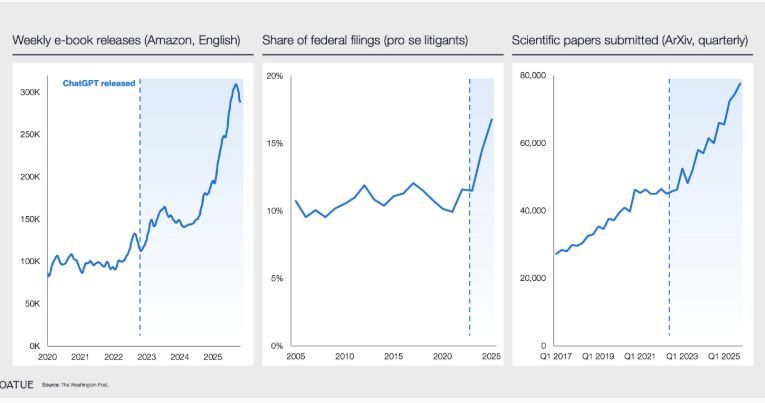

Activity is not productivity.

Many signs of a surge in knowledge work output post chat GPT, but no signs of any meaningful increase in the real sales per worker at the economy wide level.

I don’t really have many VC horror stories.

The worst ones are just meetings where there isn’t much interest. Everyone is still polite, but you can feel it’s not going anywhere. With my first company, I pitched a lot of VCs and got a lot of polite rejections.

With Linear, I approached fundraising differently. I tried to always be in a position where I didn’t need funding.

I also didn’t do pitch meetings unless there was real mutual interest. I would take casual meetings, but tried to avoid pitch meetings, until I thought the timing was right, I was in the process, and I was interested and I could see the VC interested too.

Early on, we raised a small amount from angels. We didn’t want to commit to a VC at the very beginning, and with three co-founders we knew we could build the first version without much money.

After we announced the company, investor interest started to pick up. I told most VCs no and said I was focused on building the product.

Then Sequoia reached out. I took a coffee meeting with one of the partners because, well, it was Sequoia.

The partner later pushed me to come in and “meet more people.” I assumed this might turn into more of a pitch meeting, so I came prepared with slides and some thinking. I was willing to do it, again because it was Sequoia.

Before committing to the meeting, I told them clearly that I wasn’t raising and didn’t want to waste their time. They still wanted me to come in.

After the pitch, someone asked how much we were raising, since it wasn’t in the deck.

I said what I had already told them: I’m not raising.

They asked, “Well, if you were raising, what would you raise?”

I said I hadn’t really thought about it, and we wrapped the meeting.

They didn’t invest in that moment, but a few weeks later, once we actually decided to raise, they fought against other term sheets and led our seed round.

About a year later, Linear became breakeven/profitable. Every round since has been more focused. I’ve mostly met casually with VCs, usually engaging with 3–5 firms per round, and only doing a pitch if I thought they were good and they really wanted it. I’ve still gotten plenty of passes too.

Each round has taken about 2-3 weeks, because I've built the relationships, then just completed the show, and closed within couple of weeks.

With every round, I’ve also given VCs some homework. I send them a memo and questions about the business, ask them to write answers, and then we discuss them live.

For our Series B, several people from Accel flew to where I live, booked a hotel space, and came with binders of research about our company. It wasn’t a formal pitch meeting. It was a discussion.

I share this because for every VC horror story, there are also stories where investors really go the extra mile.

There are many cases where the VC builds the case, defends and believes in the founder, and does everything they can to make the investment happen, even when the rest of the partnership isn’t fully there yet.

I’ve only raised in 2012 and from 2019 onward, so I do believe there were times when VCs had more power and could abuse it more. YC, in some ways, helped put a stop to that.

But my guess is that VCs more often do something extraordinary than treat someone badly. You just don’t hear about those extraordinary experiences as much.

I’ve seen VCs fly anywhere in the world on a moment’s notice to try to convince a founder. I’ve been called many times to help sell a founder on a firm. VCs will do everything, call in every favor, to impress the founder.

