My good friend, @LuxuryWatchGuy1, is donating a Rolex to help Texas flood relief.

We're going to raffle it off.

To enter, donate a minimum of $50 to the verified GoFundMe Texas Flood Relief Fund linked below.

And then paste a screenshot of your donation in the comments.

You can enter as many times as you want.

A winner will be chosen at random on July 23rd, and can pick whichever watch they want.

I would also appreciate it if you would share this. 100% of the money flows directly to the families impacted by the tragedy.

Thank you.

BOND MATH: A SIMPLE OVERVIEW OF DURATION AND CONVEXITY

As another bank crisis unfolds, good time to learn the most important concepts of bond math: duration and convexity.

DURATION

Duration is a measure of a bond's sensitivity to changes in interest rates: what is the bond price change associated with a 1% change in its yield?

Specifically, duration measures the weighted average time it takes for a bond's cash flows to be received.

The top left table of the image gives a good representation of this concept.

The duration is 7.8 years. If I change the yield from 6% to 5%, the price increases by ~7.8% ($1,077 from $1,000) as you can see on the middle right side of the image.

On the other hand, if interest rates rise, the present value of the bond's future cash flows decreases, leading to a decrease in the bond's price.

Bonds with longer durations have higher interest rate risks since small changes in interest rates can have a significant impact on the bond's price.

Additionally, zero-coupon bonds have higher durations since all cash flows are received at maturity, making them more sensitive to interest rate changes.

If you are careful when looking at the picture, you can notice how the duration of the case on the right side is now 7.89 years (higher than the original 7.80 years).

The duration has changed because the change in rates changed the weighted average life (you can notice how the time * weight columns are different in the two cases).

This change is what is called the bond convexity.

CONVEXITY

Convexity measures the curvature of the relationship between a bond's price and yield. A bond with higher convexity will have a more pronounced response to interest rate changes than one with lower convexity.

Think about convexity as the change in the weighted average life associated with a 1% change in its yield.

Positive convexity means that the relationship is curved upward, indicating that a bond's price will increase more than it would decrease for a given change in yield.

Negative convexity means the opposite, indicating that the bond's price will decrease more than it would increase for a given change in yield.

The graph at the bottom shows a dynamic that is essential to understand for investors: the price change is slow as yields rise, but it can be significantly faster as yields decrease.

This is why the upside / downside for every percentage increase / decrease in yield is often very asymmetric presenting investing opportunities.

For example, if we start from a starting 6% yield, a 2% increase in yield would lead to a 24% loss while a 2% decrease in yield would lead to a 40% gain (1.66x upside / downside ratio).

The upside / downside ratio increases even more as the change in yield increases. As shown, a increase / decrease in yields of 5% leads to a upside / downside ratio of 3.67x, compared to the 1.66x above.

SUMMARY AND REAL LIFE APPLICATIONS

As we learned, duration and convexity both measure a bond's sensitivity to changes in interest rates.

However, duration measures sensitivity to interest rate changes linearly while convexity measures it non-linearly, accounting for the curvature of the bond's price-yield relationship.

This means that while duration can estimate price changes for small interest rate changes, convexity provides a more accurate estimate for larger changes.

Understanding the duration and convexity of a bond helps investors estimate potential losses or gains given interest rate changes and adjust their portfolios accordingly.

Additionally, convexity provides a more accurate estimate of potential gains in rising yield scenarios, which is particularly valuable in distressed investing. In the private credit world, duration and convexity are often used to value bonds in distressed or special situations.

For example, if a private credit lender is considering investing in a distressed company's bonds, they may use duration and convexity to assess the bond's sensitivity to interest rate changes and model the potential impact on the bond's price in different scenarios.

Similarly, if a private credit lender is considering restructuring a company's debt, they may use duration and convexity to assess the potential impact of changes to the debt structure on the bond's price.

----

If this is too easy for you, check out our newsletter in my bio if you are interested in additional / more advanced content.

Future editions are free but posts go behind paywall once published so make sure to subscribe now!

Restructuring Lesson: Debtor-in-Possession

Let's make a simplified example:

A company is overleveraged and it has to file for Bankruptcy as it is not able to fund its operations anymore. The company can't take on any more debt as all its assets are already used as collateral but the company needs additional liquidity to pay the bills.

