We’re excited to share that we just signed an agreement for @salesforce to acquire @fin_ai for ~$3.6B. The transaction is expected to close in the fourth quarter of Salesforce’s fiscal year 2027.

Fin started as Intercom 15 years ago. We changed our name to cap our transformation just weeks ago. We were a darling of the SaaS era and invented so many of the patterns you see in software today. Nearly four years ago, in need of a reboot, we jumped on weeks-old modern LLMs to create and define the category we know as Customer Agents today.

Salesforce invented modern software and SaaS. And @benioff is like the final boss of tech founder CEOs. In seat for 27 years, he’s one of the last of his era. Still pushing, pivoting, placing big bets. It’s a privilege for @destraynor and I to get to partner with him and join forces with Salesforce upon close at this most fascinating time. And will be very fun to get their help bringing Fin to magnitudes more consumers.

To our customers: Over the past few years we’ve been shipping intensely. Including recently our groundbreaking model, Apex, and our paradigm-defining internal agent, Operator. With the resources of Salesforce this will only accelerate. And yet little will practically change. I’ll still be CEO, Des will still be running R&D, we’ll both still be committed to continuing to lead this category. Thank you very sincerely and deeply for your belief in us.

To all of our friends, our families, and our employees, past and present: While this is not the end, it is a major, pivotal, special, and emotional moment for us. From the bottom of our hearts, thank you. For everything.

To my cofounders, my exec team: Look what we built. Four young lads with a dream and nothing to lose. And a home grown exec team who pulled off the greatest and arguably only late stage software company pivot to AI, and invented one of the most important categories in AI. Thank you for sticking through all of this with me.

And now, time to get back to work. See you at our next product launch in a couple weeks. (:

What are buyers in the market are actually saying about $SPCX's Starlink (and Musk's former xAI)?

- Starlink: strong fit for remote/rural primary circuits and backup/failover, unlocking new IoT deployments - very positive sentiment

- Where Starlink falls short: fixed offices, where buyers cite cost and sturdiness

- xAI: was a distant third in enterprise AI. Buyers cite ecosystem immaturity, data privacy, and reputational risk

Two planned AI IPOs, one buyer scorecard across 1,500+ discussions

- @AnthropicAI leads on capabilities > 96% of discussions touching its AI capabilities are positive in our data, versus 79% for OpenAI

- @OpenAI leads on cost > 67% of cost-effectiveness discussions were positive, versus 60% for Anthropic. Both beat the industry average

- Anthropic leads again on regulatory, compliance, and security > OpenAI landing below the industry benchmark

We spoke with 158 vector database experts over the past two weeks - fewer than 5% plan to cut spend over the next 12 months

Every agentic feature shipped needs context lookups, and that means more embeddings, more queries, more spend

"I was just pulling some numbers around how much we're using AI search and how much our vector database spend has actually grown. And, it's like 50 to 60% over the last twelve months." - Principal Enterprise Architect - Cybersecurity

AI security markets are the fastest-growing in cyber

Evaluations are spread across a deep bench of specialists like:

@hiddenlayersec@prompt_security (bought by $S)

@LakeraAI (bought by $CHKP)

@calypsoai (bought by $FFIV)

@ProtectAICorp (bought by $PANW)

@wiz_io (bought by $GOOG)

Incumbents' buying spree is well-timed - snapping up the specialists buyers are already evaluating

Another example, but we still see geopolitics as a concern in tech buyer interviews:

"We would also like to use DeepSeek but the issue with it is that of security concerns even though it is way cheaper than Anthropic or Llama and it has similar performance."

