🚨 ANTHROPIC MAY HAVE JUST DECLARED WAR ON THE ENTIRE SaaS INDUSTRY.

Anthropic launched Claude Tag on June 23, a persistent AI agent inside Slack that replaces its old Claude in Slack app.

Teams tag Claude in a channel, hand it a task, and it works in the background using approved tools, data, and even codebases, then posts results back to the thread.

Anthropic says 65% of its own product team's code is now generated through its internal version of Claude Tag.

Employees also use it to analyze metrics, process support tickets, and debug issues.

This matters because Claude is no longer a chatbot you open separately.

It lives where work already happens, remembers context across conversations, and can act without being asked through an optional "ambient mode."

That puts pressure on any tool that exists mainly to summarize, draft, research, or coordinate tasks.

Smaller SaaS products built as workflow wrappers face the most risk. Freelance platforms like Upwork could see less demand for basic research and writing work.

Even larger players like Atlassian face competition as AI agents start handling documentation and coordination tasks that used to need dedicated software.

Great feedback and review @danshipper. I guess its not quite suitable for a non-power-coding, Knowledge user like myself. looking forward to hearing more reviews, as I spend more time w this new model too

BREAKING:

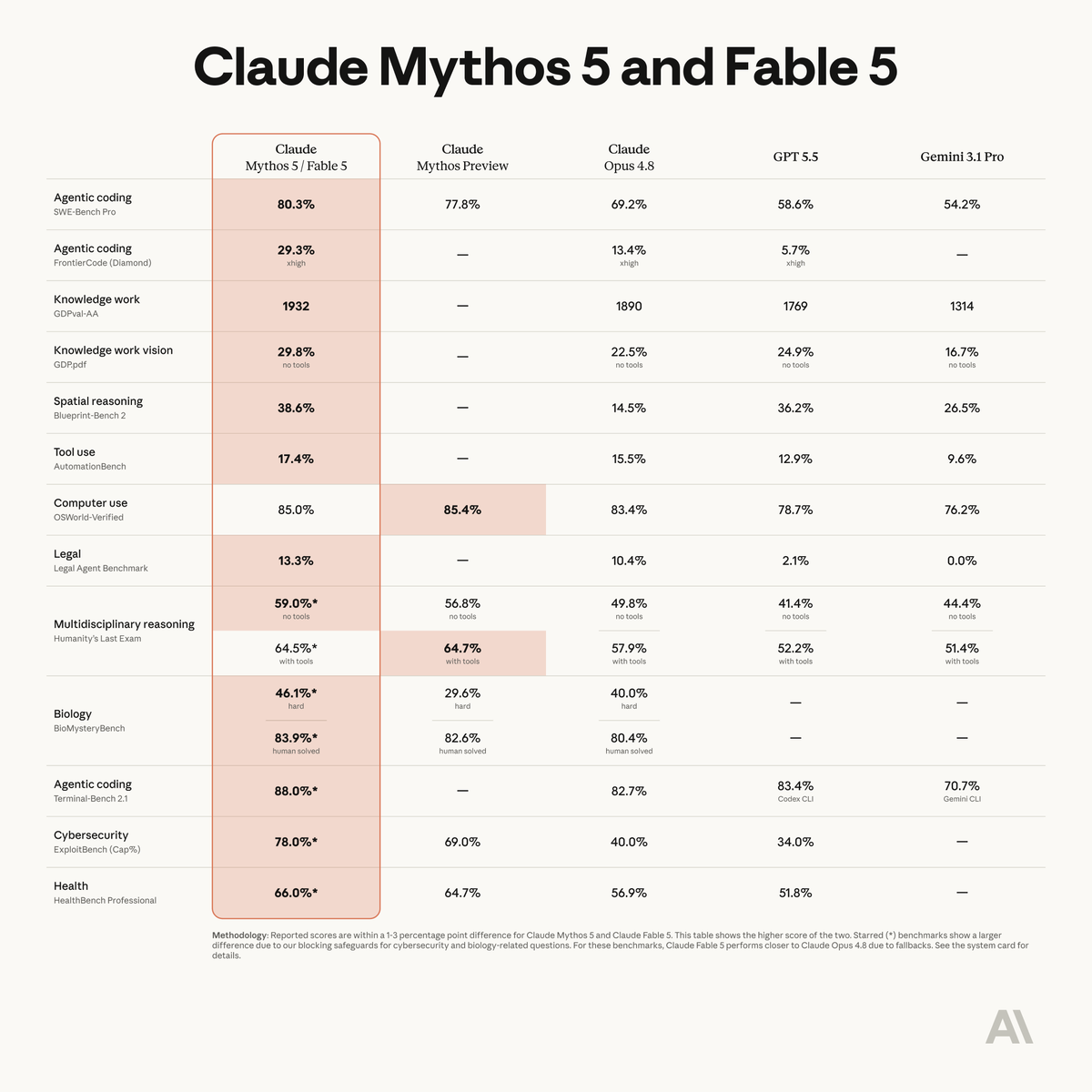

Anthropic just dropped Claude Fable 5—this is Mythos, made safe for public release. It is the best coding model in the world.

