The compute tray is the brain of an AI server rack, providing the primary processing logic required for AI workloads. Each compute tray typically contains one or more compute boards, non-volatile memory express (NVMe) solid-state drives (SSDs) for storage, network interface cards (NICs) for connectivity, data processing units (DPUs) for organizing data into discrete processing units, and a power distribution unit (PDU). This tray bears the most expensive, advanced, and most concentrated semiconductor components within a server rack, as it is directly responsible for performance per watt and AI workload throughput.

Source: SIA & Deloitte

👀1Q26 top-10 foundry revenue defied seasonality, up 3.7% QoQ to a quarterly record. Foundries are preparing 2H26 price hikes as utilization recovers. How will the market respond? 💡More analysis from #TrendForce: https://t.co/eBN461xTyk 🔗

TSMC's #CoPoS is moving fast, and the opportunities for Taiwan suppliers are taking shape. CoPoS replaces traditional round glass carrier with a square panel format, pushing utilization rates above 75%.

More on glass material development: https://t.co/Na9XtpNK8Q 🔗

Key takeaways from Ming-Chi Kuo’s analysis on TSMC CoPoS:

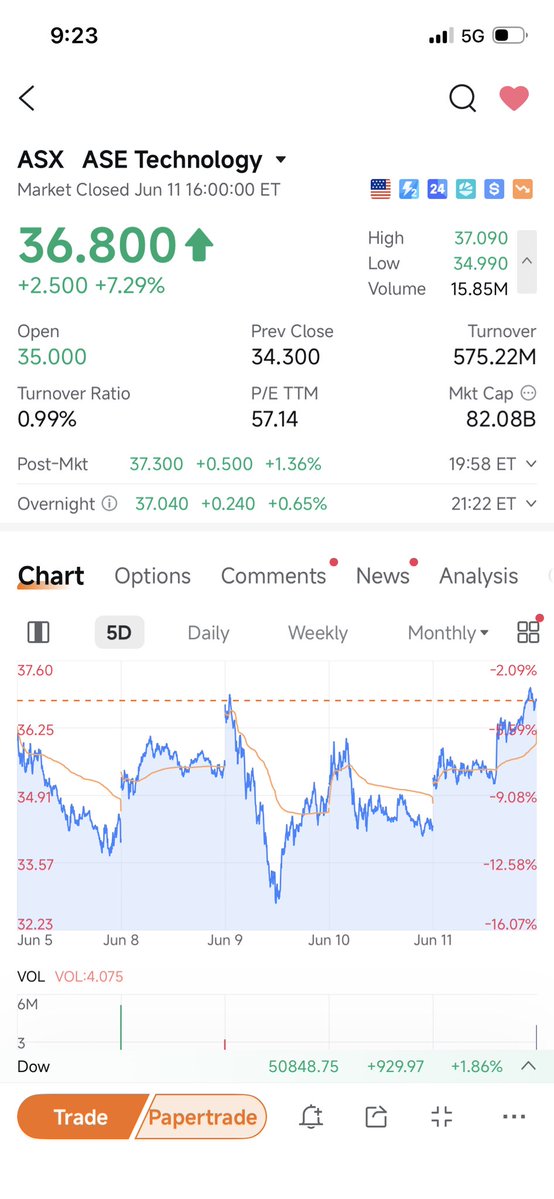

From a Taiwan investor’s perspective, while TSMC is clearly leading the next generation of advanced packaging with CoWoS and the upcoming CoPoS, one of the clearest beneficiaries is ASE Technology Holding ($ASX).

ASE is already expanding panel-level packaging capabilities, including its 310mm × 310mm automated production line. Its advanced packaging platforms such as FoCoS and FoCoS-Bridge are directly aligned with the industry’s shift toward larger and more complex AI/HPC packages.

Bullish on $ASX.

$TSM #CoPoS

《GF Overseas Electronics & Communications》

☄️ CCL: PTFE material adopted for orthogonal backplanes

👉 Nvidia has confirmed the adoption of PTFE as the core material for Rubin Ultra orthogonal backplanes. Below is our related analysis.

☀️ Orthogonal backplanes officially adopt PTFE material

According to our industry-chain checks, the previous M9 + Q-glass cloth solution failed to meet the required electrical performance standards. As a result, PTFE was ultimately selected as the core material for orthogonal backplanes.

