Después de la salida de Space X se va a rotar al sector defensa y energía de nuevo. Es lo que me parece por ahora viendo la cotización de algunas empresas.

¿Usas MyInvestor? Mucho cuidado.

Estoy ALUCINANDO con esto que ha ocurrido hoy. Es una completa barbaridad. Atento porque mañana puede pasarte a ti...

Varios clientes me comentan que tenían acciones de $CRWD, una empresa que hoy 2 de Julio realizaba un Split de acciones.

Un Split de acciones es algo habitual en bolsa. En este caso, se divide el precio de la acción de $CRWD entre 4 y, a cambio, te dan 4 acciones por cada una que poseías anteriormente. Es un canje que no afecta a la empresa.

Los brokers serios y normales hacen lo de siempre: adaptan el Split y, si tienes una orden de Stop Loss la cancelan (claro, el precio va a cambiar).

Sin embargo, @MyInvestorES la ha CAGADO monumentalmente.

MyInvestor NO ha contabilizado el Split correctamente, y ha hecho SALTAR los Stop Loss de los que tenían acciones de $CRWD.

Pero voy más allá.

Imagina que tenías 1 acción de $CRWD que ayer valía 780$.

Hoy, cada acción vale unos 195. Pero claro, tienes 4 acciones en lugar de 1.

Bien, pues si usas MyInvestor te han vendido 1 acción con tu Stop Loss (por la cara, sin ajustarlo al Split) y, en este momento, los clientes NO ven las otras 3 por ningún lado.

Es decir, si ayer tenías 780$ (1 acción), hoy te han vendido 1 a 195$. ¿Dónde está el resto? ¿Las otras 3? ¿Por qué vendéis sin adaptar el Stop Loss?

Como digo, ni en Trade Republic ni en Degiro ni en Interactive Brokers se ha visto nunca semejante barbaridad.

Y ahora viene lo bueno.

Un cliente les contacta a atención al cliente. Y desde MyInvestor les responden que "no tienen constancia" de que $CRWD haya hecho nada.

Me pinchas y no sangro.

No uséis MyInvestor para acciones.

Espero de @MyInvestorES una respuesta a estas personas afectadas COMO SE DEBE y con la MAYOR BREVEDAD POSIBLE, así como una explicación. Esto, así, NO.

🇺🇸 Anduril: The Company Rewriting The Entire Defense Industry

While everyone's distracted by SpaceX, the real disruption in defense is happening at Anduril Industries. The company just closed a $5B Series H round at a $61B valuation, doubling from $30.5B in just 9 months. Revenue went from $1B in 2024 to $2.1B in 2025 (+110% YoY), and they're projecting $4.3B in 2026.

In March 2026, the US Army awarded them a 10 year enterprise contract with a $20B ceiling, consolidating over 120 separate procurement actions into one framework. That kind of contract structure was historically reserved for Lockheed and Raytheon. Anduril just took a seat at the table the legacy primes have controlled for decades.

⚠️ Key Drivers

- Anduril's moat is software native architecture. Their Lattice OS platform fuses sensor data, AI targeting, and autonomous coordination across all domains. Legacy contractors built hardware first, software second. Anduril flipped the model,

- The Pentagon is pivoting to "intelligent mass": thousands of cheap autonomous systems instead of a few expensive platforms. Anduril's product stack maps perfectly to this doctrine. Lockheed's F-35 doesn't,

- Arsenal-1 in Ohio is a $1B, 5 million sq ft autonomous weapons factory designed to produce tens of thousands of drones per year. The Fury combat drone is already in production with Roadrunner, Barracuda, and classified programs to follow,

- International expansion is accelerating fast. Edge Group partnership (UAE), Rheinmetall (Europe), Dutch Ministry of Defence contracts, plus participation in the US "Golden Dome" missile defense system,

📈 TLDR: Anduril is doing to defense what Tesla did to automotive and SpaceX did to space launch. The legacy primes are 60 year old contractors trying to compete with a software first, AI native, vertically integrated machine. When this company goes public, it's going to be the most anticipated defense IPO in modern history.

Over the last few days I’ve heard a lot about $AVEX being cheaper than $ONDS, so I sat down to do the math. Everyone’s wrong.

