 alone, and Reuters Breakingviews has flagged that even if the capital is available, physical bottlenecks power permits, land, cooling infrastructure, and electrical grid connections mean that half of the planned data center projects are being cancelled or delayed before they ever go live.

Krishna also raised a second, structurally distinct concern that markets have largely ignored.

He argued that the largest foundation models, GPT, Gemini, Claude, Llama are converging toward commodity status.

When a product is a commodity, switching costs collapse.

When switching costs collapse, pricing power evaporates and margins compress regardless of how much capital was spent building the capability.

Morningstar's equity research team conducted a review of 132 technology companies in 2026 and found that AI had caused moat rating downgrades across roughly 40 major stocks concentrated in enterprise software, IT services, and SaaS with Adobe, Salesforce, Workday, and ADP among the companies whose competitive moats have materially weakened.

The implication is that the companies spending the most on AI model development may be building an asset that is simultaneously the most expensive to produce and the most difficult to monetize with durable margins.

This bear case is serious but it is also incomplete and that is what makes Krishna's framing so important to understand precisely.

When pressed further, Krishna explicitly said he does not believe there is an AI bubble in the technology itself only in a subset of the infrastructure capital that is being deployed against speculative assumptions rather than proven demand.

He draws the same analogy, the fiber optic overbuild of the late 1990s. Dozens of companies went bankrupt laying cable that nobody was using.

And yet that exact "wasted" infrastructure became the physical backbone of every cloud company, every streaming service, every mobile network, and every modern AI training cluster that followed.

The builders lost, the infrastructure won.

And the companies that were built on top of it, Amazon, Google, Netflix, Salesforce compounded for two decades.

The question, as Krishna framed it, is not whether AI is real.

It is which capital deployment earns a return versus which gets stranded and crucially, whether you own the stranded assets or the companies built on top of them.

On winners, Krishna was direct that distribution is the moat on the consumer side, and enterprise is wide open.

The data supports this, Meta with 3.3 billion daily active users across Facebook, Instagram, and WhatsApp is building AI into a distribution network that no startup can replicate at any cost.

Meanwhile, the productivity evidence arriving in real time is beginning to challenge the bear case's revenue projections.

Jensen Huang just showed on stage at Computex that GitHub commits, the universal measure of global software output nearly tripled in the first months of 2026, effectively converting $3 trillion in developer salaries into $9 trillion in productive output.

That is measurable, real time economic value already flowing through the system and it feeds directly back into token demand in a compounding loop that Krishna's static CapEx math does not fully capture.

Has hit the nail on his head where Indian ITeS starts to look bleak but Indian economy even more with such a high CAD and no real meaningful momentum on manufacturing front

You can’t make this up:

