The problem is treating wealth as a goal in itself, rather than as a means of supporting you in achieving your goals.

Meaningful goals are things like: building a family, building relationships, acquiring skills, building a business, having new experiences, overcoming challenges, creating and experiencing art.

You can never be “done” with those goals because pursuing them and progressing in them is intrinsically satisfying, in a way that increasing the number in your bank account never can be.

Never forget that money is only a means to achieving your real goals, never a goal in itself.

The highest-expected-value bet is also the one most likely to wipe you out:

Victor Haghani co-founded LTCM & wrote The Missing Billionaires. Now runs Elm Wealth.

Victor Haghani explains:

"Take a coin that lands heads 60% of the time. You get 20 flips."

"The highest-expected-value play is to bet it all on heads, every single time."

"And you have almost no chance of ending with any money at all."

"The whole expected value sits in one outcome: 20 heads, a million-fold return."

"Everyone instantly knows they'd never do it."

"Expected value and risk-adjusted value are two different things — and it's the second one that matters."

Nearly 20 years ago, @MebFaber published "A Quantitative Approach to Tactical Asset Allocation", one of the most influential investment research papers of the past two decades and, at the time, the third most-read paper on all of SSRN.

In our latest @ConcretumR article, we revisit the strategy and extend the analysis through 2025, adding nearly two decades of fully out-of-sample performance.

But the most interesting finding wasn't the return profile.

We found that a seemingly arbitrary implementation choice, the day of the month used for rebalancing, can create more than 2% per year of performance dispersion between otherwise identical portfolios.

We quantify this often-overlooked source of rebalance timing luck and propose a simple tranched rebalancing framework that substantially reduces its impact while also lowering turnover.

As a bonus, we also provide a complete Python implementation that automates the entire workflow, from signal generation to trade execution through Interactive Brokers.

Link to the full article in the first comment 👇

“Value investing with legends” is a great finance-specific podcast with a mix of celebrities and dedicated professionals. Here are some of my favorite episodes.

Kent Daniel: from physics to finance

https://t.co/gF4zywCWyd

Cliff Asness: quant investing, inefficiencies, being Cliff

https://t.co/SK0hGGKUHR

Nicolai Tangen: intuition, fundamental investing

https://t.co/YfTLwEAAxe

Michael Mauboussin: biases (and also learning from a master financial communicator)

https://t.co/ZKppJsGxok

it took us over 3 months to realize that we need to remove 90% of the features

previously known as ZeroPrompt

we applied the main engineering principle of subtraction and ended up with this beauty

1. paste text

2. generate link

3. send it anywhere

no more split texts in TG

no more random .txt files in Discord

no more “wait let me send this properly”

I built this to solve my own problem first

because I’m constantly sharing prompts, context files, specs, notes, ideas and random blocks of text

and I knew I wasn’t the only one

TextBar is free

and will remain that way

so if you like the idea, support the launch with a like/rt/comment/bookmark

we removed 90% of the product

so you can use 100% of it in less than a minute

Mean-variance portfolio optimization is taught in Finance courses in every business school. However, it is often criticized - and dismissed - due to it's sensitivity to the inputs, poor out-of-sample performance, and for producing overly concentrated/unstable portfolios.

Trend-Following Crisis Alpha: Does it come from beta timing or market selection? (Croce et al.)

"Beta timing constitutes 76% of the risk of a simple trend strategy.

"Vs. relative value component, beta timing has more neg. correlation to equities on avg & when stocks are down."

1/ How do you maximize compound returns?

A. Don't use too much risk.

B. Don't rely on bounce-backs.

C. Appropriate risk depends on expected Sharpe ratios.

D. Diversification increases Sharpes.

E. Hedge the (relevant) tails.

"Rule #1: Never lose money."

https://t.co/t6Dim26To0

Chris Hohn did a 90-minute sit-down with Nicolai Tangen and then dropped an investor letter the FT got hold of last week.

You’d think the guy who printed a record $18.9B last year would be doing victory laps. Instead he’s quietly rewiring his whole portfolio.

My favorite takes from both:

1.The most important thing in investing isn’t growth. It’s barriers to entry. Growth without a moat is the airline industry: 5% volume growth for 100 years and basically zero cumulative profit.

2.There are only about 200 companies on earth he considers high-quality and investable. His fund holds 15.

3.Average holding period: 8 years. Some positions 13. “You have to hold the company forever, because the stock market may be at very bad prices when you want to sell.”

4.His real test for a moat: can the company price above inflation? A 20% margin business that prices 1% above inflation grows profits 5% faster than revenue. Forever. Almost no companies can do this.

5. Industries he won’t touch: banks, autos, retail, insurance, tobacco, asset managers, fossil fuel utilities, airlines, wireless telecom, media, advertising. On banks: “sooner or later someone without a lot of intelligence comes to run them, and then it can be toxic.”

6.On AI generally: call centers go bankrupt. Indian outsourcing coders are next. But for everyone else, AI lowers costs and raises productivity. Companies with real moats become MORE valuable.

7. Here’s the punchline. The FT got hold of his investor letter. He cut his Microsoft stake from 10% of the fund to 1%. Roughly $8B sold. He’d held it since 2017 through a 400% rally. His reason: AI could disrupt Office and Azure faster than the market thinks.

8.He moved that capital into Alphabet. Doubled it from 3% to 5%. Now his largest tech position. The world’s best quality investor sold Microsoft and bought Google because he thinks Google’s moat is more durable in an AI world. Not the consensus trade.