And I don’t envy the job. It seems grueling. You have to pass on a lot of people who are obviously passionate about their business, and people take it personally. At the same time, you have to work incredibly hard to get into the best deals.

I think the challenge is that everyone can now build apps

But

1) almost nobody has distribution (like an audience), or

2) the money to pay for distribution (ads or UGC), or

3) the creative genius to get distribution for free (classically called guerilla marketing)

In 2000, Lee Kuan Yew gave a 2-hour masterclass on leadership worth more than an MBA.

He built Singapore into a First World nation in one generation

His frameworks:

- Why IQ alone destroys leaders

- Trustees, not owners

- How trust is built in crisis

12 lessons on how to lead:

@artemis@jonbma i'm surprised to see that SG, HK, and Japan show up as major senders. for instance, SG already moves USD and SGD in bulk efficiently through banks, which limits the stablecoin advantage.

so I wonder what use cases are driving those flows

@artemis@jonbma 3/ B2B payments - for global trade flows, Asian countries are typically exporters, so they’d be receivers. If trade is intra-Asia, then it makes sense that SG / Japan / HK show up more as senders

4/ treasury management - flows here are more bidirectional

We just published the most accurate onchain estimate of stablecoin payments ever.

Everyone keeps quoting $10T–$30T “stablecoin payments.”

That number is wrong. By a lot.

Built with @McKinsey payments team, we used a bottom-up approach to isolate real payments.

This report previews our new stablecoin payments dashboard, launching soon.

The real number will surprise you 👇🧵

To Whitelabel Or Not To Whitelabel?

I have repeatedly been asked this question over the last year by enterprises, potential candidates, podcasters, and more. @ramahluwalia recently made a point on @laurashin's Unchained pod that resonated with me. He said, “We need to solve real problems, customer problems. Make money movement easier, lower the cost of interchange, make borrow + lending easier, reduce counterparty risk, lower the cost of financing, do onchain tokenization of RWAs, cut settlement time. Those solve real problems.” YES. Music to my ears.

Ram, however, followed up by saying “The world doesn’t need 97 new stablecoins. [Agora] has a decentralized whitelabel platform” implying we’re contributing to the creation of unnecessary stablecoins (and to clarify it is not decentralized). His critique of those espousing 1000s of stablecoins and those who do so because it is “on theme” is warranted. Between answering this question dozens of times a week and Ram’s comments, I felt like it was about time to concisely address the question “to whitelabel or not to whitelabel”.

We believe there will likely be 5-10 very large, global “open loop” payment stablecoins. In addition to these large multi-utility players, there will be thousands of whitelabel stablecoins that serve specific purposes in primarily closed loop environments.

What defines a global “open loop” stablecoin?

- Credible Neutrality: Not competing with your customers and acceptance venues. (Note: USDC is the exception to the rule here as it does not maintain neutrality as Coinbase/Circle compete very directly with many of their customers through Base/Arc, prediction markets, custody, trading cenues, etc.)

- Global Liquidity: deep liquidity across a variety of markets including lending, spot, perpetuals, futures, and differing asset classes.

- Global Utility: broad acceptance across a variety of venues.

- Examples: AUSD, USDC, USDT

The reason there will only be 5-10 global “open loop” stablecoins is because network effects drive a positive feedback loop.

- Users want to use assets that are accepted or enable them to do things they could not do previously.

- Applications/businesses want to accept what users hold and what benefits them.

- Liquidity improves execution, pricing, and reliability, widening the gap with stablecoins with thin liquidity.

The world does not need 97 other stablecoins…trying to be the same thing. Power laws and network effects ensure that global stablecoin liquidity converges. Stablecoins are no exception — the market will support only a small number of deeply liquid, trusted monetary units. The vast majority of businesses should just tap into the existing distribution of large “open loop” stablecoins.

