One of my very first conversations with a prospect at @TripleAHQ was with the CEO of a publicly listed company who wanted to accept crypto payments and hold them on the balance sheet. Elon Musk's announcement that he held bitcoin had left its mark, and for certain executives, exposure to crypto had become a strategic signal. But the conversation quickly took a turn.

Faced with the CEO's enthusiasm, the CFO raised a more grounded concern: what does it actually mean, for a listed company, to carry crypto-asset lines on its balance sheet? How do you explain them to auditors, to regulators, to the risk committee? What he mainly saw was complexity for an uncertain upside.

From that meeting, my conviction took shape.

Most large companies want the efficiency of crypto rails without importing the risk and regulatory complexity onto their balance sheet. That's why, rather than chasing crypto-natives, we turned to e-commerce players and large enterprises that want to offer crypto payments without ever having to touch crypto themselves.

Bank transfers cost 3-7% to cross a border.

The stablecoin sandwich does it for under 1%.

How it works: local currency converts to USDC, moves across a blockchain in minutes, and converts back to the recipient's local currency at the destination.

The sender pays in their currency. The recipient gets paid in theirs. Neither side holds nor manages stablecoins.

The results: settlement in minutes instead of 2-5 days, full on-chain transaction visibility, and no capital locked in prefunded accounts.

There's now a "stablecoin toast" variant! Recipients keep stablecoins in their digital wallets rather than converting them to local currency. Gaining traction for contractor and creator payouts where holding USD beats the local alternative.