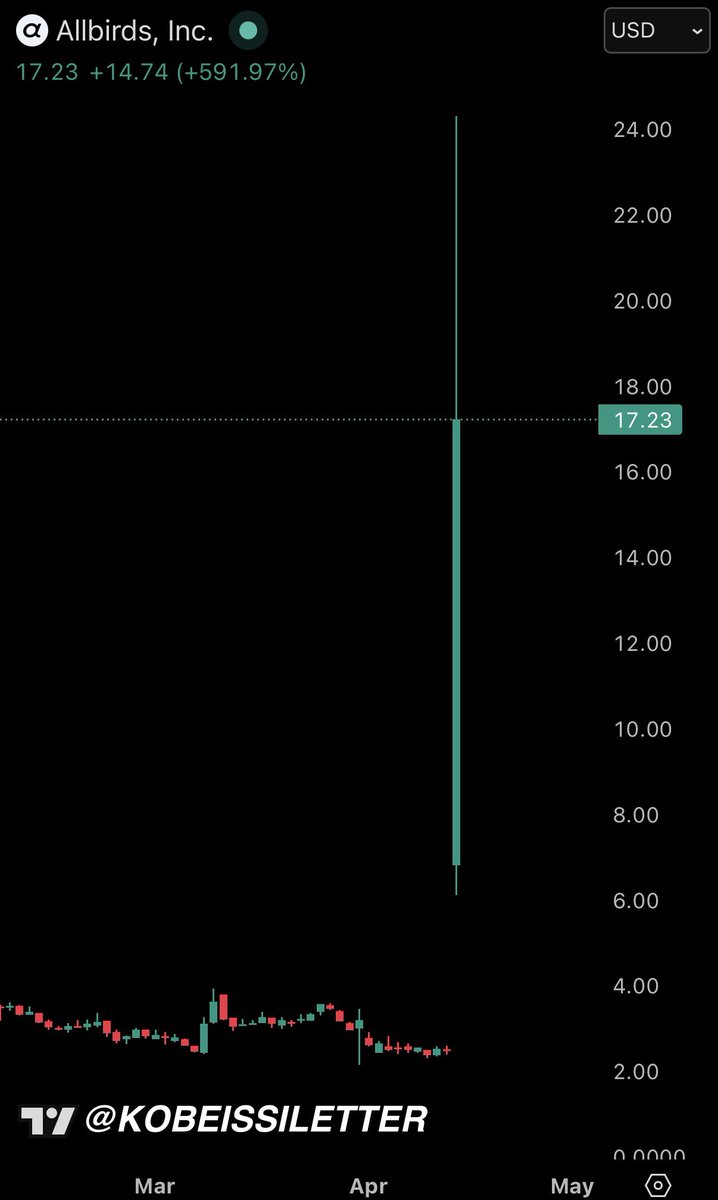

Allbird stock, $BIRD, was down -99% from its record high as of yesterday as the shoe company was collapsing.

Today, Allbirds stock is up as much as +875% after entirely rebranding as an AI company.

This includes selling all of its brands and footwear assets and rebranding to “Newbird AI.”

And, the company will use a $50M convertible financing facility to “acquire high-performance GPU assets.”

Even shoe companies are moving into AI.

#MustRead ‼️

Every generation of Indians had one constitutional moment that defined their future.

For South India, this is it. Not the Emergency. Not liberalisation. Not even the 1971 freeze. THIS Bill. THIS delimitation. THIS Commission.

Bill No. 107 of 2026, 131st Amendment Bill. What’s buried inside those 5 pages will affect South India’s political future for the next 50 years.

Let’s see exactly what’s written & more importantly, what’s deliberately NOT written.

(1/8)

I asked Claude which era of tech workers faced the most brutal market conditions, and who actually had the hardest path to building real wealth in their lifetime:

- The Dot-Com Pioneers (1995-2001)

- The Web 2.0 Builders (2004-2010)

- The Mobile App Gold Rush (2010-2016)

- The SaaS Boom (2016-2021)

- The AI Pivot (2022-Present)

And this is what Claude concluded

I just asked Gemini 3.0 to analyze the $GOOG vs $NVDA dynamic. Read this. I could be generational wealth changing.

Everyone is comparing Gemini 3.0 vs GPT-5.1 on benchmarks. You're watching the wrong scoreboard.

The real war isn't about who is smarter. It's about who creates the "Prisoner's Dilemma" that kills Nvidia's 75% margins.

I spent the morning mapping this out like a Cold War game theory scenario. Here is the board. 👇

1/ Right now, Nvidia is the "Arms Merchant." They sell the H100s. Everyone pays the tax.

Their entire stock price assumes they keep ~75% margins forever.

But Google just made a move that changes the physics of the board. They aren't trying to sell chips. They're trying to make chips irrelevant.

2/ The setup is simple:

Nvidia makes money by keeping hardware expensive (High Margin). Google makes money on ads/services, so they want compute to be free (High Volume).

These goals are incompatible. In Game Theory, this is a "Structural Conflict."

3/ For years, Nvidia had a "Hold-Up" on the industry.

You want to do AI? You pay the Nvidia tax because CUDA is the only software that works.