- Lead Data Scientist - Generative AI Natural Language Processing, IT & Telecom

What experts are actually saying on @deepseek_ai

Dominant theme: tension between DeepSeek’s compelling cost and performance profile and near-universal hesitation driven by its Chinese government ties and data security concerns

Source: @qualitateio

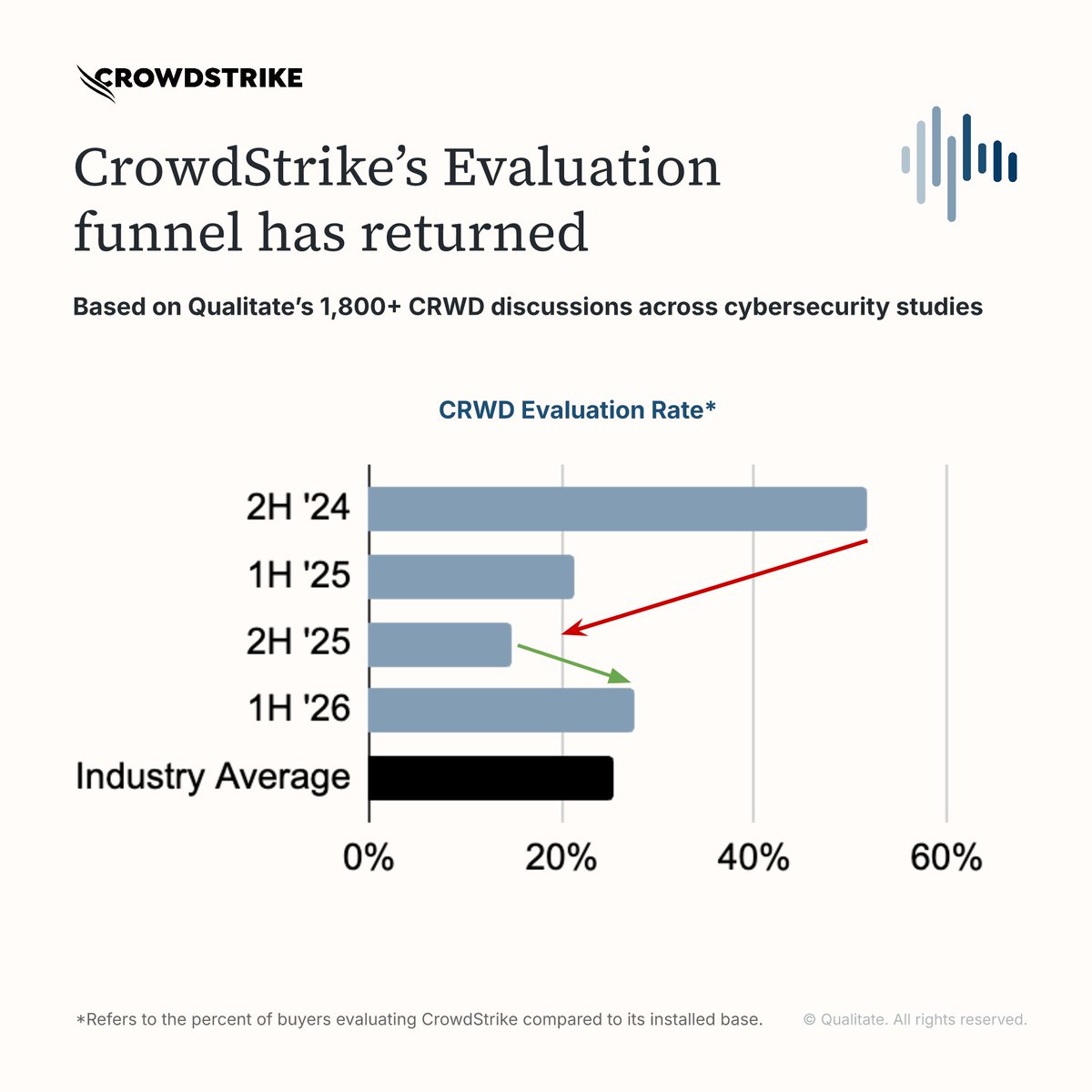

The $CRWD outage hurt evaluations, but now we’re seeing a resurrection.