Full breakdown at the link: https://t.co/n0g3XWTSRQ

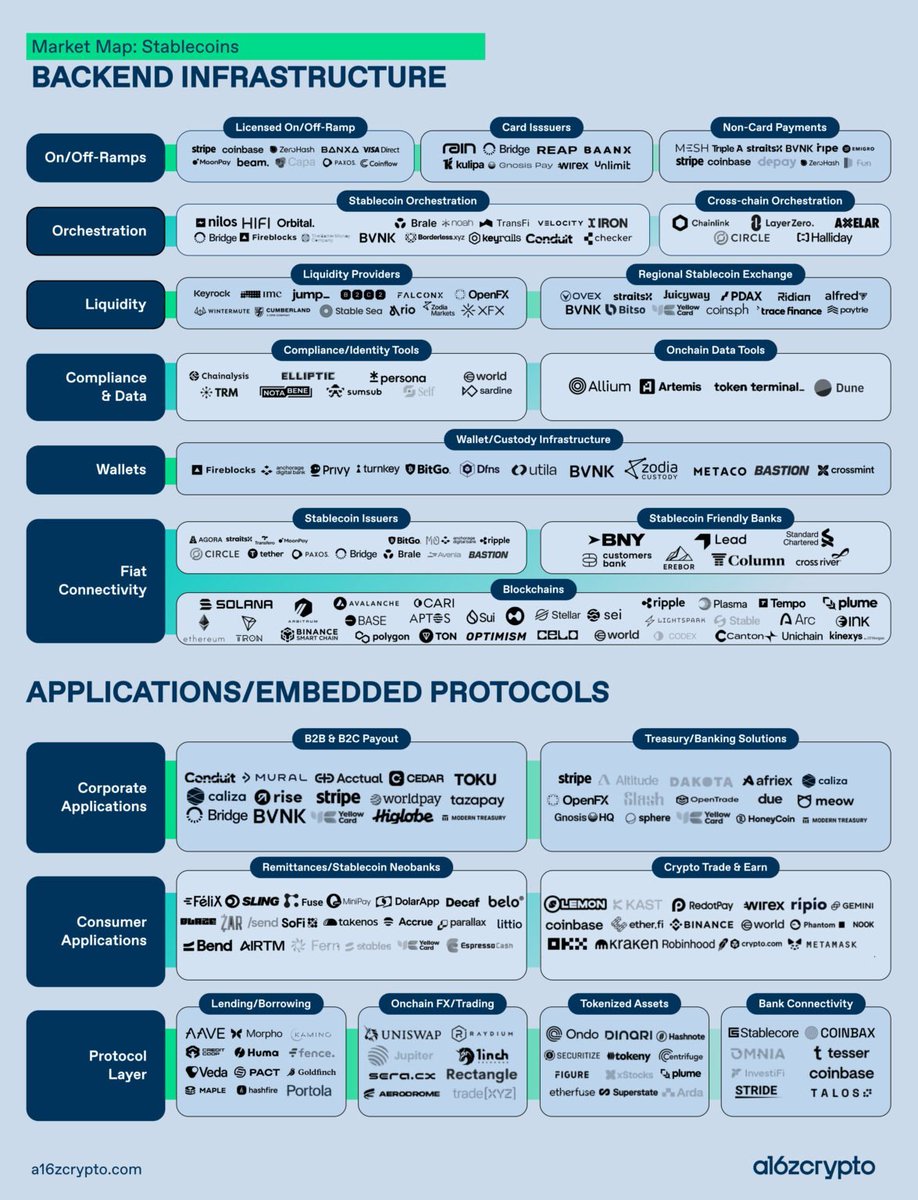

@a16zcrypto just mapped the stablecoin infrastructure stack.

Triple-A is on it. One of the names building the new rails for global finance.

700M+ people already hold digital currencies. The infrastructure to serve them is being built right now.

Proud to be part of that map, helping businesses pay and get paid in stablecoins, without ever holding digital assets.

🧵500 million people already hold stablecoins, and cross-border commerce will never be the same.

.@ericbarbier, CEO of @TripleAHQ, breaks down what's driving stablecoin adoption in C2B payments and where it's headed 👉 https://t.co/Ptx1mYpf6q

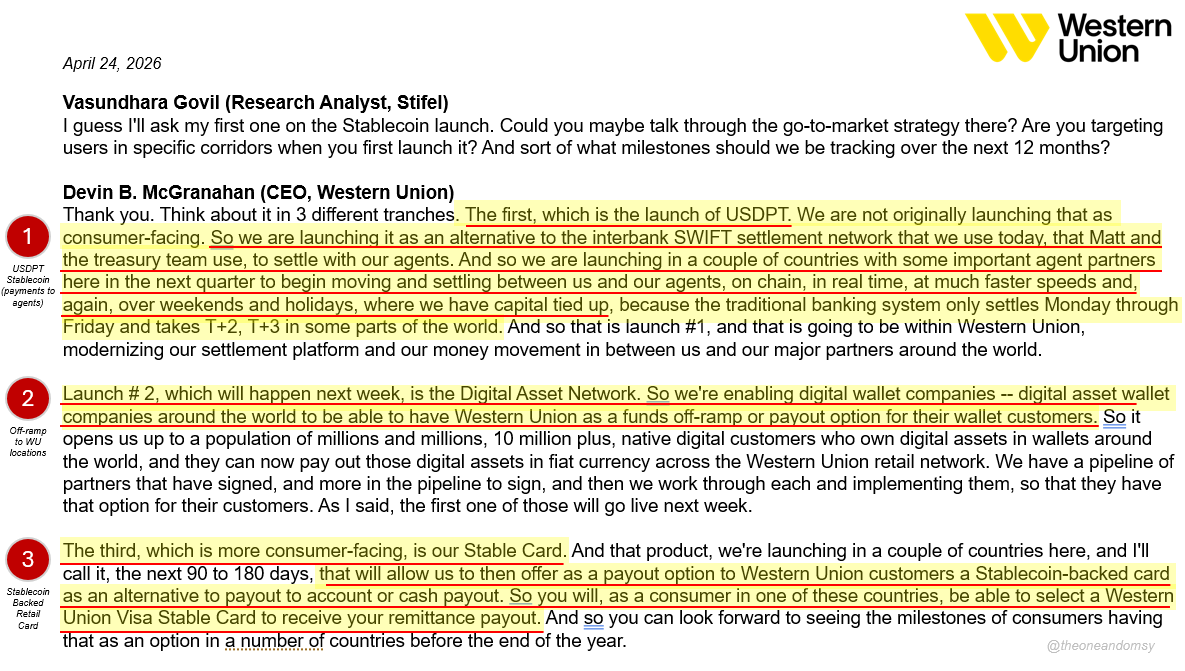

Western Union $WU (~5.5x '26E) dropping the latest on their stablecoin plans yday after earnings:

> Offramp network launching next week: will let users offramp stables -> fiat via WU locations

> Stablecoin (USDPT on @solana ) launching this q, will initially be used by their treasury team to pay their agent locations (~$500m stuck in pre-funding daily)

> Stablecoin card (h/t @raincards) for consumers to spend remittances w/out off-ramping to local cash

Markets continue pricing WU as if it's going to die. And fwiw it likely will. BUT the stablecoin business represents their best shot at salvation, letting them leverage their licenses, brand, physical locations, and flows across segments to audible the business into a modern digital pmts co

Think if we see any uptake here, it reprices or you start seeing serious acquisition discussions (i.e. @circle makes a bid, rolls it in w/ Arc and routes all the flows from merchants and consumers across their new pmts chain)

(Disclaimer: own long-dated calls in case they pull-it off, views are my own and not those of Dragonfly)

Sing Jie Lim, our Head of Business Development for SEA, was named to the Money 20/20 RiseUp Asia 2026 cohort at Money 20/20 Bangkok this past week.

One of 17 selected from across the industry. A program that has put 450+ women through leadership development since 2018, with 78% going on to a promotion or more senior role after completing it.

People talk about Triple-A's licensing footprint and infrastructure. We're proud of both. But none of it moves without the people behind it.

Congratulations, Sing Jie.

