Hace unas semanas lanzamos El Laberinto Fiscal de Colombia en la Javeriana. Para quienes no pudieron venir —o quieren revivir la conversación— el video completo está disponible.

▶️ https://t.co/6P0fFT8U6X

El fin de semana apareció una misma duda en varias conversaciones económicas: ¿Cómo se explica un crecimiento de +10% real en los ingresos laborales entre 2024 y 2025, cuando el PIB creció 2,6% y el consumo de los hogares 3,6%?

Además, el Gobierno ha atribuido el aumento de los ingresos laborales al alza del salario mínimo. Pero ahí hay un problema básico de temporalidad.

El análisis de pobreza del DANE corresponde a 2024-2025. El aumento de 23% del salario mínimo ocurrió en 2026, es decir, después. Por eso, NO se puede explicar una caída de pobreza con una política que ocurrió después de los datos.

En @ANIFCO encontramos algo importante: al revisar el comportamiento real de los salarios en 2026, la dinámica observada va en la dirección opuesta a la del año pasado.

Y eso importa mucho para poder interpretar lo que está pasando con ingresos, pobreza y mercado laboral.

Va 🧵

Sports betting is a scourge.

Legalization reduced food sufficiency by 2.1% among working-age adults without a college degree, especially during the NFL season.

That translates into an estimated 284,000 additional food-insufficient households in 9 states.

@IvanCepedaCast@SaGarcesCorrea Éste mensaje hubiera sido importante mucho tiempo atrás. Al centro político lo maltrataron, vilipendiaron, trataron de traidores, dijeron que el mayor error fue haberlos llevado al gobierno. Después de qué gracias al centro ganaron las elecciones. Hoy ya no les creemos.

Beautiful post by @HannoLustig

arguing bond holders are the most junior claimants to tax revenue-because of the political power or retirees. (True everywhere.) I was struck by this chart showing how little of government revenue even in the US is used for doing stuff and how much more is just transfers. Our governments become gigantic insurance companies.

https://t.co/ywfeNbk8Vj

Excited to FINALLY release toughest+most rewarding paper I've worked on...

….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)...

Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯

🧵

Really cool data on a long-standing puzzle: why did French fertility decline so early? At least some fertility decisions are endogenous, as Le Play mentioned 150 years ago!

Before Brexit, there were about 300K net migrants a year, mostly from the EU.

After Brexit, immigration shot up to 900K, and EU migration was negative.

It’s amazing how stupid Brexit was from every possible perspective.

Populism is a low IQ movement.

Mientras el mundo avanza hacia modelos de gobernanza universitaria más profesionales y estratégicos, Colombia mantiene estructuras diseñadas hace más de treinta años para un contexto completamente distinto. Mi columna 👇 https://t.co/EKMIiSCRBy

Hello @JeffBezos, since you question the results of our studies on the unfairness of the US tax system, please allow me to remind you of the main conclusions of our work, the most comprehensive research to date on this issue.

📉 ¿Por qué las tasas de los créditos hipotecarios van al alza incluso cuando la tasa del Banco de la República había venido bajando?

En este nuevo episodio de Cuentas y Cuentos, Mauricio Reina (@ReinaMauricio) conversa con Daniel Osorio (@danielesosorio), investigador del Banco de la República, sobre los factores que hoy están influyendo en las tasas de interés del sector inmobiliario en Colombia.

Más en el reciente capítulo del #PódcastBanRep 👉 https://t.co/GjQUiO6wzl

A partir de un análisis reciente, el episodio explora por qué la relación entre la tasa de política monetaria y las tasas del crédito hipotecario se ha debilitado, qué papel está jugando la deuda pública y por qué esto hace más desafiante el ejercicio de la política monetaria.

Consulte el Blog de #BanRepExplica "La relación entre la tasa de interés de intervención y la tasa de interés hipotecaria en la coyuntura reciente" 👉 https://t.co/MVOJNMtB6G

Con todo respeto me parece casi que extemporánea la advertencia de la #ContraloriageneraldelaRepublica al manejo de la Deuda pública externa e interna en C/bia 2025 - 2026. Cuanto desborde de las finanzas públicas se habría evitado si hubiese habido un control fiscal oportuno.

Nuevo Blog Banrep: "Este resultado muestra que el deterioro de la situación fiscal no solo encarece la deuda pública, sino que también eleva el costo de los créditos hipotecarios y el financiamiento de proyectos de inversión a largo plazo de la economía."

https://t.co/4i5Lbkh6N3

Norway and the UK drilled the same North Sea.

🇳🇴Norway got $2 trillion.

🇬🇧The UK got tax cuts.

Same basin,Same era.... Completely different outcomes.

Norway captured $30 per barrel in government revenue. The UK captured $11.

That gap, compounded over 50 years of production, is the entire difference.

Norway's model was simple: tax heavily (78% marginal rate), take direct equity stakes in fields via the SDFI, own part of Equinor, and put everything surplus into a fund invested abroad.

The Government Pension Fund Global now holds over $2 trillion in assets.

That's $390,000 per Norwegian citizen about 1.5% of all listed equities on earth.

The fiscal rule: only spend the 3% annual real return. Never touch the principal.

The UK started producing earlier, at lower prices, with a lower tax rate (40%) and no saving mechanism.

North Sea revenues flowed straight into the general budget.

