1/ 🧵 $292M of rsETH — was drained from @KelpDAO's @LayerZero_Core bridge in a single forged message. 48 hours later, $13B of DeFi TVL had walked out the door whilst it remains unclear where the losses actually will land. Let's unpack the ecosystem impact.

Excited to announce our latest round of financing that helps us bring tokenized risk to market at scale.

Over the past year, we have seen 8 major depegs, including two major defaults (xUSD/USDx) and the most intense liquidation event in the history of crypto on 10/10. Meanwhile, increasing regulatory clarity is bringing traditional financial participants into onchain markets. It is expected, over the coming years, all of finance will move towards tokenized rails, moving RWAs from $30b today closer to the $600t that exists offchain. Despite this, onchain risk infrastructure, is at it’s infancy, whilst the demand for it has never been higher.

Cork is reimagining risk for the crypto era where money is programmable and there can be a market for anything. We have a unique opportunity not just to build infrastructure for risk, but to create new ways to understand risk that are not skeuomorphic or analogous to what existed in TradFi. Institutional-grade risk management is only the first step in making these possibilities broadly available.

With the backing we announce today, we establish Cork as the leading markets based solution to tokenized risk and we are looking forward to helping scale onchain markets through world class risk tooling.

USDX is becoming a 680m$ rug pull! Disabled discord, deafening silence and zero transparency

Let’s dig into what’s becoming the biggest scam of 2025 👀

What is USDX?

@StablesLabs describes USDX as “A delta-neutral synthetic stablecoin that offers: Delta-neutral stability with 100% crypto collateral and censorship resistance by passing banks. Scalability, yield from crypto arbitrage, and transparent reserves with insurance.”

In reality, it is a pile of money controlled by the Stableslabs team, which they in the background have supposedly been performing various arbitrage strategies with to earn a yield.

The Initial Depeg

On November 6th, USDX underwent a major depeg described in further detail here.

https://t.co/C0BBo7S6kn

Following the depeg and major cascading liquidations on lending markets, there was complete silence from the Stableslabs team. No X post, no discord post. Just deafening silence. Despite the token supposedly being fully backed with no public evidence of wrongdoing.

Depeg becomes rug-pull

Towards the end of the first day of the depeg, Stableslabs deactivates their Discord. This is a very bad sign. The only reason to in such a moment disable the Discord is to prevent coordination in response to what likely is actually happening. No further commentary from the founders or investors.

On November 8th, the first message from StablesLabs since the depeg is published, referencing a “restoration agreement” to make holders whole.

https://t.co/2RxA4Gzxj6

Reading through this announcement, I have strong confidence that this indeed is a confirmed rug-pull. Let’s break down why.

First of all, the post states that:

“recovery path referenced to the value of 1 USD. This arrangement is voluntary in nature and does not constitute a guarantee, redemption obligation, deposit-taking, or collective investment product.”

What

How can you say fund recovery is voluntary!? Clearly, the team is taking the stance that they legally are not required to honor redemption requests of their tokenholders.

Secondly, there is a snapshot taken, but users are asked to register in this Google Form. For processing legal claims, this looks awfully unprofessional. It looks like an intern threw something together in a hurry, not a genuine attempt to get in touch with affected users.

Third, they announce that:

“Execution will proceed in phases, depending on:

-Resource allocation and recovery planning

-Liquidity conditions

-Cooperative arrangements”

Without stating any timelines or details about their reserves, resource allocation or anything else. All they are saying is, we won’t tell you nothing and you won’t hear from us for a while. These are delta neutral strategies, they should be fully liquid with at max 1-2 weeks delay.

The market is clearly showing us how it interprets the announcement. Normally, if 1:1 redemptions would be made available, USDX would likely recover to somewhere close to 1. In their docs, it is stated redemptions can be processed by KYCd institutions, but clearly none such redemptions have come through. The fact that it dropped about 40% following the announcement, says a lot.

It is a common strategy for teams that rug-pull, to hide behind lawyers and slowly fade away with stolen funds. I hope major tokenholders or enforcement agencies pursue legal options to make the situation right, it might be the only path to fund recovery for the thousands of affected users who were misled by promises of stable yield opportunity.

Lessons and path forward

An original value of crypto is trustlessness, that you should only need to trust the code. The reality is, most protocols are not aligned with such values. USDX is an example where users needed to put their full trust in the team, and the team betrayed their trust. Whilst trust is not inherently an issue, as a space we might want to consider taking steps to bring us closer back to trustlessness in how we design these primitives.

The collateral damage from USDX will be felt by many. Likely many funds and vaults had some exposure that will result in further contagion risk. In the next weeks, we shall see what the impact ultimately is. This is a major reason why we are building @corkprotocol to help create mechanisms to shield contagion risk and minimize ecosystem spillover when such events take place. Furthermore, risk pricing and the ability to manage risk for market participants, may help prevent these catastrophic failures from occurring in the first place.

This event is sad, infuriating and unjust, however, it is also part of the game. With high yield, comes high risk. From an evolutionary lens, USDX represents a failed experiment. I hope we at least can take away some lessons, to build back stronger.

If you like this coverage, please give @robdogeth a follow for more updates on stablecoin depegs

USDX, a $680m stablecoin by @stableslabs is undergoing a major depeg ⚠️

Let’s break down what is happening and the cascading ecosystem impact

What is USDX?

Stableslabs describes USDX as “ A delta-neutral synthetic stablecoin that offers:

Delta-neutral stability with 100% crypto collateral and censorship resistance by passing banks. Scalability, yield from crypto arbitrage, and transparent reserves with insurance.”

Why is USDX depegging?

On Nov 4th Stableslabs announced that $1m of liquidity was lost in the Balancer V2 exploit.

https://t.co/JAhhnD8Rr9

The Balancer exploit resulted in a significant contraction of onchain liquidity as various market participants withdrew funds from DEXs and lending markets. This combined with major price pressure across major assets have resulted in meaningful outflows out of various stablecoin farms. This comes with the backdrop of Black Friday, which was a systematic crash across perpetuals markets which triggered an automatic deleveraging (ADL) event which broke numerous delta neutral strategies that were farming the basis trade. Ethena, the largest delta-neutral strategy was unscathed due to bespoke agreements separating their risk which enabled them to avoid major losses from ADL across their exposures. However, interestingly this likely amplifies the ADL for other market participants which has resulted in numerous fund blow-ups.

The first major body to float from this event seems to have been Stream Finance, their XUSD blew up causing a $280m liquidation unwind. As described in further detail here.

https://t.co/7eaK9rkV97

Stableslabs USDX has a very similar name, similar strategy and lost liquidity in the Balancer hack, as a result numerous looping vaults across Euler and Lista DAO in particular were seeing significant outflows. This spiked borrow rates that putting looping trades under-water and threatening liquidations. Lista DAO today passed an emergency vote to process the liquidations on their markets to shield lenders.

https://t.co/IX90H1AZoU

Interestingly, this emergency vote changed the oracle configuration to be market based. Causing a major liquidation cascade on already thin USDX liquidity. As a result of significant outflows, borrow rates have spiked, see below Re7 Labs Clusters on Euler. Borrow APY’s are 300% on Euler and over 800% on Lista DAO. Consequently, a complete unwinding of these looping trades has been occurring the past hours.

The scope and scale of liquidations is in the range of 10s of millions, not massive for a $680m$ synthetic dollar. However, dumping directly into a market with thin liquidity has massively amplified the issue.

As a result of liquidations, peg volatility has been massive, with price dipping as low as 40c, recovering to 80c and now hovering around 60c.

Is the depeg permanent?

At this point we don’t know if this depeg is permanent or temporary because Stableslabs has not yet announced the freezing of their redemption mechanism. If redemptions come through, there is a massive arbitrage opportunity to buy deppeged tokens, however, only available to KYCd market makers.

One scenario is that market makers are simply too busy recovering from the numerous losses throughout the week to properly arbitrage this peg deviation.

The other, in my opinion likely scenario, is that USDX experienced real losses during Black Friday which are yet to be properly disclosed due to lacking transparency. In a sense, the market is pricing in a major haircut to the value of USDX collateral. If that is the case, at some point we should see an announcement of halted redemptions. Radio silence from Stablelabs during the past two days is absolutely deafening. If they do have collateral to back all the redemptions, why not just say it and calm the market?

This is an evolving situation. Please give @robdogeth a follow if you want to stay up to date as it unfolds.