We've been testing it internally @every for the last week or so across coding, writing, marketing, editing, and more—here's our vibe check:

- It broke our benchmarks. Fable scored a 91/100 on our Senior Engineer benchmark—this is human senior engineer level. The previous high score was Opus 4.8 at 63. GPT-5.5 is a 62.

- It's a one-shot wonder. You can set it and forget for hours or overnight on huge coding tasks, and come back to completed work. It cleared entire production bug backlogs, built a playable 3D, and even made a 2-minute animated film—all one-shot.

- Taste and attention to detail. In coding and knowledge work tasks, it has much better taste and attention to detail than we've ever seen. It gets subtle things right, adds little features you might not have thought of, and generally understands the assignment in ways that surprised us.

- Great use of context. We set it loose analyzing customer feedback surveys and our website data and it came back with a crisp, clean report that identified a. our biggest problem and b. a concrete testable solution—and then we sent it off to build that.

- It's best for power users. If you're already used to orchestrating multiple agents in your work, this model can do things that you've never seen before. If you're a knowledge worker or vibe coder with a more basic setup, you're not going to notice a huge difference—in fact, it probably isn't the right model for you.

- It's very slow, token-hungry. Using this thing for regular knowledge work is like squashing an ant with a rocket launcher. It also routinely uses 500k to 1M tokens on tasks. That's why it's best for your heaviest jobs—but not as good for tasks like collaborative writing.

- It's expensive. It's about twice as expensive as Opus, and it's also incredibly token hungry—so expect it to be something you'll use sparingly unless your company pays for it.

Overall, I think of it like a warp drive for coding: It can get you across the galaxy in a few hours, when it used to take months or years. But it's not appropriate for getting around town—you need something faster, cheaper, and more maneuverable.

The ceiling is extraordinarily high on this model though. Even our most advanced testers like @kieranklaassen felt like they were only scratching the surface of it.

Want our full vibe check with all of our testing and benchmarks? Read it on @every: https://t.co/MgJLZszJUB

Fable 5 is state-of-the-art on nearly all tested benchmarks, with exceptional performance in software engineering, knowledge work, scientific research, and vision.

The longer and more complex the task, the larger Fable 5’s lead over our other models.

Bernstein estimates a $NVDA Vera Rubin NVL72 rack will cost ~$9.1M with HBM4 pricing rising to ~$53/GB by 2027 as volumes ramp.

That would put memory/storage near ~$3.2M per rack and imply a major HBM revenue step-up for $MU, Samsung and SK Hynix.

🚨 EVERYTHING THAT COULD GO WRONG FOR MARKETS WENT WRONG TODAY.

S&P 500 down -1.65%, wiping out $1.14 trillion.

Nasdaq down -2.60%, wiping out $1.11 trillion.

Gold down -3.38%, wiping out $1 trillion.

Silver down -6.9%, wiping out $280 billion.

Bitcoin down -6.31%, wiping out $80 billion.

In total $2.5 TRILLION wiped out in a single session. These were not isolated moves. Everything started breaking at the same time.

It started with the jobs report this morning.

The US economy added 172,000 jobs in May. Wall Street expected 88,000. That is almost double.

On any normal day, strong jobs is good news. But inflation is already at 3.8% and oil is sitting at $90. A labor market this strong tells the Fed it cannot cut interest rates and may actually need to raise them.

The probability of a rate hike this year went from 40% to 57% in a single day. That spooked every investor holding tech and growth stocks because higher rates mean those stocks are worth less today.

Then the AI trade started cracking.

Yesterday Broadcom reported record earnings: revenue up 48%, AI chip sales up 143% and the stock still crashed 12.6%. The reason was simple.

Broadcom did not raise its AI revenue targets for the year. Investors had expected it to. That single miss made people ask a question they had been avoiding for months: are we paying too much for AI stocks?