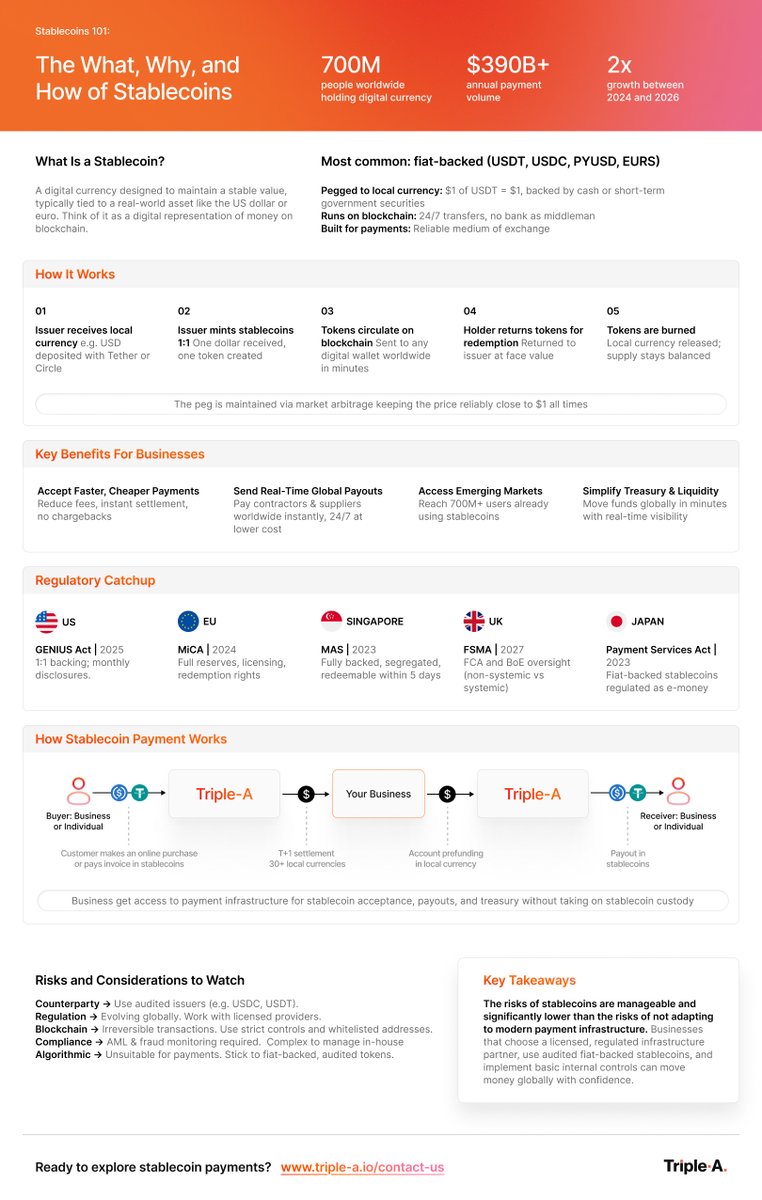

Stablecoin payment volumes have reached over $390B in 2025. At Triple-A, 85% of our payment acceptance volumes are driven by stablecoins.

If you’re a business owner considering stablecoin payments and want to know more about them, read our Stablecoin 101 guide here: https://t.co/pVYepcMgsb

#Stablecoins #Payments #Fintech #CrossBorderPayments

Triple-A is attending Money 2020 Bangkok (21-23 April), the leading global event for the Fintech industry 🇹🇭

@ericbarbier (CEO), Kailash Madan (CCO), Sing Jie Lim (Head of Business Development) and other members of the team will attend to engage with the Fintech community and exchange views on how stablecoins can improve efficiency and speed within the financial ecosystem.

If you’re attending Money 2020 Bangkok, let’s connect!

#Money2020 #Fintech #Payments #Stablecoins

⚖️ The shift is in: Singapore fintech is moving from payments to institutional infrastructure.

These 10 voices aren't chasing visibility—they are setting the direction for how finance will be built and governed across Asia.

📖 Read the full list: https://t.co/vfmtoRaPrT

🚨 Ep. 3 of Stablecoin Stories: Serial Founder Eric Barbier - Why Stablecoins Are the Best Cross Border Rail

With hosts:

💳 @sytaylor, GTM, @tempo

🔥 @rangoldi, VP Payments, @FireblocksHQ

With guest:

🌐 @ericbarbier, CEO, Triple-A

In this episode, Sy, Ran and Eric discuss:

💥 The inefficiencies in traditional remittance that inspired Triple-A

💸 How stablecoins reduce working capital needs in payments

🌍 Real world example of using stablecoins for cross border B2B

📊 Why Fortune 500 companies avoid holding stablecoins on their balance sheet

🪙 Stablecoins as a lifeline for consumers in emerging markets with dollar restrictions

🎮 Adoption of stablecoins in the global gaming sector

🏦 The regulatory landscape and challenges with banks for stablecoin firms

***

Timestamps:

00:00 Introduction

2:21 The inefficiencies in traditional remittance that inspired Triple-A

7:44 How stablecoins reduce working capital needs in payments

10:55 Real world example of using stablecoins for cross border B2B

13:06 Why Fortune 500 companies avoid holding stablecoins on their balance sheet

18:33 Stablecoins as a lifeline for consumers in emerging markets with dollar restrictions