Lessons and path forward

Financial markets deal with risk, farming novel stablecoins can provide high yields, looping such tokens can further amplify the yield, however, also the risk. The challenge is excessive risk taking is currently blowing up in everyone’s faces. We are missing transparency disclosures and risk pricing.

This is why we built @corkprotocol, to provide a liquidity buffer and hedging mechanism for onchain participants to manage and price these risks. Crypto doesn’t need to eliminate risk, it needs to properly internalize the price of risk. There is no free lunch, with yield comes risk, but we must become better at pricing and managing such risks so that we don’t create a house of cards.

This week is brutal not only because of the erosion of trust caused by these numerous blowups, but the fact that they keep cascading. Which is the next body to float?

For crypto to become institutionally adopted and to become the fabric of modern finance, we urgently need to develop risk management infrastructure. This is why I am so bullish on @corkprotocol and I hope as we weather this storm take a moment to reflect and build back stronger.

The future of finance must include risk management.

⚠️USDX, the $680m delta neutral stablecoin by @StableLabs is depegging ⚠️

This comes after they said that 1m$ of liquidity was drained from the Balancer hack

This could be a similar story to Stream's XUSD where delta neutral strategies blew up due to ADL after Black Friday

xUSD is undergoing a major depeg and default event following a $93m hole in their balance sheet resulting in $280m of leverage unwinding. Let’s break down what is happening:

What is xUSD and Stream Finance

Stream Finance operates numerous vaults, which effectively are managed as onchain hedge funds. xUSD in particular is described as “ takes advantage of market neutral strategies to earn high yield. This strategies vary from lending arbitrages, to incentive farming, to dynamically hedged HFT, to market making.”

xUSD has 382m$ of AUM which is offering an estimated 18% yield. Today, Stream announced that an external fund manager which was running their book lost 93m$.

https://t.co/j6Sqna0tqR

The reason this is causing such a tremendous amount of collateral damage is not only because of the 93m$ hole in their balance sheet, but what the rest of the balance sheet is comprised of.

The xUSD Loop

A core part of the yield generation strategy was aggressive looping using xUSD as collateral. A part of this strategy surrounded a bespoke looping agreement with Elixir, but additionally xUSD was deposited across various lending markets to borrow collateral (such as USDT0) and this collateral was used to mint more xUSD. Repeated multiple times such that an initial 1$ deposit may mint several $ of xUSD. As a result, Stream became the major holder of xUSD. It is today not fully clear exactly what is backing xUSD as there is a missing transparency report, but various onchain resources that I have assembled pieced together the story.

The primary reason for the looping strategy is to harvest various forms of yield arbitrage in lending markets, with the added benefit of significantly inflating AUM for xUSD as well as partnering protocols. It’s unclear if the strategy was somehow nefarious or simply excessive risk taking gone wrong.

As the market internalizes the $93m hole in the balance sheet, a major unwinding of all these loops are currently occurring. Let’s dig into the adjacent impact across the DeFi ecosystem.

Elixir Impact

deUSD from Elixir was borrowed in a bespoke agreement to Stream with xUSD as collateral. Elixir is the only debt holder with a 1:1 claim to xUSD redemptions.

https://t.co/4wsRTwzPzu

The exposure is 68m USDC, about 65% of deUSD backing. Supposedly, the bespoke agreement shields Elixir as a senior debt holder in this story which is alleviating some of the concerns about deUSD’s backing. However, questions remain about the ability to repay the loans from Elixir, which has resulted in significant peg volatility for sdeUSD.

Lending Market Impact

xUSD was widely used as collateral, mostly on L2s such as Plasma, where it was aggressively levered using hardcoded oracles. A full rundown of the affected lending markets was compiled by YAM with combined exposure of $284.96m.

https://t.co/rBYeIbRJqM

To use the largest market as an example, let’s examine xUSD on Euler on Plasma. $107m of xUSD is supplied with a hard-coded oracle at 1.27$. The collateral is used to borrow USDT0, plUSD and msUSD. Each of these lending markets are facing a serious amount of bad debt. Actual liquidation and clearing of this bad debt will likely pend the full bankruptcy of xUSD due to the hardcoded oracles.

Oracle design and lender losses

The above example may be the largest single loss for DeFi lenders (non-exploit related) and underpins the real risks of lending to high risk assets with hardcoded oracles. Lenders in these markets will be stuck for the foreseeable future as liquidations are blocked by the oracle. The borrower (xUSD) will face a 75% borrow APY in the meantime which further increases the losses for Stream. So far, Morpho Vaults on Ethereum mainnet seem largely unscathed. However, fear both tied to deUSD as well as broader contagion risk is pushing several of the largest vaults to 40%+ yields as many markets have limited excess liquidity as loops are being liquidated and lenders withdraw their funds.

A significant part of the xUSD has been converted to other yield bearing tokens to perform loop arbitrage. A major exposure is Midas mHYPER (which is fully backed!), that was minted and looped on Morpho. Currently at a 90m$ market size and 65% borrow rate, this loop is being unwound by xUSD.

This major spike in borrow rates across numerous assets is resulting in loop unwinding for other market participants. The issue is exacerbated by a general liquidity shortage following the Balancer exploit, Black Friday and overall negative price movements.

Solutions and lessons

We built @corkprotocol for these exact types of events, it can both act as a redemption buffer for liquidity crunches as well as a risk market to price risk and enable users to hedge against losses.

Ultimately, the culprit is excessive risk taking, rehypothecation and poor transparency for xUSD depositors.

Oracle design played a major role in amplifying the issue, if Euler markets were not hardcoded, less bad debt would have accumulated and positions could have been liquidated when there was existing AMM liquidity. Hopefully we as a space consider adopting alternative approaches to oracle design.

The story is still evolving, please give @robdogeth, @talkintokens and @corkprotocol a follow if you want to stay up to date on this event as it unfolds.

Excited for the next chapter for Cork

We received a lot of signals about where risk management infrastructure is needed. We keep hearing the biggest issue is duration risk

RWAs, vaults, protocols, all face duration risk but have no DeFi native tooling to address it

Until now

Black Friday wasn’t just a correction

It was a coordinated liquidation event

And USDe was the trigger

But not how you think

Let’s talk about the oracle problem no one wants to touch

And how a stablecoin became the perfect weapon

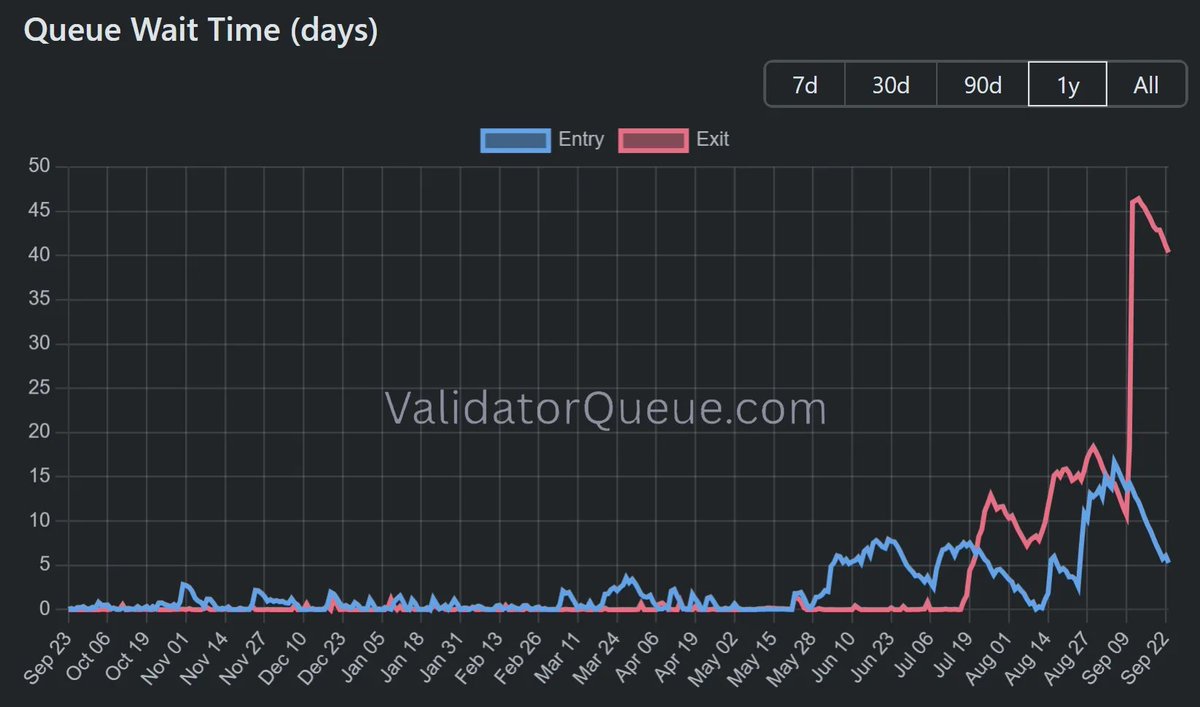

Is the validator exit queue a ticking time-bomb in plain sight?

