SpaceX $SPCX is planning to go public on June 12.

It's the biggest IPO in history and will instantly reprice the entire space sector.

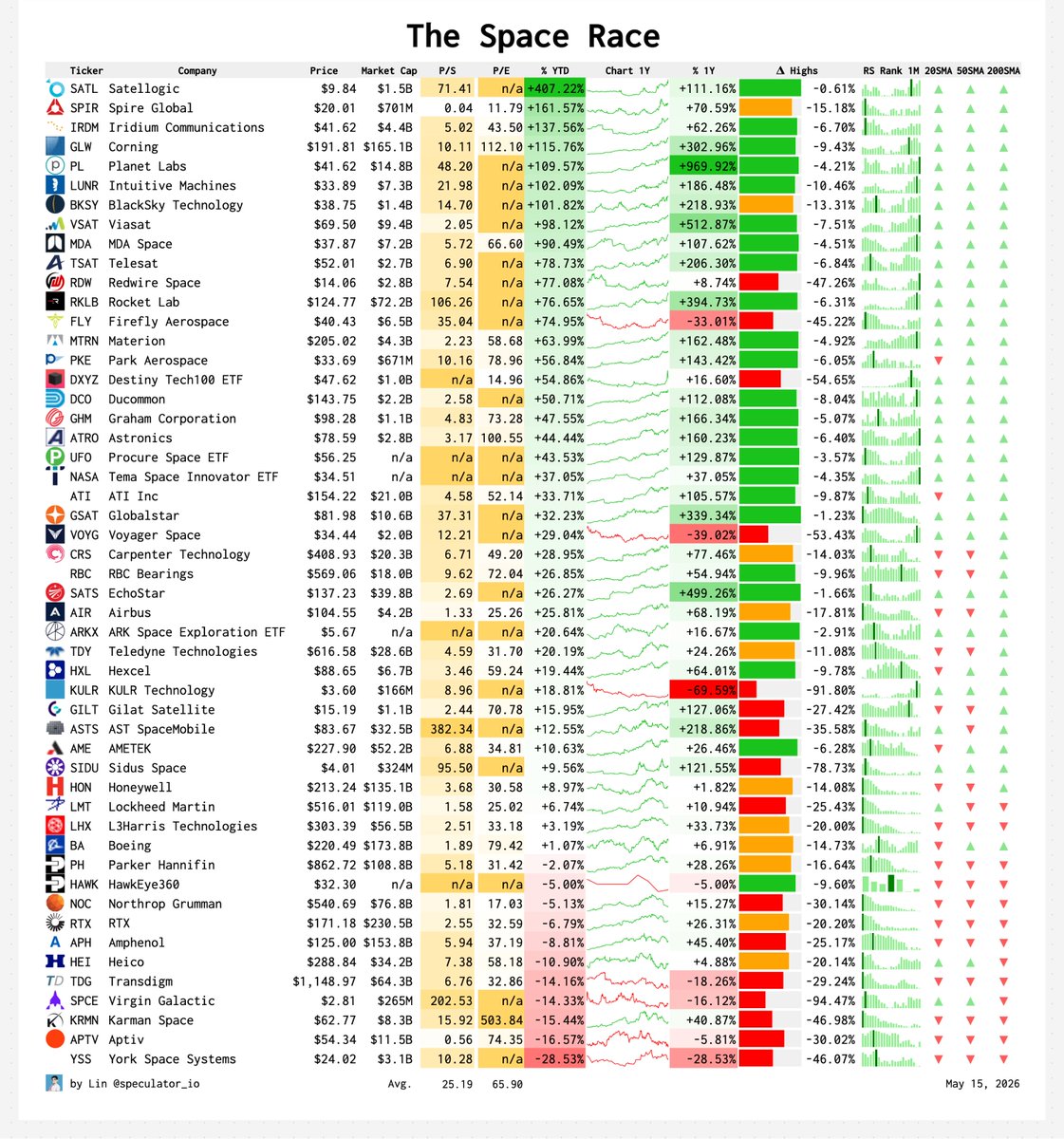

These are the key space sectors to watch:

Launch Service Providers

$RKLB Rocket Lab

$FLY Firefly Aerospace

Space Imaging

$PL Planet Labs

$SATL Satellogic

$GSAT Globalstar

$BKSY BlackSky Technology

$SPIR Spire Global

$HAWK HawkEye 360

Satellite Communications

$ASTS AST SpaceMobile

$GSAT Globalstar

$SIDU Sidus Space

$SATS EchoStar

$IRDM Iridium Communications

$ETL Eutelsat

$TSAT Telesat

$GILT Gilat Satellite Networks

$VSAT Viasat

Space Infrastructure

$RDW Redwire Space

$LUNR Intuitive Machines

$MDA MDA Space

$VOYG Voyager Space

$YSS York Space Systems

Speciality Materials

$CRS Carpenter Technology

$MTRN Materion

$HXL Hexcel

$ATI ATI

$GLW Corning

$PKE Park Aerospace

Aerospace & Defense

$RTX RTX Corporation

$LMT Lockheed Martin

$KTOS Kratos Defense & Security

$VOYG Voyager Space

$LHX L3Harris Technologies

$NOC Northrop Grumman

$BA Boeing

$AIR Airbus

$HO Thales

Space Components

$TDY Teledyne Technologies

$APH Amphenol

$KRMN Karman Space

$RBC RBC Bearings

$PH Parker Hannifin

$AME AMETEK

$VELO Velo3D

$GHM Graham

$HEI Heico

$DCO Ducommun

$ATRO Astronics

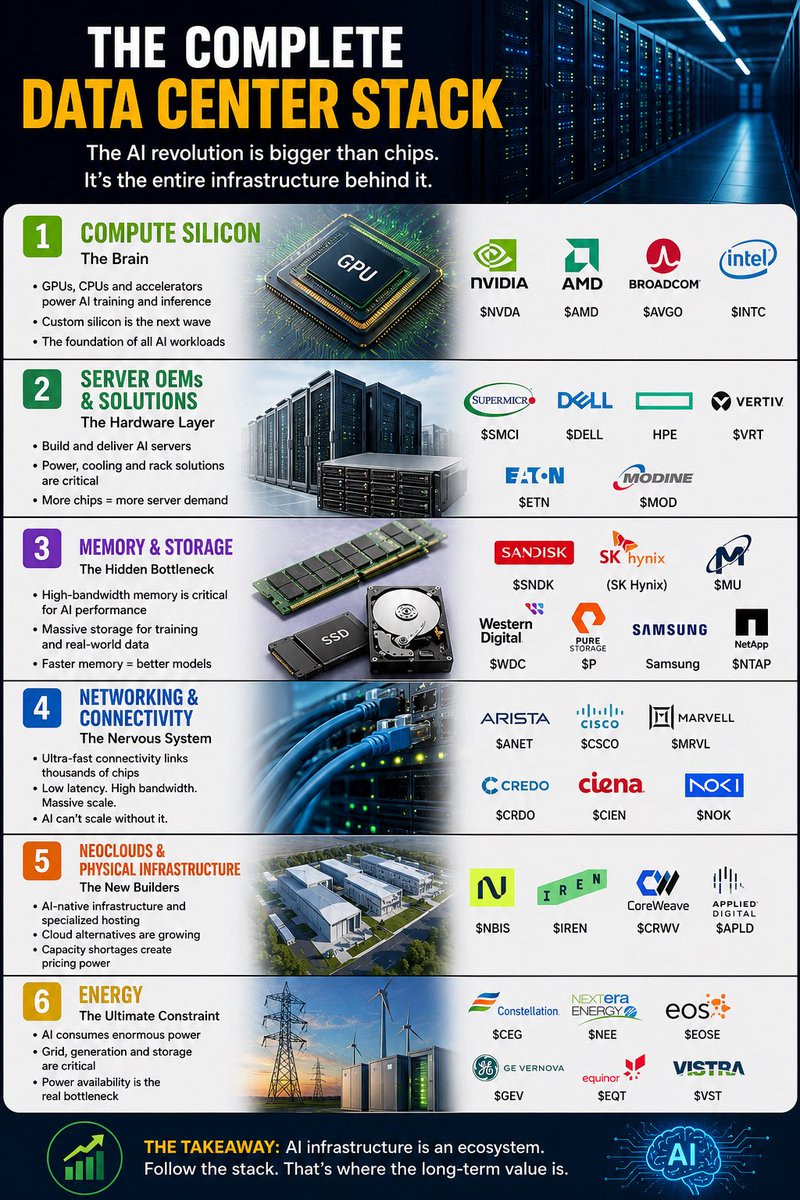

The Complete Data Center Stack: Where the AI Infrastructure Money Flows Most investors still think AI is just about GPUs. That’s incomplete.

AI is an infrastructure buildout, and the real opportunity spans the entire data center stack. Every inference, every training run, and every deployed model depends on multiple layers working together.

Here’s the breakdown:

1. Compute Silicon (The Brain)

Tickers: $NVDA, $AMD, $AVGO, $INTC

This is the foundation. GPUs, CPUs, accelerators, and custom silicon power training and inference.

Why it matters:

- Compute demand keeps rising with larger models

- AI workloads are forcing faster chip innovation

- Custom ASICs are becoming a major trend

2. Server OEMs & Solutions (The Hardware Layer)

Tickers: $SMCI, $DELL, $HPE, $VRT, $ETN, $MOD

Chips need systems. These companies assemble and deliver the physical AI servers and power systems.

Why it matters:

- AI racks are denser and hotter

- Power distribution is now critical

- Cooling is becoming a competitive advantage

3. Memory & Storage (The Hidden Bottleneck)

Tickers: $SNDK, SK Hynix, $MU, $WDC, $P, Samsung, $NTAP

AI models consume massive amounts of memory bandwidth and storage.

Why it matters:

- High-bandwidth memory is becoming strategic infrastructure

- Data storage demand rises with AI deployment

- Faster access = better model performance

4. Networking & Connectivity (The Nervous System)

Tickers: $ANET, $CSCO, $MRVL, $CRDO, $CIEN, $NOK

AI clusters must communicate at ultra-high speed.

Why it matters:

- Faster networking reduces latency

- Data movement is becoming expensive

- Scale depends on interconnect efficiency

Key idea: AI cannot scale without bandwidth.

5. Neoclouds & Physical Infrastructure (The New Builders)

Tickers: $NBIS, $IREN, $CRWV, $APLD $CIFR $DGXX

These companies provide specialized AI infrastructure and hosting.

Why it matters:

- Cloud alternatives are growing

- AI-native infrastructure is becoming valuable

- Capacity shortages create pricing power

6. Energy (The Ultimate Constraint)

Tickers: $CEG, $NEE, $EOSE, $GEV, $EQT, $VST $OKLO $BE $FLNC

AI consumes enormous electricity. Power availability is becoming a limiting factor.

Why it matters:

- Grid demand is surging

- Battery storage is essential

- Reliable baseload power matters

Final Thought

The market often focuses on one winner.

But AI infrastructure is an ecosystem.

If you want to understand where capital flows next, follow the stack:

Compute → Servers → Memory → Networking → Infrastructure → Energy

The biggest winners in the AI cycle may not always be the obvious names.

Sometimes the best opportunities are in the supporting layers that make the whole system possible.