That question got louder today when a research firm called SemiAnalysis revealed that Nvidia's next-generation AI chips will need significantly less memory than everyone assumed, roughly half of what the market was pricing in.

Memory chips are what companies like SK Hynix and Samsung make. SK Hynix fell nearly 10% today. Samsung fell over 6%.

South Korea's entire stock market crashed 5.5% in a single session. Japan's semiconductor stocks did the same.

And then Anthropic added fuel to the fire by publishing a report warning that AI is getting close to the point where it can improve itself without human help and calling for a global pause in AI development.

Coming on the same day as the memory demand news and Broadcom's miss, it fed a single growing fear across the market: what if the AI boom is moving faster than the business models can keep up with?

Underneath all of this, there is a liquidity problem nobody is talking about.

SpaceX goes public next week at a $1.75 trillion valuation. Anthropic just filed to go public. OpenAI is next.

These three companies together are worth $4 to $5 trillion. Fund managers need cash to buy into these listings.

But cash levels are already at their lowest since early 2024. The only way to raise cash is to sell what they already own. That selling is happening right now.

The new Fed Chair Kevin Warsh will also hold his very first policy meeting in 11 days. He was appointed by Trump with the expectation of cutting rates.

He is now walking into a situation where inflation is high, oil is high, and the job market is running hot. Investors do not know what he will do.

When nobody knows what the most powerful central banker in the world will decide in less than two weeks, the safest move is to reduce risk today.

Everything that could go wrong, went wrong at the same time. A hot jobs report, a collapsing ceasefire, a crack in the AI trade, a trillion dollar liquidity drain, and a Fed meeting with no clear outcome.

97% probability $SPY crashes at least 10% after June 15.

There's 4 massive reasons $SPY can't avoid it:

1. Large IPOs like $SPCX will trigger sell off.

Major IPOs drain liquidity. The 1999–2000 dot-com IPO wave pulled $100B+ from markets before $SPY crashed 78%.

2. Kevin Warsh hawkish FOMC on June 17

Hawkish Fed surprises trigger immediate selloffs. In June 2022, a surprise 75bps hike sent SPY down 8.4% in 5 days.

3. $MU $ORCL earnings is the peak of market

Semis and enterprise software peak earnings historically signal cycle tops. $MU peaked in June 2018 $SPY followed with a 20% correction by December.

4. Midterm elections for Trump is this year

Midterm years average a 17% $SPY drawdown before Q4 recovery. 2022 saw $SPY drop 25% into October before reversing Trump's 2026 midterms follow the same cycle.

♻️ RESHARE this post and write 1 comment, I'll share with you my $SPY target for the crash.

Every software company just got a second life and Jensen just explained why (Save this).

The conventional fear was straightforward, AI agents replace human workers, human workers use software tools, therefore agents destroy SaaS.

Jensen Huang stood on stage at Computex 2026 and walked through exactly why that logic is backwards.

Agents don't replace software, they consume it at machine speed, around the clock, without weekends.

Here's the actual architecture Jensen laid out.

An agent isn't just a large language model but rather an LLM sitting inside a harness that manages memory, orchestrates tool use, routes context, and plans iterative actions.

That harness has to constantly call tools, spreadsheets, databases, browsers, and code engines, with every reasoning loop triggering another tool call.

A human might use Salesforce 40 hours a week, an agent running inside a company uses it 168 hours a week and never misses a context window.

The GitHub data Jensen showed on stage makes it tangible, 90 million pull requests merged, 1.4 billion commits, and 20 million new repositories created every month.

As of April 2026, GitHub is processing 275 million commits per week on pace for roughly 14 billion by year end, a 14x explosion in a single year and AI agents are the source.

Pull requests opened by AI agents went from 4 million in September 2025 to 17 million in March 2026 more than 4x in six months.

That's AI becoming the largest software user on earth.

Goldman Sachs quantified the downstream effect last month, token consumption is expected to multiply 24x by 2030, reaching 120 quadrillion tokens per month globally.

A traditional chatbot consumes roughly 1,000 tokens per session, an embedded copilot burns 5,000 tokens per day while a continuously running enterprise agent? Over 100,000 tokens per day.

The software companies that figured this out first are already printing money, Salesforce Agentforce hit $800 million ARR growing 169% year over year, with 29,000 deals closed.

ServiceNow's Now Assist crossed $600 million in ACV, just raised its full year target to $1.5 billion, and told investors that when its agents replace a 20-person support team, total ServiceNow spend by that customer grows more than 5x even after accounting for reduced seat licenses.