Let’s investigate the mechanics driving the explosive growth in the validator exit queue and it’s consequences for DeFi

Understanding the exit queue

To secure Ethereum, validators stake ETH. To ensure continuity of economic security, there is a limit to the amount of ETH that can simultaneously be staked and unstaked.

By design, only 1 in every 65k validators (of 32 Eth each) can exit each epoch. Each epoch lasts for about 6.4 minutes, which means there are 225 epochs per day. Assuming 8 validators can exit per epoch, this means 57,600 Eth can exit the network per day at a maximum.

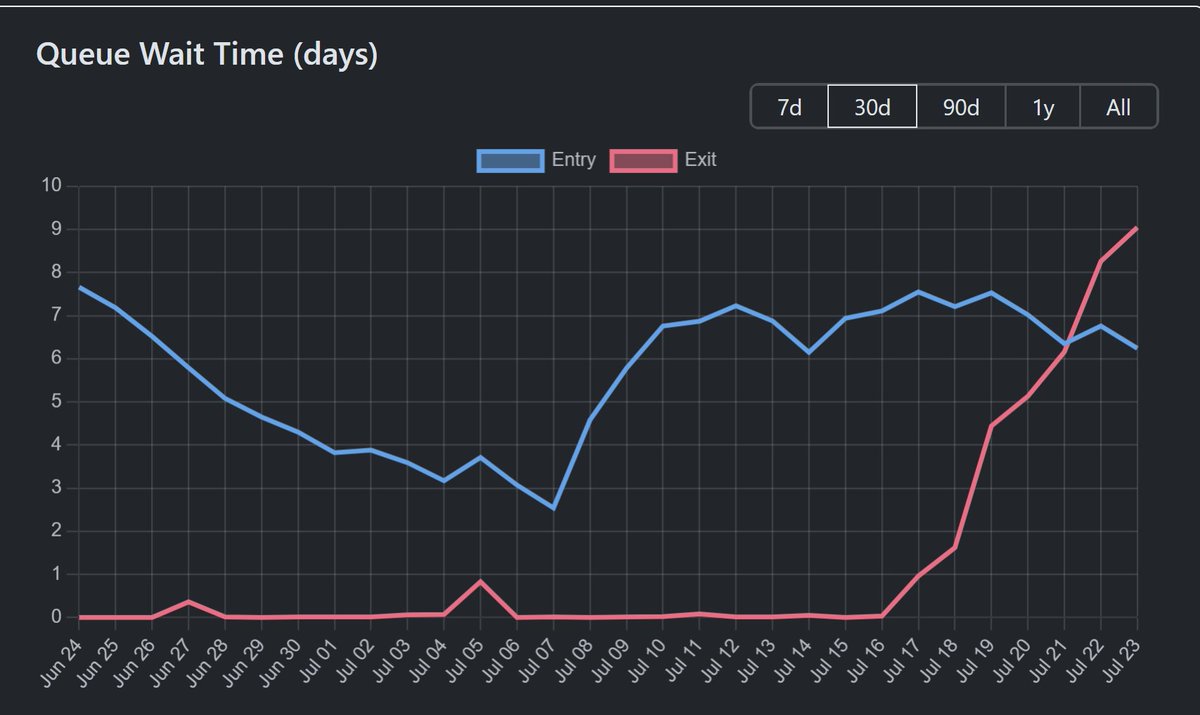

The validator exit queue has recently gone vertical, roughly tripling the previous all-time-high to reach 45 days. Fundamentally more people need to unwind their validators than there is exit capacity, resulting in growing queues. The problem is that this could trigger a vicious unwinding loop which has massive systemic impacts on DeFi, lending markets and the use of LSTs as collateral (to be explored below).

What drove the exit queue growth

The initial trigger to the queue was a reshuffling of ETH on Aave which drove a great stETH looping unwind (as explained here):

https://t.co/d0IgP1sUqg

This created initial queue congestion. Since then, stETH has consistently been trading slightly below peg, reflecting a continuous unwinding of stETH through exit queue arbitrage (which we will explore further below). Subsequently, Kiln Finance for security reasons have rotated their validator set resulting in major volume across the entry and exit, this was the primary driver of the most recent spike.

https://t.co/W4UzcYJOH3

There is significant FUD around the queue claiming that it represents sell-pressure overhang, that validators are dumping and as a result ETH price will tank. This is a fundamental misunderstanding of the dynamics at play. This unwinding is in my opinion largely neutral on ETH/USD because it relates to ETH rotations. Though, it has everything to do with the LST/ETH price, and the peg stability of major LSTs/LRTs. To understand this point, we must first understand the liquidity mechanisms of LST/LRT pegs.

LST peg stability

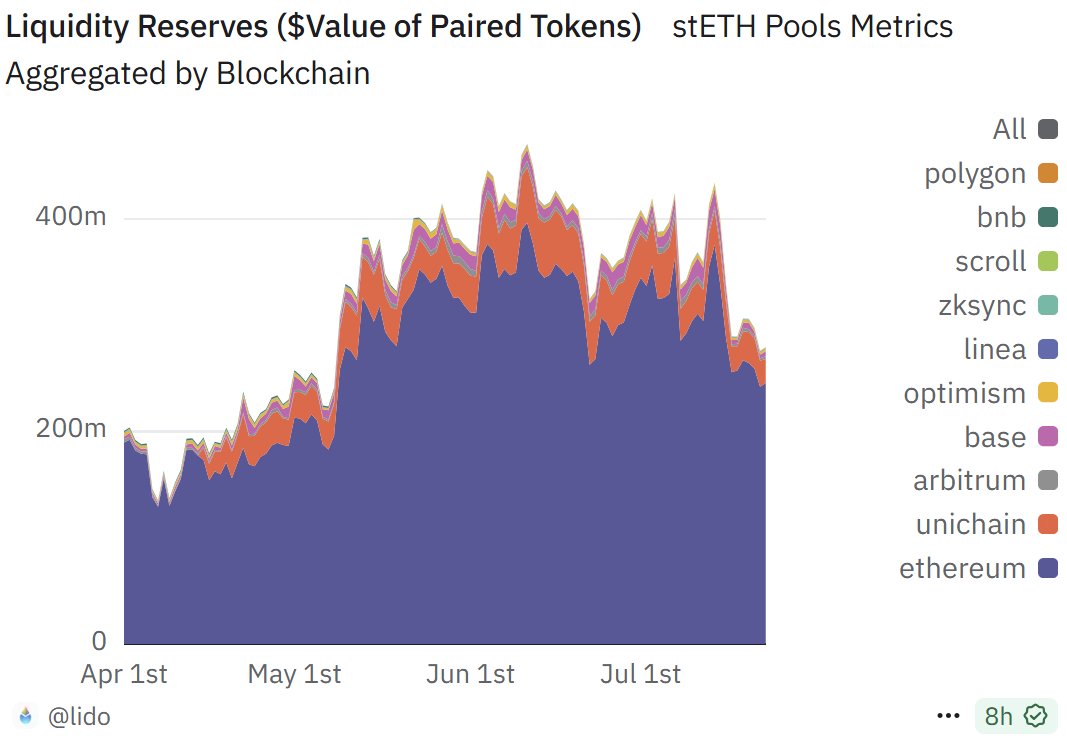

The by far largest LST is Lido stETH, with 86% market share. It has a TVL of $39b, however, it has only $450m in AMM liquidity.

A fraction of this liquidity can be exited at once without moving prices. As a result, only 10-20m$ can realistically exit through the AMM at any one time without creating meaningful price impact. The reason stETH is price stable, is because there is significantly more liquidity depth through secondary mechanisms that rely on peg arbitrage. Let’s dig into the arbitrage economics supporting LSTs like stETH.

