Bill Ackman literally gave a 44-minute masterclass that explains money better than any business school.

1. Starting early is the single biggest advantage you have. If you save $10,000 at age 22, never add another penny, and earn 10% a year, you have $600,000 by retirement. wait until 32 to start, and the same money only grows to $232,000. The decade you lose at the beginning costs you more than any decade later because compounding does its heaviest lifting at the end.

2. The return rate matters even more than most people grasp. That same $10,000 at 22 earning 10% becomes $600,000. At 15% it becomes over 4 million. At 20%, the rate Warren Buffett has achieved, it becomes 25 million. Einstein called compound interest the most powerful force in the universe. Ackman's lecture is essentially a demonstration of why.

3. Avoiding losses matters as much as chasing returns. if you reach for a 20% return but lose half your money every 12 years from bad decisions or a rough patch, your 25 million collapses to 1.8 million. Buffett's rule one is never lose money. Rule two is never forget rule one. the math of recovery is brutal, so protecting the downside is not caution, it is strategy.

4. Debt is safer, but the upside is capped. Equity is riskier, but the upside is unlimited. In the lemonade stand example, the lender who put up $250 earns a steady 10% and gets paid back first if the business fails. the equity investor who put up $500 earns over 100% if it succeeds but gets wiped out if it fails. The equity holder earns more precisely because they took the risk the lender refused.

5. The risk that matters is permanent loss, not price movement. most people think risk is the stock price bouncing up and down every day. Ackman says ignore that. the real risk is whether you will permanently lose your money. Short-term volatility is noise. the question that matters is whether you get your capital back with a return over the long run.

6. Avoid startups and complicated businesses. You do not need 100% a year to build a fortune. you need 10 to 15% over a long period. so skip the lemonade stands and unknown ventures. Invest in public companies that are established, liquid, and have to clear real hurdles before going public. If you cannot understand how a business makes money, avoid it no matter how good its track record. Ackman cites Enron, a business almost nobody actually understood.

7. Invest in a business you could own forever. if the stock market closed for 10 years, you should not be unhappy holding it. Coca-Cola is his example. easy to understand, sells a syrup and earns a profit on every drink, the population keeps growing, and it is nearly impossible to disrupt with new technology. McDonald's is another. People have to eat, the food is cheap, and they keep growing. find a business you would be comfortable holding through anything.

8. You want products people are loyal to and will pay a premium for. People buy generic flour and sugar without caring about the brand. but they want the Hershey bar, the Cadbury bar, the see's candy specifically. you do not want to sell a commodity that anyone can sell cheaper. You want something unique that customers refuse to substitute even at a 20% discount.

9. Low debt is a safety feature. In the lemonade stand example, $250 of debt was manageable. But if it had been $1,000 and the business hit a rough patch, it could have gone under and wiped out the shareholders. Find companies with little debt or so much profit relative to their interest payments that a bad year cannot sink them.

10. Barriers to entry protect your returns. You want a business that is hard for someone to compete with tomorrow. Coca-Cola's market presence is so strong that you expect to get a Coke at any restaurant. Pepsi has coexisted with it for decades, but neither can put the other out of business. If a competitor can show up next year with a better version and steal the customers, the business is not worth owning long term.

11. The best businesses are immune to outside factors you cannot control. Coca-Cola has survived 120 years through world wars, nuclear weapons, and every kind of crisis, and each year it makes slightly more money. You want companies that do not depend on commodity prices, interest rates, or currency moves. A business that keeps earning regardless of what is happening in the world is the kind you hold forever.

12. Low capital intensity is one of the most underrated qualities. The worst businesses require massive reinvestment to grow. The auto industry has to build enormous factories and buy machine tools before selling a single car, and those tools wear out. GM's stock barely moved over 40 to 50 years for exactly this reason. Coca-Cola, by contrast, sells a formula and collects a royalty. American Express takes a few percent of every dollar spent on its card. a business that earns a royalty on other people's capital is one of the best things you can own.

13. Pay down debt and build a cushion before you invest. If you have high-interest credit card debt, paying it off is a guaranteed return equal to the interest rate. same logic, to a lesser degree, with student loans at 6 or 7%. and you want 6 to 12 months of expenses in the bank so that losing your job tomorrow does not force you to sell. You can only handle market volatility if you do not need the money.

