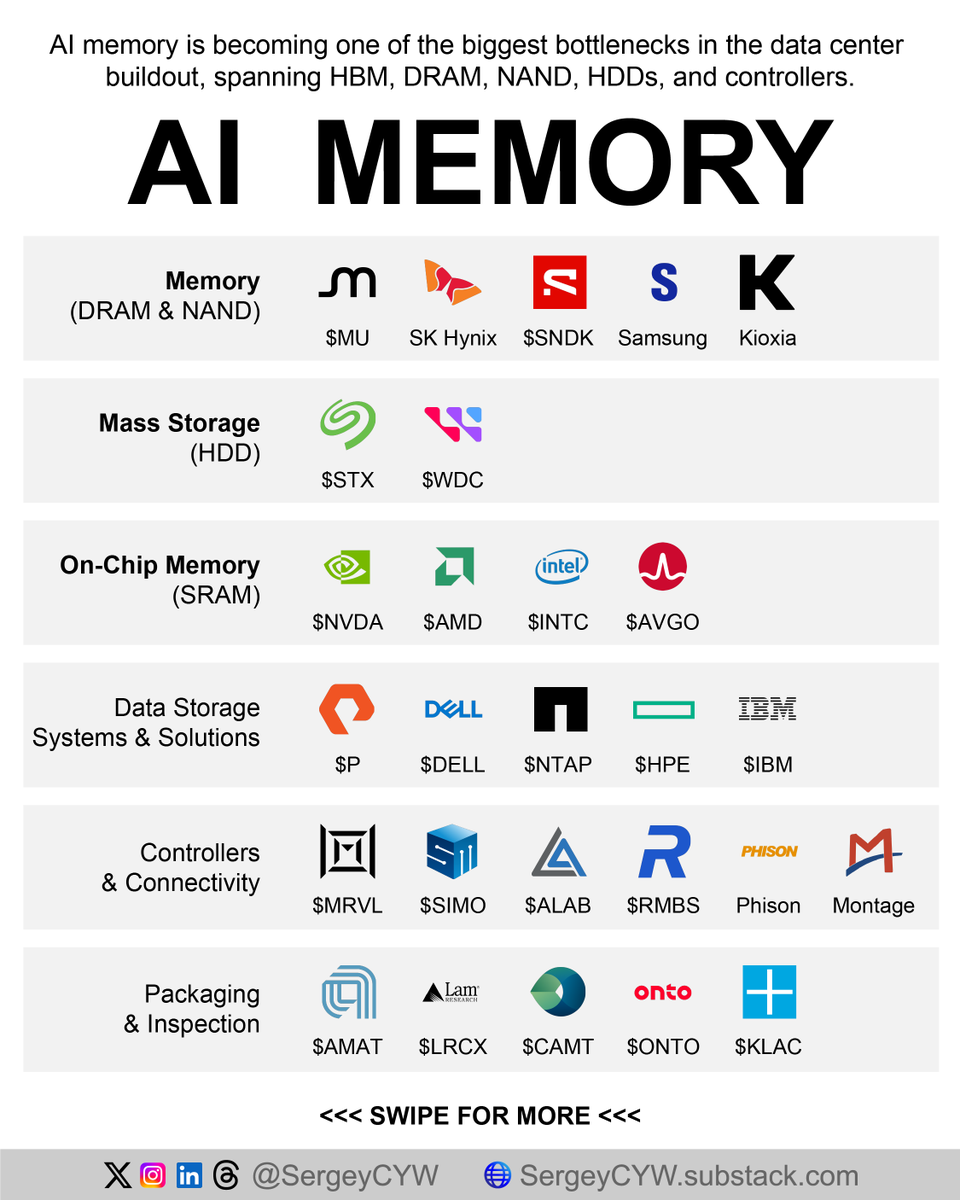

AI memory is becoming the real bottleneck behind the data center buildout.