The Rise of Whitelabeling

Whitelabeling was popularized over the last year as enterprises bargained to further monetize their platforms. The desire for distributors to monetize their distribution is obvious and one of the reasons we started Agora in the first place. Many companies think they need to whitelabel to control economics, but that is not true. Whitelabeling had been on our roadmap since the start of the business, so we decided to move it up in the priority queue and add “whitelabel stablecoins” as an additional product.

Paxos has “whitelabeled” for the Enterprise for years (remember BUSD), but true to our nature, we wanted to launch a product only if we could improve upon it and make it scalable. We announced whitelabeling as a product over the summer and are thrilled to see @coinbase mimic exactly how we do it in their announcement two weeks ago. Clearly we did something right, +1 for @drakeevans ingenuity.

Custom Stablecoins for Customized Use Cases

For the last two years, people have been calling everything that targets a $1 peg a stablecoin presupposing they are competitive with one another. The term “stablecoin” is most clearly affiliated with the globally liquid “open loop” stablecoins backed by high-quality liquid assets (eg. Short-Dated U.S. Government Debt). I do not believe the world needs or will support 97 other “open loop” stablecoins like AUSD, USDC, or USDT, but it will support a range of assets trying to do specifically different things.

So where do custom stablecoins make sense?

- Closed Loop Systems (eg. Loyalty Points, In-Game Tokens)

- Applications where there is a strong consumer brand or trust element present (eg. Robinhood, Paypal).

- It is a product requirement. For example, many yieldcoins have a non-yielding component to their staked/yielding version.

- When leaning into regulatory or operational control is necessary.

From what we have seen, most custom stablecoins are trying to achieve a very specific objective and none, are trying to become a global “open loop” stablecoin. Many that have launched over the last year are really Hedge Funds/Debt Products offering differing sources of yield to token holders.

Custom stablecoins are in many ways accounting and brand tools for specific use cases. Some of them will be entirely abstracted away from the user in the first place, probably by the “Super Apps” Ram mentioned. Side bar – We believe that most users of AUSD, USDC, and USDT in 10 years will likely not even know they are using those assets under the hood.

We’re excited to work with many partners requiring custom stablecoins as AUSD is a great complement because you can:

1) pair liquidity against it

2) use it as the deposit/withdraw asset for minting/redemption of the new stablecoin

3) share in the revenue

4) leverage its broader liquidity and infrastructure (eg. LayerZero/Stargate, CEXs, On/Off Ramps, etc.)

5) find a true PARTNER that has experience working with the best teams to build liquidity and launch net new products

For Agora, there is a tremendous symbiotic relationship with companies looking to issue custom stablecoins for the above reasons. We’re excited to continue working with exceptional startups as well as huge brands (more to come in Q1). I’ll sign off with this teaser: we will power whitelabeled issuance for the clients at one of the hottest names in banking in the new year.

The bank lobby is furious about stablecoin yield under the GENIUS Act. They're calling it a "loophole" that needs closing.

But here's what they're missing: We've seen this movie before. And it built an entire generation of fintech companies.

🧵

Imagine sitting at a poker table where your opponent gets a free last look at your cards before deciding to call or fold. That is how many on-chain exchanges operate today.

@paradex reimagines onchain markets from First Principles to make perps trading fair.

In the current decentralized perps markets, high-speed market makers enjoy a “free last look” at your trades, canceling their orders last-second if the trade would be unprofitable for them. It’s as if the house never loses, and you’re not the house.

This structural imbalance is invisible to most users (the UI feels fast, after all), but it shows up in subtle ways: ever notice how you’re instantly down a percent or two after a perp trade on some DEXs? That’s your opponent peeking at your hand.

Paradex’s core thesis is that they can build a better game, one where trading is fair by design, not by how fast you are. After all, isn’t the point of crypto to level the playfield to give the little guy a shot?

There are two philosophies to the Perp Dex landscape:

Camp A: copy TradFi microstructure on-chain (cancel priority).

Think Hyperliquid and friends. Ultra-low latency, price-time priority, special casing cancels so makers feel safe and show tight screens. It’s snappy, but it’s still a latency arms race where makers keep a “free last look” and regular users eat the slippage.