Understanding peg arbitrage and secondary liquidity

If stETH trades at call it 0.99 ETH, you can effectively buy 1 ETH for 0.99 ETH, subject to the duration risk of waiting for the stETH to pass through the validator exit queue. Today, the queue is 45 days, which means if you would buy stETH, exit it and redo this trade, you are earning roughly an 8% APY. If the queue doubles again to 90 days, the APY will be 4%. There is a significant amount of capital on the sidelines looking to harvest this yield by purchasing depegged stETH to perform this arbitrage, assuming the implied yield is high enough.

If we assume the hurdle rate for arbitrage funds to lock their capital for 45 days is roughly 12% today, the true price floor of stETH is 0.985 ETH at current queue levels. Currently stETH is trading at a premium to this floor, however, I believe this is largely due to systematic inflows due to the space being in the latter stages of a major bull market. If inflows turn meaningfully negative, especially in the presence of a few major liquidations/unwindings, I believe we will start seeing stETH trading closer to it’s arbitrage related price floor. The larger the queue becomes, the more vulnerable stETH becomes to a depeg.

After ETH staking withdrawals were enabled, stETH has not meaningfully depegged, however, prior to this point it saw major peg instability with stETH depegging about 6.5% at it’s peak. Today’s environment is like a blend of pre-withdrawals (long duration risk) and the past two years where the duration risk was 1-5 days.

Each time a stETH sell order hits the market, this drives down the peg and triggers arbitrage through validator exits, which increase the queue size. The longer the queue becomes, the lower the implicit arbitrage yield whilst simultaneously increasing the position illiquidity for an arbitrageur, which increases the illiquidity premium that lowers the implied peg floor. This can become a vicious cycle.

How big can the queue get?

Based on the rate that validators can exit, if for example an additional 10% of validators exit (3.56m ETH), the queue grows by an additional 62 days to reach a 107 day delay. If 20% would exit, the queue approaches 169 days, almost half a year of duration risk, similar to the duration risk of holding stETH in late 2022 when withdrawals were 4-5 months away from being implemented and stETH traded consistently 100-200 bps below peg.

As we can see, the exit queue could meaningfully inflate in an unwinding scenario, which subsequently will have very meaningful impacts on the duration and liquidity profile of LSTs and LRTs. Now let’s dig into why this is so critical for DeFi and the potential contagion which may ensue.

Unwind triggers and vicious cycles in DeFi

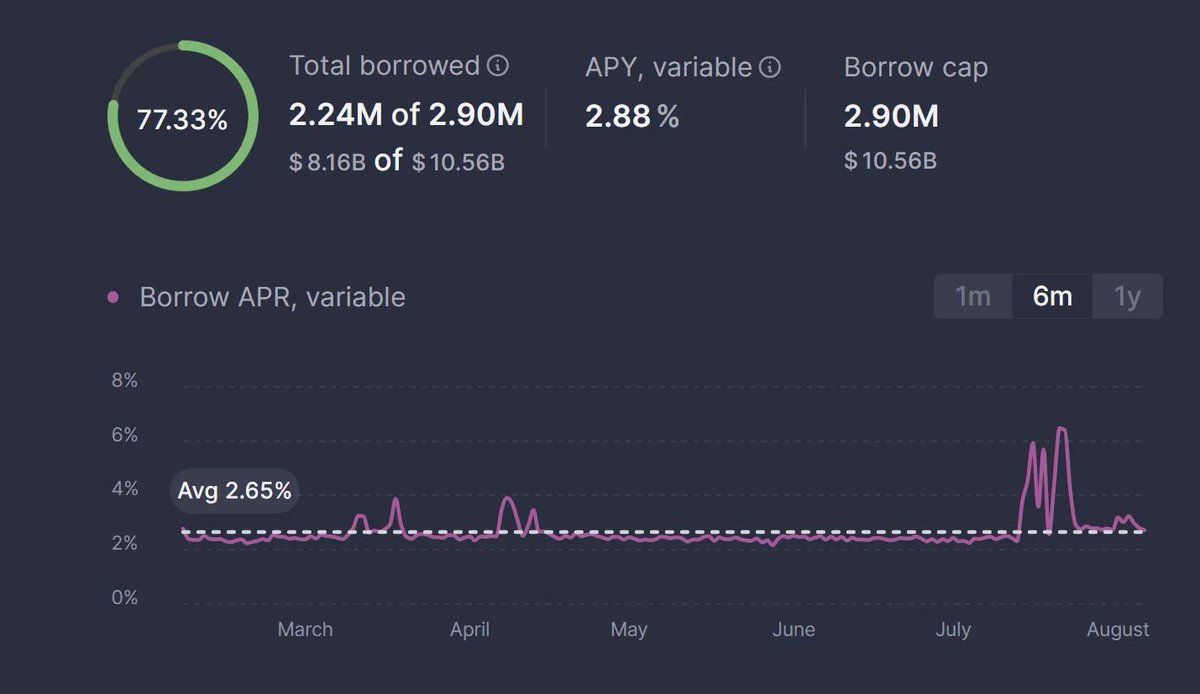

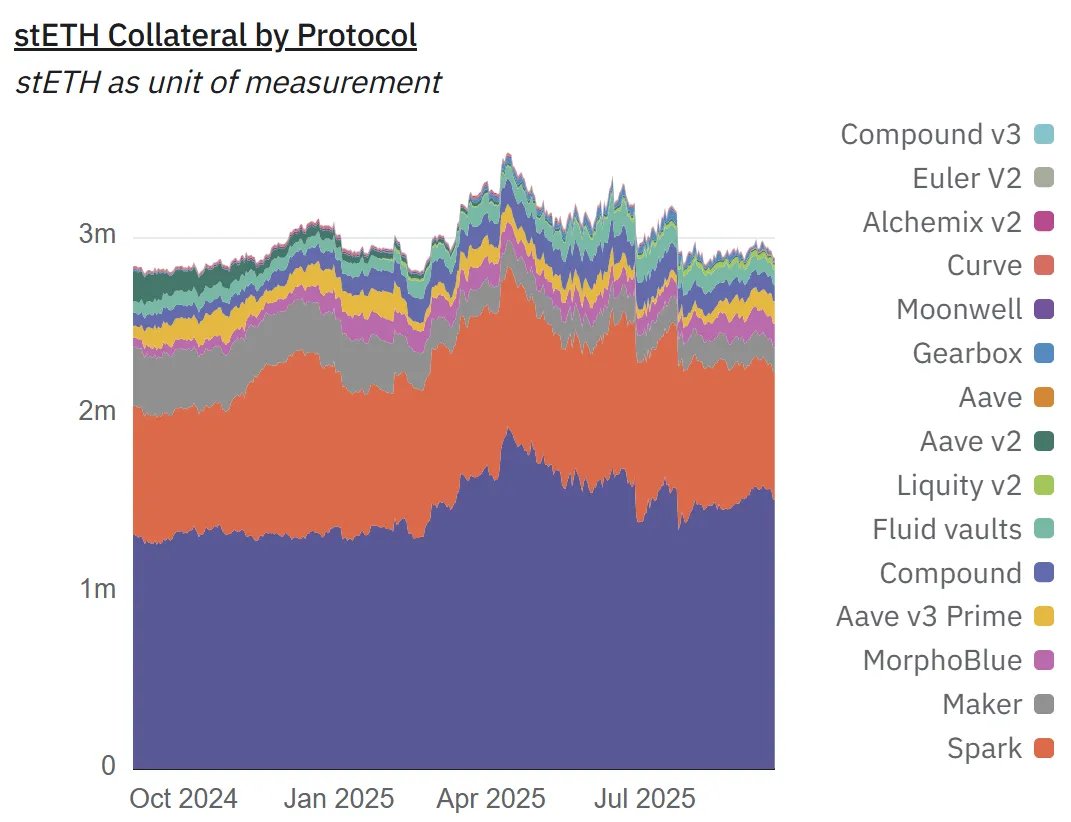

LSTs and LRTs are the largest collateral types in DeFi. Lido stETH alone is responsible for about $13b of TVL, largely across Aave V3 and Spark.