Why would creditors lend the company money if they can't get even secured protection through collateral? Thankfully, DIP Loans (allowed only after filing for Bankruptcy) allow companies to give new creditors a senior or equal lien on assets that are already encumbered.

Let's go in more detail. If you bookmark this, please leave a like to increase its reach!

Debtor-in-Possession (a.k.a. DIP) loan is post-petition secured debt that is used to fund a company’s operations during a bankruptcy proceeding.

Before going in-depth about this topic, it is important to remember that borrowings made post-petition, including normal trade credit, are characterized as administrative claims and thus have priority over prepetition unsecured liabilities.

Even with such priority, many lenders will be unwilling to extend credit to a debtor on anything other than a secured basis. This creates a problem because it is likely that the debtor has already pledged all of its assets to secured creditors before filing for Bankruptcy.

To deal with this problem, the Bankruptcy Code allows the debtor, with bankruptcy court approval, to grant the DIP facility lender a super-priority interest in previously encumbered assets of the debtor so that the lender can have greater assurance of repayment.

DIP Requirements

Filing for chapter 11 does not entail the company to incur a DIP loan. However, if a company is experiencing enough financial distress to prompt a bankruptcy filing, then its available cash is usually insufficient to fund its operations. The Bankruptcy Code provides certain requirements for obtaining bankruptcy court approval for post-petition financing in either a Chapter 7 liquidation or a Chapter 11 reorganization.

1. The debtor is required to seek unsecured, post-petition debt for the estate in the ordinary course of business (e.g., payment terms from vendors) that will receive priority payment as an administrative expense.

2. If that approach proves insufficient, a debtor may request that the bankruptcy court approve unsecured post-petition debt outside of the ordinary course of business (e.g., new unsecured notes) that will receive priority payment as an administrative expense.

Last Resort

If offering funding sources administrative expense status that ranks pari-passu with the debtor’s other administrative expenses fails to attract capital, then the debtor can request that the bankruptcy court approve the estate’s incurring debt on one of the following terms:

• Unsecured post-petition debt that will receive administrative expense status, but with priority payment over all other administrative expenses

• Secured post-petition debt with a lien on unencumbered property of the estate

• Secured post-petition debt with a junior lien on encumbered property of the estate (problematic if one or more junior liens already existed pre-petition)

As a last resort, if the debtor can demonstrate that all of these tactics have proved inadequate to attract sufficient capital, the debtor may request that the bankruptcy court approve the estate’s incurring secured post-petition debt with a senior or equal lien on encumbered property (DIP Loan).

Considerations

Given this framework, Congress appears to have intended for debtors to incur secured post-petition debt with first liens on the property of their estates only under extreme conditions. However, DIP loan markets are often inefficient, with few parties that are willing to devote the time and effort of underwriting, negotiation, and documentation.

Therefore, DIP lenders typically face no consequences for demanding the best position and protection possible, knowing that the distressed company really has no viable alternatives. As a result, the last resort alternative has become much more common than Congress may have originally intended it to be.

Adequate protection quick summary

In order to not impair the original secured creditor’s position, the granting of the super-priority lien will require the debtor to show that the original creditor is adequately protected.

Adequate protection is a term that refers to the right of the creditor to insist that it be protected against any loss in value of an interest in property it has (such as a security interest) as a result of the bankruptcy.

For example, the lender may be owed $65 but have $150 of accounts receivable as collateral. In such cases, the bankruptcy court may conclude that a proposed $75 DIP facility may be given a super-priority interest to the extent of $75 of the collateral (leaving $75 to cover the $65 owed) and still find the prepetition creditor adequately protected.

Risk-reward profile

DIP loans should be a great investments for lenders to make, with moderate risks but high yield from interest and fees. After all, the lender already knows that the business is in severe financial distress, so the underwriting assumptions can be very conservative.

Moreover, the DIP lender is the 1st party to be repaid at the end of the bankruptcy proceeding, giving it the best position in the capital structure, called a Superpriority claim. In addition, the assets are under the supervision of the bankruptcy court, giving the DIP lender extra protection from the misdeeds of the borrower or other creditors.

Furthermore, the bankruptcy process provides transparency for the company’s operations. Finally, while technical defaults are common because the uncertainty of operating in bankruptcy makes it difficult to set financial covenants accurately, it is extremely infrequent for debtors to experience a payment default on DIP loans.

---

Comment what other topics you want to read about.