Camp B: redesign for crypto’s strengths (Paradex).

Instead of assuming the traditional model is optimal, Paradex is redesigning the playing field itself by embracing crypto’s unique strengths: on-chain validity proofs for trustless execution, protocol-level privacy, and new order types like RPI and supplementary execution protocols like RFQ to execute large and complex trades with atomic leg execution. This first principles approach changes the game to make it fairer for a broader range of participants. This camp acknowledges that blockchains are not NASDAQ and shouldn’t try to be; they have different constraints and superpowers.

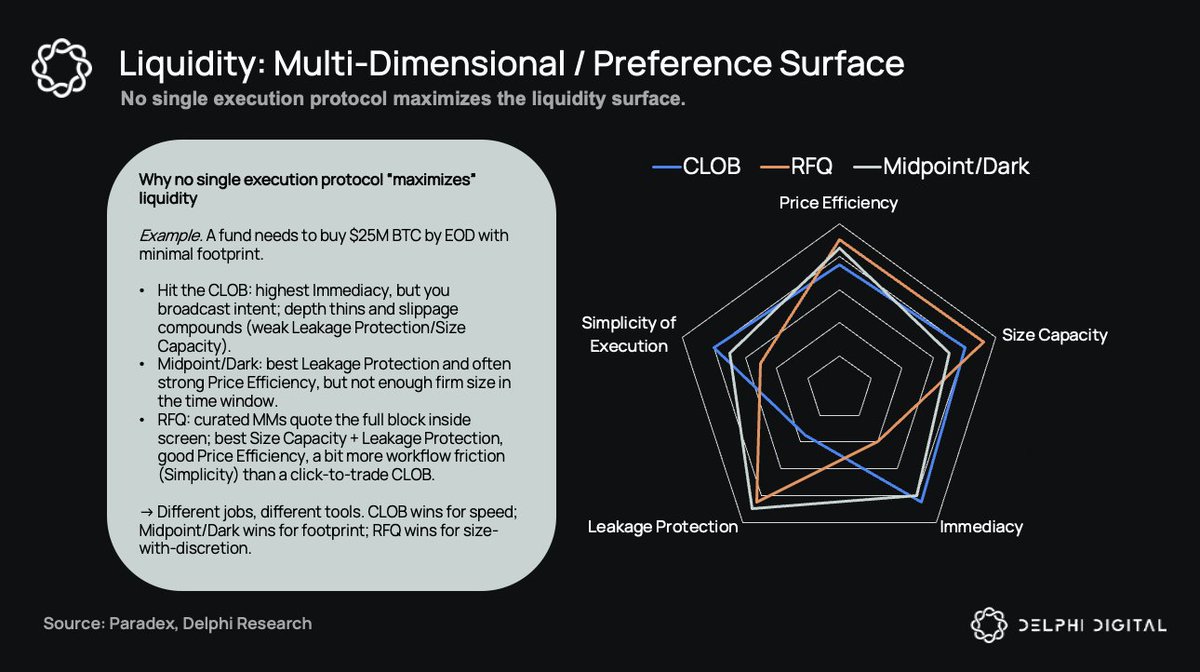

Liquidity is a system, not a number

Paradex treats liquidity like a surface, an n-dimensional trade-off across price, size, immediacy, info-leakage, and execution complexity. Different protocols sit on different parts of that frontier: CLOB, RFQ, dark. You can slide along it, but you can’t max every axis at once. Paradex leans into that reality instead of fighting it.

Two key lanes make the “speed game” matter less:

1) RPI (Retail Price Improvement): a UI-only top-of-book that’s invisible to APIs. Makers flag quotes as RPI and post tighter spreads because they won’t get run over by toxic/latency arb. UI traders naturally hit better prices with zero taker fees. Makers get clean flow; takers get better fills.

2) RFQ: for size and complexity. Route larger or multi-leg orders without broadcasting your hand to the entire market, preserving privacy and price.