Workday delivered 1.7 billion AI actions across its platform in fiscal 2026.

The key unlock Jensen pointed to and what investors need to understand is MCP, the model context protocol is the interface layer that makes software agent-readable.

Software that supports MCP can be called by any agent, from any model, through any harness.

Anthropic created it, OpenAI, Microsoft, and Google all adopted it and it was donated to the Linux Foundation.

It is effectively becoming the HTTP of agentic computing.

Software companies with native MCP support are plugged into the agent economy.

Software companies still waiting are one product cycle away from becoming invisible to the fastest-growing category of software users in history.

$MRVL Revenue Structure — Breakdown-

How they actually report it:

Officially, $MRVL reports 2 end markets:

1/ Data center = $6.1B (74% of total) for FY2026, vs $4.2B in FY2025 and $2.2B in FY2024

2/ Communications & Other = $2.1B (26%) for FY2026

So full-year FY2026 total = $8.2B, up 42% YoY 📈

Most recently, Q1 FY2027 data center hit $1.83B (76% of revenue), with comms & other at $585M (24%)

Within Data Center — the real breakdown you want:

The two pillars are:

1. Custom Silicon / XPU (ASIC)

This is the biggest and fastest-growing bucket — Google TPUs, Amazon Trainium, and Microsoft custom AI chips.

Custom silicon programs entered volume production in Q1 FY2026 and are the primary driver of the 76% YoY data center surge .

Analyst estimates put custom at roughly 55-65% of data center revenue in FY2026, likely approaching $ 3.5-4B for the year.

2. Electro-Optics (DSPs, TIAs, laser drivers, DCI modules)

$MRVL’s electro-optics portfolio — including high-speed PAM4 DSPs, TIAs, laser drivers, and datacenter interconnect modules — leads the market and contributes substantially to AI revenue .

The most recent Q1 FY2027 call specifically called out strength in 800G and 1.6T scale-out optics, scale-up optical solutions for NPO and CPO applications, and scale-across datacenter interconnect modules .

Optics is estimated at roughly 25-35% of data center revenue !!

3. Data Center Networking / Switching

Ethernet switches (51.2T), PCIe/CXL switches (via XConn). Smaller but growing.

The forward story:

Celestial AI (acquired Feb 2026) brings Photonic Fabric optical interconnect technology for scale-up connectivity, with Marvell expecting meaningful revenue starting H2 FY2028, targeting a $500M ARR by Q4 FY28, doubling to $1B by Q4 FY2029 .

So the optics bucket is about to get a major uplift layer on top of the existing DSP/transceiver business.

The ASIC/XPU side is what’s driving the valuation re-rate — it’s why $MRVL trades at a significant premium. Optics is the asymmetric upside kicker, especially post-Celestial AI.

Trading at life-time high P/S of 30 !!

BREAKING: As Anthropic confidentially files a draft S-1 for an IPO, the company is now expected to close above $1.8 trillion in market cap on its first day of trading.

Between SpaceX and Anthropic, combined market cap on IPO day is expected to exceed $3.5 trillion.

JENSEN AT COMPUTEX TAIPEI JUST NOW:

- Marvell will become the next trillion-dollar company

- Marvell and Nvidia are strengthening their partnership to expand critical networking & connectivity to power AI data centers

Jensen touch...plus 17% 😂

Prompting is the worst way to use Claude in 2026.

Here's what the top 1% do instead:

They set up these 5 files once.

Then they barely prompt again.

File 1: about-me .md (Your identity)

Who you are, how you write, how you think.

Open Cowork. Use Opus 4.7 + Adaptive thinking.

Prompt: "Build my about-me .md. Interview me with 20 questions via AskUserQuestion.

To download mine, go to https://t.co/psB7XxB2Y4.

Don't pay anything. It's free in the welcome email.

File 2: anti-ai-writing-style .md (Your boundaries)

Every word you ban, the structure you reject, tone you hate. 80% of this file is what you're NOT.

Go to https://t.co/psB7XxB2Y4 to download anti AI guide.

Don't pay .Open the email. Click on Notion.

Open '.md files' Download 'ANTI AI STYLE .md'.

File 3: my-company .md (your goals & hard nos)

Same Cowork session as about-me.

Prompt: "Build my my-company .md. 6-8 questions on goals and decisions. Under 1,000 tokens."

Cover: yearly targets with numbers, quarterly focus.

