Goldman Sachs: Optical Networking

> Driven by an AI infrastructure ramp-up and rising computing power per rack, Goldman Sachs forecasts a 9x expansion in the total addressable market (TAM) from US$15bn (GB300 NVL72, mainly in 2026) to US$154bn (Rubin Ultra NVL576, mainly in 2028).

> CPO is projected to contribute US$91bn, capturing 59% of the overall US$154bn TAM (assuming a 29% penetration rate in scale-out).

> Aggregate networking dollar content per computing unit across scale-up and scale-out is expected to surge 29x, jumping from US$315k in the GB300 NVL72 to US$9.4bn in the Rubin Ultra NVL576. Per computing unit, dollar content increases by 16x in Scale-Out and 45x in Scale-Up.

> The addressable market for optical modules/engines expands 13x when moving from scale-out to scale-up architectures.

Pluggable Optical Modules & Silicon Photonics (SiPh)

> The value market for pluggable optical modules in scale-out will grow 10x per computing unit from the 2H25 server model to the 2H27 server model.

> Equivalent 1.6T units per computing unit will skyrocket from 216 units (GB300 NVL72) to 2.5k units (Rubin Ultra NVL576).

> Silicon Photonics adoption in the datacom market is expected to spike from 6% in 1Q24 to 45% by 4Q28, offering up to a 32% BoM cost advantage and 20% price advantage over traditional EML solutions at 1.6T speeds.

Technology Matrix & Supply Chain Realities

> Copper cables and PCBs remain king for short-distance, cost-effective, and low-power connections, but optics become essential for high-speed, long-distance interconnections.

> Light source supply (both EML and CW lasers) is expected to remain very tight through 2026/2027 due to booming AI demand and Indium Phosphide (InP) substrate export controls from China. Supply balance isn't expected until 2H28 as supply chain expansions come online.

> Alternative entirely optical signal switches (like Google's Palomar OCS) are scaling rapidly, enabling datacenter speed upgrades without needing to replace the switches themselves. Lumentum’s OCS backlog crossed $400M as of Feb 2026.

This is a report from April which is made publicly online by GS, but I don't think people covered it enough. Hence, revisiting and highlighting key data potentially missed.

Goldman Sachs: June 2026 Update Supply/Demand

Compared to their May report, they have updated:

> NAND and DRAM from "tight" to "very tight" supply in Q1-Q2 of 2027.

> InP from "very tight" to "tight" in CY27

> T-Glass from "balanced" to "tight" in CY27.

Highlights:

> DRAM Pricing Surge: Like-for-like prices for DRAM are projected to skyrocket by 250–300% in 2026, with Average Selling Price (ASP) including product mix jumping 300–350%.

> Memory & T-Glass Supply Relief Delayed: The supply/demand balance for DRAM/NAND and T-Glass is expected to remain "Very Tight" longer than previously expected, extending all the way through Q2 2027 before potentially easing slightly to "Tight" in Q3 2027.

> InP Substrate: Like-for-like pricing for 2026 has been updated to 15–20%.

> Foundry (TSMC): Stays severely constrained through 2027.

> Advanced Substrates & Materials: ABF Substrate, PCB, and CCL face persistent, severe shortages. This is reflected in heavy price hikes, with CCL and ABF Substrate seeing price increases of 30–50% in 2026 and climbing even higher (45–60%) in 2027.

> Optical Components: Optical Cables and Optical Devices remain severely supply-constrained through the end of 2027, maintaining steady double-digit price increases.

> Global Power & Analog Semis: Shifting from "Balanced" or "Easing" in early 2026 to "Tight"by late 2026/early 2027. Note: Local China supply for these sectors is expected to remain "Balanced".

> Silicon Wafers (300mm): Starting out "Easing" in early 2026, but projected to transition to "Tight" by 2027.

> Local China Foundry & Equipment (SPE): Supply conditions for local Chinese foundries and Semiconductor Manufacturing Equipment (SPE) remain mostly "Balanced" with minimal price fluctuations (0–5%).

