Respected @nsitharaman ji and @FinMinIndia ,

Suggestion 1 of 3 for strengthening India's capital markets:

Long-term capital gains tax on listed equities should be abolished.

A long-term shareholder is not a speculator but a provider of patient risk capital. By investing in and holding businesses, investors help companies expand, create jobs, innovate and contribute to India's economic growth.

India requires enormous amounts of long-term capital to build world class enterprises, infrastructure and global champions. Tax policy should encourage households to move savings from passive assets, including imported stores of value such as gold, into productive businesses that create jobs, generate tax revenues and build national wealth.

The appreciation in a company's value is not created in isolation. During its growth journey, the government already collects corporate tax, GST, income tax from employees, customs duties, stamp duties and numerous other levies. Long-term capital gains are often the final outcome of economic activity that has already generated substantial tax revenues.

Most importantly, tax policy should clearly distinguish between investment and speculation. A long term shareholder is a partner in wealth creation, not merely a participant in market transactions. Tax policy should reward long-term ownership of productive businesses and distinguish it from short-term speculation.

India needs more patient capital, more entrepreneurship and more long term investing. Abolishing long-term capital gains tax on listed equities would be a powerful step in that direction.

Respectfully submitted.

Japan Is Bracing for a Hard Transition

Japan isn’t rolling out a ¥17 trillion plus package because it suddenly rediscovered big government spending. It’s doing it because the country is in the middle of a very delicate shift, moving from a deflationary, low rate world that lasted 30 years into a higher price, higher rate environment that Japanese households simply aren’t built for.

Finance Minister Satsuki Katayama told reporters recently that the package will exceed ¥17 trillion, not just meet it. the intention is to relieve the blow of rising living costs and pour money into future growth sectors like AI and semiconductors, areas Japan can’t afford to lag in as the global economy fractures and supply chains get rewired.

In other words, this isn’t pure stimulus. It’s stabilization. Japan is trying to help households absorb higher prices without forcing the central bank to slam on the brakes, and at the same time fund the industries that must anchor its next decade.

Why This Matters Far Beyond Japan

The U.S. will be watching this closely, not out of curiosity, but because Japan is effectively running a dress rehearsal for challenges the U.S. will face in a few years.

The first thing markets will watch is the bond market. If a package this large pushes JGB yields higher, even modestly, that shifts the global flow of money. Japan is still one of the world’s biggest foreign holders of Treasuries. If returns at home start to look a little better, capital quietly migrates back and that puts pressure on the long end of the U.S. curve at a time when Washington is issuing record amounts of debt.

The second layer is the yen. For decades it’s been the world’s preferred funding currency. If Japan’s mix of fiscal spending and BOJ normalization makes the yen firmer or more volatile, the carry trade unwinds. And when that unwinds, it doesn’t just hit Japan, it tightens financial conditions everywhere. Equities feel it. Credit feels it. Anything that relies on cheap global liquidity feels it.

And then there’s the deeper, slower second order effect. If Japan pulls this off, if it can run a stimulus package greater than $110 billion, keep households afloat, and prevent its bond market from convulsing, it gives every other advanced economy with aging demographics and heavy debt a green light to push fiscal harder. It broadens the perceived safe zone for deficit spending in a world where monetary policy is no longer the main stabilizer.

That’s the real reason this matters. Japan isn’t just trying to manage its own economic transition. It’s showing the rest of the developed world what the next era of economic policy might look like and whether the global system can actually handle it.

Japan is the test case. The U.S. is the audience. And the spillover effects will tell us more about the next decade than the headline number ever will.

@EurekaForbes Extremely disappointed with the ongoing delay in installing my product! Despite multiple attempts, the concerned person isn't answering my calls. This is unacceptable customer service. Please intervene and resolve ASAP, or refund me immediately! #PoorService

Unfortunate that two of most important projects in Maharashtra are being hit by some politicians both in Government and Opposition.

Shaktipeeth Expressway is must along with Pune Nashik IC E-way .

If there is opposition from Kolhapur ,Bypass Kolhapur District but don't cancel it as it would be unfair to other districts and same goes for Nashik Pune IC E-way.

Shameless Politicians still busy in appeasement politics .

@Dev_Fadnavis@Devendra_Office@kdhavse@AjitPawarSpeaks@ghatge_raje@mieknathshinde@CMOMaharashtra