Here’s the comparison everyone’s making. They take what each company is worth and divide it by what it’s expected to sell this year:

$AVEX: worth ~$2B, sells ~$610M this year → about 3x

$ONDS: worth ~$4B, sells ~$390M this year → about 10x

So $ONDS looks three times more expensive. Case closed, right? That’s where almost everyone stops. And it’s wrong on two levels.

First problem. That 10x for $ONDS ignores something big: the company is sitting on $1.4B of cash. Cash is money you basically get back, so you subtract it before judging how expensive a stock is. Do that and ONDS isn’t 10x, it’s closer to 7x. Most people skip this step entirely.

But even 7x vs 3x is the wrong comparison, and here’s the real point. Comparing two companies on sales only makes sense if each dollar of sales is worth the same. It isn’t.

When AVEX sells $1, it keeps about 22 cents as profit. When ONDS sells $1, it keeps 49 cents and that number has climbed three quarters in a row, heading toward 50-60 cents. So a dollar of ONDS sales is worth more than double a dollar of AVEX sales. Judging them on sales is not a good comparison.

So compare them on profit instead of sales. Once you do:

AVEX: you pay about 15x its profit

ONDS: you pay about 14x its profit

They cost basically the same. That whole “ONDS is three times more expensive” thing? It was never real. It was just people forgetting that ONDS keeps way more of every dollar it sells.

Now the part that matters for where these go over the next couple years.

AVEX is a low-margin hardware company, and that won’t change much, so the stock probably won’t get re-rated higher. Its margins are stuck, so its valuation is stuck. It’s profitable and it’s fine, but it’s a parked car, not an engine.

ONDS is the opposite on every front. Its margins are rising. Its market is enormous and getting bigger: it just expanded from defensive anti-drone systems into actual strike weapons (loitering munitions, the kind the Pentagon is spending the most on right now). It became a direct government contractor six months ago through its Mistral deal, which opened doors it didn’t have before. And its order book is growing faster than it can even fill it: over $150M in new orders this quarter alone.

Run the same profit math on 2027 and $ONDS becomes cheaper than $AVEX outright. The stock that looks “expensive” today is the bargain on a two-year view - as long as it turns those orders into actual sales. That’s the bet.

And here’s the thing almost nobody has noticed. There’s a set of warrants people keep calling “dilution.” But those warrants, if used, hand the company about $3.4B in fresh cash on top of the $1.4B it already has. Management says that’s enough to buy companies that could add up to $1.8B in new yearly revenue. So everyone’s anchoring on this year’s $390M sales number while the company is quietly pointing at a path to four times that. The “expensive” multiple is built on the wrong number.

One last thing, since someone always brings up the cash burn. Last quarter it looked like $ONDS bled a lot of money, but most of that wasn’t really burn, it was them buying inventory to fill orders they already have. That’s cash turning into product that ships, not money disappearing. The real burn is small, about $11M a quarter, against $1.4B in the bank. They’re set.

Bottom line: $AVEX is a cheap, safe, low-margin name that probably stays put. $ONDS costs the same on profit today, but with rising margins, a far bigger market, a growing order book, and billions in spare firepower behind it. More risk, yes, but the upside is on the side of the one that can actually re-rate.

Stop judging defense stocks by their sales. Judge them by the profit those contracts actually produce. Do that, and “ $AVEX is cheaper” stops being true.

Not advice. Both are speculative. Do your own work.

Best,

- Jan

Qué cerca está $ADBE al precio ideal de compra... espero una bajada rápida, cargar y esperar cambio de tendencia. Creo que tocará los $160 puntualmente antes de finalizar la tendencia bajista.

Everyone is looking at $XFAB and $SIVE right now.

But there is a quieter bottleneck sitting one layer down, the one both Jensen and Goldman have already flagged: liquid cooling.

So I decided to map the entire liquid cooling supply chain, every name, in this thread.

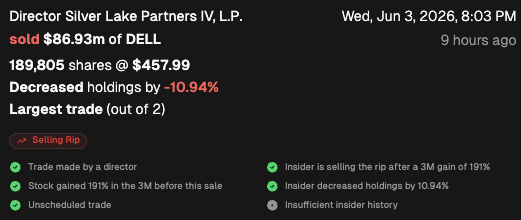

Director (Silver Lake Partners IV, L.P.) at Dell Technologies Inc. $DELL sold $86.93M (largest sale ever, out of 2).

Rip Sell: the stock was up 100% in the previous month.

4 other insiders also sold the stock in the last 30 days.