File 4: global-instructions .md (persistent rules)

Settings → Cowork → Global Instructions.

Paste this: "Before every task, read every file in ABOUT ME/. Never touch OUTPUTS/ or TEMPLATES/ unless I point you to a file. Save deliverables in OUTPUTS/. If unclear, use AskUserQuestion."

Claude follows them before every task.

File 5: /47 skill (your prompt automation)

Download directly from https://t.co/psB7XxB2Y4.

Upload it via Customize → Skills.

Type /47 + your bad prompt.

Claude rewrites it with action verbs, and "go beyond the basics" on creative work.

The secret was always these 5 files behind it.

I wrote 2 guides so you can copy my exact system:

✦ My full 5-file setup: https://t.co/psB7XxB2Y4

✦ My Cowork folder walkthrough: https://t.co/uWTpOI3Woc

(save this to never write a long prompt to Claude)

I worked as a Big 4 auditor for a decade, here’s my take on the Burry “Fugazi” thread

The transaction is real and the figures check out. Apollo led a $3.5bn capital solution for Valor Compute Infrastructure to fund a $5.4bn purchase of GB200 GPUs leased to xAI on a triple-net structure. Nvidia went in as an anchor LP. All publicly disclosed

But the accounting isn’t prima facie erroneous, and the thread oversells two things

On Nvidia’s revenue. Selling to an SPV is fine. The question under ASC 606 (US revenue standard) is whether control actually transferred. If VCI bears the risks and rewards, Nvidia books the sale legitimately

The REAL issue is the $1.9bn Nvidia ploughs back into VCI as an LP. That’s the round-trip. Net, Nvidia took in roughly $3.5bn of outside cash but booked $5.4bn of revenue

If part of your “sale” is funded by capital you re-injected, that portion isn’t a sale. The honest treatment is either net the $1.9bn off the transaction price, or run a “variable interest entity” (VIE) analysis and consolidate VCI. Recognising gross revenue on round-tripped capital is the potential weak apot

On “legally invisible.” This is rhetoric. The chips sit on VCI’s balance sheet, xAI carries an ROU asset and lease liability under ASC 842 (US leasing accounting standard). Nothing vanishes. It’s held by an entity nobody consolidates, and whether that non-consolidation is correct is the VIE question above

On Level 3 (fair value measurement tier). “No outside party can verify what they’re worth” is wrong. Level 3 means no observable inputs for that specific asset, NOT unverifiable

We typically ALWAYS brought in valuation specialists particularly for high risk material txs, you use observable comps and secondary GPU prices as model inputs, and auditors treat it as a critical audit matter. It gets more scrutiny, not less

The legitimate concern is smaller than this post lets on. Level 3 marks are management estimates exposed to optimistic bias, 34.7% concentration is high for retail annuity backing, and that sits on top of 16.6x leverage and a Bermuda captive outside US statutory oversight. Stack GPU residual-value risk on a multi-year lease and that’s the main concern

Burry’s substance is defensible. The “retirees unknowingly carry invisible risk” packaging is sensationalised. Policyholders hold fixed contractual claims, their exposure is to Athene’s solvency, not directly to GPU residuals

TLDR: auditors need to test whether the sale is overstated by the $1.9bn round-trip, and apply extra scrutiny to the unobservable Level 3 inputs

I’d hate to be the Audit partner signing these transactions off particularly given the public interest and frequency of similar transactions

Arthur Anderson Déjà vu?

You know what I’ve started to really think about…

In 2008, those that called the housing crisis had something that the entire stock market did not have: data around the housing crisis.

Now, the data was available to the entire market, but only a few people chose to deeply study it and interpret what could happen.

In today’s AI driven stock market, the only way for there to be a 2008 like crash is if there is something underneath the surface that the market is completely ignoring.

That would have to be the smoking gun that someone finds out about and can then use to determine what would crash the entire rally.

But…isn’t everyone already looking for that?! Like, aren’t people obsessed with trying to find out how the bubble pops?

We have people daily dedicating every bit of their research to find out how this breaks. Every argument, whether it’s circular funding or capex slows down or higher inflation etc is theorized about daily.

It’s almost like we have so many people afraid of the dot com bubble happening again that there is an OVER emphasis on all the things that can go wrong (which is healthy) and as a result, every massive bear case is already out there…already discovered…already priced in.

Which means that if every market participant is analyzing every single thing that could go wrong, there is going to need to be a REALLY good and original bear argument for things to go bad.

Everytime you hear a bear case, it should be more original and something you haven’t thought of because if not, it might have already been discovered and not actually be a bear case.