Result: fewer flickering quotes, tighter effective spreads, and execution that’s optimized for who you are and what you’re trying to do, not how fast your bot is.

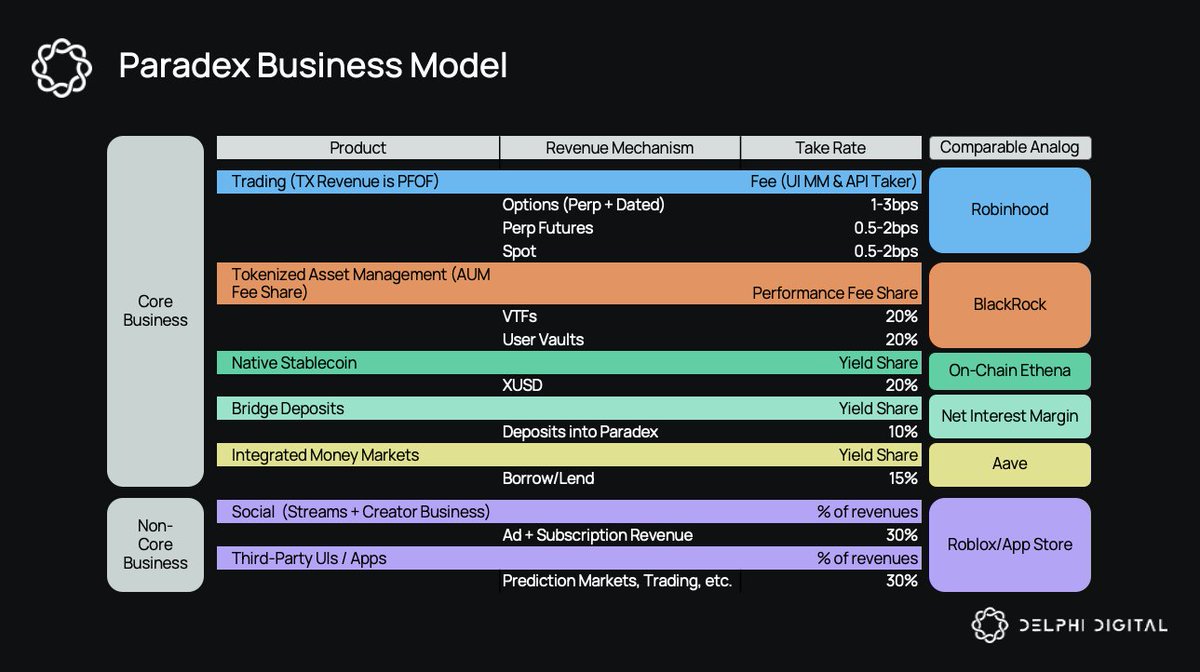

The business model everyone hand-waves past

Flow segmentation (via RPI) unlocks PFOF on-chain. That’s the engine behind “zero-fee” trading: market makers pay for access to high-quality retail flow, the platform forgoes taker fees, and users trade cheaper while spreads stay competitive. Think “Binance-level spreads, zero taker fees,” funded by the parties who profit from filling the orders.

This isn’t new in finance, just look at Robinhood, what’s new is making it work on-chain without poisoning the well for serious traders. Segment the flow, protect makers from toxic hits, and you can sustain zero taker fees without turning the venue into a carnival.

Why this matters

Institutions don’t just need fast, they need trustworthy. Deterministic finality, privacy for size, and protection from toxic flow are table stakes if you want real balance sheets trading on-chain. Paradex’s first-principles approach is a different road to the same destination: pros get reliable execution; everyone else gets a fairer game.

PFOF is a compelling business model

Paradex could end up with 5+ distinct revenue streams, all feeding the token.

Paradex represents a high-conviction bet on a fundamentally different approach to building an exchange. Ultimately, my thesis is that we see a zero-to-one improvement in on-chain exchange design. If we analogize to the evolution of exchanges: first-gen DeFi (Uniswap, etc.) was an innovation (AMMs vs order books), second-gen (dYdX, GMX, etc.) tried to bring more pro features but still lacked certain elements, and now Paradex is the third-gen that combines the best of CeFi and DeFi.

