For those following the Russia-Ukraine War closely, this is a must listen episode. Well done my friend @DanielLDavis1! It's eye-opening in many respects -- not least because it's a conversation among two combat veterans who thoroughly understand modern warfare.

As a (mostly) China specialist, I'll also note that at about 23 min in, there is a fascinating dialouge concerning how China is innovating in military tech and how Russia is eager to take advantage of those innovations. I would urge all of you interested in military affairs to listen regularly to this fine series of interviews by my @defpriorities colleague LTC Daniel Davis (USA-ret), as I do.

If the US wants CNY to rise v. USD, the US need only let gold rise sharply against USD - for example, see what gold and USDCNY did in 2025 and early 2026.

Allowing gold to rise a lot against USD will also keep 10y UST yields & oil prices contained (again, see 2025.)

Philip Su, early OpenAI engineer who shipped the ChatGPT desktop apps:

"Winter is coming. That is my warning."

His math is the part nobody says out loud. You do not need AI to replace 98% of jobs for collapse. In America, 4% unemployment is already a world of hurt. 6% is depression territory.

So AI taking even 5% of white-collar work is enough to break the system.

He is not predicting your job vanishes. He is predicting the small slice that does is enough to drown the rest of you.

His advice is brutal: get into the top 25% of developers, or start gathering nuts like a squirrel

A PHYSICS PROFESSOR GAVE THE SAME LECTURE 1,742 TIMES TO WARN ABOUT ONE IDEA QUIETLY BREAKING THE HUMAN RACE. IT IS THE WORD EVERY AI LAB THROWS AROUND TODAY AND ALMOST NONE OF THEM ACTUALLY UNDERSTAND IT.

72 minutes from Albert Bartlett, a University of Colorado physicist, on the one piece of math he called humanity's greatest blind spot.

-> The idea that lands: a small steady percentage is never small. 7% a year sounds calm, but it doubles in a decade, doubles again in the next, and quietly runs away from you.

He shows it with bacteria in a bottle, with money, with whole cities -- the same curve that looks flat for ages and then explodes almost overnight.

Everyone calls that curve "Exponential". He proves most people hear it as "Fast" when it actually means something far more violent.

Right now every lab and every headline calls AI exponential. This is the talk that shows you what the word truly does -- so you see both the hype and the real danger the way the math demands.

You thought it was a boring math word. It was the whole story the entire time.

Save this one. You'll never hear "Exponential" the same way ↓

I figured this would eventually happen, but not as quickly as it seems to be happening and, for this, Paul Krugman should get credit. For years mainstream economists were unable to understand how trade and globalization work because they were locked into trade models that implicitly assumed that trade was balanced (except, occasionally, over short time periods) and that capital flowed towards its most productive use. That is why their understanding of trade had no relevance to the actual world of trade that emerged in the 1970s and 1980s.

But this couldn't last. As the problem of unbalanced trade became more obvious , and as policymakers were increasingly forced to ignore the advice of their economists and respond to real problems, mainstream economists would eventually begin to recognize how, in an unevenly globalized world, countries that aggressively intervene in their domestic economies and externalize the costs through trade surpluses are also effectively intervening in the domestic economies of countries that supposedly remain committed to "free trade".

Most economists still don't understand trade. But with Krugman now acknowledging that tariffs and other forms of trade intervention can be expansionary under some conditions and contractionary under others (as Ragnar Nurkse explained as long ago as in his 1944 book), I suspect that younger economists will develop a completely different understanding of trade, and one that is perhaps a little more realistic.

A chi tuona che paghiamo le #rinnovabili anche quando non producono segnalo che per il prossimo trimestre @TernaSpA prevede una spesa NEGATIVA per la modulazione straordinaria (si veda TIDE).

Il P_other direi che pare il vaso di Pandora... famo finta di niente va 😅

⚡️⚡️⚡️⚡️⚡️

Quando oggi alle 11:30 abbiamo raggiunto la domanda elettrica record di 57,5 GW, le fonti intermittenti, insensibili come noto all'umano bisogno di condizionamento producevano: 0,7 GW eolici (appena il 5% della potenza installata) e 24 GW fotovoltaici (il 49% della potenza installata). E per fortuna che importavamo 7,7 GW, di cui 6 dalla Francia (direttamente e via Svizzera): 6 GW nucleari, cioè 5 reattori da 1200 MW tutti per noi, alle 11:30 (non ditelo a quelli che "l'energia nucleare ce la svendono di notte, chè non sanno che farsene").

