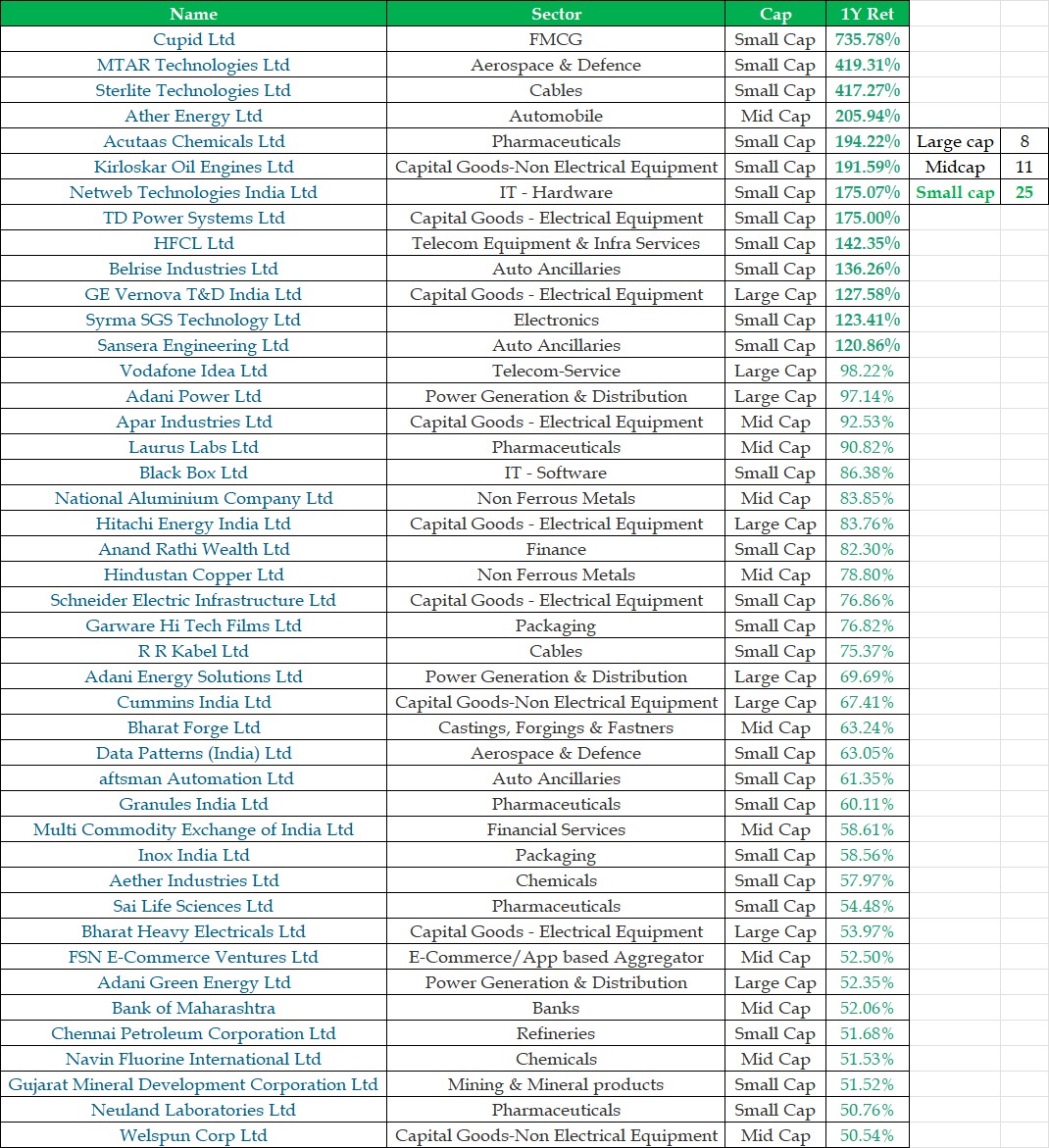

🚨 Did You Know?

Out of the Top 500 stocks, 44 stocks generated returns of more than 50% in just the last one year.

Here's the break-up:

🟢 Small Cap: 25 stocks

🔵 Mid Cap: 11 stocks

⚫ Large Cap: 8 stocks

The takeaway?