> MLCC & Tantalum Powder: Enjoying an "Easing" or "Balanced" state in early 2026 before settling into a stable "Tight" market for the remainder of the forecast period.

BofA: AI Power Demand

> 100+ GW Supply Gap: The US is projected to face an electricity generation shortfall of over 100 gigawatts (GW) between 2026 and 2030.

> Surging Demand vs. Capped Supply: Global semiconductor team forecasts imply a need for 230+ GW of capacity demand, while the US utilities team expects only 93 GW of accredited supply from regulated utilities.

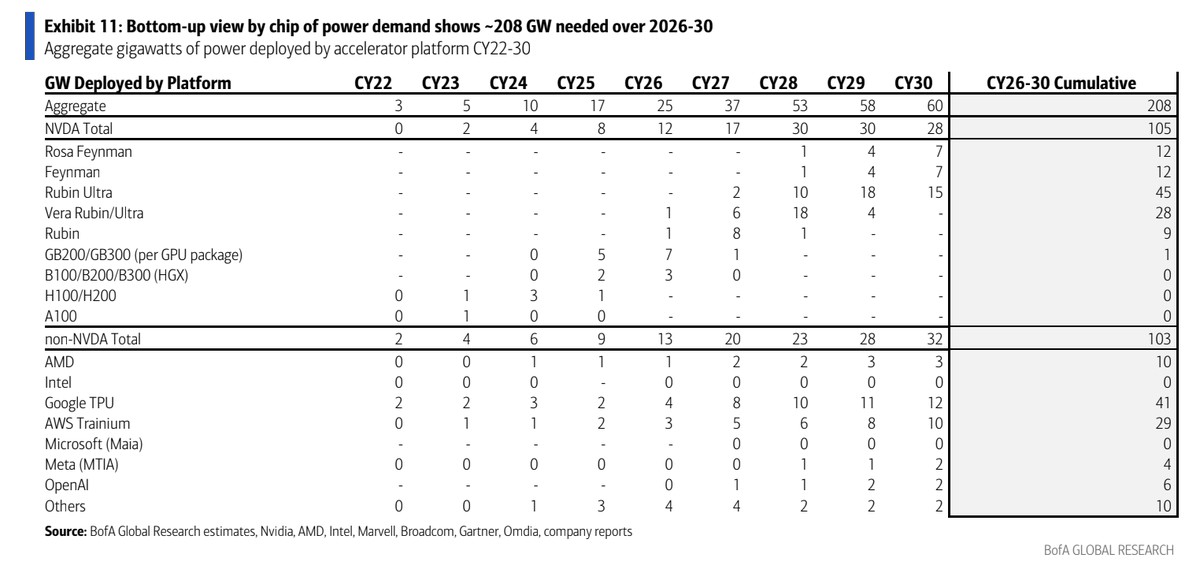

> Massive Compute Load: Driven by AI accelerators, global IT load is expected to require 208 GW between 2026 and 2030. Factoring in a 50% North American share and a 1.20 Power Usage Effectiveness (PUE) multiplier to account for cooling and facilities, this translates to 125 GW of direct US data center load growth.

