@bgurley we have been doing some analysis on this...I don't agree that SBC is the root cause based on the data.

==

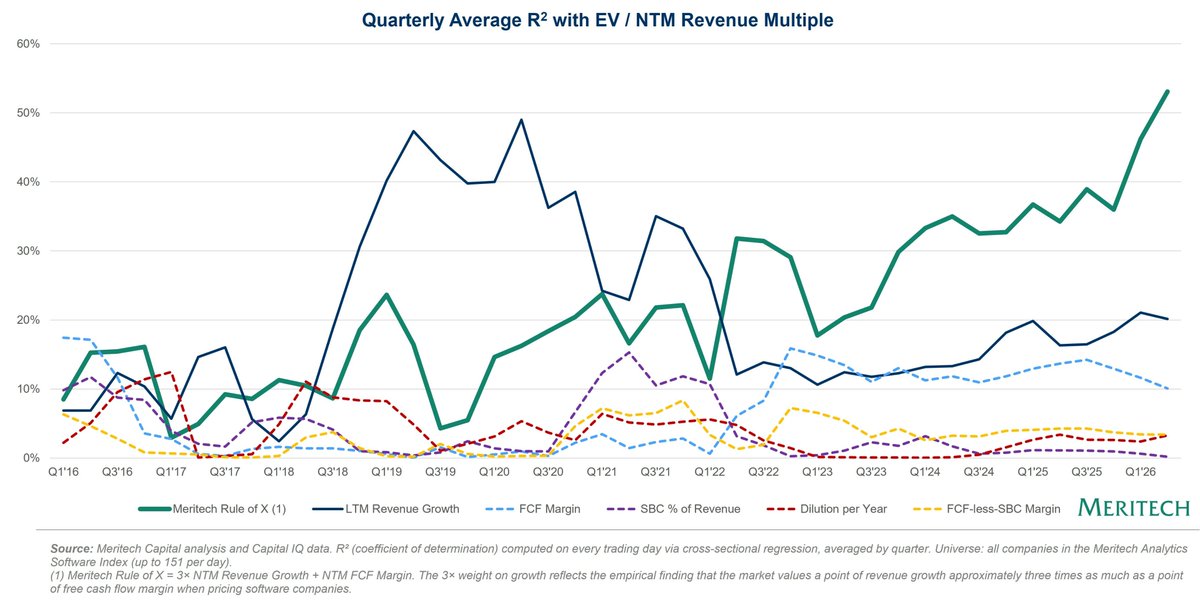

SBC (stock-based compensation) is not the root cause of the selloff in software — it's slowing revenue growth as AI threatens the core value proposition of sticky, recurring revenue and ever-growing absolute free cash flow.

SBC is a derivative of this (to be clear, it should be treated as a cash expense). We looked at 1.5M data points from 10 years of trading data across 141 companies, and there is no discernible correlation between either dilution per year or SBC as a % of revenue and valuation multiples.

The Street cares about revenue growth. Each time there is a correction and/or growth slows, as it did in 2022, the SBC comments emerge. That is not to say that dilution is not important, because it is, but high and durable revenue growth matters much more.

For example, over the past 10 years, 88% of the time, there is a stronger correlation between revenue growth and valuation multiples than between any SBC, dilution, or free cash flow metric.

Moreover, 100% of the time (by quarter) over the past 10 years, reported free cash flow had a higher correlation to valuation than free cash flow less SBC.

The market has never, in any single quarter over the past decade, placed more value on SBC-adjusted free cash flow than on reported free cash flow….

A few other notes: we looked at every company that has been continuously in the public software index over the past 10 years (33 companies with full 10-year track records). Dilution explains 12% of return variance; SBC as a % of revenue has essentially zero correlation with returns (r-squared of ~0). Revenue CAGR is the single strongest predictor, explaining 41% of 10-year return variance (r-squared=0.41).

The top quartile by share price return over the past ten years (SHOP, AXON, TTD, PANW, NOW, APPF, HUBS, TWLO) diluted a median 47% and returned a median 635%. The bottom quartile of share price returns (RPD, BLKB, OTEX, PRGS, FIVN, BL, SGE, SPSC), which included 4 net share buyers, returned a median of (7)% and had a median cumulative dilution of 4% (basically nothing!).