Però, per gli ultimi no nuke ruspanti nostrani, il problema è la riduzione del 5% della potenza nucleare francese (per far fronte ai fiumi caldi)... e non l'indisponibilità del 95% dell'eolico italiano.

The real reason oil is below $100/bbl. It isn’t fundamentals. It’s capital aversion. Policy uncertainty has made oil too volatile to hold. Investor VaR has collapsed by c.$5B. Open interest is at the lowest level in years. Global oil stocks are still drawing 5-6mb/d; however, investors say they don't care.

Start with investor VaR - the best measure of how much capital is willing to engage with oil. It has collapsed to $1.4B (see chart). Not forced out by rising rates, sanctions or external margin calls. Investors are simply choosing not to hold. The policy noise - deal on/off, attack, not attack - has made the carry uncompensable.

VaR compression has one direct consequence: it drains open interest. Contracts are closed. Market depth disappears. 2026 YTD open interest decline is the worst on record. Unlike 2022, there’s no rates shock or sanctions forcing the exit. This is capital aversion.

Managed Money VaR and YTD OI Change

US President Trump says since last month more than 100 million barrels of oil have left the Persian Gulf in a “secret” US mission to get tankers out via the Strait of Hormuz.

If true, and counting 40 days (all May and first 9 days of June) that would equate to ~2.5m b/d.

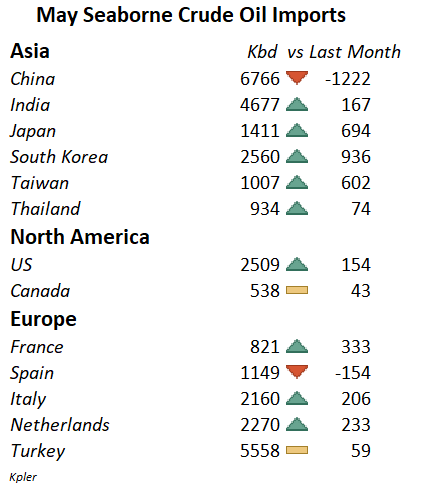

I think we are generally sleeping on the fact that China ramped imports up by 1-2 million bpd for over a year, and then slashed them by 6 million bpd in a few months, all through direct market interventions.

If the closure of the strait of Hormuz is the biggest deliberate market manipulation in history, what has happened with Chinese imports ranks as No. 2.

🧵1/ Let's engage in a thought experiment. Let's assume for a second the reason China's energy stockpiles are not being drawn down isn't because the country has gigantic secret stockpiles no-one in the market has as yet detected.

Let's assume instead it's because the warehouse receipts underpinning these reserves exist as a type of base money that funds an extremely over-extended and leveraged shadow financing system. A parallel-dollar clearing system if you will. And that liquidating any of this collateral would trigger a daisy chain credit event, equivalent to a run on the yuan.

Far-fetched you say? Well let's test the hypothesis by running through what you would expect to see more broadly if it is indeed true that the reason the stockpiles are not being liquidated is because the system can't financially afford to extinguish that collateral without sparking a financial crisis.

https://t.co/BzNLQzXTKh

@Bogachan_1971 I fear that anyone who believes a deal is possible, with the stock market at an all-time high, might also believe in Martians, flying donkeys, and teleportation.

@kyleichan@electricfelix For decades, Germany invested little, preferring the returns of an undervalued currency, which it obtained by joining the euro, destroying the industries of Italy and France. Now Godzilla has arrived, and the Germans don't know what to do.

lol so china's basically monetizing trade imbalances through gold appreciation instead of printing into fx reserves -- creditors get paid in appreciating collateral that doesn't show up as a liability on pboc's balance sheet. cleanest deficit financing since oil-for-gold in the 70s

Multiple oil tankers are attempting crossing the Strait of Hormuz (via the Iranian shipping lane), including 2 Chinese VLCC and 1 South Korean. All are carrying non-Iranian oil.