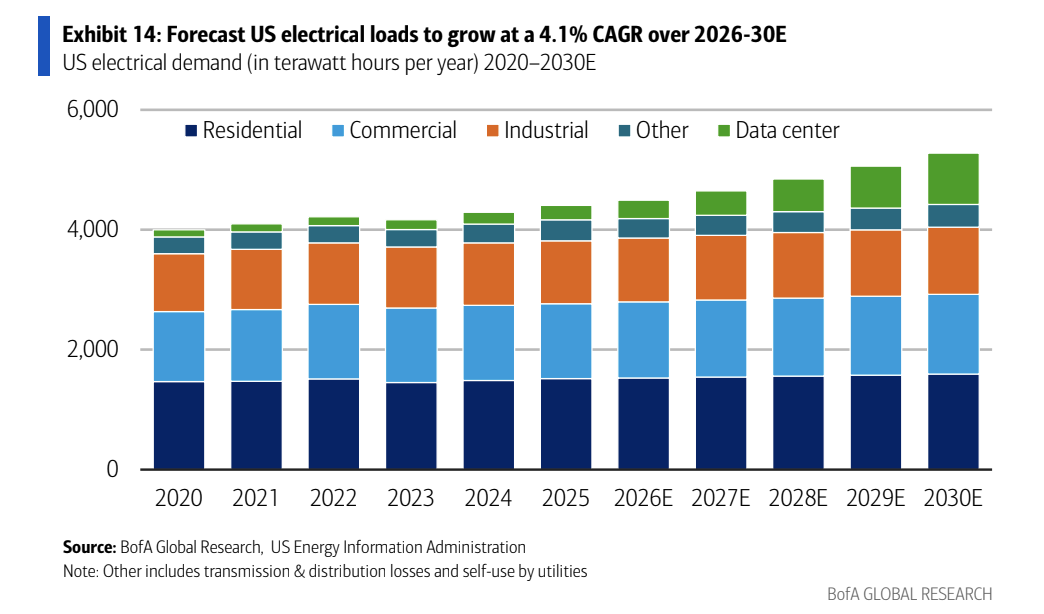

> Accelerated Growth Rate: After flat growth from 2010 to 2020 (largely due to a 150bp drag from LED adoption, appliance efficiency, and residential solar), US electrical load is projected to grow at a 4.1% CAGR from 2026 to 2030.

> Rise of Gas Engines: Due to turbine scarcity and the need for fast-response grid balancing, data center developers are shifting to gas reciprocating engines. Leading manufacturers like Caterpillar, INNIO Group, Rolls Royce, and Wärtsilä have all announced capacity expansions.

> Exponential Rack-Level Power Growth: BofA Global Research pointed out a staggering leap in the power density required by Nvidia's hardware generations. Power density has jumped from 35 kilowatts (kW) per rack for the Nvidia H100 chip up to an estimated 600 kW per rack for its upcoming Feynman architecture.

$GEV $CAT $NVDA $AMD $GOOGL $AMZN $INTC

Morgan Stanley: CPO Update

> Rapid Scale-Out CPO Growth: CPO switch shipments are expected to grow from 23k units in 2026 (mostly 100T switches led by NVIDIA's Spectrum) to 59k in 2027, and reach 200k units by 2030, representing a 144% CAGR from 2024 to 2030.

> Coupling Mainstream: Grating coupling remains the mainstream choice for TSMC's $TSM COUPE platform and major customers (NVIDIA, AMD, Ayar Labs), with mass production expected to begin soon in 2H26.

> PIC Capacity Ramping: TSMC plans to expand Photonic Integrated Circuit (PIC) capacity from 10k wafers per month (kwpm) in 2026 to 15kwpm in 4Q26, and to at least 25kwpm by 2028.

> Customer Pipeline: Due to limited initial capacity, primary mass-production customers for 2026–2027 are expected to be NVIDIA $NVDA, Broadcom $AVGO, and AMD $AMD. In 2028, MediaTek, Marvell, and Ayar Labs are projected to scale up.

> Testing Bottleneck Easing: Wafer-level testing (Insertion 2) times have vastly improved from an entire day per wafer in 2H25 to six hours per wafer today, with a 3–4 hour target in sight for the next 6–12 months.

Technology Spotlight: GlassBridge vs. Traditional FAU

> GlassBridge Potential: Corning’s $GLW GlassBridge (a wafer-based glass interposer solution using waveguides) offers great scaling, high density, and detachment features, but is still far from mass production.

> FAU Resilience: Traditional Fiber Array Units (FAU) remain the highly customized, lowest-loss mainstream choice. Analysts do not expect GlassBridge to disrupt high-end players like TFC in the near term, as it is more likely to compete with low-end edge-coupling FAUs first.