24:24 Adoption of stablecoins in the global gaming sector

29:08 The regulatory landscape and challenges with banks for stablecoin firms

***

👉𝘚𝘦𝘢𝘳𝘤𝘩 '𝘛𝘰𝘬𝘦𝘯𝘪𝘻𝘦𝘥 𝘗𝘰𝘥𝘤𝘢𝘴𝘵' 𝘖𝘯 𝘠𝘰𝘶𝘛𝘶𝘣𝘦. 𝘈𝘱𝘱𝘭𝘦, 𝘚𝘱𝘰𝘵𝘪𝘧𝘺 𝘰𝘳 𝘢𝘯𝘺 𝘗𝘰𝘥𝘤𝘢𝘴𝘵 𝘗𝘭𝘢𝘺𝘦𝘳! 👈

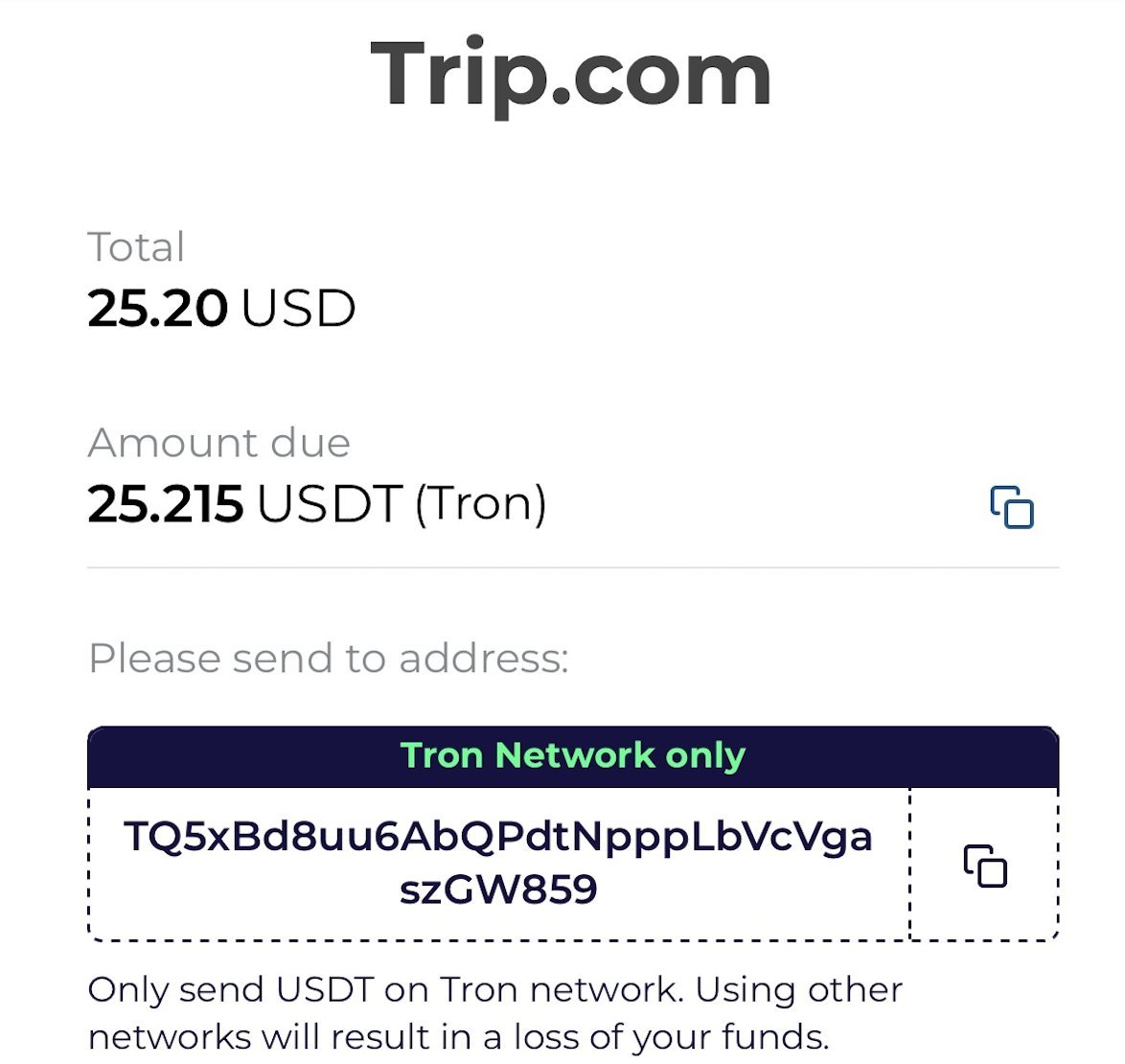

Trip. com rolls out stablecoin payments for travel bookings

@Trip, the overseas brand of Ctrip, has launched stablecoin payments for hotel and flight bookings, supporting $USDT and $USDC.