14. Be a buyer when everyone is selling and a seller when everyone is buying. The natural human tendency is the opposite, a lemming-like instinct to sell in a crash and buy in a bubble. people sold into the 1987 crash when they should have been buying. The only way to resist this is to be financially secure enough that the money at risk does not affect your life, so you can withstand the swings without panicking.

15. The stock market is a voting machine in the short term and a weighing machine in the long term. Ben Graham's idea, which Ackman repeats. short-term prices reflect the whims and emotions of investors. long term, prices reflect the actual value of the underlying businesses. If you buy good businesses at reasonable prices and hold them while they grow, you make money over time as long as you are never forced to sell at the wrong moment.

16. A stock is just a bond where you do not know the coupon. Flip a price-to-earnings ratio over, and you get an earnings yield. A stock at 10 times earnings is a 10% earnings yield, which you can compare directly to a 3% treasury. the difference is the bond's coupon is fixed and the stock's coupon, its earnings, moves up and down. Ackman wants an earnings yield higher than a treasury that will also grow over time, so he does not need to be right about explosive growth to earn a good return.

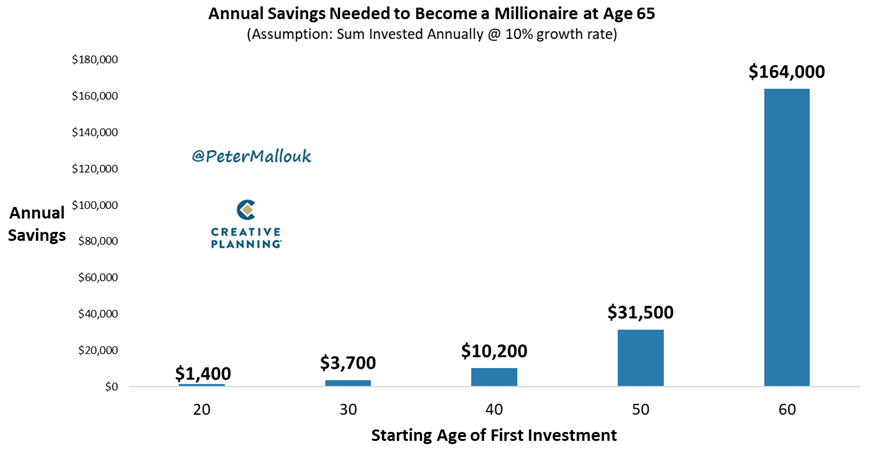

Annual savings to become a millionaire by 65 with a 10% return:

20 - $1,400

30 - $3,700

40 - $10,200

50 - $31,500

60- $163,800

Time in the market matters. Start as early as you can!

As always, Thank you for reading this.

If you enjoyed this post:

1. Follow me @hasantoxr for more of these

2. RT the tweet below to share this thread with your audience

Last day to submit! We invite submissions to the 2026 Stanford Financial Education Symposium, taking place April 23–24 at @StanfordGSB during Financial Literacy Month.

We welcome submissions from faculty, researchers, and advanced PhD students working on financial education, personal finance and financial decision-making.

To be considered, please email papers to: [email protected] by Jan. 31. Here is more info about the Symposium: https://t.co/q2WZFkGb30

Research has shown that the strongest predictor of happiness and success is social connection. Not wealth. Not status. Not education.

In this episode of 𝐈𝐜𝐨𝐧𝐬 𝐚𝐧𝐝 𝐈𝐝𝐞𝐚𝐬, happiness expert @shawnachor and I discuss how to create meaningful — and strengthen existing — connections in our life.

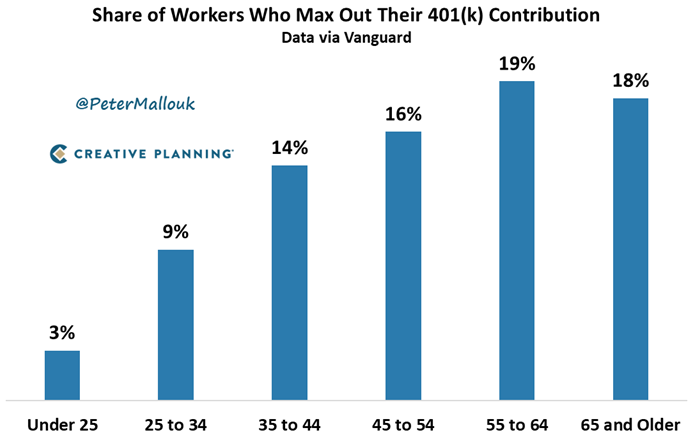

This chart says it all: the closer people get to retirement, the more serious they become about saving.