9.The underlying thesis: “AI eats software.” If AI agents do the work humans used to pay per-seat SaaS licenses for, the whole SaaS model gets re-rated. Oracle, Adobe, Salesforce all ~40% off highs. Microsoft 25% off. Market is starting to agree.

10.When to sell? Not when something gets expensive. When conviction drops. Valuation is one variable, conviction is the other. What kills you isn’t being wrong, it’s permanent loss of capital.

11.He admits hardcore activism doesn’t work anymore. Too much of the shareholder base is passive index funds. And even when activism wins, you usually win in a bad business. “The business always wins.”

12.Counterintuitive take: there are more good companies in public markets than in private equity. The best businesses are too big for PE to buy. And when public companies sell something to PE, they’re selling the assets they want to get rid of.

13.On intuition: “thinking without thinking.” Pattern recognition from 20 years of reps. It’s how he sniffed out Wirecard while the German establishment was defending it. “Most investors trust authority too much.”

14.He basically stopped shorting. “You’re going to be eventually right but not be able to fund the losses.” The first guy to short Wirecard had to cover 19 years before it hit zero. Buffett told him he and Charlie studied shorting and concluded it was too hard.

15.He gives almost everything away. ~$500M a year. $10 prevents an unwanted pregnancy in Africa. $40 saves a child from severe malnutrition. $50 prevents permanent blindness.

16.Tangen asks: advice to young people? Hohn, who runs the world’s most profitable hedge fund: “Go on a spiritual path.” The guy who made $18.9B last year ends the interview saying only purpose and meaning matter.

The headline: the world’s best quality investor just sold his biggest tech compounder because he thinks AI is breaking the moat. Quietly, with conviction, on an 8-year horizon, while everyone else is still buying the AI winners of 2023.

Good morning my loves, happy Saturday. Sorry I've been quiet, obviously been busy, but thought it'd be nice to give you all the details on the multi-strategy absolute return program that experienced the 28% drawdown this year. (1/n)

Nicolai Tangen has interviewed all the most important CEOs and investors in the world (that's what $2T AUM buy you: lots of access). He has also interviewed a fair number of HF managers. Here are my favorites. Even so, it's almost 4 hrs. But I recommend actually listening, over the gemini summary.

Chris Hohn: https://t.co/5CdNm3fHI6

Paul Singer: https://t.co/DLq2U0atoa

Marc Rowan (not a HF, still interesting): https://t.co/k2BHwbPJFv

Stan Druckenmiller: https://t.co/H4sOAC1mU4

Ken Griffin: https://t.co/iepjcVwGOZ

f*ck discipline

work on your identity

don’t think “i should do X”

think “im someone who does X”

the difference is insane

become the best version of yourself

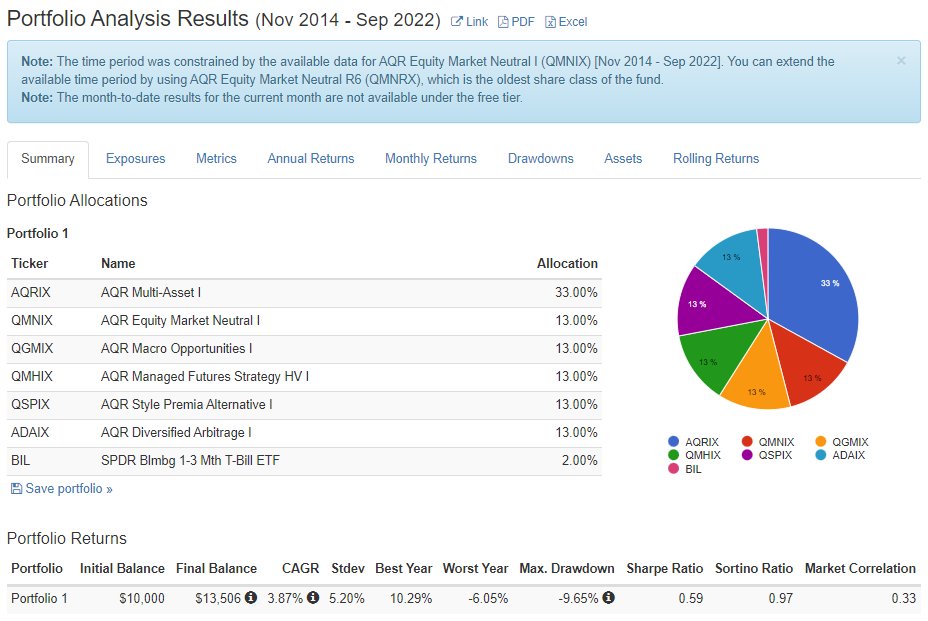

1/ AQR's AQR Diversifying Strategies Fund

(QDSIX: https://t.co/puDuOPkpMR)

is risk-balanced across asset classes and uncorrelated style strategies.

The fund itself is only two years old. Here's a link to a portfolio with the underlying funds in it:

https://t.co/9GohgNPp7k

I Wrote a New Book!!!

Optimization: A Bootcamp for Machine Learning, Inverse Problems, and Control

Pre-Order Now (July 31)

https://t.co/EoDMFapUUf

Coming Soon:

* Free PDF on website

* YouTube Videos for entire book

* Python code on GitHub

TLS is an elegant extension of OLS when both dependent and indep variables are noisy. TLS looks just like ridge regression (aka regularized OLS) except it's “de-regularized”

TLS solution is less numerically stable than OLS since both dependent & independent variables are noisy