The pattern is clear: the best-performing software companies used equity aggressively to attract top talent and fund growth, while the most capital-conservative companies delivered the weakest returns. Even during the 2022–2023 rate-hike correction — the most hostile environment for growth stocks in a decade — growth metrics only lost to FCF and SBC metrics in 3 consecutive quarters before reasserting dominance.

Many public software companies are in a "burn the ships" moment, figuring out how to grow revenue faster, which requires getting into the token flow. It's almost akin to being an offline business in 1997 and needing to go online. Public technology markets care about high, durable revenue growth, and I don't believe that, looking back in 10 years, the companies that didn't make it will be the ones that just limited SBC. It will be the ones that failed to innovate / hire the best people, and failed to achieve high, durable revenue growth.

This is clear when looking at this chart over time...the market cares about Rule of X (which is mostly growth).

@Chime filed their S-1/A yesterday and is slated to go public imminently. This is the most anticipated fintech IPO since the 2021 ZIRP era. See @MeritechCapital full S-1 Breakdown.

https://t.co/eOB1jXIPFC via @LinkedIn

Vertical software company @ServiceTitan ($TTAN) filed for an IPO, the 3rd SaaS company of the year. They’re almost $800M in ARR growing 25% year-over-year and should be trading in the next few weeks. $TTAN’s performance should be a barometer for the dozens of other SaaS IPOs thinking about the public markets. More in our post in the link below. Thanks @amdecamillo, @ausw2000 and @danKnightNews1

SUBSCALE IPOs

The Meritech team @MeritechCapital continues to put out some excellent analysis. This one is on IPO scale.

TLDR is that companies with less than $700m annualized revenue underperform after going public. Actually, not just underperform - they have NEGATIVE absolute returns. This makes it hard to retain employees, sustain analyst interest or build a book of permanent buy-and-hold shareholders.

A few months ago, I had posited that one needs $500m in revenue to go public. If a startup goes public with $250m in revenues, unless they are growing really fast (>50% YoY if not faster), they should expect the next few years to be a daily struggle. Sadly, an acquisition by a larger company or by PE might be an inevitability, as we’re seeing almost daily today.

Rubrik ($RBRK) is the first SaaS company to file for an IPO in 2024. $RBRK is an almost $800M ARR business growing almost 50% year-over-year, the fastest LTM ARR growth rate among all current public SaaS companies. A lot more here:

https://t.co/AI7vcj2iZm

We are delighted to open nominations for the 6th annual #ForbesAI50 alongside @Forbes and @sequoia, showcasing the world’s leading AI companies. Don’t miss this chance to show your AI company is best in class. Submissions are open now through February 5th:

https://t.co/sUbPkhuoHD

We talked last week on @theallinpod about looking at long term multiples in SaaS and our friends at @MeritechCapital sent us this chart that they keep looking all the way back to the Salesforce IPO in 2004.

Bottom line is that 6x NTM revenue is the 20 year trend.

If you run a SaaS company and your last round was meaningfully above this metric, a solid piece of advice is to manage your burn until your NTM revenue x 6 == your last valuation.

Meritech is excited to partner with @koenbok, @jornvandijk, and the entire Framer team on their mission of creating a new standard of web design. If you're building a site, check it out!!!

https://t.co/KtoiCGRAny

The highly anticipated @Instacart IPO is around the corner! See @MeritechCapital's S-1 Breakdown of the company that aims to break open the consumer technology IPO window.

https://t.co/4p1kZVYxj4

A wonderful step toward building the next-generation of financial products for all. Come join us at @Wealthsimple to help the world achieve financial freedom!

https://t.co/UDSToDm40w

Do you even @TegusHQ? The product is incredible. @TegusHQ has become one of the most critical research tools we use @MeritechCapital.

Beyond expert calls, @TegusHQ database of public and private companies enable us get an in-depth perspective on markets and companies quickly.

@root_insurance is the next fintech / insurtech to try its hand hand in the public markets. Check out @MeritechCapital's S-1 breakdown of the company here.

https://t.co/37YPO2QmPu

@HarryStebbings speaking with @NewfrontHQ CEO, Spike Lipkin, on leadership and building the next generation of technology companies. Check it out on @twentyminutevc and if interested in helping to modernize the insurance market please reach out directly!

https://t.co/j6Qs0B6BZv