Rule changes for the SpaceX $SPCX IPO:

Index providers waived the profitability requirement and cut the seasoning window from 90 days to 5.

This forces over $30 trillion in passive 401k and retirement money to buy SpaceX at IPO valuations.

Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months.

Russell 1000 and Nasdaq 100 funds will absorb 24%.

The rules built to protect passive investors:

1. S&P 500 has required 12 months of trading and 4 quarters of GAAP profitability since 2002. Both waived.

2. Nasdaq cut its inclusion window from 90 trading days to 15.

3. FTSE Russell cut its to 5.

All three benchmarks are now structured to buy SpaceX at IPO pricing.

The SpaceX IPO and Data Centers in Space

There isn't a financial model that justifies the SpaceX IPO, but data centers in space are plausible, and that might be enough.

https://t.co/ZiN64VB8Ay

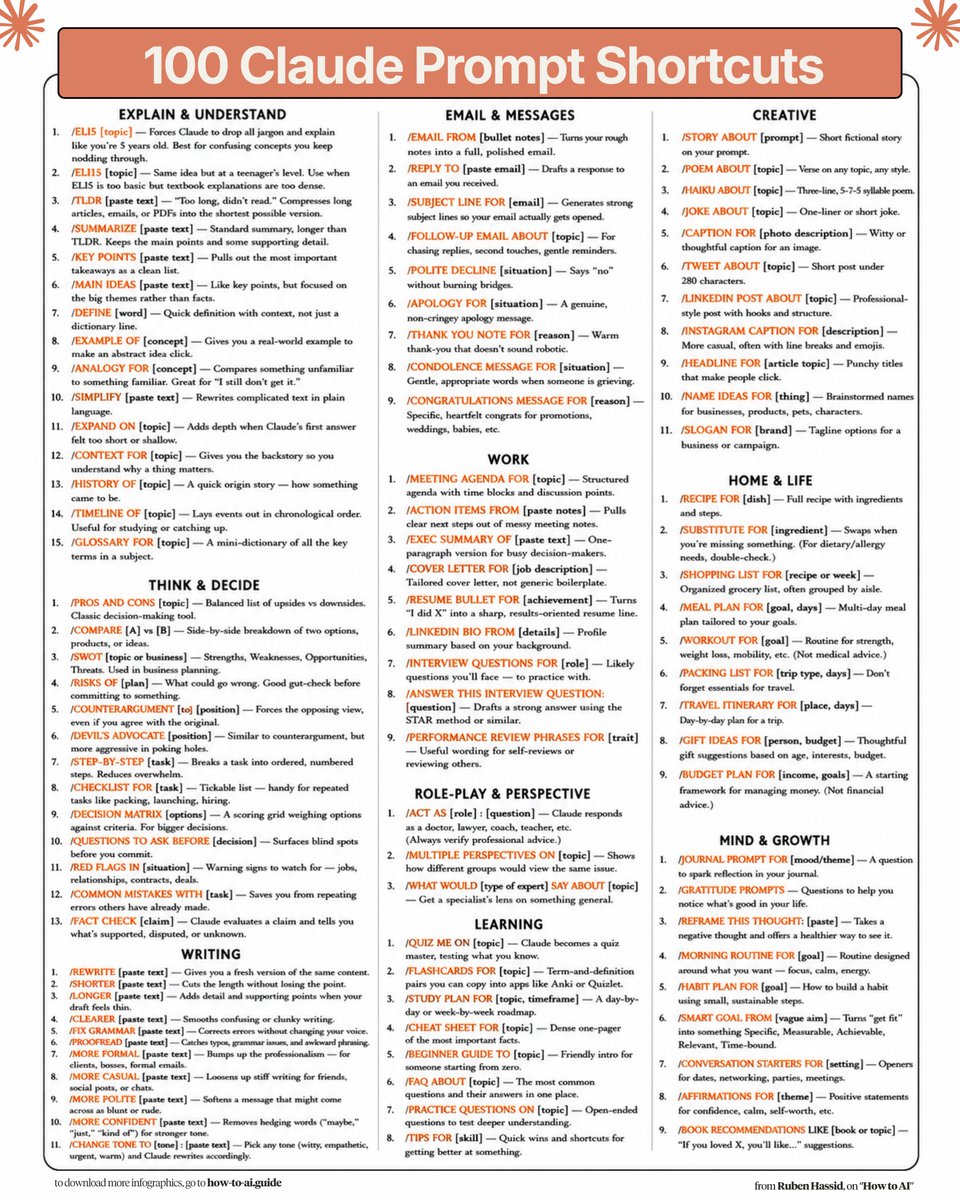

Stop typing long prompts to Claude.