The use of LSTs in lending markets is largely driven by the looping/carry trade. Users deposit stETH or other yield bearing ETH LSTs/LRTs to borrow ETH. This ETH is used to buy more stETH which is used to again borrow ETH. Because the ETH borrow rate is generally lower than the stETH yield, each loop increases yield, as long as the borrow rate does not spike. On Aave the Loan To Value (LTV) ratio that loans can be taken out at is 93%, which enables a high degree of leverage. One can question if this LTV parameter shouldn’t be updated based on the withdrawal queue growth.

As a result, much of the ETH on Aave is lent out to this looping trade. If for example the market environment suddenly shifts, such that many ETH holders would like to rotate out of their positions (eg another Terra/Luna or FTX level event), there will be a significant withdrawal of ETH. However, only a limited amount of ETH can be withdrawn because the majority is lent out. This may cause a run on the bank, where ETH borrowers try to withdraw asap which spikes utilization rates and as a result raises the borrow rate for loopers. Even larger individual fund rotations (such as Justin Sun earlier this summer) can cause borrow rate spikes.

In this scenario, loopers will be deeply under-water for several reasons:

1. They have a levered exposure to the borrow rate, which if it increases, results in levered negative yield which will force an unwind

2. To unwind, they would need to sell their levered stETH on the market. If stETH for example trades at it’s current arbitrage floor of 0.985, this means at 10x leverage you absorb at least a 15% haircut on the initial principal.

3. Because of the high LTV on loops, if trades are not unwound and the negative yield is high, positions will eventually be liquidated. There is nowhere near enough liquidity to absorb major liquidations and loopers will face significant liquidation penalties.

The net effect of any unwind scenario will be a reduction in stETH supply, which puts further pressure on the exit queue and the stETH peg floor.

Impact on vaults

The above scenario of utilization spikes and exit queue growth has meaningful impacts across Vaults. A significant portion of vault yields come from ETH lending market supply and stETH looping related yields. The increased duration risk of stETH means it cannot be quickly exited without a haircut. This would meaningfully complicate the redemption and liquidity profiles of vaults if there were major systemic outflows.

Front-running risks

As we approach the latter parts of the bull market, many funds will start considering their exit path including rotating out of validators and LSTs. The growth of the exit queue fundamentally changes the liquidity profile of any exposure related to ETH staking, in this scenario, you could imagine funds starting to front-run further queue increases by exiting validators such that they have ETH available to sell when the time is right. Is it worth 3% yield to be illiquid for 45 days when prices move 20% per week? Not really. There is a real risk of a self-reinforcing loop where the exit queue as a result grows further in anticipation of further queue growth in a downtrend. I am personally rotating out of LSTs/validators for this reason.

Solutions

There is a clear and apparent lack of tooling to deal with duration risk in DeFi. This issue is not isolated to LSTs, for example duration risk has been a major blocker for longer duration RWAs to be integrated into DeFi to support looping trades. These use cases are specifically why we designed for and built @corkprotocol to provide a market based solution to price and manage duration risk. Cork enables the creation of “swaps” markets that provide an instant liquidity buffer and enable hedging of duration risk. Long term capital providers can absorb the duration risk as a service in exchange for yield, to support instant liquidity for looping markets, vaults and funds.

As an ecosystem, we need to be aware of and adequately manage duration risk. As a collateral type, LSTs and LRTs have varying degrees of duration risk depending on the queue type, and risk management frameworks need to factor these in their assessment of lending market and vault designs. If an asset goes from 1 day duration to 45 days duration, it is no longer the same asset. For example, oracles should have a discount factor based on duration (similar to how Pendle PTs are valued), as opposed to solely looking at the fundamental backing of stETH. I have written a longer piece on duration risk here for those curious:

https://t.co/Da4rpj2ffw

Since LSTs are fundamentally a useful and systemic infrastructure to DeFi, we should consider making upgrades to the throughput of the exit queue. Even if we increased throughput by 100%, there would be ample stake to secure the network. DeFi is one of the biggest use cases of Ethereum and as recently argued by Vitalik - a major driver of economic security.

https://t.co/5PEBAyJJ8W

This minor tweak would boost the quality of the biggest collateral type in this ecosystem, which as a result may strengthen it’s economic security.

So far we have not seen any major depegs of LSTs/LRTs from the exit queue growth, but this doesn’t mean they are not highly susceptible to a depeg in current conditions. If the inflows and uptrend reverses, we are at risk of seeing real unwinding occur. It is only in such scenarios, that duration risk truly rears its ugly head, when liquidity dries up and everyone tries to exit. As an ecosystem we need to be ready to weather storms, because if one thing is for sure it is that another storm will come. It is only a question of wen.

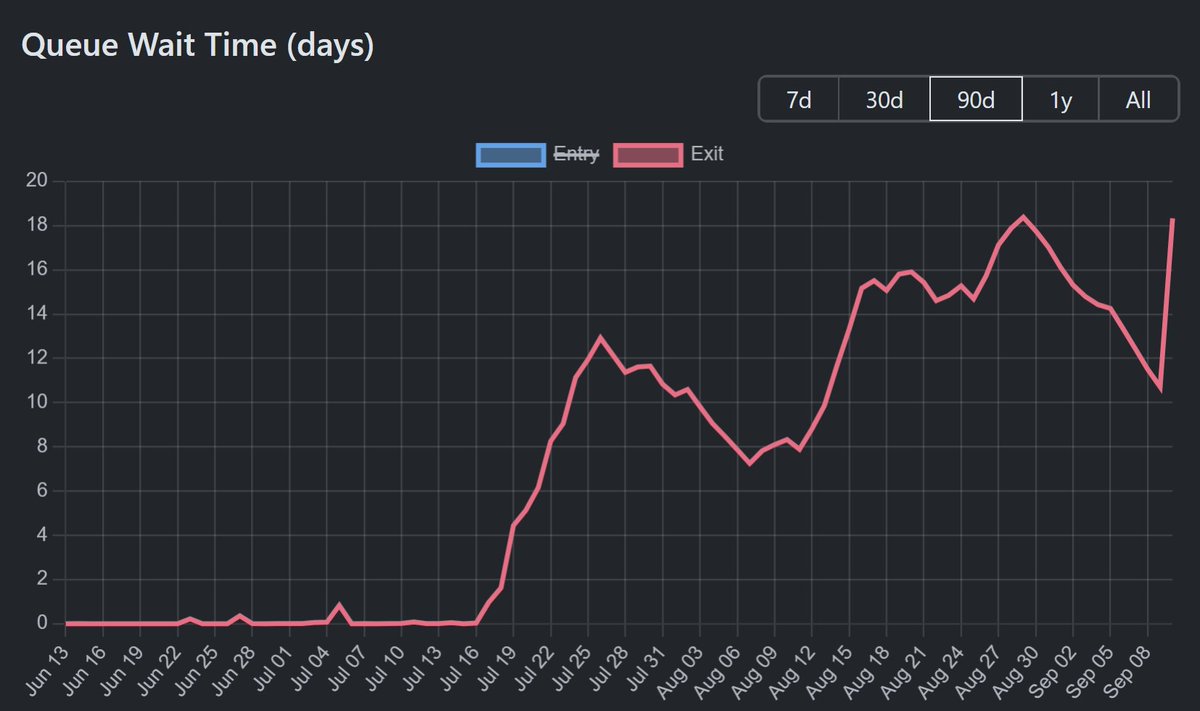

As the validator exit queue reach new all-time-highs, it is time for us to re-underwrite the duration risk and liquidity profile of LSTs/LRTs

Recently @Kiln_finance rotated 700k ETH and are about to rotate another 900k ETH for security reasons. This results in continued exit queue growth, which may cause further unwinding and rotations

This has clear effects on the viability of LST/LRT looping trades as well as LST/LRT rehypothecation and their use as a collateral asset. The depth of liquidity of these assets is meaningfully different at a 1 day exit queue vs 18 day vs 30 day. This impacts their quality as collateral for lending markets, bridges, AMMs.

So far LSTs have sustained only 20-50bps depegs as there is an ample number of arbitrageurs that keep the pegs afloat. At a 50bps depeg, the withdrawal queue arbitrage is only about 10% APY (ignoring fees), if the queue grows to 30 days, the APY declines to 6%. This is below the hurdle rate for many arbitrage funds, especially considering the illiquid nature of the strategy due to the duration risk.

It is in environments like this, when duration risk rears its ugly head, that we need swap facilities and liquidity buffers. This is why we built @Corkprotocol to help support capital allocators, institutions, protocols and vaults to manage duration related risks, by providing instant liquidity facilities to assets with duration risk.

