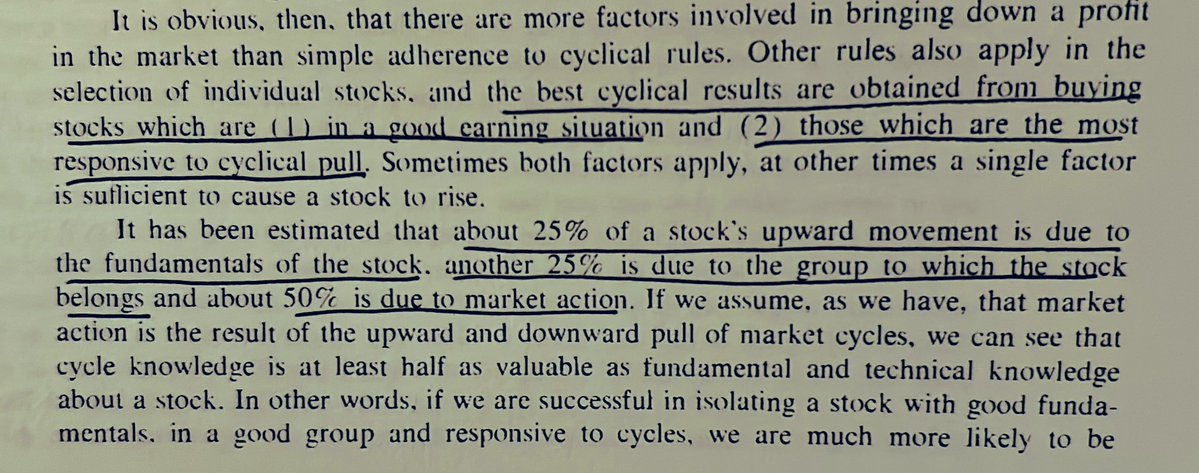

William Garrett nailed it in 1973 when he said:

“About 25% of a stocks upward movement is due to the fundamentals, another 25% is due to the group which it belongs, and about 50% is due to market action.”

Humbling reminder for fundamental investors.

the “boring” industries will pay you more than any sexy niche ever will

- freight

- insurance

- logistics

- compliance

these industries have no hype, no noise, but insane cash flow

most of them still run on outdated systems...which means even small fixes create massive ROI

they don’t want hype...they want predictability

and the person who gives them that becomes impossible to replace

i broke down how to spot these overlooked niches and plug the gaps no one else sees

like, rt & comment “BORING” and i’ll send the doc

must follow so i can dm you

Let me walk you through my interpretation of where $BABA $JD $BIDU $PDD currently stand in the market cycle, based on observable signals such as price action, news sentiment, and broader investor psychology.

Admittedly, this is speculative, but I find such exercises intellectually stimulating and perhaps you’ll enjoy reading it as much as I enjoy theorizing. Who knows, there might even be some truth to my musings.

Markets are as much about narratives as they are about numbers, and sometimes, stepping back to assess the prevailing mood can reveal opportunities obscured by short-term noise.

I believe Chinese equities, particularly high-profile ADRs are firmly in the "disbelief" stage of the market cycle. For reference, this is the phase where early signs of recovery emerge, but skepticism remains so entrenched that most investors dismiss them.

The psychology here is fascinating: bad news is magnified, good news is ignored, and sentiment is overwhelmingly bearish despite improving fundamentals.

Right now, the narrative around China is dominated by:

Geopolitical and Regulatory Risks: The lingering U.S.-China tensions, potential ADR delistings, and unpredictable regulatory crackdowns (e.g., Alibaba’s antitrust fines, gaming restrictions) have left investors wary.

Earnings Volatility: Recent misses from Alibaba and PDD, alongside slowing consumer spending, reinforce the perception that China’s recovery is fragile.

Structural Distrust: Many global investors now view Chinese equities as "uninvestable" a sentiment eerily reminiscent of past market bottoms where extreme pessimism created value.

Historically, the best entry points occur when:

Sentiment is at rock bottom (headlines are universally negative, positioning is overly bearish).

Valuations disconnect from long-term fundamentals (e.g., Alibaba trading at distressed multiples despite its cash flow and market dominance).

Early positive catalysts are ignored (e.g., selective policy easing, buybacks, or insider buying).

We’re seeing all three today. The market is pricing in a worst-case scenario, but China’s equity risk premium may have overshot reality.

I’m betting half my net worth on the revaluation of Chinese tech ADRs.

Feel free to check my portfolio @julius5207

Let me walk you through my interpretation of where $BABA $JD $BIDU $PDD currently stand in the market cycle, based on observable signals such as price action, news sentiment, and broader investor psychology.

Admittedly, this is speculative, but I find such exercises intellectually stimulating and perhaps you’ll enjoy reading it as much as I enjoy theorizing. Who knows, there might even be some truth to my musings.

Markets are as much about narratives as they are about numbers, and sometimes, stepping back to assess the prevailing mood can reveal opportunities obscured by short-term noise.

I believe Chinese equities, particularly high-profile ADRs are firmly in the "disbelief" stage of the market cycle. For reference, this is the phase where early signs of recovery emerge, but skepticism remains so entrenched that most investors dismiss them.

The psychology here is fascinating: bad news is magnified, good news is ignored, and sentiment is overwhelmingly bearish despite improving fundamentals.

Right now, the narrative around China is dominated by:

Geopolitical and Regulatory Risks: The lingering U.S.-China tensions, potential ADR delistings, and unpredictable regulatory crackdowns (e.g., Alibaba’s antitrust fines, gaming restrictions) have left investors wary.

Earnings Volatility: Recent misses from Alibaba and PDD, alongside slowing consumer spending, reinforce the perception that China’s recovery is fragile.

Structural Distrust: Many global investors now view Chinese equities as "uninvestable" a sentiment eerily reminiscent of past market bottoms where extreme pessimism created value.

Historically, the best entry points occur when:

Sentiment is at rock bottom (headlines are universally negative, positioning is overly bearish).

Valuations disconnect from long-term fundamentals (e.g., Alibaba trading at distressed multiples despite its cash flow and market dominance).

Early positive catalysts are ignored (e.g., selective policy easing, buybacks, or insider buying).

We’re seeing all three today. The market is pricing in a worst-case scenario, but China’s equity risk premium may have overshot reality.

I’m betting half my net worth on the revaluation of Chinese tech ADRs.

Feel free to check my portfolio @julius5207

EXCLUSIVE: I had the pleasure to interview the Chairman and CEO (Jeffrey Edwards) of one of our largest holdings - Cooper Standard $CPS. This is one you don't want to miss. I'm excited to say it exceeded all expectations I had going in! Watch here 👇

https://t.co/pPniD2huP5

🚨🚨🚨HOLY FUCK:

- BYD Zhengzhou factory will be BIGGER than San Francisco

- 10x LARGER than the Tesla Gigafactory Nevada

how the fuck will @elonmusk compete with this scale?

Everyone thinks Trump is guilty for this market crash.

I see something different.

What looks like economic incompetence might actually be a brilliant strategic move.

The 4D chess explanation: 🧵