Extraordinary returns aren't confined to one market-cap segment. Opportunities exist across the market—but identifying them requires research, discipline, and patience. Fortune Investment Services (P) Ltd.

ARN: 197457

📌 This post is purely for educational purposes and is not investment advice. Please do your own due diligence before making any investment decisions.

The Sudarshan Chakra is India's planned multi-layered air and missile defence shield, announced by Prime Minister Narendra Modi in his 2025 Independence Day address.

Named after Lord Krishna's divine discus, it aims to build a nationwide protective umbrella against aerial threats including drones, cruise missiles, ballistic missiles, and aircraft.

The government has set a target of making the system operational by 2035, drawing inspiration partly from Israel's Iron Dome but on a far larger scale suited to India's size and diverse threats along its borders with Pakistan and China.

The concept envisions an integrated network of sensors, command centres, and interceptors working together to detect, track, and neutralise incoming threats at multiple ranges and altitudes. It is meant to protect critical infrastructure, military installations, cities, and economic assets.

Defence equipment likely to be needed includes:

Long range surface to air missile systems such as the S-400 Triumf and the indigenous Project Kusha, designed to engage targets at extended ranges.

Medium and short range air defence systems like the Akash, Akash NG, and the Barak 8 (MRSAM), for layered coverage closer to protected assets.

Ballistic missile defence interceptors, including the two tier Prithvi Air Defence and Advanced Air Defence systems for exo and endo atmospheric interception.

Counter drone and counter UAS systems, including directed energy weapons (laser based systems) and electronic warfare jammers to tackle swarm drone threats.

Advanced radar and sensor networks, such as Swordfish long range tracking radars, AEW&C aircraft, and space based surveillance satellites for early detection.

Integrated command and control infrastructure to fuse data from all layers and coordinate interception in real time.

Very short range systems and point defence guns for terminal protection of high value targets.

Defence businesses in Radars, electronics, anti drone systems & those involved in indigenisation of SAM systems will see big traction over the next few years.

Trust Small Cap

Massive Outperformance against Benchmark ( 24.9% vs 1.57% )

Top Holdings

🔥Navin

🔥MCX

🔥Acutaas

🔥ITD Cementation

🔥Sai Life

Managed by @theMihirV 🔥🔥

#Investing#MutualFunds

What is Stanley Druckenmillers Biggest position?

It isn't a Tech, Space x or an AI co. It belongs to the Biotech sector.

Name of the company is :- Natera

What the company does:

Natera is a genetic and molecular diagnostics company. In plain terms, it runs blood and DNA tests that help doctors make decisions in three areas: cancer (oncology), pregnancy (women's health), and organ transplants (organ health).

Its older flagship products include Panorama, a non-invasive prenatal test screening for chromosomal abnormalities in a fetus, and Horizon, a carrier screening test for hereditary conditions. But the real growth engine now is oncology. The business narrative shifted in early 2026 when the company hit a major milestone by generating $107.6 million in positive cash inflow in 2025, removing the dilution risk that had made hedge funds wary of its high cash burn.

Signatera — the blockbuster product:

Signatera is a personalized blood test that detects traces of cancer DNA left in the body after treatment. It belongs to a category called MRD (molecular/minimal residual disease) testing. The idea is simple but powerful: after a tumor is surgically removed, tiny amounts of cancer DNA can linger in the bloodstream long before a tumor is visible on a scan.

Signatera tests for any evidence of cancer cell DNA in a patient's blood and is used to stratify patients and guide therapy decisions after surgery, monitor how patients respond to treatment, and detect early cancer recurrence. It is the leading test in the MRD category and has been proven to meaningfully affect patient outcomes in colorectal, breast, and bladder cancer.

Adoption is the key bull signal: in early 2026, over 50% of all US oncologists had ordered a Signatera test in the previous quarter, and oncology test volumes grew 55% year-over-year in Q4 2025. Natera and bulls believe MRD testing can be a $20 billion market as oncologists keep adopting these tests and clinical utility is proven in more settings. Because cancer patients need repeated monitoring over time, each adopted patient becomes a recurring revenue stream and the feature that makes the long-term economics so attractive.

Razor Blade business model in Biotech, always fascinating to study unique companies.

Disclaimer: no recommendation to buy or sell.