Save this image for 100 prompt shortcut hacks:

1 - Download this infographic. Send it to your team.

2 - Add these at the very start of your prompt.

3 - Pro tip: Use /TLDR for long articles. /ELI5 for confusing concepts. /STEP-BY-STEP for any task you're stuck on.

To (actually) learn how to prompt Claude properly.

Read my free guide here: https://t.co/Sw2tg2QkBK

To copy-paste all of these prompt shortcuts:

Step 1. Go to https://t.co/psB7XxB2Y4.

Step 2. Subscribe for free. Don't pay anything.

Step 3. Open my welcome email (most skip this).

Step 4. Hit the automatic reply button inside.

Step 5. Go to the Notion link.

Step 6. Open the "Claude cowork" folder.

Step 7. Locate "PROMPT SHORTCUTS" toggle list.

♻️ Repost this to save your team 10 hours a week.

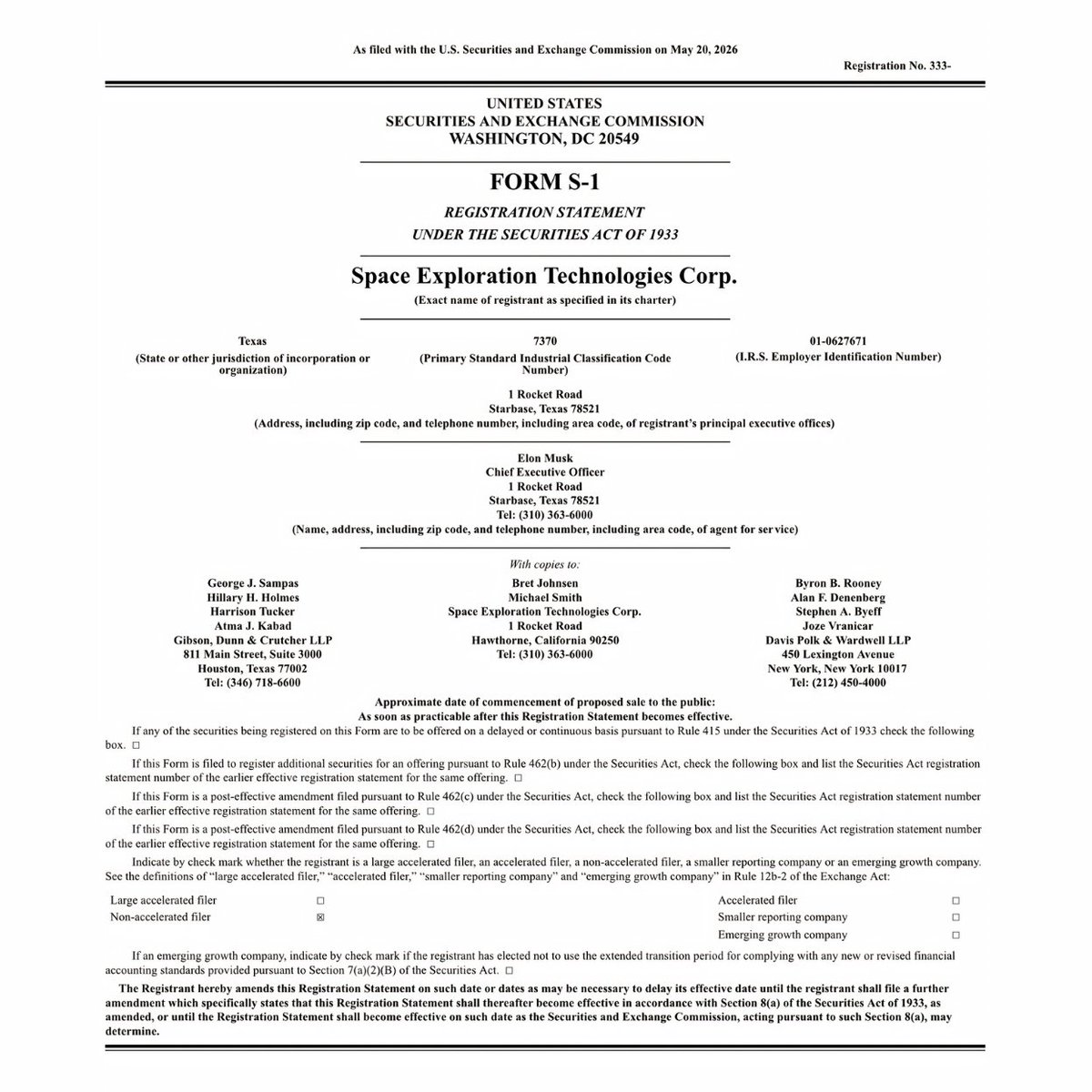

Breaking: SpaceX just officially filed for the largest IPO in human history

It'll be listed under the ticker $SPCX, dual listed on Nasdaq and Nasdaq Texas.