Why do some founders raise easily while others struggle, even with great ideas?

Antler has shared a cheat sheet to help founders assess their ability to raise capital in their initial funding round -

It explains why two founders with equally good ideas can have wildly different outcomes when raising capital.

Here’s the blunt truth: Fundraising isn’t just about the idea.

It’s about how fundable you look to investors.

1. Founder pedigree

If you don’t have traction, investors look at your past. Where did you work? What did you build? They're trying to de-risk the bet by betting on you.

Harsh, but true: "Some incredible founders get ignored just because they don’t fit the typical pattern."

And when investors are sifting through hundreds of decks, pattern-matching is a shortcut.

2. Traction

Traction beats pedigree. If you’ve already built something that’s working, even a “non-pedigree” founder can raise. It’s not about being famous.

It’s about showing real progress, proof that the market wants what you’re building.

Some factors can change the game.

→ Strong co-founder

→ Domain expertise

→ A unique insight or unfair advantage

These push you to the “right” on the fundraising matrix.

But others can hurt:

→ A product that’s hard to explain

→ No experience in the space

→ Poor storytelling or confusing deck

These push you to the “left.”

There are two must-haves without which you won't be able to raise, regardless of pedigree or traction:

→ Fundraising-ability: You need reasonable fundraising skills. Networking, sales skills, storytelling, and running a tight process are crucial.

→ Market attractiveness: Your market must be significant and attractive. At early stages, it's binary - either investors get excited about the opportunity, or they don't.

Remember

→ Valuations are a function of capital raised. Assume 15-25% dilution irrespective of the amount raised. For example, if a team raises 800k, the valuation will likely be between 3.2m - 5.3m.

→ LinkedIn profile beats pitch deck in very early stages. Many investors will check your LinkedIn before deciding on a first meeting or looking at your pitch deck.

When is this wrong?

→ Numbers are purely directional. They've been validated with experienced investors, but they're not exact.

→ This model is primarily for software startups. Biotech & Hardware companies play by different rules.

→ Copycat models are very binary. Experienced teams can attract large funding, while others struggle to raise anything.

→ Raising from a rich uncle or family/friends who aren't experienced venture investors follows different rules.

Remember, great founders come from all backgrounds.

If you don't fit the "classic" profile, you might need to prove more in the beginning, but there are countless examples of founders without traditional backgrounds building awesome companies.

@dunkhippo33 I’m afraid it’s not an isolated case… Have been recently hearing about other VCs coming across fraud cases in their portfolios. That’s why we use https://t.co/z74yTwpAQI !

![Nick_van_Eck's tweet photo. To Whitelabel Or Not To Whitelabel?

I have repeatedly been asked this question over the last year by enterprises, potential candidates, podcasters, and more. @ramahluwalia recently made a point on @laurashin's Unchained pod that resonated with me. He said, “We need to solve real problems, customer problems. Make money movement easier, lower the cost of interchange, make borrow + lending easier, reduce counterparty risk, lower the cost of financing, do onchain tokenization of RWAs, cut settlement time. Those solve real problems.” YES. Music to my ears.

Ram, however, followed up by saying “The world doesn’t need 97 new stablecoins. [Agora] has a decentralized whitelabel platform” implying we’re contributing to the creation of unnecessary stablecoins (and to clarify it is not decentralized). His critique of those espousing 1000s of stablecoins and those who do so because it is “on theme” is warranted. Between answering this question dozens of times a week and Ram’s comments, I felt like it was about time to concisely address the question “to whitelabel or not to whitelabel”.

We believe there will likely be 5-10 very large, global “open loop” payment stablecoins. In addition to these large multi-utility players, there will be thousands of whitelabel stablecoins that serve specific purposes in primarily closed loop environments.

What defines a global “open loop” stablecoin?