Check out our newsletter in bio if you are interested in additional / more advanced content.

---

Source: Distressed Debt Analysis

I retweet this not as a Republican or Democrat but as a very concerned American at how twisted our educational system has become.

Bravo for having the leadership to take this issue head-on. 👏👏👏

I made the decision to dive head first into ecom right around this time last year

Launched Presale in April and shipped first orders out in July

Here are some mistakes to avoid from a beginner that just made them 👇

- Spending money stupidly

Once you start a biz and have money coming in/starting capital there are so many things you “can” spend money on: website templates, courses, apparel, software, etc…

The list goes on

If I were to give my 1 year ago self advice I would tell me to be much more frugal with my capital

- Tracking Finances

Another aspect you won’t find in most starting guides is how to and how important it is to track spending and the flow of your money properly

My advice: use one credit card and one bank account (if you start with personal accounts like I did eventually you’ll shift to one business account and card) and just start with quickbooks

- Almost no activity takes priority over Marketing

You can get lost in an endless cycle of tasks - design, logistics, watching videos

And all of them most likely need to get done but *almost* none of them move the needle as much as marketing your product

Cold reach out to influencers

Organic content

Creating and running ads

All of these take priority ^

- Overseas manufacturing > US manufacturing

I spun my wheels for 3 months trying to get my product made in the US only to make more progress within 3 days once I went overseas

And the crazy part? My biggest concern was quality and putting “made in the US” on the label.

And yet?

The quality of overseas product was higher

Customer service was 10x

- Get your hands dirty with every aspect to the point of “understanding” and then delegate

This was a tough one that I’m still learning

At what point do you decide you understand how something works and pay an expert?

Website design, copywriting, ad creation, content creation

All of these things are super important and can be done on your own but at a certain point it makes sense to pay someone to have them done right

If you want to see more content like this I ask you to please comment or share this post

Still surprises me knowing how few people actually want to become wealthy.

You only live one life: this one life isn't a practice run. Without wealth how do you own your dream home. Your dream car. Raise your kids the best way possible. Go travel the world. Be able to tend to yourself and love ones when unwell. Have control of your limited time.

At least around me, I do not see anyone even close to being as determined as me - maybe they are but I hardly see results.

I truly cannot relate when people bitch about the most inconsequential things that wouldn't move the needle in *anything*.

This is why finding the jungle was a literal blessing. In a world devoid of driven people, I am growing with like minded people who are talented, working towards success and/or already successful. Thanks @BowTiedBull

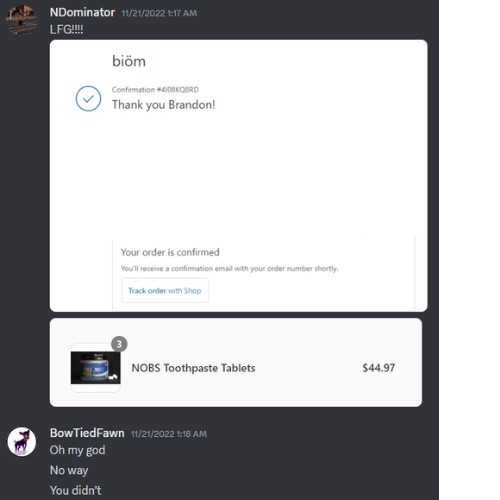

On 1:17AM 11/21/2022 an order was placed by a secret shopper that started an oral health revolution.

Right as the poor deer @BowTiedFawn was drifting off to sleep, ready to dream about launch day, the first of many magical dings of a Shopify order came through.

Yes I did.

Here's what you need to know about @BetterBiom straight from NOBS Customer #1's mouth.

• I brushed my teeth twice a day.

• I used a water pick.

• I flossed.

Surely that meant my dental and oral health was fine right?

I couldn't have been more WRONG.

Before NOBS, I thought toothpaste was toothpaste. If it's on the brush and minty, it's fine.

Until I started getting canker sores.

And they weren't going away.

Canker sores and mouth ulcers are NO JOKE.

You don't want to eat, everything hurts, and it takes forever to heal.

It turns out one of the ingredients in my CankerGate toothpaste was turning my mouth into a warzone.

To make matters worse: my mouth hurt AND my gums were stinging at random.

Thanks SLS.

Sensitive teeth, canker sores, and stinging gums for doing what I thought was right by 9/10 dentists.