JUST IN: For forty years, memory chips were the worst business in technology. A brutal commodity, made of sand, sold by the ton, with profit margins that collapsed to nothing every few years. Last night that business reported the kind of margins only software companies dream of. AI just broke a cycle that defined an entire industry for four decades.

The numbers do not look real. Micron's revenue quadrupled in a single year, to 41 billion dollars. Net income went from 1.9 billion to 28 billion. And the number that should stop every investor cold: gross margin hit 85%. One year ago it was 39%. Memory chips, the most commoditized product in tech, now earn the fat margins of a software company, on a physical thing you can hold in your hand.

Understand what that means, because it breaks a 40-year rule. Memory was the definition of a cyclical business. Prices boomed, everyone built factories, supply flooded, prices crashed, margins went negative. Every few years, like clockwork. That clock just stopped. The CEO said shortages now run until 2028, and the company has locked half its future revenue in binding multi-year contracts. A commodity does not get contracts. A chokepoint does.

This is the whole year in one earnings report. AI did not just create winners in software and chips. It reached down into the most disrespected business in technology, the one nobody wanted, and turned it into the most profitable hardware on earth, because the machines cannot run without it and there is not enough to go around.

The worst business in tech just became one of the best. Not because memory changed. Because AI changed what memory is worth.

The cycle did not turn. It broke.

Life gives us two choices:

Either accept your circumstances as they are, or accept the responsibility to change them.

Complaining changes nothing. Waiting changes nothing. Blaming changes nothing.

The moment you take responsibility, you take control. Every meaningful change begins when someone decides to stop accepting limitations and start creating possibilities.

Your future is not shaped by the conditions you face, but by the actions you choose despite them. ✨

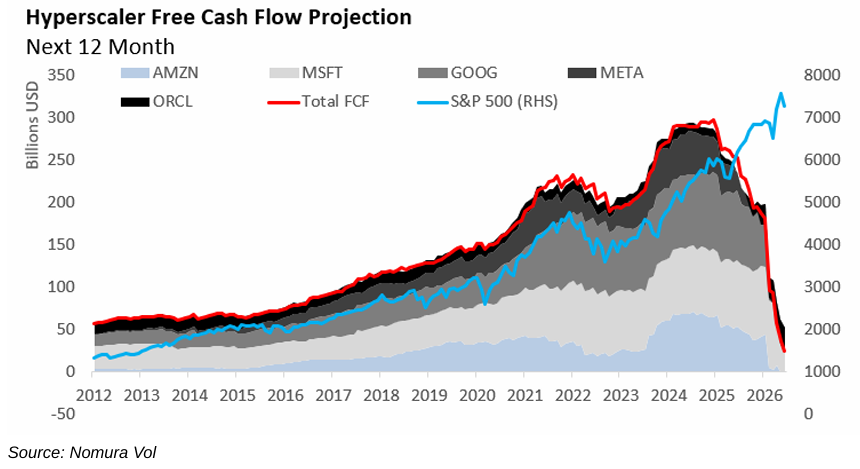

Big Tech just ran out of money building AI and what they're doing to cover it up should be illegal.

Google, Amazon, Microsoft, and Meta are spending a combined $700 BILLION this year on AI infrastructure.

This eats up 94% of their total operating cash flow.

The richest companies in human history are almost broke. And instead of slowing down, they're covering it up with the biggest financial engineering operation since 2008:

Google just sold $80 billion in stock to fund AI infrastructure. That was their first equity raise in 20 YEARS.

The last time Google needed to sell stock, YouTube didn't even exist. Sundar Pichai admitted the thing keeping him up at night is "compute capacity."

The company that prints $100 billion a year in ad revenue just told Wall Street it isn't enough anymore.

Amazon's free cash flow is projected to go NEGATIVE this year for the first time ever. Morgan Stanley estimates a $17 billion deficit and Bank of America says $28 billion.