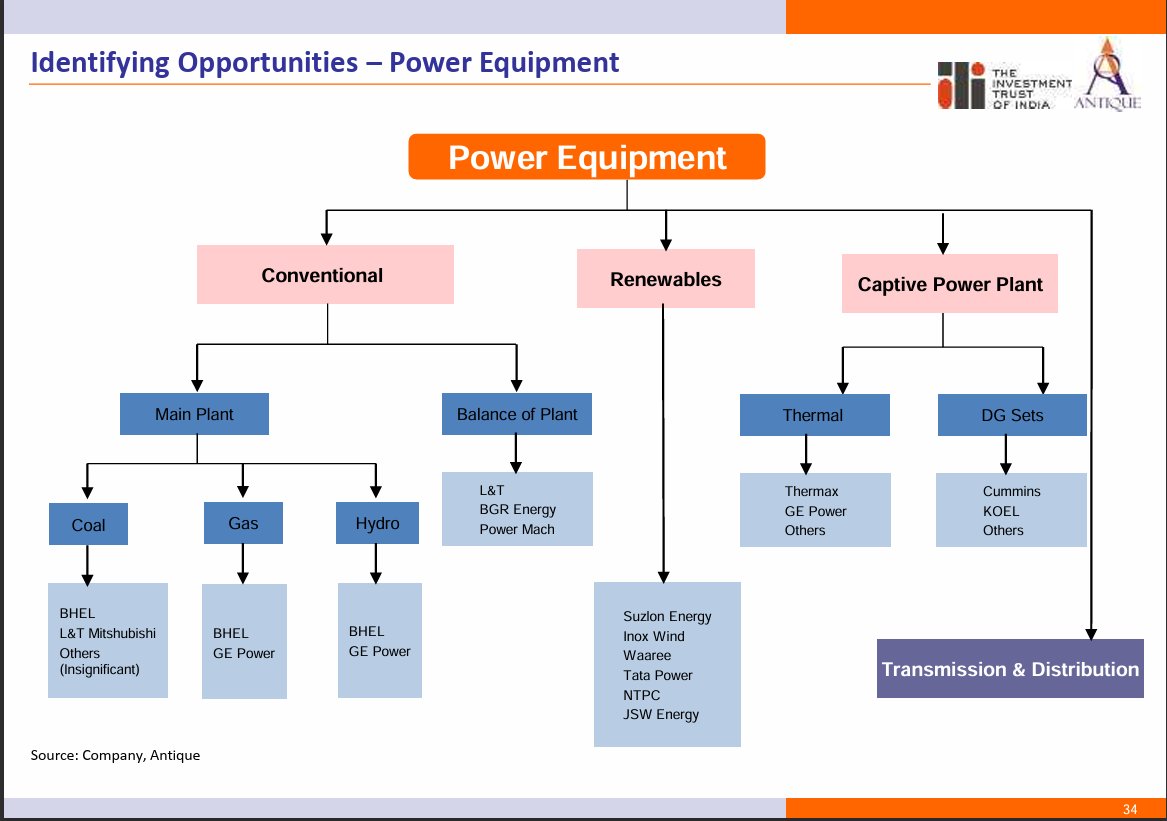

The entire listed power universe has been covered well in these two slides. You may ask your specifc questions in the comments and i ll try to answer them. Please no buy sell recommendations. #Energytransition

My year end musings. A Financial Sector Model for India’s dream: 9% annual growth, $30 trillion GDP by 2047.

India is transforming from a nation of savers to investors. The tussle between the saver/ borrower and issuer/ investor model is underway.

In the early 80s, the Indian saver had low confidence in financial assets versus gold and land. Slowly the saver moved some part to bank deposits, UTI and LIC.

Even in the 90s, investing in equities was considered “speculative”. Hence companies looking for capital went to the foreign institutional investor (FII). FIIs saw potential and bought into companies while the Indian saver stayed away. Companies raised capital through the less known Luxembourg stock exchange. India’s capital market was being exported.

Some of us highlighted this phenomenon to SEBI. That began the private placement market (QIP) in early 2000s. Hence FIIs could also buy on Indian markets. The Indian saver’s interest in markets improved after the global financial crisis.

That saver is now savouring the joys of investing. Mutual fund platforms, cash equities and derivatives markets, insurance funds, global private equity in India, other platforms like AIFs, lower tax regime for equity, have all converted a saver to an investor.

How do we create a sustained growth story hereon?

1.Many investors have joined post Covid. They have mainly seen upside. While the situation is not comparable at present, we need to keep Japan of the 80s at the back of our mind. Its Nikkei Index peak was 1989. 34 years later with near zero interest rates, the Nikkei is still below its 1989 peak. We must avoid bubbles through policy, regulation, education, and supply of quality paper. Companies should raise equity at lower cost of capital for productive use.

2.While we must avoid tax arbitrage in debt, unless debt markets grow it will be a one legged race. The current gap on highest marginal tax rate between debt and equity of 39% and 10% is perhaps too wide.

3.Double taxation on dividends needs relook. A shareholder is like a partner. There is no additional tax when money is moved from the partnership to the partners capital account. Same principle applies to shareholders.

4. Low cost leverage through derivatives can distort financial markets. This needs attention.

https://t.co/M1heYN2OvA savers become investors the banking sector faces challenges on its deposits and cost of funds. The large corporate sector has to meaningfully move to capital markets (debt and equity) and away from banks. Banks will become distributors of corporate debt rather than storage houses. They will need to penetrate mid sized corporates, MSMEs and consumers.

6. We should avoid a retrospective tax and regulatory regime. We will need to balance developmental and regulatory role.

7. Two areas which need urgent focus for India’s aspiration are acquisition financing and streamlining of the IBC/ NCLT process.

As India aspires, the financial sector will be the key engine for delivery. Impact of technology is a separate subject of discussion for a future date. The saver/ borrower and the issuer/ investor models will coexist. It is time for a wholistic financial sector view.

BJP MP from Ladakh Tsering Namgyal addresses Nehruvian blunders in Lok Sabha, spotlighting lost territories – PoK, Shaksgam, Aksai Chin, Minsar, Mount Kailas and Mansarovar, regrettably given to China by Pandit Nehru.

Lalu Parsad Yadav, Mamta Banerjee, Nitish Kumar, etc. have been our previous Central Government Railway Ministers; now see this.

Mr. @AshwiniVaishnaw , M. Tech, MBA. (B. Tech from IIT Kanpur) Former IAS, Former MD(GE Transportation). No Political Background and yet made the Minister of Railways as well as Minister of Electronics and Information Technology.

The result is in front of us..... Amazing clarity, How he is working silently and in a synced manner. He speaks like a CEO of a $1 Trillion Corporation ... Fully on top of his subject...

At the World Economic Forum ! (Please don't watch if you have allergies of BJP, Narendra modi and his ideology)

"There are answers worth billions of dollars in 30$ books " — Charlie Munger

Charlie Munger passed away. He was one of the smartest people of our time.

Here are 9 Book recommendations from Charlie Munger (as a tribute to Charlie):