Read the Battle of Ten Kings, preferably in Sanskrit. You will notice many important things. Four of the most important observations are

1. He ruled the Doab which contains Harappa

2. That the enemies were kinsmen as well - it was a fight but not something aimed towards annihilation

3. That the enemies tried to flood his kingdom

4. There were attacks from across India as well. Who were they?

What are the inferences?

India's only approved HVDC transformer winding wire player has delivered 61% growth in FY26.

Now management is conservatively guiding for another 60% growth, while launching a new high-margin product and adding fresh capacity that will drive further volume growth.

Combination of Volume growth + Revenue growth.

I studied the business model, key growth drivers and future prospects of this specialized magnet winding wire manufacturer.

a beneficiary of the CAPEX cycle in Power Transmission, Renewable Energy and Data Centers.

Here's my investment note on KSH International 👇👇

Here are the 7 MNC stocks

1) Timex

Watch Manufacturer

2) GE Power

Servicing and upgradation

3) SKF India (Industrial)

Bearings, seals, lubrication

4) Kingfa Science

High performance polymers

5) Kennametal

Metal cutting tools

6) John Cockerill

7) Schneider Electric

India's thermal power story has flipped. ⚡

2008–19 was the graveyard: 20+ thermal cos went bankrupt, PLFs (Plant Load Factor) crashed 78% → 53% on demand-supply mismatch.

Now manufacturing, EVs & data centers have relit the fire. 🔥

The setup:

📊 80–97 GW new coal capacity ahead

💰 ₹7–10 lakh cr capex supercycle

NTPC's ₹6.22 tn supercycle, Adani 18→42 GW, JSW & Vedanta (3x base) all guiding hard.

Everyone chases the generators. The smarter seat is downstream.

🏗️ Balance of Plant: 40–50% of the value chain.

BHEL's ₹2–4 lakh cr book spills into installation, civil & BoP - a ~₹60,000 cr runway for players like Power Mech.

🔧 Then piping & tubes: the IBR-moated, reorder-heavy layer: Ratnamani Metals, Venus Pipes (SS) and DEE Development (HRSG + high-pressure process piping) right where the boiler-to-turbine plumbing gets specified.

Caveat worth respecting: PLFs are still ~67%. Capacity-led cycle, not utilization-led yet.

Credits to @ishmohit1 (SOIC) for a sharp deep-dive today 🙏

Link: https://t.co/fGbUl8nDvo

Survive first, compound later.

Stay not out 🏏

Disclosure: Not SEBI registered. Educational only, not investment advice. Do your own research; I may hold positions in stocks mentioned.

@Helios18818@RaghavanTh1738@Gamenut1 Exactly. All of their so-called historical achievements are modern insertion during copying. Bamboo Piped natural gas? My foot.

Zoetis, the world largest animal health company, went from $4.5 billion to $9.2 billion in revenue between 2013 and 2024.

India Sequent Scientific tracked nearly the same curve, going from Rs 327 crore to Rs 1,551 crore. Now merged and renamed Viyash Scientific, FY26 revenue hit Rs 3,420 crore with 20% EBITDA margins.

Target is Rs 4,000 crore by FY28. This is one of those sectors where an Indian company is tracking a global leader growth path with a 10 year lag and the underlying demand drivers are identical.

US has 186 million pet dogs and cats combined, roughly one per household. India has about 31 million pet dogs and only 29% eat commercial food.

India pet care market is around $3.6 billion and growing about 20% a year. When pet owners start treating animals the way they treat children, which is happening fast among Indian millennials, they spend more on healthcare.

That vet healthcare spend is exactly what animal pharma companies like Viyash Scientific are built to capture, and India is still very early in this transition.

The company now sells companion animal drugs directly in Spain and Italy. What makes this rollup work is that the demand underneath is not cyclical.

People treating pets like family and spending on their healthcare is a one way behavioral shift happening in every major market, and it feeds directly into animal pharma volumes.

One of India's oldest engineering companies could be sitting at the center of multiple long-term megatrends.

Most investors know the defence names.

Very few talk about the companies that manufacture the critical components behind India's nuclear reactors, missile programs, submarines, and space missions.

Walchandnagar Industries is one of them.

Why it's worth tracking:

- Nuclear: India aims to expand nuclear capacity from 7.5 GW to 100 GW by 2047. WIL has supplied reactor pressure vessels, steam generators, heat exchangers, and other critical equipment to NPCIL & BARC for over four decades.