The most profitable logistics machine on Earth is about to burn more cash than it generates, and they quietly filed with the SEC saying they may need to raise even more debt and equity to keep building.

All four hyperscalers are now borrowing hundreds of billions in bonds to keep the AI buildout alive. These were the most cash-rich companies in human history, and they're leveraging themselves to the teeth to build infrastructure that nobody has proven will generate enough revenue to pay for itself.

And the cracks are already starting to show:

Broadcom makes the custom AI chips that power Google, Meta, OpenAI, and Anthropic. This week their AI revenue TRIPLED year over year, sales grew 48%, and profits smashed every Wall Street estimate.

The reward for all of that was $320 billion in value erased in a single trading session.

Their CEO Hock Tan went on the earnings call and exposed three things about the AI industry:

Google is already shopping for cheaper AI chip alternatives, broadcom abandoned its strategy of selling complete AI systems and is now retreating to selling bare chips at lower margins.

And despite supposedly "unprecedented demand," Tan refused to raise his full-year forecast, which tells you everything about what he's actually seeing behind the curtain.

Wall Street heard all three and hit the sell button so hard it dragged AMD, Intel, and the entire chip sector down with it.

When a company triples its AI revenue and gets punished because tripling isn't fast enough, the expectations have left the atmosphere entirely.

And here's the really scary part...

These companies ARE your retirement account. Apple, Microsoft, Amazon, Google, Meta, and Nvidia make up roughly 30% of the S&P 500. If you have a 401k or an index fund, you are already exposed to this bet whether you chose to be or not.

Every single one of these companies is telling you AI will generate trillions in revenue. But right now the math says they're spending trillions FIRST and hoping the revenue shows up later.

If the revenue catches up, this becomes the greatest infrastructure buildout in human history. Bigger than railroads and bigger than the internet.

If it doesn't, the companies that make up a third of the American stock market just leveraged their balance sheets into the largest write-down cycle since 2000.

And unlike the dot-com crash, this time the bubble companies aren't random startups with no revenue. They're the backbone of the entire global economy.

instead of watching 2 hours of Netflix tonight, watch this 40-minute masterclass from the founder of a $20B China AI company

it's the clearest explanation I've seen of how Agent Swarms and AI systems actually work at scale

useful whether you've never built an agent in your life or have been using Claude every day for the past year

I took the key ideas and turned them into a practical guide on how to actually build with Kimi

find it below

The best rewards in life come from playing long games. Your physical and mental health, personal relationships, and wealth are a direct result of your ability to be consistent and disciplined. You win by doing the boring stuff over and over and over again.

A single Vera Rubin Ultra rack will pull 600 kilowatts in 2027, That is 5x today top racks and 75x the global average.

The chips are ready, grid is not, Nvidia is shipping, US substations need 160 weeks to deliver one transformer.

12 GW of data center capacity was announced for 2026, only 5 GW is under construction, Power was a boring utility cost, Power is the new chip 😎

While America builds AI factories, China builds the boring stuff that powers them. 60% of global power transformer production sits in China.

Chinese transformer exports jumped 36% to 9.3 billion dollars last year, US lead times stretch to four years. China lead times are months.

Hyperscalers are quietly buying Chinese transformers to fill the gap, Imports from China jumped from 1,500 units in 2022 to over 8,000 in 2025, The chip war misses the real chokepoint - Iron and copper still rule.

India runs 1.2 GW of data center capacity today, China and the US are planning racks that each pull 0.6 megawatts on their own.

The gap is not just compute, the new chokepoint is wattage, transformers, and substations. India added 44 GW of renewable capacity in 2025 but transmission to data center clusters remains the weak link.

Hyperscalers are picking sites by power availability, not labor cost, India needs grid first

People say that France's nuclear power plants produce cheap energy, but they forget to tell us that you can't repeat the trick. Building costs and requirements have increased a lot.

Newly built wind/solar is around $30–80/MWh, new nuclear is typically $100–150+/MWh.