Economists estimate the UK missed out on roughly £400 billion compared to a Norwegian style regime.

The windfall largely financed tax cuts in the 1980s rather than a fund.

Where things stand in 2026?

Norway's petroleum sector will generate $63 bn in net cash flow this year alone feeding a fund already large enough to cover 10-15% of the national budget from returns alone.

The UK is a net energy importer.

Since 2021 it has paid countries like Norway more than £100 billion for gas.

One country treated oil as a finite resource to convert into permanent financial wealth.

The other treated it as income.

image source:eia

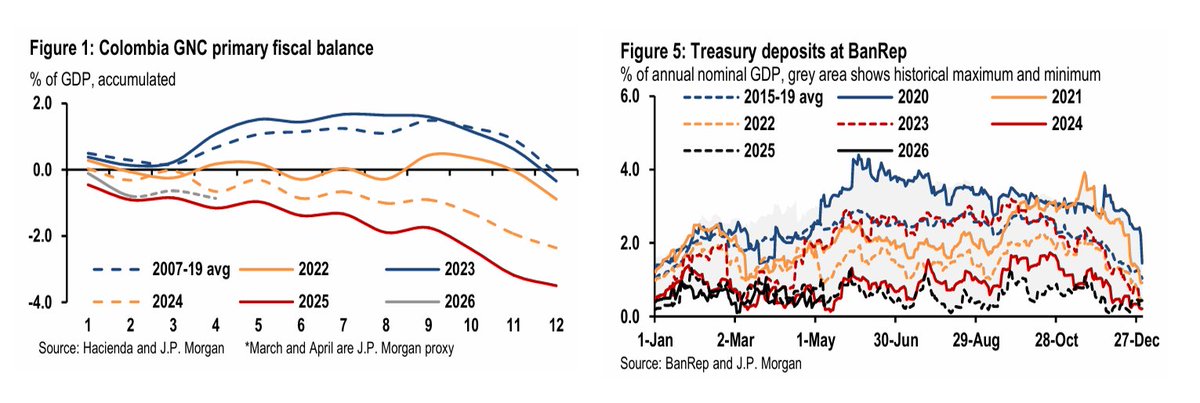

Colombia - Fiscal charts from JPM’s Juan Goldin and Diego Pereira tell a troubling story - a widening primary gap and an evaporating Treasury cash buffer. Elections matter.

Europe is one of the best places in the world to live, but one of the hardest places to build and scale a company.

After 5+ years in France, following 16+ in the US, I have a conflicted admiration for Europe.

On the one hand, Europe has great potential. When I lived in the US, I was skeptical of the European quality-of-life argument. But after getting used to Sunday morning markets, walkable cities, and 4.5 meter ceilings, I get it. There are things that you simply cannot import or experience as a tourist.

These things can make Europe very attractive for creative and intellectual work. I honestly believe some parts of Europe are the “best neighborhood” in the planet. But that’s not the full story.

I am not only a husband and a dad. I am also an entrepreneur. I founded a company in the US 12+ years ago that has offices in the US and Chile and clients throughout the world. I live in France, yet I have not opened a subsidiary here. That is telling.

We once hired someone in France through one of those remote employment platforms. The person received about 5,000 euros net per month, which is considered a very good salary here. But the total cost to the company was closer to 13,000 per month.

That makes hiring feel less like a relationship between a company and a worker, and more like renting someone from the state. At the same time, you take an enormous amount of legal and administrative responsibility. The presumption is that all companies should operate like a 1960s car manufacturer. The response is simple. Don’t set up operations in Europe.

But this is not a remote-work story. I know many small entrepreneurs in France who do not want to cross the threshold from being a one-person activity to becoming an employer. They sometimes refuse a new customer to stay small and avoid the obligations that come with hiring one person. That should worry us.

Many social protections here are described as being provided by the state, but in practice, a lot of the cost and complexity of the implementation falls on the administrative shoulders of entrepreneurs. That is reasonable for a large energy company or bank. But for a small business, it is the difference between an entrepreneur waking up on a Monday to think about product or paperwork.

Growth is not the enemy of the European social model. It is what enabled it. Much of the quality of life we enjoy here today dates back to growth incubated in the past. Growth that is increasingly hard to find. France once led frontier industries, like bicycles in the 1860s, cinema in the 1890s, and aviation and automobiles soon after. Since then, Europe built a more humane social model. But that model was built on the assumption that Europe and the US were the only two rich and industrialized places in the world.

That is no longer true. Global competition in the 21st century is not what it used to be 50 years ago, and the padding built to protect us, may have grown into the handbrake that constrains the growth of the small and flexible firms we need to compete in new frontier sectors.

We should be able to be critical about Europe in our own terms, without comparing ourselves to the US or China. Innovative parts of Europe, like Sweden or Switzerland, operate differently and provide clues. Sweden has embraced a dynamic of capitalization in its pension system for a long time in a continent where fewer people buy stocks. Switzerland, a place that shares an enormous amount of geography and culture with its neighbors, is built in part on strong internal competition among its cantons.

But neither can light a candle to a French open-air market on a Sunday morning. A market where cash is king, and for a reason.

Europe may be the best place in the world to live. But it is also one of the most challenging places to build and scale an innovative activity. The goal is not to weaken the European model. But to get to a place where we can lead again by example. The world will follow us, but only if we are ahead.