The net effect on ETH of the validator queue growth is largely neutral as mostly of the ETH that is exiting is rotating into the entry queue which is also at an all-time high.

As these queues continue to grow, we are entering a new territory as it relates to LST/LRT duration dynamics and it will be interesting to see what impact it has to their composability in DeFi - I will continue to track it.

See my original thread on how the queue growth initially started and a deep-dive into the mechanics:

https://t.co/d0IgP1tsfO

For more content relating to risk management in DeFi please give @robdogeth, @TheRealStone@Philfog, @talkintokens a follow 🫶

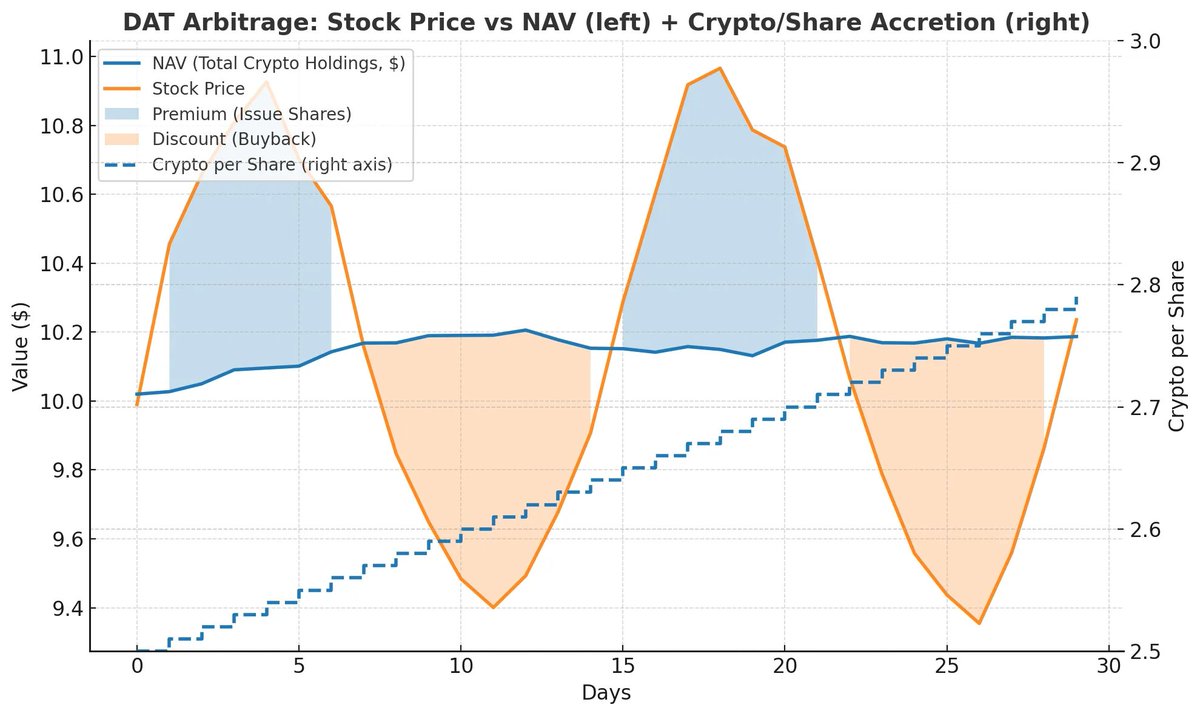

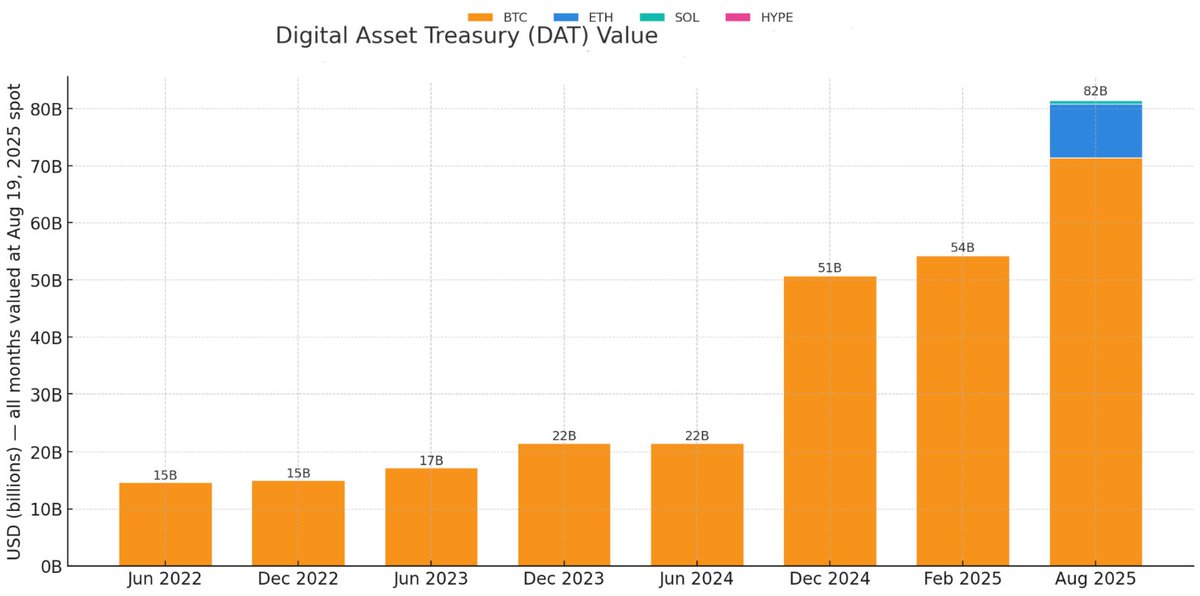

Why is everyone launching Digital Asset Treasury (DAT) companies?

Let’s explore the fundamentals of the DAT model and why it is a beautifully orchestrated arbitrage ponzi that has accumulated over 80b$ of crypto assets 👇

The arbitrage method

The core objective of a DAT is to increase the crypto holdings per share. For existing shareholders, this means you receive a “yield”. For example SharpLink Gaming increased their “ETH Concentration” per share by 94% in about 3 months. How did they do this?

The way this yield is achieved is through arbitrage of the Net Asset Value (NAV) relative to market cap. If the $SBET NAV per share is 10$ but the stock price is 15$, the multiple of NAV, often referred to as “mNAV” is 1.5.

When the mNAV is above 1, there is an arbitrage opportunity the DAT can perform by issuing new shares and selling these At The Market (ATM) and buying crypto with the proceeds. This increases the crypto holding per share as long as mNAV is above 1.

When you buy a DAT share, you are thus betting that the stock will continue to trade at a premium, such that you may continue to benefit from the arbitrage. This is one reason why DATs are a form of sustainable “ponzi game”, because it is the expectation of future buyers continuing to keep the mNAV inflated, that makes the trade profitable to begin with. The earlier you enter the trade and the longer the stock trades at a premium, the larger the crypto yield.

Downside scenario

Now calling this a ponzi game makes it seem like the whole enterprise will collapse if the buyers stop flooding in, which is NOT the case with DATs. What happens when inflows are surpassed by outflows? If the stock is trading below the NAV, (mNAV below 1), stock buybacks that effectively do the inverse of stock issuance, are executed to further increase crypto per share. Buybacks can be funded by selling crypto holdings or leveraging cash on hand. This further produces yield for DAT shareholders, making the arbitrage accretive on both the upside and the downside.

DAT Permanence

A key idea of DATs is that they will be long term buyers and holders of crypto that will not sell in a downturn. I would contest that notion. As Charlie Munger famously said, “show me the incentives and I will show you the outcomes.” - DATs have a fiduciary duty to increase shareholder value and selling crypto to buyback shares when they are trading below mNAV of 1 is the optimal strategy to maximize crypto per share, which is the purpose of the vehicle. For example Tom Lee’s Bitmine Immersion has already authorized 1b$ of buybacks to be performed in response to BMNR trading below mNAV of 1.

Michael Saylor has stated Strategy will not sell their holdings even if there is a discount to NAV. Because of dilution, Saylor doesn’t have voting control of Strategy anymore, so I suspect shareholder incentives will decide the outcomes in the end, which would indicate dumping of BTC in a downturn to perform buybacks.