- Defence: The company has supplied 1,000+ rocket motor casings for Agni, Akash, and Astra missile programs, along with critical equipment for India's nuclear submarine program.

- Space: WIL has manufactured key sub-assemblies for Gaganyaan, while also contributing to missions like Chandrayaan-3 and Aditya-L1.

- New Defence Tech: Through its majority stake in AICITTA, the company has entered the fast-growing Unmanned Ground Vehicle (UGV) segment.

- Operating Leverage: The existing manufacturing base has significantly higher capacity than current revenue, meaning incremental order execution could have a meaningful impact on margins.

The investment case isn't just about today's earnings.

It's about whether India is entering a multi-year capex cycle across nuclear, defence, and aerospace, and whether companies already embedded in these strategic supply chains stand to benefit.

If you keep on looking on today's financials, you will never want to invest in such companies. But you have to sometime look beyond numbers and keep your eyes on the capability.

That said, the risks are equally important:

- Promoter pledge remains elevated.

- Order inflows need to accelerate.

- Interest costs continue to pressure profitability.

- Nuclear projects have historically seen execution delays.

This is a stock where execution will matter far more than the narrative.

Worth keeping on the watchlist.

#StockMarket #Investing #Defence #Nuclear #ISRO #MakeInIndia #Manufacturing #SmallCaps

@AethosWealth

NOPL Solar Projects Private Limited which is a subsidiary of Vikran engineering with 0 employees and 0 revenue has given order to vikran Eng worth 3500 cr 😮

Let me recall what is there on top of my head

Power sector - hitting 52 weeks highs and daily top gainers with govt tailwinds

Lumax auto and ind - PEAD earnings call impact

Dee Dev - tracking since ipo and big order inflection point

Stltech - tracking for last 18 months earnings call tone

Hfcl - sub tailwind of Stltech

Textiles - waiting ??

It may sound simple . May be confluence of FA and TA at the best

Samsung, SK Hynix, and TSMC source 80% of their WF6 from Japan. Two Japanese companies produce 25% of the world's tungsten hexafluoride. Both Kanto Denka and Central Glass are stopping all WF6 production on July 1. We manufacture chemicals. WF6 is a chemical. The semiconductor industry never asked what it's made from. WF6 deposits the tungsten contact plugs inside every advanced chip on Earth. There is no substitute for running production lines. Qualifying a new supplier takes 12 to 18 months. Building new capacity takes two to three years. China controls 80% of the tungsten powder WF6 is made from. Japan's tungsten imports from China have been zero since February. The two producers survived on stockpiles for five months. The stockpiles are gone. WF6 prices are up 232.7% year over year. Upstream tungsten powder is up 557%. Only six companies produce 90% of the world's supply. Two just quit. Every AI accelerator, smartphone chip, and SSD depends on a gas about to lose a quarter of its supply.

A lot of you asked after my HTLS post: who actually makes these conductors in India?

Here is Part 2. The supply side.

Only a handful of companies in the country can manufacture HTLS. And there are two competing technologies you need to understand first. This distinction determines who has the real moat.

ACCC (by CTC Global, USA)

First gen carbon core. Proven globally. But needs specialized hydraulic tools, custom sleeves, trained crews to install. One mistake and you get hidden micro fractures in the core.

AECC (by TS Conductor, USA)

Second gen. Carbon core comes pre tensioned and wrapped in aluminum during manufacturing. Installs using the exact same tools crews already use for regular ACSR. No special training. No special equipment.

For India's ground reality where grid work is happening in tier 2 and rural areas with standard contractors, AECC has a massive practical advantage.

Now here is who has access to what. 🔥

━━━━━━━━━━━━━━━━━━━━

THE ACCC PLAY

━━━━━━━━━━━━━━━━━━━━

Apar Industries

World's largest conductor manufacturer. 50% share of India's reconductoring market. Deep tie up with CTC Global.

→ FY26 revenue: ₹22,902 Cr (+23% YoY)

→ Conductor division alone: ₹12,712 Cr

→ Premium HTLS mix: 6% in FY16 → 49% in Q4 FY26

→ EBITDA/MT: ₹43,000 (vs own guidance of ₹35,000 to 36,000)

→ US business surged 250% sequentially in Q4

→ 45%+ revenue from exports across 100+ countries

Apex predator of the global conductor business.