The feature is powered by Singapore-licensed crypto payment provider Triple-A and supports multiple blockchains, including #Ethereum, #TRON, #Polygon, #Solana, #ArbitrumOne, and #TON.

For hotel bookings paid in $USDT, users only need to provide a name and email, while flight bookings still require passport details to meet aviation compliance requirements.

#Stablecoins #CryptoPayments #TravelTech #Web3

I think we should replace the stablecoin sandwich with the stablecoin toast.

For many of our clients, the real pattern isn’t fiat/stablecoin/fiat. It’s stablecoin/fiat or fiat/stablecoin.

Take one of our clients in Asia who exports to Africa.

His customer in Nigeria accepts payments in stablecoins and keeps them. The local currency never enters the picture. No conversion, no top slice of bread.

But our client wants to be paid in its local currency. He’s a traditional business in Asia and doesn’t want to hold stablecoins. So we convert them for him.

That’s the classic toast scenario: one side in stablecoin, the other in fiat.

In a country with an unstable currency, holding stablecoins is safer, more liquid, and even offers yield. And since the local ecosystem widely accepts stablecoin payments—freelancers, merchants, suppliers—it has become the natural choice (and will increasingly be so).

The stablecoin sandwich exists, yes. But in reality, what we see most often is the stablecoin toast.

"People don’t want stablecoins. They want US dollars."

Stablecoins are permissionless

They thrive where you can’t ask for permission:

capital controls, volatility, political distrust.

That’s why USD stablecoins were willed into existence without clear regulation,

while non-USD ones are still waiting for it.

So what’s the next currency demanded by the people?

See the full episode in the comments for more gems from @ericbarbier, Founder & CEO of Triple-A

A few years ago, onstage discussions about stablecoins would spark heated debates.

Today, everyone agrees on their importance.

The ecosystem has come a long way, a clear sign that stablecoins are here to stay.

Thanks @money2020 for having me!

Par idéologie, EDF (propriété de l’Etat) a refusé de valoriser ses surplus électriques par le minage. Résultat : sa filiale Exaion, déficitaire, est cédée à un mineur américain — avec, comble de l’absurde, interdiction pour EDF de faire du calcul intensif (HPC) pendant deux ans !

Quand les États-Unis transforment leur énergie en puissance numérique, la France brade son atout majeur : une électricité nucléaire décarbonée, stable, abondante et augmente sa dépendance au Cloud Act.

Ce n’est pas une affaire technique, c’est une question d'indépendance.

Il est temps d'assumer une vraie doctrine :

- Définir ce qui doit rester français (énergie, data, IA) ;

- Libérer l’investissement privé, et non pas subventionner les pertes ;

- Permettre à EDF de développer des datacenters flexibles et d'exploiter ses excédents ;

- Développer un minage industriel encadré, vertueux, créateur de valeur.

Refuser d’entreprendre, c’est renoncer à être libre dans un monde de confrontation géoéconomique permanente.

@obchakevich_ I don’t think businesses in developed countries will be holding to stablecoin. They will prefer to hold their balance in their bank accounts. Use stablecoin yes; hold probably not.

Nine European banks plan to launch a euro stablecoin.

I understand the sovereignty argument, and it’s a good thing that banks are starting to take the topic as a consortium.

I genuinely believe they could be the big winners of this transition. They control deposits, payments, credit, and above all, trust.

But who’s going to use a euro stablecoin when SEPA Instant already does the job? And who’s even using the euro for international payments?

It’s the perfect example of a project riding a trend rather than solving a real need.