It was a monopoly based on fear: "Switching to another chip is too risky. What if the code breaks?"

4/ Enter Gemini 3.0.

Google trained it on TPUs. They run it on TPUs. They don't pay the Nvidia tax.

This means their internal cost-per-token is structurally ~50% lower than OpenAI's (who has to pay Microsoft, who has to pay Nvidia).

5/ (This is the part that clicked for me)

Google creates a "Price Ceiling."

If Google sells intelligence for $1, OpenAI can’t sell it for $2 just because they use expensive Nvidia chips.

OpenAI must match the price to survive. But they can't. Not while paying Nvidia's margin.

6/ This traps Nvidia’s best customers in a corner.

To match Google’s prices, Microsoft and OpenAI are forced to build their own chips (Maia) to stop paying Nvidia.

Nvidia’s own pricing power is exactly what is incentivizing its customers to destroy it.

7/ So where does the equilibrium settle? I ran the scenarios. It leads to a split.

Zone A: Discovery (Nvidia Wins)Researchers still use Nvidia because speed matters more than cost.

Zone B: Utility (Google Wins)Once a model works, you run it on cheap custom chips.

8/ You can see the strategies shifting in real-time right now:

Google: Aggressive subsidies ($350k credits) to get startups to rewrite their code off CUDA.

Nvidia: Bundling software (NIMs) to make leaving impossible.

It's classic "Free Drugs" vs "Golden Handcuffs."

9/ If you are building in AI, here is the "Tripwire" to watch.

Ignore the benchmarks. Watch the Token Price.

If GPT-5 class pricing drops below $2.00/1M tokens, the "Nvidia Tax" is mathematically dead. The market is fleeing to custom silicon.

10/ The one question to ask your CTO tomorrow:

"If we had to switch from Nvidia GPUs to Google TPUs or AWS chips tomorrow, would it take us 1 week or 6 months?"

If the answer is 6 months, you are the "sucker" at the table paying the tax.

11/ The takeaway:

In a gold rush, it's usually good to sell shovels.

Unless your biggest customer decides to invent a steam shovel just to stop paying you.

Game on.

Japan Is Bracing for a Hard Transition

Japan isn’t rolling out a ¥17 trillion plus package because it suddenly rediscovered big government spending. It’s doing it because the country is in the middle of a very delicate shift, moving from a deflationary, low rate world that lasted 30 years into a higher price, higher rate environment that Japanese households simply aren’t built for.

Finance Minister Satsuki Katayama told reporters recently that the package will exceed ¥17 trillion, not just meet it. the intention is to relieve the blow of rising living costs and pour money into future growth sectors like AI and semiconductors, areas Japan can’t afford to lag in as the global economy fractures and supply chains get rewired.

In other words, this isn’t pure stimulus. It’s stabilization. Japan is trying to help households absorb higher prices without forcing the central bank to slam on the brakes, and at the same time fund the industries that must anchor its next decade.

Why This Matters Far Beyond Japan

The U.S. will be watching this closely, not out of curiosity, but because Japan is effectively running a dress rehearsal for challenges the U.S. will face in a few years.

The first thing markets will watch is the bond market. If a package this large pushes JGB yields higher, even modestly, that shifts the global flow of money. Japan is still one of the world’s biggest foreign holders of Treasuries. If returns at home start to look a little better, capital quietly migrates back and that puts pressure on the long end of the U.S. curve at a time when Washington is issuing record amounts of debt.

The second layer is the yen. For decades it’s been the world’s preferred funding currency. If Japan’s mix of fiscal spending and BOJ normalization makes the yen firmer or more volatile, the carry trade unwinds. And when that unwinds, it doesn’t just hit Japan, it tightens financial conditions everywhere. Equities feel it. Credit feels it. Anything that relies on cheap global liquidity feels it.

And then there’s the deeper, slower second order effect. If Japan pulls this off, if it can run a stimulus package greater than $110 billion, keep households afloat, and prevent its bond market from convulsing, it gives every other advanced economy with aging demographics and heavy debt a green light to push fiscal harder. It broadens the perceived safe zone for deficit spending in a world where monetary policy is no longer the main stabilizer.