- Credible Neutrality: Not competing with your customers and acceptance venues. (Note: USDC is the exception to the rule here as it does not maintain neutrality as Coinbase/Circle compete very directly with many of their customers through Base/Arc, prediction markets, custody, trading cenues, etc.)

- Global Liquidity: deep liquidity across a variety of markets including lending, spot, perpetuals, futures, and differing asset classes.

- Global Utility: broad acceptance across a variety of venues.

- Examples: AUSD, USDC, USDT

The reason there will only be 5-10 global “open loop” stablecoins is because network effects drive a positive feedback loop.

- Users want to use assets that are accepted or enable them to do things they could not do previously.

- Applications/businesses want to accept what users hold and what benefits them.

- Liquidity improves execution, pricing, and reliability, widening the gap with stablecoins with thin liquidity.

The world does not need 97 other stablecoins…trying to be the same thing. Power laws and network effects ensure that global stablecoin liquidity converges. Stablecoins are no exception — the market will support only a small number of deeply liquid, trusted monetary units. The vast majority of businesses should just tap into the existing distribution of large “open loop” stablecoins.

The Rise of Whitelabeling

Whitelabeling was popularized over the last year as enterprises bargained to further monetize their platforms. The desire for distributors to monetize their distribution is obvious and one of the reasons we started Agora in the first place. Many companies think they need to whitelabel to control economics, but that is not true. Whitelabeling had been on our roadmap since the start of the business, so we decided to move it up in the priority queue and add “whitelabel stablecoins” as an additional product.

Paxos has “whitelabeled” for the Enterprise for years (remember BUSD), but true to our nature, we wanted to launch a product only if we could improve upon it and make it scalable. We announced whitelabeling as a product over the summer and are thrilled to see @coinbase mimic exactly how we do it in their announcement two weeks ago. Clearly we did something right, +1 for @drakeevans ingenuity.

Custom Stablecoins for Customized Use Cases

For the last two years, people have been calling everything that targets a $1 peg a stablecoin presupposing they are competitive with one another. The term “stablecoin” is most clearly affiliated with the globally liquid “open loop” stablecoins backed by high-quality liquid assets (eg. Short-Dated U.S. Government Debt). I do not believe the world needs or will support 97 other “open loop” stablecoins like AUSD, USDC, or USDT, but it will support a range of assets trying to do specifically different things.

So where do custom stablecoins make sense?

- Closed Loop Systems (eg. Loyalty Points, In-Game Tokens)

- Applications where there is a strong consumer brand or trust element present (eg. Robinhood, Paypal).

- It is a product requirement. For example, many yieldcoins have a non-yielding component to their staked/yielding version.

- When leaning into regulatory or operational control is necessary.

From what we have seen, most custom stablecoins are trying to achieve a very specific objective and none, are trying to become a global “open loop” stablecoin. Many that have launched over the last year are really Hedge Funds/Debt Products offering differing sources of yield to token holders.

Custom stablecoins are in many ways accounting and brand tools for specific use cases. Some of them will be entirely abstracted away from the user in the first place, probably by the “Super Apps” Ram mentioned. Side bar – We believe that most users of AUSD, USDC, and USDT in 10 years will likely not even know they are using those assets under the hood.

We’re excited to work with many partners requiring custom stablecoins as AUSD is a great complement because you can:

1) pair liquidity against it

2) use it as the deposit/withdraw asset for minting/redemption of the new stablecoin

3) share in the revenue

4) leverage its broader liquidity and infrastructure (eg. LayerZero/Stargate, CEXs, On/Off Ramps, etc.)

5) find a true PARTNER that has experience working with the best teams to build liquidity and launch net new products

For Agora, there is a tremendous symbiotic relationship with companies looking to issue custom stablecoins for the above reasons. We’re excited to continue working with exceptional startups as well as huge brands (more to come in Q1). I’ll sign off with this teaser: we will power whitelabeled issuance for the clients at one of the hottest names in banking in the new year.](https://pbs.twimg.com/media/G9WCyjgXwAAVBbU.jpg)