Since one of the circle will fit into the square, and leave same area as shown here, we only need to subtract the area of one circle from the area of the square, to get the area of the shaded region.

196 - (49π)

I believe the CSCS or company registrars could improve their notification process to inform applicants of any type of equity offer when shares are credited to their accounts.

This arbitrary check to verify whether the shares are there or not is not ideal.

If you are going into the equity market, never conclude that a low stock price equates to being cheap.

A N1 stock can be more expensive than a N500 stock

Space X trailing PE ratio is 1000x which essentially means earnings need to compound 30% for around 20 years before it grows into its valuation. How does Elon always get away with this? Lmao.

NGX vs Ecobank: A ₦627 Billion Market Cap Discrepancy Investors Cannot Ignore

So, I was discussing with the TG members during our usual Sunday session, something we have consistently hosted every Sunday since 2021, free of charge. One of the topics we discussed was why continuous dilution should never be ignored when building long-term positions in companies. As we started breaking down the banking sector, we got to @GroupEcobank. We noticed major discrepancies in the reporting of its outstanding shares compared to what @ngxgrp currently displays on its platform, which, ideally, should be the go-to and most reliable source for investors.

So, I decided to do a deeper dive.

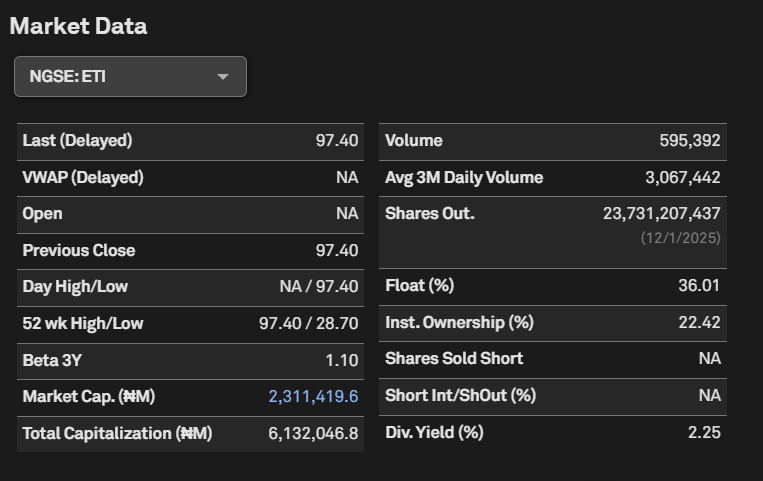

The first screenshot is from the @ngxgrp platform, which currently shows Ecobank’s total outstanding shares at 18,155,073,977. Multiplying that by Friday’s closing price of ₦97.4/share gives a market capitalization of ₦1,768,304,205,359.80.

The second screenshot is from S&P Capital IQ, which reports Ecobank’s outstanding shares at 23,731,207,437 shares. Interestingly, the last update there was dated 1 December 2025. Using the same closing price of ₦97.4/share gives a market capitalization of ₦2,311,419,604,363.80.

The final screenshot is extracted directly from Ecobank’s Q1 2026 financial statement under Note 14, page 29. The company itself reported outstanding shares of 24,592,619,000 shares. Multiplying this by ₦97.4/share gives a market capitalization of ₦2,395,321,090,600. What shocked me even more was that the same outstanding shares figure was also reported in Q1 2025.

Now, today is a weekend, so I do not currently have access to the Bloomberg Terminal to cross-check further, but working with these three data points raises serious questions.

So, who exactly should investors believe here?

Personally, I would naturally rely on the company’s own financial statements because they are the primary source, and I should know their actual outstanding shares.

NGXGROUP Market Cap for ETI = ₦1,768,304,205,359.80

Ecobank Q1 2026 Financial Statement Market Cap = ₦2,395,321,090,600

Difference = ₦627,016,885,240.20

That difference is highly material and honestly quite alarming.

Even if we compare S&P Capital IQ with Ecobank’s reported figures, we still get a discrepancy of about ₦83.9 billion, which remains very material. Meaning even S&P Capital IQ appears to be underreporting Ecobank’s market capitalization.

Now, this becomes a serious issue if @ngxgrp is not accurately reporting something as fundamental as outstanding shares. Market capitalization is one of the most basic valuation metrics investors rely on daily. If discrepancies of this magnitude exist, then it raises broader questions around data integrity and market transparency.

What does this mean for the future of our market if basic company information is either underreported or overstated? This is 2026; these are issues we should have moved past long ago. It honestly breaks my heart because these were part of the same structural issues that contributed to market inefficiencies during the 2007/2008 era.

And Ecobank is not even the only example. Even @ngxgrp previously had issues with the reporting of its own outstanding shares at some point (although I do not know if that has now been rectified).

This is why I always encourage investors to scrutinize everything. It is not just about making money. It is also about ensuring our market institutions uphold accuracy, transparency, and investor confidence.

I drop my pen here.

An acquaintance and I met recently, and we discussed stock investing. He was trying it for the first time, and I was very intentional about making his experience a successful one. One of my purposes is to, in my own way, increase participation in the Nigerian financial markets, particularly in the equities market.

A few months in, my guy was already in the money. Portfolio return was already at 70%, including specific names that had done 2x (e.g., CAP PLC).

We recently did a catch-up, and he was so excited. I was excited too. He said he wished he had invested more money, and I was like "na so e dey be when the sight green, lol".

He then chipped in "omo, na to close my farming business and do stocks o". I knew he was joking with that line, but I still thought I'd make a point about it... Just for informational purposes.