That’s the real reason this matters. Japan isn’t just trying to manage its own economic transition. It’s showing the rest of the developed world what the next era of economic policy might look like and whether the global system can actually handle it.

Japan is the test case. The U.S. is the audience. And the spillover effects will tell us more about the next decade than the headline number ever will.

What’s the matter with India?

It is not inevitable that India be poor. Its people are certainly capable of being extremely productive. Indian immigrants to the United States and elsewhere have been very successful. India’s government has been stable since independence, and largely democratic throughout. While their growth rate has picked up, they have not had the booming success of China. India was socialist for a long time; but then, so was China. Why isn’t India a developed country yet?

To suggest a monocausal explanation would be an exercise in arrogance; India has many problems, and there is no one simple trick to growth. I nevertheless hold that much of India’s stagnation is due to its judicial system.

The facts are simple. There are at least 50 million cases pending — nobody knows how many for sure. The Supreme Court has 69,000 piled up, waiting for resolution. Of these, 18,000 have been pending for more than thirty years. Every family has a horror story. I have a friend whose dad, near the beginning of his career, was named in a suit involving a bank. Growing up, every few years his dad would be called to appear in court. My friend is 40 now. His dad has retired. The suit remains ongoing.

The Indian government estimated that, at current capacity, it would take 324 years to clear all of the cases. That was in 2018. Since then the number of pending cases has doubled. India has one of the lowest ratios of judges to population in the world, with 21 judges for every million people. Surprisingly, this is an improvement over the past — in 2002 the ratio was 10 for every million. The EU average is 200 per million, and the US 150 per million. One reads with grim amusement concern that a low number of judges — say, 100 per million — will endanger the rule of law in Ireland or Denmark. If that is what it takes to endanger, then rule of law in India is positively extinct.

Nobody knows the average time it takes a court case to be resolved for sure, but it is somewhere around five years for it to be resolved by the high courts (the second tier of courts) and 13 years for the Supreme Court. 40,000 new civil suits are filed every day, covering everything from land disputes to layoffs to bankruptcy. 66% of all pending civil cases involve claims and counterclaims over who owns what land. The upshot of this is that firms cannot resolve disputes through the courts. They must instead turn to extrajudicial methods, and the most common of them is keeping the business in the family.

In the late 2000s a team of researchers – Bloom, Eifert, Mahajan, McKenzie, and Roberts – conducted a randomized controlled trial on management quality in Indian textile mills. Prior work by Bloom and Van Reenen had shown that family run firms in the West, in particular those run by an eldest son, were poorly run compared to professionalized businesses. We would not be able to tell in India, however. Of the 126 firms they surveyed — a comprehensive census of the firms in the towns near in and around Mumbai — every single one of them was family run. The single strongest predictor of firm size was not productivity, revenue, or profitability. It was simply the number of male family members in the family. These are not simple mom-and-pop shops either, with but a few employees. As Bloom et al write, “These firms are also complex organizations, with a median of two plants per firm (plus a head office in Mumbai) and four reporting levels from the shop floor to the managing director. In all the firms, the managing director was the largest shareholder, and all directors were family members. Two firms were publicly quoted on the Mumbai Stock Exchange, although more than 50% of the equity in each was held by the managing family.” (p. 9)

The experiment by Bloom et al was to test how much management mattered by randomly assigning some firms to receive management training. They found that a firm receiving the management training increased their annual profits by 17%, or almost $300,000 a year. Since these are extremely simple interventions — things such as “write down what types of yarn you have and how much” and “have a schedule for repairing machines”, one wonders why the companies never adopted them on their own.