CrowdStrike's evaluation funnel (aka buyers shortlisting) has risen from about 15% the size of its install base to 28% the size of its install base in Qualitate's 1H ‘26 data

Seeing big jump in senior tech buyers shortlisting @collibra for data governance

Evaluations are largely driven by:

- governance/compliance needs

- strong reputation

- collaboration capabilities

- replacement of competitor solutions

Context: based on @qualitateio's AI-moderated discussions with 556 cyber buyers in 1H'26

3. Vendor diversification - buyers leaning heavily on OpenAI and Anthropic still want a working Plan B

"While we're mostly doubling down on OpenAI and Anthropic, we're not really ignoring the rest of the market. For us, it's really about having a plan B." - Analytics Lead, IT & Telecom (Large Enterprise)

While @AnthropicAI and @OpenAI are grabbing headlines, open-source LLMs are still drawing enterprise customers.

I took a look at our expert discussion data and @MistralAI is the open-weight provider worth watching. Compared to xAI, $META, and @deepseek_ai, Mistral counted more wins than losses in our 1H '26 study with ~500 senior decision-makers.

Against the frontier labs, Mistral loses more than it wins. But buyers aren't choosing between them so much as choosing them for different use cases...

2. Cost - buyers credit Mistral's efficiency to deliberate model design

"We're more comfortable with Mistral AI because they have a strategy that is more based on scarcity. They produce models that don't cost a lot of tokens or a lot of GPUs to work." - CIO, Professional services (Large Enterprise)

Databricks is holding strong

I pulled what senior buyers are telling us about their spend on @databricks (n=296 in 1H'26)

Current customer spend growth at the 80th percentile among data management & AI vendors in 1H '26 - ahead of $SNOW

Looking ahead, next twelve month (NTM) spend plans have softened since 2H '24

But the drivers are optimization of existing deployments and continued stickiness, not pullback

Massive raise

Anthropic has a deep funnel heading into the 12 twelve months as we've been seeing in @qualitateio buyer interviews, previewing market share gains

We've raised $65 billion in Series H funding at a $965 billion post-money valuation, led by @AltimeterCap, Dragoneer, @Greenoaks, and @sequoia.

This investment will help us advance our research and expand our capacity to meet growing demand for Claude.

29% of $CRM upsells in 2H ’25 were directly driven by AI functionality, up 10pp in 6 months

Agentforce is a key incremental spend driver (just crossed $1B in ARR)

What’s standing out is where buyers increasing spend want agentic workflows to live: close to their existing systems and data

“If this is an agentic [component] that is going to be touching a Salesforce product, well, that is going to be running in Salesforce.” - Senior Director, IT Architecture, FinServ (Large Enterprise)

Seeing a lot more buyer awareness of Cortex - mentions appeared in ~7% $SNOW discussions in 1H'26 (up from 1-2% year prior)

Direct example of this - Senior Director, Data Strategy at large finserv enterprise (3/30/2026) reducing vendor spend to build on Snowflake:

"Vendors that we're decreasing spend with are Tableau, and we are trying to reduce our spend with Salesforce and Salesforce Marketing Cloud. We are trying to reduce our spend with Qualtrics survey analytics. And we are shifting those functions to internal tools or tools built on Snowflake and AWS Connect for our call center. We are also internally building using AI tools with Cursor, Claude Code, and Cortex Code to automate things that are being done by those tools as well"

From @qualitateio pool of 1,300+ Snowflake discussions

Behind $CRM earnings with 2,245 direct buyer discussions in last 12 months:

*Sticky core - entrenched in enterprise AI stacks

*AI-driven upside - Agentforce is primary incremental spend driver

*Cost-driven pressure at the margins - headcount reductions, license cost concerns, early platform migrations

Snapshot from @qualitateio research analyst

![ibselles's tweet photo. 29% of $CRM upsells in 2H ’25 were directly driven by AI functionality, up 10pp in 6 months

Agentforce is a key incremental spend driver (just crossed $1B in ARR)

What’s standing out is where buyers increasing spend want agentic workflows to live: close to their existing systems and data

“If this is an agentic [component] that is going to be touching a Salesforce product, well, that is going to be running in Salesforce.” - Senior Director, IT Architecture, FinServ (Large Enterprise)](https://pbs.twimg.com/media/HJalZo5XkAQ4Ffi.png)