Morgan Stanley calls memory “THE bottleneck” in AI, while Goldman Sachs flags memory, power, and labor as key physical constraints. Agentic AI, larger KV caches, multimodal workloads, and longer context windows are pushing demand beyond GPUs into HBM, DRAM, NAND, HDDs, SRAM, controllers, storage systems, and packaging tools.

Layer 1: DRAM & NAND

Core memory suppliers sit closest to the AI capacity shortage. HBM feeds accelerators. DRAM supports servers. NAND supports fast retrieval, inference storage, and active AI data pipelines.

$MU Micron: Micron is the U.S. pure-play memory supplier across HBM, DRAM, NAND, and SSDs. Its 12-high 36GB HBM4 moved into high-volume production ahead of schedule, while customer agreements cover HBM capacity through 2026. HBM4E base dies also shift to TSMC, strengthening advanced foundry integration.

$000660(.KS) SK Hynix: SK Hynix remains the key HBM supplier for Nvidia platforms. The company started full-scale 1b DRAM production for HBM4 and added 40,000 wafer starts per month at M15x. Its base-die transition to advanced logic nodes supports the 2048-bit interface needed for larger AI models.

1. TrendForce: AMD has started scrambling for high-power CW lasers.

2. TSMC insiders: CW lasers are sold out everywhere. 🤯

Everyone knows about $LITE and $COHR…

But I happen to know a tiny Taiwanese company that’s probably one of the purest $MRVL suppliers, also shipping CW lasers, and management expects revenue to grow ~4x this year.

Do you know who it is? 👀🍿

https://t.co/tSf7dUqCoI

📈 포트폴리오 1 - 장기투자(1년 이상) 목적

1. $IREN - AI 데이터센터 전력 인프라 수혜주(5.8GW 확보)

2. $RKLB - 우주, 방위산업 수직계열화 완성(피터벡❤️)

3. $TSLA - 로봇 + 자율주행, 피지컬 AI 최대 수혜주

4. $IONQ, $INFQ - AI 다음 거대 흐름은 양자컴퓨터

모건스탠리는 삼성전자가 내년에 글로벌 기업 가운데 이익 1위가 될 것으로 전망했습니다.

반도체 소부장 관련주, 삼성전자 핵심 공급사 Top10

1. 원익IPS (반도체 증착 장비 핵심 공급사)

2. 동진쎄미켐 (감광액 및 식각액 핵심 공급사)

3. 솔브레인 (감광액 및 식각액 국산화)

4. 비에이치 (스마트폰용 연성회로기판 공급사)

5. 에스에프에이 (공정 자동화 설비, 물류장비 공급)

6. 파트론 (갤럭시S, A 카메라 모듈 핵심 공급사)

7. 하나마이크론 (반도체 후공정 패키징)

8. 심텍 (반도체용 연쇄회로기판 공급)

9. 대덕전자 (고성능 반도체 기판)

10. 한솔케미칼 (반도체 세정용 과산화수소, 퀀텀닷)

Some napkin math on $AAOI:

> Management explicitly told you that their mid-2027 target is $471M transceiver revenue - that's $5.65B annualized just from their 100G/400G, 800G and 1.6T lines.

> The biggest risk is management doesn't achieve this (it is ultimately a huge ramp, but one they've raised capital for). But if they do, that puts AAOI at roughly 2.4–2.9x P/S at today's market cap. That is stupid cheap compared to larger optical peers: Lumentum trades around 15x FY2027 sales and Coherent around 8x FY2027 sales.

> CPO laser also sits on top as a free option (GS already predicts this will reach ~$100B in 2028).

> $AAOI (pluggables) will be a big beneficiary if CPO is delayed as Semi Analysis argues in their CPO report.

I think $AAOI, while not without risk, presents great risk to reward. NFA - I am long.

Full analysis below, including my take on the "risk" that management is unable to succeed in ramping production.

Everyone needs to think about buying $AAOI shares!

Huge opportunity - EVEN beyond 2028.

I'm not joking or hyping. Read this...