The commonly cited reason by firm owners and plant managers was that they simply didn’t know that that was what one should do. But not knowing is arguably downstream of firm owners being unable to delegate. Basically all decision making is done by the owners, and middle managers are not free to, nor are they incentivized to, introduce improvements of their own. The root of this is the fear of expropriation by the managers, for which the owners would have no timely recourse. If the courts were efficient enough to be a check on fraud, owners could trust their managers and implement better practices. Instead we are stuck in a world which no one wants.

It is little surprise that, within a given industry, resources are misallocated. The most productive firms are too small, and the least productive too large. Hsieh and Klenow (2009) kicked off a literature on quantifying how much misallocation reduces output, and while the figure of a 40 to 60% increase in output simply by reallocating labor and capital between plants in an industry have been rightly challenged as biased upward by measurement error, it is inconceivable that allocation is as good in India as in the United States. Studies on small samples which we might very plausibly believe to be more accurate than mailed out surveys consistently find serious misallocation, such as in Banerjee, Duflo and Munshi (2002) and Banerjee and Munshi (2004).

Some researchers have directly measured the effect of courts on misallocation, and how it affects the production process. Obviously, simply regressing court congestion and growth would be biased – places which have greater economic growth might file more cases, for example. What Boehm and Oberfield use is the age of a court, which strongly predicts how congested it is. If a new High Court is formed, it naturally starts out with no cases, and only accumulates them over time. Places with worse courts will do more things in house, and will not rely upon other companies to make products. This is a big deal! Being able to fragment your production allows for greater specialization by each of the parts. They estimate that simply making every court system like the least congested systems would, by itself, raise productivity by 4%.1

Misallocation can come from stunted growth. In India, firms grow far more slowly than in the United States. In all countries, plants start out small, and then add workers over time as they learn about the market and their business. A 40 year old plant in the United States will employ seven times as many workers as a newly formed plant. In India, they grow by barely 50%. The gap in average revenue product between the most and least productive plants is five to six times higher than in the United States.

This can be traced back to the courts as well. Slow courts increase the cost to fire anyone. In India, someone employed for a year by a firm which has more than 100 employees can only be dismissed for habitual absence or proven misconduct. To fire workers for economic reasons requires local government permission, and then eventually, permission from the court system.

Bharat Forge Co Ltd v. Uttam Manohar Nakate is a particularly famous case, but quite instructive. A worker, Mr. Nakate, was found asleep while on duty. As this was the fourth time he had been caught in such a state, he was duly fired after all due procedure. The local court disagreed, and required him to be reinstated at half-pay for back wages. The factory appealed the Supreme Court, which ruled that the firm had indeed been justified in firing Mr. Nakate, and ordered the case dismissed. Mr. Nakate had been found asleep on the 26th of August, 1983. The Supreme Court dismissed the case in 2005. Justice delayed is justice denied.

Much as how the first-order effect of a ban on divorces would be to reduce marriages, making it harder to fire workers prevents expansion of productive businesses, or the reduction in size of those which faced an adverse shock. Firms hold back from hiring employees with whom they will be saddled if things don’t turn out well. The harms from this show up primarily not in misallocating particular workers, but in firms being the wrong sizes — it is a sound explanation for the pattern seen in Hsieh and Klenow’s work.

Outside competition is stifled by the court system. Multinationals do not have family members to employ, and would have to rely upon the court system to enforce their decisions. Since multinationals are much more productive than domestic firms, and bring their better management practices with them, preventing them from coming to India makes the management of domestic firms worse too.

India’s court system costs India at least 10% of its GDP every year, which is comparable to some of the low end estimates of the effect of climate change. It is a very big deal. In the next section, we will answer a few basic questions: Why are there so few judges? Why does adjudicating a court case take so long? And what can the Indian government do?

The fundamental problem is that India does not spend enough on judges. India spends .1% of its GDP on the justice system, which is smaller than it looks. Providing the rule of law has increasing returns, insofar as it requires high fixed costs and then a low marginal cost to apply to many people. A richer country would naturally have to spend a smaller proportion of its GDP on the judiciary.