PTFE offers excellent high-frequency transmission characteristics, with lower signal loss, and can support 337G and above SerDes signal transmission on the Rubin Ultra platform.

Traditional PTFE materials are relatively soft, making them prone to burr formation during drilling, which creates challenges for mass production. However, the newly developed silicon dioxide, SiO₂, filler-modified PTFE has significantly improved mechanical rigidity. This material has now successfully passed electrical performance testing and mass-production feasibility validation.

☀️ PTFE to gradually replace traditional glass-fiber materials

PTFE CCL no longer uses glass-fiber cloth. The production process involves coating hydrocarbon resin onto the PTFE surface, then directly laminating it with copper foil.

According to our checks, the unit price of the modified PTFE material is around RMB 150,000 per ton, and each CCL sheet uses approximately 800g of PTFE. The selling price of a finished PTFE CCL sheet can reach RMB 2,500.

At present, the final design of the orthogonal backplane has not yet been determined. Candidate designs include mixed-stack combinations of 78-layer and 108-layer structures using PTFE CCL / M9-Q cloth / ABF-filled CCL. The final design is expected to be confirmed in July.

☀️ Summary of PTFE industry-chain beneficiaries

We expect Shengyi Technology, https://t.co/MyWBLDCSCJ, to become the primary supplier of PTFE CCL. Taiflex, https://t.co/J88n54Nui2, is currently in the product qualification stage and has a high chance of becoming a secondary supplier.

On the upstream raw-material side, Dongyue Group, https://t.co/GCCsVNbOdg, is currently Shengyi Technology’s key PTFE raw-material supplier. Daikin, https://t.co/ZAZYazoMw4, and Haohua Chemical, https://t.co/O0itg20aMk, are potential raw-material suppliers.

Based on the initial order scale, the PTFE CCL TAM corresponding to the 2027 Kyber platform could reach RMB 8 billion. Subsequent volume ramp from the Feynman platform is expected to drive additional demand.

Due to the complexity of the manufacturing process, mass production of midplane-related products is expected to begin from the end of 2026.

The new process is also positive for PCB manufacturers. In current HLC PCB products, the ratio of total PCB value to CCL material value is around 2–2.5x. Under the new design, this ratio could rise to 3–3.5x, significantly increasing the product value for PCB manufacturers.

🤔The race to 400-layer NAND is reaching a critical tipping point, and memory giants like #Samsung, #SKhynix, and #Kioxia are pulling out all the stops.

▶ AI servers squeeze high-end MLCC supply, sending Taiwan firms toward China alternatives

- Expanding demand from AI servers and high-voltage EVs is tightening the global supply of high-end MLCCs; to cope with lengthening lead times, some Taiwanese supply-chain players are moving to qualify Chinese alternative sources such as Chaozhou Three-Circle.

- Supply-chain sources characterize the current market as a structurally tight phase rather than an outright shortage, with demand for high-capacitance, high-voltage, high-reliability MLCCs for AI servers, HPC, and 800V EV platforms rising faster than expected.

- Lead times for some MLCC part numbers have stretched to more than 20 weeks from prior bookings, with certain products facing even longer delivery schedules.

- Customers are paying more attention to supply stability than to price, and procurement teams are prioritizing inventory buffers and source reliability to reduce the risk of production stoppages.

- Murata and several major Taiwanese suppliers are managing high-end MLCC order intake and shipments on a restricted basis, while the expansion of AI data centers and EV electrification is prompting downstream customers to increasingly secure second- and third-source suppliers.

- Three-Circle, having expanded into high-end MLCCs over the past several years, stands to benefit, and Chinese players such as Three-Circle and Fenghua Advanced Technology are maintaining high utilization rates.

- The "order lock-up" cited across the industry is interpreted not as a halt to new orders but as a prioritized allocation to long-term customers and contracted demand; in the AI server supply chain in particular, CSPs and AI platform customers are pre-empting high-end MLCC capacity through LTAs.

- Rising GPU power consumption is increasing reliance on MLCCs for voltage regulation and filtering inside AI servers; AI server platforms require several times more MLCCs than standard servers, driving the increase in high-end product demand.

- Because the 2018 passive-component shortage was followed by a sharp price reversal after channel over-ordering and inventory build-up, manufacturers in this cycle are managing overheating risk by pacing shipments, verifying real demand, and limiting spot transactions.