The real hack?

Don’t wait. Every dollar you put in during your 20s and 30s works harder than the dollars you scramble to save later.

Want $1 million by age 65?

Start at 20 → save $1,400/year

Start at 60 → save $164,000/year

Time and compounding are the greatest advantages investors have. Don’t waste them.

Harvard released the results of the longest ever study on longevity. The study spanned over 80 years.

And what is the #1 predictor of a long, good life?

It isn’t genetics. It isn’t diet. It isn’t exercise. It isn’t wealth.

It is the quality of your relationships.

Be sure to invest in the most important things you can: the relationships with your family and great friends.

I am very happy that our Council on Financial Education was chosen to deliver a Spotlight Session to the other Councils attending the @wef in Dubai.

The Session was titled: "Money Talks: Are We Listening?"

Financial literacy is a macroeconomic priority critical to both individual and systemic resilience, particularly in times of instability. We explored how to rethink financial education to meet the demands of a changing, financially volatile and connected world.

Here is a brief summary of the main points we covered in the Spotlight Session.

(i) Individuals make thousands of decisions a day, many with financial consequences. Financial literacy, which is the knowledge of fundamental concepts at the basis of financial decision making, can help individuals to make sure those decisions are well-informed.

(ii) Financial education not only improves individual outcomes, it also reinforces macroeconomic resilience. When individuals are equipped to save, invest, and plan ahead, their money flows into businesses and financial markets, supporting growth and stability.

(iii) When individuals understand how to manage money, they not only improve their own financial well-being. They make monetary policy more effective, as discussed by @Isabel_Schnabel in her 2025 Mais Lecture at Bayes Business School.

(iv) Financial education its not a ‘nice-to-have’, it is necessary for economic stability.

We will write more extensively about it, so stay tuned.

Join us! The 4th Teaching Personal Finance Conference 2025 will be live-streamed.

This half-day conference brings together educators, experts and innovators from across the country to share experiences, ideas, and best practices in teaching personal finance.

Thursday, September 25 | 9:30 AM – 12:30 PM PT

Join live on YouTube:

https://t.co/B1WMYurhfK

Our program includes:

• President Laura Rosenbury (Barnard College) on the Francine LeFrak Foundation Center for Well-being at Barnard College: Fostering Resilience and Promoting Lifelong Success

• Ronjon Nag (@Stanford ) on AI and personal finance education

• Irene Foster (@GWtweets ) and filmmaker Chris Temple on storytelling

• @sharon_epperson , @CNBC Senior Personal Finance Correspondent

Check out our program here: https://t.co/AbMnRK6MVa

Please share with anyone interested in this event.

For any questions, please contact the Stanford Initiative for Financial Decision-Making (IFDM) at [email protected]

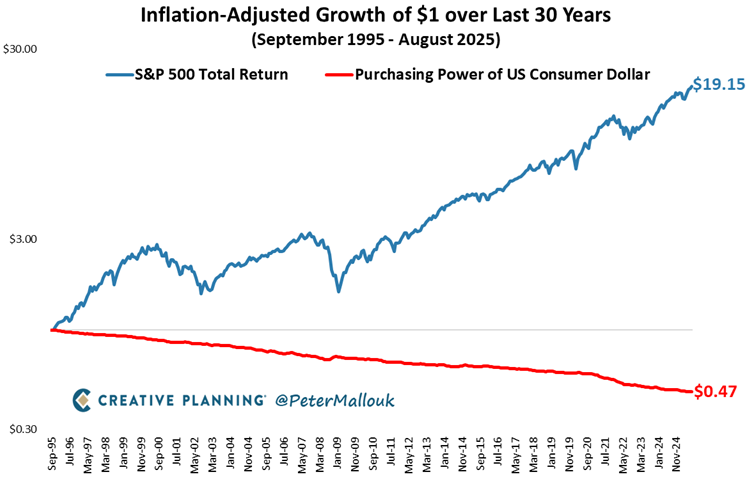

Inflation is the silent thief.

Over the last 30 years, it cut the value of $1 in half.

But $1 invested in the S&P 500 became $19 – after adjusting for higher prices.

That’s the power of ownership.

I'm grateful to the Stanford Report for today’s story. In the article written by @Sam Scott, I shared why teaching financial literacy is key and how, through our Initiatives for Financial Decision-Making, we aim to democratize access to financial education

https://t.co/XHf8h5mADf