Everyone's celebrating "AI agents replaced our call center."

In production the actual pattern is messier.

The agent handles 60-70% of volume. The remaining 30% is the hard stuff that needed humans anyway — refunds gone wrong, edge cases, angry customers who escalate the second they hear a bot.

You don't save 100% of the cost. You save maybe 40%.

And your CSAT on the hard tail gets worse before it gets better.

The win is real. But it's not "industry wiped out." It's "industry restructures" — and the teams who design the human handoff well end up with better economics than the ones chasing full automation.

Anyone shipping this in production knows: the handoff is the whole game.

@rauchg we used this last night and its better than Fable and slightly worse than GPT 5.6 Sol. And it would soon be open weights. Models will be a commodity its what we do with them that will matter.

@divlohia The CRM tax on reps is real. Every deal I've watched slip started with "I'll update it later." Curious how Katalyst handles the messy stuff — half-remembered calls, side channels on WhatsApp, the deal context that never makes it into any field.

Bangalore and Chandigarh topping is the real story. Both are planned-ish cities with concentrated white-collar work. Delhi and Mumbai carry huge informal economies that drag the average down. Income tables reveal more about a city's job mix than its wealth.

https://t.co/SgX49hjOMu

@divlohia@startupideaspod The Salesforce agent layer sounds great until you realise the CRM data is 40% junk. Reps don't log calls, deal stages are wrong, contacts are stale. An agent with opinions on bad data gives you confident garbage. Fix the input layer first, then the smart layer earns its keep.

Everyone thinks large cap means safe. Infosys and TCS are both down 50% from their tops.

Safety was never in the market cap. It was in the business underneath.

The IT services model got repriced the moment AI started writing usable code in production. Not because revenue collapsed, but because the market stopped believing the next 10 years look like the last 10.

Big doesn't mean protected. It just means further to fall when the story changes.

The Enterprise AI Stack Reality:

1. Generic models lose to domain models trained on your messy real data

2. Your moat isn't the model, it's the eval set only you can build

3. Tacit workflow knowledge takes years to encode

Most teams obsess over #1 and skip #2 and #3.

https://t.co/ojvO0kkmIz

Every enterprise will have its own model-harness-sandbox-eval flywheel with token value per watt optimization. This is the future. Simple reason: tacit knowledge about the domain and customers and their workflows that the company uniquely understands and has built trust around.

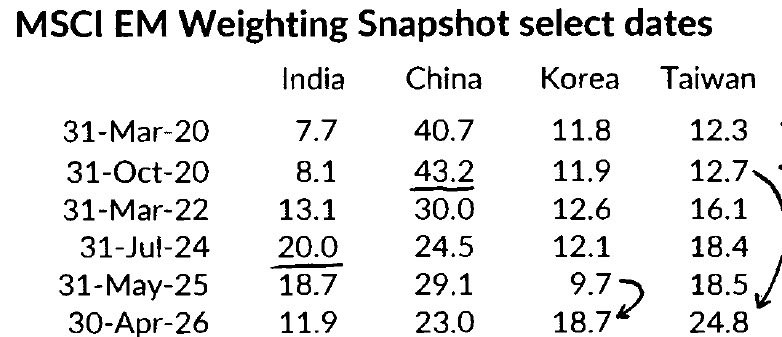

The math here is wild. Two small economies own 43% of EM weight while India+China, with a third of the planet and nearly a third of world GDP, sit at 35%. Index construction lags real economic gravity by a decade. The rerating is coming!!

https://t.co/JBt5ajK2XS

Korea + Taiwan 43% of EM index.

1% of world population and

2.5% of world GDP (PPP basis)

India + China now 35% of EM index.

35% of world population.

29% of world GDP (PPP basis)

@vsvicky_ Compounding looks slow until it doesn't. Each trillion is the same percentage move getting easier in absolute years because the base is bigger. The real test is whether per capita compounds like this, not GDP.

@NeilBahal The algo didn't bury F1 and tennis. It noticed you stopped clicking and gave up on you. Newspapers don't care what you like, which is exactly why they're useful.

Zoho building enterprise software for the Indian Army is a bigger deal than most realise. Defence tech has been foreign-vendor territory for decades. An Indian SaaS company crossing into that buyer is the kind of signal that changes what young founders here believe is possible.

https://t.co/sn6JSkt6Bz

The bubble isn't in AI. It's in the slides explaining why this AI company is different from the other 400 AI companies in the same deck.

https://t.co/RGAQ2SnANm

While I did not agree with Prof on Zomato at 40 rs where he called it worthless, I do agree with him on the bubble in valuations of several AI cos.

Though I believe in AI itself as a technology and enabler.

Vertical SaaS had two moats. The data you collected over years, and the workflows nobody else understood well enough to rebuild.

Inference just commoditized the second one.

A new entrant can now ship the workflow in weeks, not years. The depth that took a decade to encode in code is now a prompt and a decent eval set away.

What's left as a moat is the data, the distribution, and the trust of the customer. Everything else is rentable.

The vertical SaaS that survives this cycle won't be the one with the best product. It'll be the one whose customers can't imagine switching.

The under-discussed point here: Zoho cracked China the hard way. 25 years, localised product, 300 people on the ground. Most Indian SaaS folks treat China as a closed market and skip it. Vembu treated it as a customer base. Different mindset, different outcome.

https://t.co/2W19McbPbn

We have been operating in China for 25 years and we have over 300 employees there spread across multiple offices. We have steadily gained market share as we have invested heavily in localising our software and understanding the needs of Chinese customers.

We have two data centers in China dedicated for hosting Chinese customer data.

谢谢 🙏

The boring sectors are quietly running the show. Power, cables, transformers — none of this was in the WhatsApp group chats two years back. Capex cycles take time to show up in stock prices, and when they do, most retail investors are already late.

https://t.co/22NOXrtm7R

When the sector was ignored and called a slow grow thing sector, power and cables and wires hit a new high. So did transformers. Yesterday I was looking at the huge rally in some of the textile stocks. The UK FTA deal effectuates around 15th July and should do this sector well. The consensus trade of many research was buy large cos, IT and consumer and much of this flopped. The sector focussing on water treatment also did well- another sector where I wrote on way early some cos earlier when I could name (now I don’t due to lack of clarity on Sebi guidelines).

Point is trends play well if you enter early and hold. Stocks see a lot of up and down and most ask on cos at highs not lows as then suddenly the light shines from the top of a mountain. The real achievement is in finding the road, spotting an opportunity in the strength of a mountain, wearing your all weather gear and climbing. You will get tired, sometimes dehydrated but the feeling of a stock at highs is the adrenaline that makes it worth it when you reach the top and look at where you started from.

Last few days, working on a massive list of cos as a universe and sifting through them to identify a few. Idea of a large list is to remove bias across cos or sectors and understand better- and I’m in no rush. Even if I miss a co I can learn from it if not earn from it.

This summer with no foreign travel intend to catch up more on my research and reading and making myself better.

Powerlook going from a single store to a ₹1,000 Cr target by FY30 is the part of the D2C story that doesn't get told on stage.

Everyone wants to talk about online brands going offline. Nobody wants to talk about offline brands surviving long enough to even attempt the jump.

The boring math: most D2C brands die between ₹50 Cr and ₹200 Cr. Not because the product breaks. Because the founder hasn't built the back-end to run 50 stores, 500 SKUs and a marketplace at the same time.

The ones who cross ₹1,000 Cr aren't the loudest. They're the ones who built supply chain discipline before they built a brand book.