Trades at ~64x earnings.

━━━━━━━━━━━━━━━━━━━━

THE AECC PLAYS

━━━━━━━━━━━━━━━━━━━━

Universal Cables (MP Birla Group)

Signed TS Conductor agreement early 2026. Known for underground EHV cables, now pivoting into overhead HTLS transmission.

→ FY26 revenue: ₹3,023 Cr (+25.5%)

→ Net profit surged 82.5%

→ Order book: ₹3,025 Cr (₹495 Cr in exports)

→ Executing ₹550 Cr capacity expansion at Satna

→ Trades at ~26x earnings

Dynamic Cables

Rajasthan based. Signed TS Conductor agreement April 2026. Virtually zero debt. ROCE above 26%.

→ FY26 revenue: ₹1,198 Cr

→ PAT growth: 30%

→ Highest ever order book: ₹808 Cr

→ Spent ₹40 to 45 Cr on facility generating ₹250+ Cr turnover

→ Trades at ~22x earnings

Capital efficiency here is exceptional.

━━━━━━━━━━━━━━━━━━━━

HTLS VIA OWN MANUFACTURING

━━━━━━━━━━━━━━━━━━━━

Paramount Communications

Six decade old company. Debt free after ARC restructuring in late 2024. Manufactures HTLS composite core conductors including 61 strand ACCC type configurations for long span transmission and renewable evacuation.

→ FY26 revenue: ₹1,913 Cr

→ ₹300 Cr greenfield plant in MP (commercial by Q3 FY27)

→ Targeting ₹5,000 Cr revenue by FY30 to FY31

→ Heavy US export focus (40% international target)

→ Trades at ~35x earnings

⚠️ Risk: US tariff doubled from 4.5% to 10% overnight. OPM collapsed from 8.3% to 3.36% in one quarter. Geographic concentration without pricing leverage can be brutal.

━━━━━━━━━━━━━━━━━━━━

THE EPC DEPLOYERS

━━━━━━━━━━━━━━━━━━━━

KEC International

Order book exceeding ₹40,000 Cr. Power T&D is 68% of business. Makes conductors internally (₹2,217 Cr from that division in FY26).

→ But FY26 free cash flow: negative ₹743 Cr

→ Debt to equity approaching 0.87x

→ Debtor days stretched from 81 to 101

Classic EPC working capital trap. Revenue grows. Cash does not follow.

Transrail Lighting

Recently listed. Cleanest EPC financials in this space.

→ FY26 revenue: ₹6,880 Cr (+30%)

→ EBITDA margin: 12% (exceptional for EPC)

→ Order book: ₹16,361 Cr

→ Doubled tower manufacturing capacity

→ Trades at just ~17x earnings

━━━━━━━━━━━━━━━━━━━━

THE WILDCARD

━━━━━━━━━━━━━━━━━━━━

Diamond Power Infrastructure

Post NCLT turnaround. Q4 FY26 revenue spiked 108% YoY. PAT up 691%. Order book ₹3,498 Cr. 250,000 MTPA conductor capacity. Manufacturing AL 59, HTLS, MVCC.

But:

→ Net worth: negative ₹604 Cr

→ Total debt: ₹2,529 Cr

→ Operating cash flow: negative

→ Auditor qualifications flagged

High risk. High reward. Not for everyone.

━━━━━━━━━━━━━━━━━━━━

The valuation map:

Apar → 64x (proven global dominance)

Paramount → 35x (own HTLS mfg, export risk)

Universal → 26x (AECC pivot, mid cap)

Dynamic → 22x (AECC, zero debt, small cap)

Transrail → 17x (best in class EPC)

Diamond → 68x (turnaround, negative net worth)

━━━━━━━━━━━━━━━━━━━━

The context that ties it all together:

→ CEA has revised RoW norms specifically for HTLS

→ Berkeley study shows 4 year payback on cost premium

→ 300 GWh wasted in ONE quarter because wires could not carry enough

→ ₹9 trillion committed to transmission infra by 2032

Demand is not speculative. It is already here.

Supply is being built by this very small group.

Not advice. Study this yourself. ⚡

Save this alongside Part 1.