21 judges per million is in fact an improvement over the recent past. There were about 14 per million in 2002, when the government planned to raise it to 50 per million in the next five years. Of course, they said the same thing in 1987, when there were only 10.5 per million, with the same goal too.

Judges are appointed to the High Courts by the President, and to the district courts by the Governor of that province, but this is done in consultation with the high judges. Because they meet infrequently, positions are often unstaffed. In November of last year, there were 5,600 unfilled vacancies, including two in the Supreme Court and 364 in the High Courts. Incentives are not aligned – the relative importance of each judge increases the fewer there are. Since the judges have so many cases to resolve, meetings are rare. The collegium for the High Courts met only 12 times between 2017 and 2020, 3 of which were to discuss the appointment of a single judge. The courts are also an independent power from the Modi government, who has been delaying the appointment of judges for political reasons. The average length of a vacancy is 8 months, and has not improved for years.

The court procedure is excessively dilatory. Being a descendant of the British system leaves them with a more formalistic legal system, which is robustly associated with legal procedures taking a longer time to accomplish. The Indian judiciary is far too generous to lawyers who are absent. They need to require timeliness, or else dismiss the case. An example reported on in the New York Times is of a Mr. Mahendar, who was accused a decade ago of selling adulterated milk. The inspector who filed the case had been reassigned to a different case, and had never shown up at a trial, a matter of little importance to the court. Every few months, Mr. Mahendar goes to court, has his attendance taken, and is reassigned another court date.

The Indian judiciary should be more assertive in simply dismissing cases. Everyone can play out who is more vulnerable to an extended period of litigation, so lawyers for the side which would prefer time wasted plead for extensions and delays. The judges, rather than punish the lawyers or dismiss the case entirely, go along with this.

The notorious prolixity of Indian judges and lawyers is a small part as well. This may seem like a trivial, even silly, thing, but I am not joking. The Supreme Court routinely indulges in producing preposterously long opinions. There is no conceivable way the court is spending its time well producing, as in State vs Jayalalitha, a 570 page opinion (with 552 paragraphs!), with excruciatingly tortured prose to boot! No seriously, look at this. This is from a supplement to the main opinion, because sometimes you just don’t say everything you want to say in the first 570 pages. “A growing impression in contemporary existence seems to acknowledge, the all pervading pestilent presence of corruption almost in every walk of life, as if to rest reconciled to the octopoid stranglehold of this malaise with helpless awe. The common day experiences indeed do introduce one with unfailing regularity, the variegated cancerous concoctions of corruption with fearless impunity gnawing into the frame and fabric of the nation’s essentia. Emboldened by the lucrative yields of such malignant materialism, the perpetrators of this malady have tightened their noose on the societal psyche. Individual and collective pursuits with curative interventions at all levels are thus indispensable to deliver the civil order from the asphyxiating snare of this escalating venality.”

Good god!2

In short, the judiciary lacks urgency. It does not recognize the damage which it has done to India, and is not acting in India’s best interests. I think the district courts should be made into an equivalent of a civil service position, and many more people hired. Courts should have a maximum number of adjournments or delays allowed, and if these are exceeded should rule against the delinquent side.

Ultimately, India needs to make judicial reform a priority. Not judicial reform as part of political power struggle, but as part of a genuine effort to staff the court. Until it chooses to do so, we cannot expect India to ascend to the level of development which its people are capable of.

Everyone asks, "How do I break into PM?" but nobody asks, "What would I actually DO as a PM?"

Here's the truth every aspiring, junior or jaded product manager needs to hear:

Amazing footage of Iranian Ballistic missiles from a flight’s cockpit. Can see the 1st stage separation and then the missile going into outer space to achieve an altitude of 400kms, before re-entering at the speed of 2400m/sec.

Most PMs chasing "technical skills" think they need to learn code.

But what they’re really chasing is credibility, confidence, and career security.

The myth of the "technical PM" keeps you stuck.

I'll teach you in 2 minutes what took me 5 years to see:

🧵 1/16