The stock market truly is described as the "greatest wealth-creating machine ever invented".

Also, the stock market will make you rich and it won't also make you rich. The deeper point is about not confusing the source vs the vehicle.

The farming business provided the capital, and the stock market has multiplied it.

When your portfolio is up significantly, it's easy to feel like you've "figured it out" and that the market can now replace your salary. But what people forget is that the portfolio only exists because the job provided the consistent capital to fund it in the first place. The income was the seed, the market was just the soil.

So if you want more returns, you have to double your efforts at your job to make money (via salary increases, bonuses, or other sources of income).

Additionally, in this person's case, his farming business is a form of private equity. The stock market is a public equity - both are still equities, and he might need to even diversify into other asset classes (say fixed-income, except there is a specific investing constraint. Another option is real estate.

The @WHO org is currently having a live session about the Hantavirus updates.

Are we all going to be in lockdown by next weekend?

This research report done via @ValyuOfficial says a lot about Hantavirus origins & what's likely to happen next!

https://t.co/GgNj5kchWM

Revisiting this: https://t.co/5yLjLHsvSd

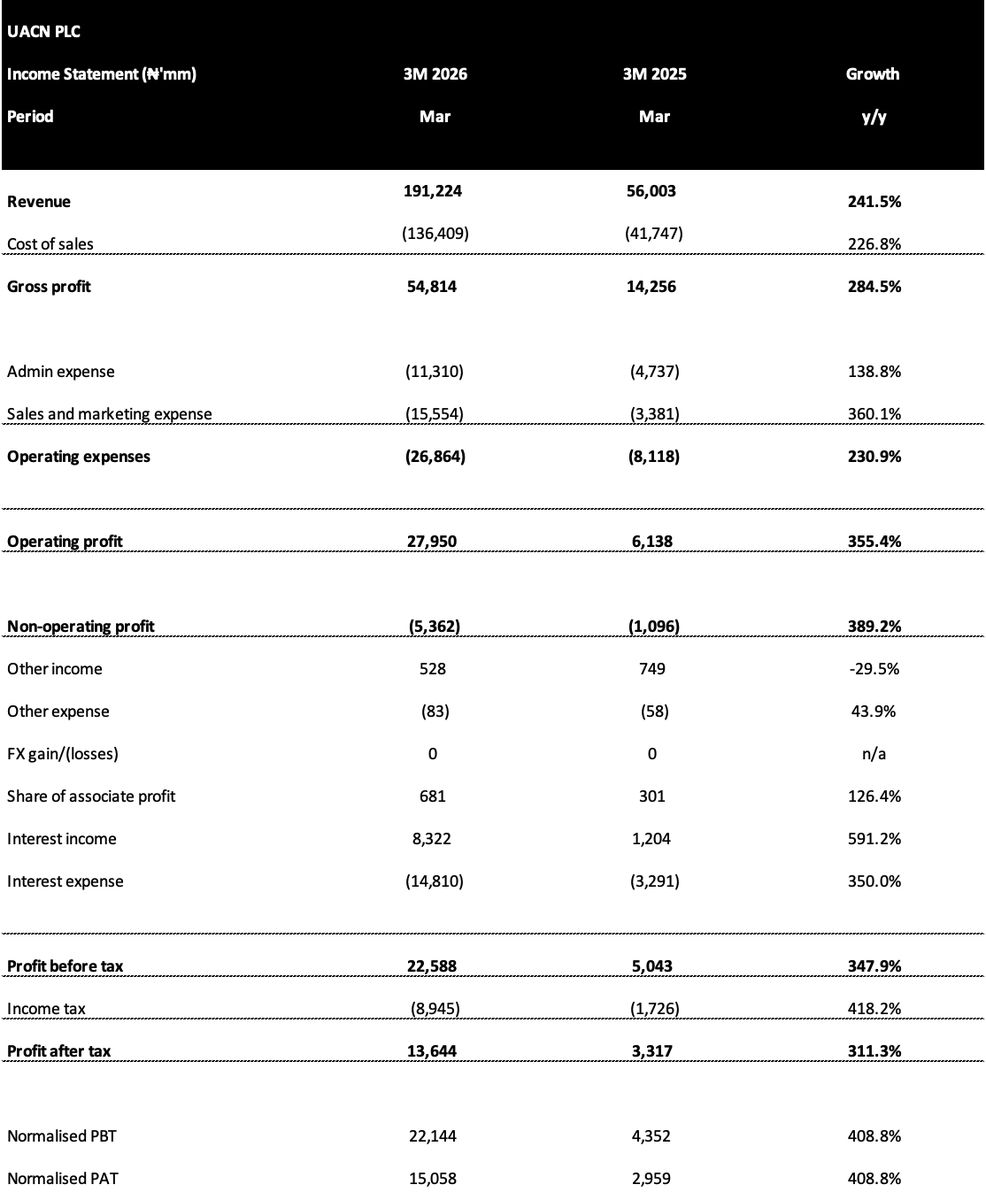

UACN released its Q1 2026 results, and we can now see the numbers of the enlarged entity. The numbers are really looking more than I had anticipated (before I made this move (https://t.co/u7Jm8XgWe4).

Current valuation looks like a 7x P/E and a 5x EV/EBITDA. A crazy steal.

Now, I can have some peace; the Edibles & Feed business is no longer the biggest segment, and I trust Mr Oloyede to work wonders in the Packaged Foods business.

I estimated a 23% return on invested capital, which is still low but much stronger than recent historical trends.

I saw the cash flows too, and I nodded my head to say "okay, okay, we're starting so well".