The blowup risk

The only real blowup risk in DATs stem from the use of leverage. None of the ETH DATs currently deploy any leverage. The use of leverage can further increase crypto per share without dilution, however, the cost basis begins to matter for purchases using leverage. If you borrow $ to buy ETH and the price of ETH drops, that’s a loss that all DAT shareholders will have to absorb. In the inverse scenario, profit accrues to shareholders. Only Saylor’s Strategy has meaningful leverage (5.2b$ non-converted debt, 3.95b$ preferred stock). As the market reaches the later stages of the bull market, my only worry is that DATs begin to lever up at the wrong time and go deeply under-water as a result. This could nuke crypto prices in a bear market, similar to the unwind of 3AC or FTX. However, we are yet to see this and several of the ETH DATs have expressed very conservative views on the use of leverage.

Future of DATs

I believe we will see the proliferation of DATs across many tokens and possibly other commodity markets (eg gold) with limited supplies. On some level, a DAT is a form of “token IPO”, which opens access to crypto exposure for new pockets of capital such as mutual funds, certain ETFs and wealth advisors. Whilst many blue chip tokens will likely launch ETFs in the future too, there is a broader set of tokens which will have DATs. Already today HYPE, ENA and SOL have major DATs, each with hundreds of millions in holdings.

From first principles, having broader market access is positive part of the trend of crypto and traditional finance rails merging. Whilst these vehicles push short term buying pressure, they likely are not long term fundamentally altering the value of the tokens held. Whilst a token being more widely held and liquid across more venues may add some premium, ultimately it is the underlying protocols and networks’ actual adoption which will determine the success of the tokens over time.

In the short term, the market is a voting machine, in the long term, it is a weighing machine. DATs bring many votes, but they don’t bring real weight. Heavy is the protocol with a strong product and network effect. Let us not forget why we are building the future of finance.

If you enjoyed this analysis, consider giving @robdogeth a follow :)

A deepdive into duration risk: the fundamental cause to the current stETH looping unwind and a major obstacle to the scaling of looping trades including RWA adoption in DeFi

What is duration risk?

Duration risk is the risk that the market value of a fixed‑income‑like position will change when the discount rate used to value its future cash flows changes. Practically what this means is that if you hold a bond and risk free rates change, the value of your bond decreases. The longer the maturity, the larger the value decrease is. In crypto, the relevant rates are not just short-dated T-bills, but also the USDC/USDT borrow rates on lending markets.

In crypto, duration risk rears its head largely as a result of major market shifts which drive rate changes and large redemption volumes that combined can cause significant losses. A good example is the wstETH:ETH looping trade unwind. In July 2025, positive price movements drove up the borrow rates across lending markets. Loopers were rate arbitraging the delta between the stETH yield and the ETH borrow rate on @aave, by depositing wstETH as collateral to borrow ETH which is used to buy more wstETH which again is deposited as collateral in a loop. Because wstETH loopers receive a relatively stable rate of yield, but are exposed to variability on the borrow rate, effectively loopers are short duration. When borrow rates spiked, there was a looping unwind that caused the validator exit queue to grow to 12 days which caused a depeg of stETH.

As a result, loopers were stuck for a while holding negative rates or exiting into a depegged stETH market. This is an excellent example of how duration risk can unfold and wreck looping trades, because even just a 12 day increase in exit duration in the context of borrow rate spikes caused major market turmoil and significant losses. At the time of this writing, we have a second leg to this unwind occurring, I encourage you to read my initial lengthy explainer which dissects the exact mechanisms and math behind the unwind.

https://t.co/d0IgP1sUqg

Another angle to duration risk, is the management of duration mismatches. A Vault offering a 1 week withdrawal window with assets across strategies with a 2 week redemption duration could face temporary liquidity crunches due to the duration mismatch of their assets and liabilities, often necessitating cash buffers that lower capital efficiency. Another example is if a bridge rehypothecates deposits into vaults, such as the case of the @katana VaultBridge which deposits funds into conservative @MorphoLabs Vaults, they may face duration mismatch challenges. The challenge arises from the high utilization in Morpho Vaults (often 90%), which means only 10% of bridge funds are available for instant withdrawals. Whilst there is no real question on fund safety, this could cause real UX issues during volatile periods which may hurt some level of composability.

Fundamentally duration presents a challenge to DeFi composability, as it affects liquidity guarantee of yield bearing strategies. Organically to receive yield, capital often has to be locked up for a duration of time. The ecosystem is seeking to tokenize and embed these yield streams into financial products, which is one of the superpowers of DeFi, however, in the process this design pattern exposes users to duration risks during periods of market volatility. If DeFi cannot handle duration risk, it cannot absorb the vast majority of capital in credit markets which involves significant duration exposure.

Duration in RWA Looping Trades

A form of RWA looping trade is the stablecoin basis trade loop, where USDe or sUSDe is used as collateral to borrow USDC or a similar stable, to leverage rate arbitrage between the USDC borrow rate and sUSDe yields. At the time of this writing, there is 6.2b$ of sUSDe, USDe and their relevant PTs on Aave alone, which is driving yield and utilization across their stablecoin markets. USDC and USDT have a borrow rate of 5%, whilst @ethena is currently yielding 11%, providing an attractive rate arbitrage for loopers. In a sense, Aave is providing a low cost of capital at scale for the Ethena basis trade to be scaled up and down to match demand for perps.

In the case of Ethena, there is a relatively immediate redemption window and as such, the duration risk is quite minimal. However, to support this redemption profile, Ethena also must limit it’s collateral to immediately liquid sources, this explains the relatively minor exposure to stETH due to the exit queue duration risk. Likely, if Ethena rates would drop relative to the borrow rate on Aave, we will see a major loop unwind that will stress test the system. The result will be a significant Ethena TVL contraction, borrow rate volatility on Aave and likely a minor temporary depeg on USDe. Due to the short redemption window on USDe, the peg can quickly be arbitraged back up, but such an event would further battle test the ability of Ethena to rapidly process billions in redemptions.

Illiquid RWAs

What happens when we do the equivalent trade without immediate redemption windows or liquid secondary markets? Currently there are efforts to perform looping trades using traditional credit funds. Many offchain credit funds yield 9-12% with relatively conservative risk ratings. If these can be levered up through rate arbitrage similar to Ethena, this would present a major opportunity to drive a new sources of organic yield and expansion of credit instruments in DeFi. Such a market structure is being experimented with, for example the @Securitize Apollo Diversified Credit Securitize Fund (ACRED) on Polygon which has 1b$ of AUM (100m$ onchain) is available as collateral on Morpho. This is a novel market yet to properly scale, but an exciting proof of concept of what is to come. Whilst ACRED yields 9%, it can be looped at a 3.6% borrow rate, providing an attractive rate arbitrage opportunity.

However, there are two major duration related challenges for ACRED or other RWAs in scaling the looping trade:

1. The redemption window is often relatively long. For example ACRED has a quarterly redemption offer with a 21-42 day redemption window.

2. There is no liquid secondary market, finding a buyer to OTC offload can take many weeks.

In this context, loopers using ACRED or similar RWA style instruments, even with only 1-2 week redemption windows, face significant duration related risk. If rates flip such that the loop becomes negative ROI, how will the looper unwind their trade? If the trade is at 10x leverage, even a 3% negative APY for a month would amount to a 2.5% impairment of the collateral, a significant loss for a “fixed income” exposure. Furthermore, it creates some level of illiquidity risk for depositors on the lending markets, as it may not be so easy to liquidate positions when needed which may push lending markets up to full utilization in times of outflows, again resulting in further pain from rate volatility. This duration related risk not unique to looping, it affects any use case where RWAs are used as collateral. Solving duration risk for RWAs is a major challenge preventing their use in DeFi.

How to solve duration risk for RWAs

To tap into the cheaper cost of capital of onchain lending markets, RWAs need liquidity facilities that mitigate their duration risks. One novel method for solving this is @Corkprotocol , which offers the ability to set up markets where a Reference Asset (such as ACRED) can be immediately swapped for a liquid Collateral Asset such as sUSDS. This serves as a swap line or instant liquidity facility. The facility solves the duration issue and enables an underwriter of the facility to earn a premium from providing coverage of the duration risk, introducing a new DeFi native yield source. This solution has the potential to significantly change the risk profile of RWAs or other semi-illiquid yield bearing assets that take part in the lending market rate arbitrage game. In the same way Aave has driven 6.2b$ of USDe supply through it’s rate arbitrage game, likely the RWA rate arbitrage if designed correctly could meaningfully scale the size and opportunity of onchain lending markets and the TVL of RWAs in DeFi.

