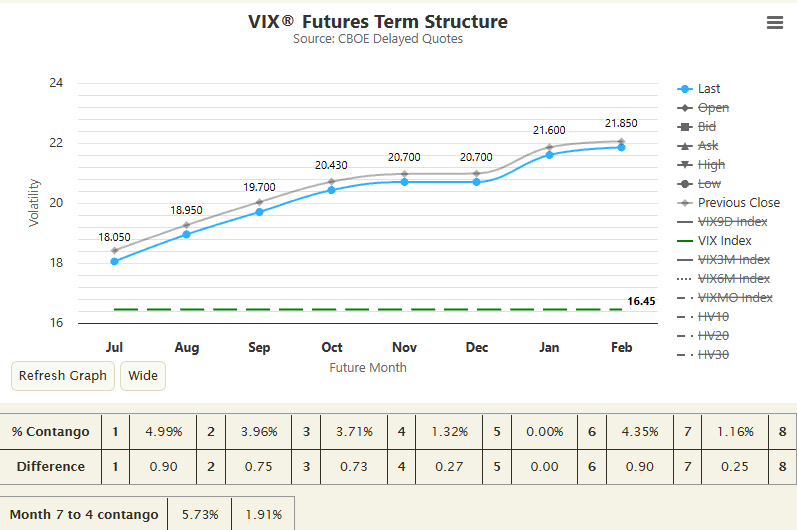

$VIX futures curve continues to remain in contango. It’s important to remember that low vol induces lower vol (clustering).

The VIX is one of the more unique asset classes where it experiences volatility clustering. This just means that vol isn’t randomly distributed. Put simply, when markets are calm or turbulent, that period will tend to persist for some time. So for example a VIX reading at ~16 will tend to stay around that range for a period of time. It’s statistically a better trade to short low volatility than it is to long it as counterintuitive as it may sound. Earlier on in my career, I can't even tell you how many times I got so excited to buy vol <15 only to get steamrolled thereafter.

You can look at an extreme example of clustering effects with a year like 2017 where VIX was sub 17 for over a year and realized vol came down to a 4 handle. That would mean $SPX was only moving an average of roughly 0.25% a day. To calculate this: you can take the square root of the trading days in a year (252) and you get 15.87% but we’ll typically round up to 16 for simplicity. Then divide realized vol (4) by 16 to get 0.25%.

The one concept that’s a bit more challenging for folks to comprehend is the effects when vol is elevated. Yes it’s very common knowledge that the VIX is mean reverting, but when it’s elevated it will tend to remain elevated for a bit. Clustering effects do however on average last longer to the downside because of that mean reversing tendency, given it’s under normal spot/vol correlations. That just means when SPX goes higher, “normal” spot/vol corr will see vol (VIX) go lower as well. Equity markets inherently have skew where the most likely moves are to the upside so this is all partly why clustering will last longer to the downside.

Back to the upside effects. So when you see a VIX at say 35, the most likely next move is for it to print 40 than it would be to print 25. This is why you’ll see many vol participants talking about buying a VIX at 35 even after it’s come up from say 20. The clustering effects work both ways and that's the important concept to remember.

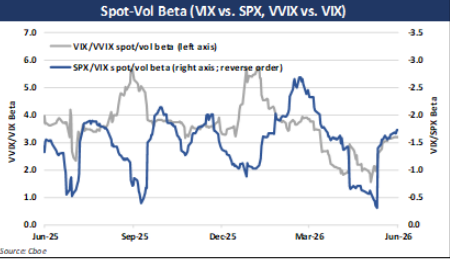

Looking at our current environment, we haven’t seen VIX print over 23 since April and it’s been floating around this 15 range for the last few weeks. This is exactly another example of what volatility clustering is. We currently see VIX futures sitting in Contango which means that prices further out in time (months) are higher prices than its current spot price (VIX) and front month price. This is why since SPX topped on June 2nd, it’s pulled back 400pts, but VIX in that same time is only up 0.5pts.