Until I met the ONE dentist: @BowTiedGatorDDS and his dream concoction.

In an instant my canker sores started to heal.

After 2-4 weeks my teeth sensitivity was gone.

After a month my gums were happy and healthy.

NOBS took away the physical problems I was having.

Tthe bigger impact was healing years of bad emotional dental experiences (just like the nano-hydroxyapatite helps heal your enamel).

NOBS changed my expectations of what it meant to go to the dentist.

• No more white knuckle bug-eyed pain fest with plaque and tartar flying everywhere.

• No more cramping jaw from stress clenching.

• No more bleeding irritated gums.

For the first time in my life I looked forward to go to the dentist.

I got to walk out of the office like a champion: because my teeth looked good, no cavities, see ya in six months.

If you want to change the way your dentist sees your mouth.

A product that will change your life.

And rewrite your beliefs on dental care.

The Fawn and Gator will see you now.

https://t.co/OKuiYhhXKQ

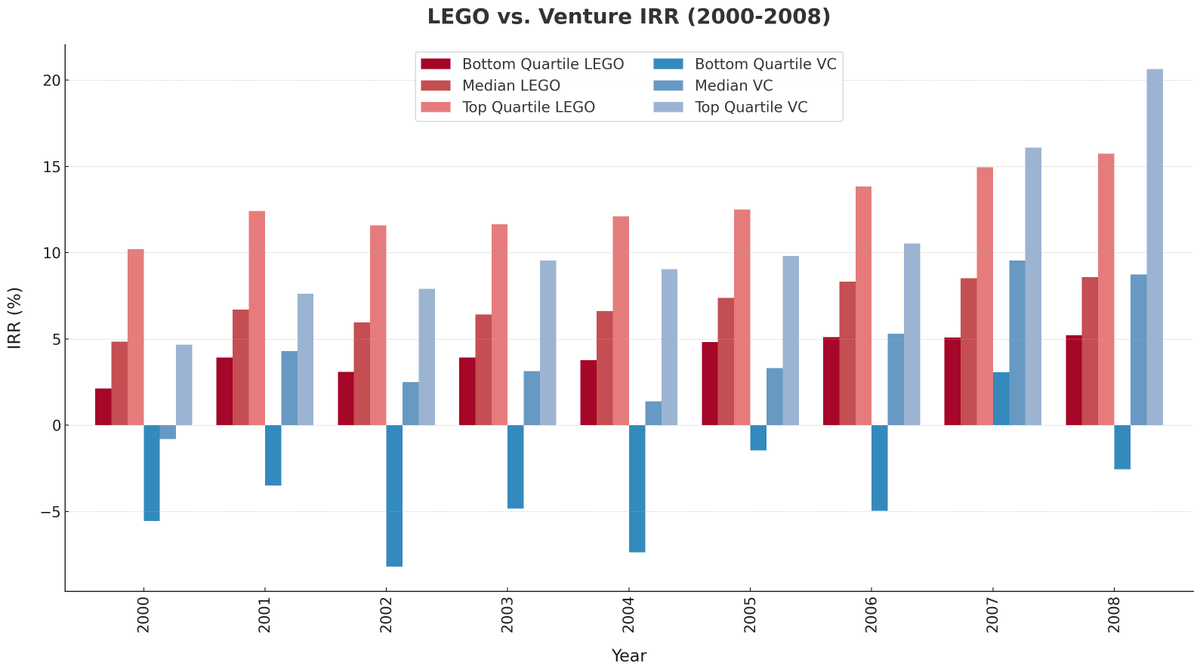

You can outperform most venture funds by buying LEGO.

I analyzed the last 20 years of secondhand LEGO pricing data, and found randomly purchasing sets will match most VC's returns

if you're somewhat intentional about what you buy-- you massively outperform even the best firms

$1M is not going to buy much in 2053 it certainly won't be enough for a good retirement.

When you plug in the 401K (roth or regular doesn't matter) be sure to discount what that will buy 30 years from today.

Don't tell us $1M buys the same today vs. 1993.

GM, Happy Holidays everyone!

Here’s an early gift to y’all for the Christmas Lolz: Project Homeless

Big thanks to @BowTiedPingu for spinning up the deck in a day! 🐤🤝🐧

@BowTiedBull any chance you guys use this at Consensus 2023? LOL

1/x