- In the MLCC market, commodity products for consumer electronics are recovering toward balance following inventory adjustments, whereas high-end MLCCs for AI servers, data centers, automotive, and industrial applications remain in tight supply-demand conditions.

- High-end MLCCs require advanced material formulations, ultra-thin dielectric processing, and precision multilayer stacking technology, making it hard to close the supply-demand gap quickly through short-term capacity additions; tight supply is expected to persist over the next one to two years.

- Within the Taiwanese supply chain, Yageo and Walsin Technology are expected to benefit, though a portion of demand is also beginning to shift toward the Chinese MLCC supply chain.

The development of CPC is not the result of a single company’s technological breakthrough, but rather the co-evolution of an entire industry ecosystem.

At the hardware level, CPC requires high-precision connectors and cable technologies. Companies such as Samtec, Amphenol, and TE Connectivity play critical roles in this space. These suppliers have long provided DAC cables and high-speed connectors for data centers, giving them a strong technological foundation in the CPC era.

#SemiVision #Semiconductor #SiPh #SiliconPhotonics #CPO #Photonics #AI #Insight #Technology

U.S. officials are reportedly pressing China over delays in indium phosphide export approvals, as the material becomes a bottleneck for AI data center buildouts.

Reuters says Coherent CEO Jim Anderson raised the issue during a U.S. business delegation trip to China in May, and it was also discussed in U.S.-China trade talks in Seoul.

FWIW: InP is critical for photonic chips used in high-speed AI infrastructure.

AXT $AXTI says InP export permits are its biggest current challenge.

Coherent $COHR warned of an InP shortage in May.

Lumentum $LITE is reportedly sold out through 2028 despite quadrupling output.

6-inch InP wafer prices are up 250% to around $5,000.

Key takeaways on TSMC's next-generation advanced packaging, CoPoS (publicly available technical details omitted):

1. CoPoS is currently expected to enter mass production in 2H28. It is designed to improve the economics of ultra-large packages above the 9.5x reticle-size class, with NVIDIA’s Feynman AI chip a potential first adopter.

2. According to industry checks, glass is used in two distinct places (dimensions in mm):

→ 310 x 310 temporary glass carriers

→ 250 x 250 (pilot) / 510 x 515 (mass production) glass panels, processed and later cut into individual glass core substrates

3. The glass core substrate is essentially a three-layer structure: a glass core sandwiched between ABF (ABF-GCP) build-up layers on both sides. The widely discussed glass processing challenges, such as TGV formation and copper filling / metallization, are tied to this part of the stack.

4. Common misconceptions about CoPoS:

→ ❌ Misconception 1: CoPoS uses a glass interposer. ⭕️ Correction: The glass is not an interposer. The interconnect role is instead handled by the chip-side RDL, plus the TGV/Cu interconnects and ABF build-up layers in the glass-core substrate stack.

→ ❌ Misconception 2: Glass replaces ABF. ⭕️ Correction: As the substrate architecture above shows, glass and ABF coexist.

→ ❌ Misconception 3: Chips sit directly on glass. ⭕️ Correction: Chips are attached to the ABF build-up surface of the glass core substrate.

5. CoPoS should extend and reinforce TSMC’s leadership in advanced packaging, potentially giving that advantage visibility through around 2032.

Very interesting and scary report from Morgan Stanley

The financial engineering behind hyperscaler capex

The truly unsettling part of the AI boom isn’t how much money is being spent

It’s how that money is being engineered through accounting

Hidden liabilities (> $1.8T)

Huge obligations sit off‑balance‑sheet: nearly $1T in purchase commitments, $800B+ in leases not yet started, $2T+ in RPO.

Future cash outflows that don’t show up as debt.

The coming depreciation hit

Profits look good only because spending is stuck in CIP.

Big Tech faces $520B+ in depreciation over 3 years.

ORCL’s depreciation ratio: 7% → 28%.

Supplier financing pressure

Unpaid capex is ~$110B.

ORCL’s DPO exploded from 35 → 170 days.

The whole supply chain is effectively financing the AI build‑out.

Lease accounting gray zones

Whether GPU contracts count as leases or services is subjective — and companies use that flexibility to shift billions on/off the balance sheet.

$ORCL = the most aggressive

Largest lease commitments, RPO up 300%+, capex‑to‑sales hitting 189%.

Oracle is running the highest financial leverage in the ecosystem.