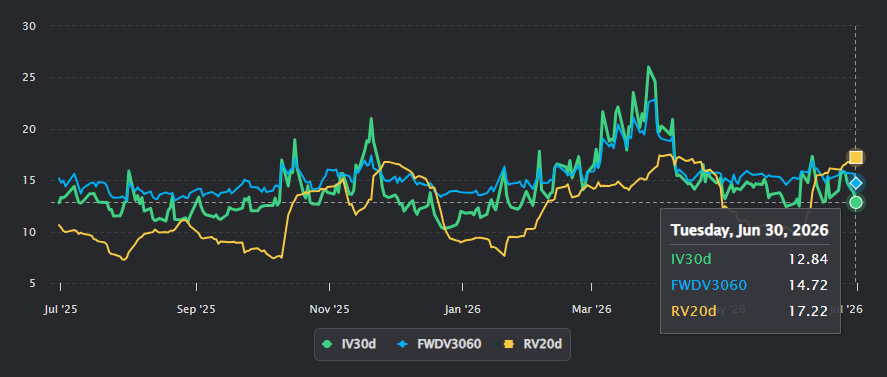

What’s rather interesting here is the variance risk premium (IV-RV) which sits at -5pts which is quite large. We’ll typically see that large of a negative reading after steep and quick SPX drawdowns. The bias with this setup is to on average decay vols further with lower close-close realized vol to bring the basis back into the mean. The other but less likely option is to see implied vols rise into realized vol but with /VX sitting in contango there isn’t much to say of that right now. If you look at COR1M (implied correlations 1 month) it’s at a 5 handle which is also historically very low, so this means single stock vol is moving into new highs with lots of dispersion. It makes sense to see this when skew is steep (currently at 30th %ile) so participants just bid upside convexity like every other pullback the last year.

You have to really zoom out in time to see any sort of “slight” worry and that is for midterm elections. This midterm vol is hanging at 20 right now with an ever so slight backwardation between Nov-Dec at 0.1pts. I’ve written some posts on how dispersion and vol behaves around elections and the TL;DR is that within the 30 trading days sampled, vol peaks 3 TDs before the election and normalizes thereafter. Anyways, there’s lots of opportunities across the landscape right now as we head into the typical summer trading lull months. So we'll have to stay tuned to see if it ends up being quiet or not. Cheers!

In March, Meta signed a $27B cloud services deal with Nebius. In April, Meta signed a $21B expansion of their cloud services agreement with CoreWeave.

Two weeks ago, Bloomberg reported that Meta signed up to rent 1.6GW of data center capacity from Crusoe. And just 3 days ago, the Financial Times reported that Google had capped Meta's use of Gemini because of capacity constraints.

And now all of a sudden, Meta actually has excess capacity?

In reality, I suspect Meta looked at SpaceX's valuation and recent deals to sell excess capacity.. And came to the conclusion that investors will look favorably upon any willingness to monetize their capacity externally.. Which will give their share price some relief, and allow them to raise capital.. Which they'll use to buy and build more compute capacity, lol.

$META $GOOG $NBIS $CRWV

“What matters is not the eggs, it is the Goose itself”

SoftBank probably down -13.5% today

after markets saw this investor presentation today.

Also the OpenAI IPO possible 2027 delay cause Altman wanted a $1T valuation might have been a small cause…

Micron results: I think the biggest take away for me is really simple: Micron made more profit this quarter than NVDA made almost exactly 1 year ago. And next quarter’s guidance is way more than what NVDA made in Q3 of 2025. NVDA did about $35 billion in revenue and $20 billion in profit in q3 2025. Micron will do $50 billion in revenue and $35 billion in profit next quarter. Does everyone see this? Does everyone understand this? NVDAs market cap at the time was $4 trillion. Micron’s current market cap is $1 trillion dollars. Micron is growing faster than NVDA did last year in actual dollars and percentages and it trades at 1/4 the valuation. Math is math. Liars figure, but figures never lie.

The biggest changes that come from AI are going to be things we can’t even conceptualize yet.

In 1995-2000 nobody could have accurately predicted the iPhone, YouTube, Instagram, Facebook, FaceTime, ecommerce, cloud, Uber, TikTok, streaming, etc.

The entire world lives online.

People are trying to understand AI through what already exists. Wrong way to go about it.

In reality it’s going to create entirely new products, behaviors, companies, and industries that seemed impossible.

Yes AI will have its own versions of the iPhone, YouTube, cloud, etc. that radically change the world.

The world 10 years from now is going to look more different than people can imagine.

@ChizaramNelo $100K ….. when you start seeing daily swings of $1K to $3K it’s a tough mental adjustment. When you get to $1M its $50k swing days. It’s a wild rollercoaster of emotions. Over the years you go numb to it and just focus on having your decision making compound, the numbers follow

Jeff Bezos reveals why compromise is one of the worst ways to resolve a disagreement

"An example of a really bad way of coming to agreement is compromise. If I say the ceiling is 11 feet and you say 12 feet, we say let's call it 11 and a half. That's compromise"

"The advantage of compromise is it's low energy. But it doesn't lead to truth"

"Another really bad resolution mechanism is who's more stubborn. Two executives disagree, they have a war of attrition, and whichever one gets exhausted first capitulates. You haven't arrived at truth, and this is very demoralizing"

"Escalation is better than a war of attrition. Escalate to your boss and say, we can't agree, we like each other, we're respectful, but we strongly disagree, we need you to make a decision"

"Exhausting the other person is not truth seeking. Compromise is not truth seeking"

These people don't appear on any published rich list.

The shadows and gutters of global finance are filled with anonymous billionaires, heirs, and villains.

And we don't have a clue.

When you go buy a Dell laptop bundle only to find out that the CPU is Intel, the RAM is Micron, the GPU is AMD, the internal Hard Drive is Seagate, the external Hard Drive is Western Digital, and they toss in a bonus SD Card that is SanDisk.

It all makes sense now...

It all makes sense.