> Raymond James ($300B AUM) analyst reiterated an outperform rating for the company a few days ago, following his meetings with their CFO. The company increased also their stake by 93% in Q1'2026.

> Monthly production capacity by mid-2027 to more than $450M, which implies an annual revenue of ~$6B by 2028. Raymond sees it as a realistic bull case.

> Company believes it could gain market share from chinese competitors due to geopolitics, with Innolight being added to the 1260H list (identified as chinese military company) by U.S. DoD. 2027 looks like the year when it becomes clearer.

> Beyond 2028, the upside still exists, with CPO adoption through their ELSFP modules & lasers. Capacity increase today holds them even steadier for the next cycle.

> Raymond analyst Leopold mentions opportunities extending beyond $NVDA, with $AMD and $AMZN being recognized too.

So...

The story keeps getting better for $AAOI. Independent of the timelines for CPO. Initially I was skeptical due to their transceiver business being the main theme. That is why I saw it as a 2 year play. But now it certainly looks like they will keep growing beyond 2028, especially with the capacity they are planning to reach. And with the competition, by having a US footprint, $AAOI stands out even further.

PTs: $50-$60B in valuation by early 2028. That is a 4X upside in a year and a half.

Extremely bullish.

$NOK JP Morgan upgrading their PT from $14 -> $21

After Northland Securities upgrading theirs from $13 -> $20

They are starting to catch on finally.

4대 하드웨어병목:

연산, 메모리, 인터커넥트, 전력

1. 연산 (Computation) $NVDA $AMD

주요 역할: 시스템의 핵심인 데이터 처리 및 명령 실행을 담당합니다.

2. 메모리 (Memory) $MU $SNDK SK hynix Samsung

주요 역할: 데이터의 저장과 로딩을 수행합니다.

병목 요인: 데이터 처리 속도를 결정짓는 대역폭(Bandwidth)과 지연(Latency) 문제가 주요 병목 지점이 됩니다.

3. 전력 (Power) $NBIS $BE $IREN

주요 역할: 안정적인 전력 공급과 에너지 효율성을 관리합니다.

병목 요인: 시스템의 성능과 직결되는 열 관리(발열 제어)가 매우 중요한 요소로 작용합니다.

4. 인터커넥트 (Interconnect) $MRVL $LITE $AAOI $COHR $VIAV $CRDO

주요 역할: 시스템 내부에서 데이터를 이동시키는 통로 역할을 합니다.

병목 요인: 서로 다른 시스템(구성 요소) 간의 데이터 통신 과정에서 병목 현상이 주로 발생합니다.

(26.6.11 미래)

< 삼전 벨류는 시작도 안했다 >

지금 엄청난 일이 벌어지고있음.

삼전이 TSMC 사업 일부를 가져온다는거.

전세계 AI칩 생산 전부를 TSMC가 독점하고 있는데

구글같이 추론칩 시장의 파이를 먹어볼라고 하는 기업은

전부 TSMC에 줄서있음.

추론칩시장은 이제 시작 단계로

엔비의 학습칩 시장의 10배 이상됨.

그 많은 물량을 TSMC 혼자 생산해내는건 물리적으로

불가능하고 삼전 팹이 생산해낼거라고

테슬라가 삼전에게 맡겼을때부터 예상됬던 일임.

안그래도 구글과 삼전, 겔럭시폰에 제미나이 탑제로

끈끈한 관계이고 이번에 구글의 스마트 안경 삼전이 만든것만봐도 둘의 관계는 엄청난 공생관계.

소프트웨어 구글 + 하드웨어 삼전.

구글이 삼전에게 차세대 TPU 생산을 맡기는건

정말 예정된 미래였고 그 미래가 확인받음. ㅋㅋ

사실은 이거 내가 평소에 많이 하던 이야기여서

햇제 하고싶은데 ㅋㅋ X에는 처음 써서 할수가 없음 ㅋㅋ

암튼 삼전 주식의 벨류는 시작도 안했다에 한표~! ㅋ