Cork will soon pilot the first markets where the facility is solving duration mismatch/risk use cases in DeFi which may unlock a meaningful new category of yield and arbitrage opportunity.

Duration risk in DeFi is real as we can see by the stETH looping unwind, and as an ecosystem we need better tooling and strategies to understand, manage and overcome this risk. Risk management is the new frontier, as DeFi prepares to accept trillions flowing from traditional financial rails.

If you appreciate the analysis please leave a comment & give a follow for more insights: @robdogeth@TheRealStone@Philfog

Significant media about the ETH validator exit queue being negative for the ETH price

They completely miss the point that this is driven by the unwinding of the stETH looping trade which is neutral in ETH/USD terms

Everyone loves a fabricated bearish story on a down day

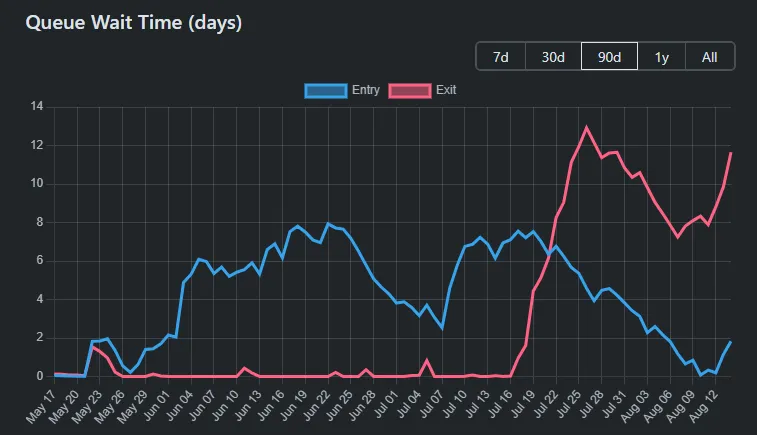

stETH is experiencing a sustained depeg - let's dig into the mechanisms driving it and how the great stETH looping unwind is playing out

stETH is a liquid staking token by Lido, which dominates it's category and is considered an exceptionally safe token. So why is it depegging? It all relates to the mechanisms to arbitrage it's price and surrounding market structure/leverage in the system. Let's dig in.

Core factors impacting the stETH peg

Let's first look at liquidity, stETH has about 280m$ of available AMM liquidity. Whilst 280m$ seems like a lot of liquidity, we have to consider the token has about 33b$ of TVL and only a fraction of 280m$ can be tapped at a 1:1 price with ETH.

As such, liquidity depth supporting the stETH peg price is driven largely by it's redemption mechanism. Users can redeem stETH 1:1 for ETH, which triggers ETH to be withdrawn from the validator set. However, there is a limit to how many ETH validators can simultaneously exit, per block. Most of the times this queue is negligible, however, in periods of large outflows of stakers, this queue can grow. In the past week, it went from 0 days to currently 9 days and growing.

This has a critical impact on all liquid staking tokens, with an outsized impact for tokens that are widely levered up. Because stETH was relying on the redemption mechanism arbitrage to keep it's peg at 1, the growth of this validator queue makes the token increasingly susceptible to outflows. Currently, stETH is only depegged by 50-60bps, however, with leverage that amount adds up. 60 bps also represents almost a quarter of yield accrual in stETH.

The arbitrage math

Arbitrageurs can capture this discount by purchasing stETH and waiting 9 days in the validator queue to perform a redemption, this is always what is holding holding up the peg. The annualized yield of this strategy with a 9 day delay is 25%, which considering the low risk of the strategy is fairly profitable. However, this highlights the clear relationship between the peg and the exit queue. If the rate at which that market will lock up capital to perform this redemption is 25% APY, it means the longer the queue gets the larger the depeg will become. If the queue becomes 18 days instead of 9, the arbitrage take rate becomes a 100-110 bps depeg. If the queue is 0 days, the rate is closer to 0-10 bps which is where stETH usually trades. This is a clear example of the relationship between asset liquidity profiles and their respective prices, which we see time and time again cause depegs due to duration mismatches, for example the Usual USD0++ depeg had a similar dynamic.

Leverage and Justin Sun

Now with a grasp of the fundamental mechanism backing the peg, what caused this outflow and resulting depeg and exit queue? The short answer is Justin Sun. Justin, and many others, have played a game of leveraged stETH yield farming, where stETH is deposited as collateral, to borrow ETH, to purchase more stETH which is again used to borrow ETH in a recursive loop. This market on Aave alone was capped at 7.6b$ or 1.76m$ stETH. Justin was unwinding and repositioning a major stETH looping position (450k ETH reportedly), which resulted in a major spike in outflows which had drastic impacts on the utilization rates and APYs on Aave. It is likely that prior spikes in utilization, driven by demand for leverage due to the bullish price action already made the looping trade unprofitable which triggered the rebalance. Either way, high utilization rates on ETH borrow is forcing stETH loopers to unwind or absorb negative yield on high leverage.

The Unwind

To understand why these positions must unwind, we can take an example for a regular stETH looper on 10x leverage. If stETH is yielding 3% and your borrow rate on ETH in the past 14 days is on average 8%, you are absorbing a roughly 50% negative APY. Across a 14 day time-period, you are eating a loss of 1.91%. That is a massive loss for a safe low-yielding trade. There is no guarantee that utilization rates will go down for ETH because of how bullish price action has been. So for loopers in need of an unwind they are faced with three options:

1. Unwind on the open market, absorb 50-60bps on each loop (5-6% total loss)

2. Exit through the validator queue, 9 days on each loop so 90 days total if the queue remains constant, whilst you absorb negative APY during the exit period

3. Hodl and keep absorbing negative APYs praying that utilization rates on ETH drop

These guys thought the stETH looping trade was free money and now they are stuck between a rock and a hard place. What was the saying about free lunch again..?

Path forward

This is starting to look like the beginning of a major leverage flush tied to stETH looping. I personally expected this to happen at some point, I wrote a blog post on this in late 2023 based on which the initial design for @Corkprotocol was conceived to help address liquidity challenges like this one. Whilst loopers will likely get hurt in this process, that's the game they play. No crying in the casino. I am very curious how the unwind will unfold, but moving forward I hope we think more closely through the market design behind some of these looping trades and incorporate better risk management into the playbook of such trades. I am excited to be building out risk toolkits at Cork, such as slashing, depeg and slippage covers which programmatically could have protected loopers in these market conditions. This could have avoided this nasty fallout from an otherwise clean method of rate arbitrage which looping represents. Moving forward, let's make looping safe again.

If you liked this post and want to follow more deep content on pegs, consider giving a follow to @robdogeth@Philfog@TheRealStone@Corkprotocol

Crypto volatility is a result of it's recursive nature

Regulatory clarity means the recursive loops will now enter institutional scales. Trillions instead of millions

Onchain finance is on the verge of explosive expansion

GENIUS Act needs to address stablecoin risk

As the GENIUS Act progresses with wide bipartisan support, it is looking increasingly likely it will be written into law which would be a huge step forward for the stablecoin and broader crypto ecosystem. However, if stablecoins are to replace banking rails and process $100s of trillions we need to take the "stable" part of stablecoin extremely seriously.

The GENIUS act does help establish stability through:

1. Requiring immediate 1:1 redemptions

2. Backing by cash or cash equivalent assets

3. Bankruptcy remote structure requirement

This is a step in the right direction but the bill does not prevent defaults or major price deviations from occurring in regulated stablecoins. These events can unfold through a variety of unaddressed risks:

1. Smart contract related risks

2. Custody failure risks

3. Temporary depeg risks due to volatile flows

Whilst GENIUS Act is a welcomed step towards regulated stablecoins with relatively safe designs, as an ecosystem we cannot ignore that even these lower risk stablecoin designs are not risk free.

For stablecoins to be the backbone of commerce globally, regulatory frameworks need to adequately address these risks. It would further be useful to extend risk tooling towards stablecoins and perhaps mandate certain levels of coverage against risks unfolding that could permanently impair the value of these stablecoins.

Because it is only if stablecoins are truly stable, that they will win.