The company is targeting a valuation of $1.75 trillion and aims to raise $75 billion, more than double Saudi Aramco's $26 billion record from 2019.

The S-1 reveals the numbers for the first time.

In Q1 2026, SpaceX generated $4.69 billion in revenue and lost $1.94 billion from operations. In all of 2025, it generated $18.67 billion in revenue and lost $2.59 billion from operations.

Starlink is the only part of the business making money.

It generated $3.26 billion in revenue in Q1 2026 with $1.19 billion in operating income across 10.3 million subscribers in 164 countries.

The AI segment generated $818 million in revenue but lost $2.47 billion in the same quarter. In all of 2025, the AI segment lost $6.36 billion.

Of the $10.1 billion spent on capex in Q1 2026, $7.72 billion went to the AI division.

The S-1 also disclosed several things nobody knew before. SpaceX is building a platform called Macrohard, described as a fully AI-operated software company.

It is building Terafab, a chip manufacturing initiative targeting one terawatt of compute hardware per year. Its flagship AI data center called Colossus is already operating in Memphis Tennessee as a gigawatt scale training cluster, with Colossus II already under construction.

SpaceX plans to launch orbital AI data centers into space by 2028, using solar power for energy and the space environment for cooling.

Elon Musk will hold majority voting control through Class B shares that carry 10 votes per share versus 1 vote for the Class A shares being sold to the public.

He will control the outcome of every shareholder vote after the IPO regardless of how many shares the public owns.

Once listed, SpaceX joins the Nasdaq-100 after just 15 days of trading, forcing every index fund tracking the index to buy the stock.

🚨 Anthropic just showed a 27-minute workshop on how to actually do prompts for Claude.

Taught by the people who built it.

Free. No registration. No paywall.

I've seen $300 courses that don't cover what they teach in the first 8 minutes.

Watch it and bookmark it now.

You don't understand the current AI race if you don't think about it in terms of compute - and compute clearly distinguishes 3 tiers of companies.

Arthur Mensch, Mistral's CEO, recently had a hearing at the French Assemblée Nationale. He elegantly framed the AI race as a compute issue, where sovereignty would be ~"the ability to get leverage along the AI value chain" from electrons to tokens.

He also provided numbers (in MW) for Mistral's available compute : I was surprised at how low these numbers were compared to the gargantuan numbers touted by US labs.

So I ran the numbers, based on the recent and excellent @EpochAIResearch study, adding in my (not that reliable) AI-powered estimates of Chinese compute (see assumptions in blog post).

And I found out that there are 3 quite separate tiers.

1. US Champions are really far ahead. Anthropic, OpenAI and Google each command multiple gigawatts (OpenAI ~15 GW once you count the Stargate/Azure/Oracle capacity it rents). Ever wondered why their Claude/GPT /Gemini consistently top benchmarks? Now you know. By the way, tick in Meta and xAI and you'll see them entering tier 1 too with their recent buildouts.

2. Chinese giants scale fast. Alibaba, ByteDance, Tencent, Huawei and the three state telcos are racing from hundreds of MW toward multi-GW, increasingly on domestic Ascend silicon and the national "East Data West Compute" grid. They report "computing power" in EFLOPS rather than MW, so their points here are estimates, could be quite off the mark.

3. The contenders. Europe's Mistral commands ~90 MW today and aims at 1 GW by 2029, an order of magnitude behind the leaders. Interestingly, some of the best Chinese labs (DeepSeek, Moonshot, Zhipu, MiniMax) have no longstanding compute : they are pure-play : they rent or get allocations from government capacity for specific efforts. DeepSeek (~90 MW, the only one of this category that owns its cluster) is the largest.

With all that said, I hope someday someone in Europe wakes up to the absolute necessity of building compute faster than we do today.

If you want to go inspect the graph, I've got the interactive version and full sources in my blog post, link below.