Just made your first crypto transaction? That's worth 3 USDC at Ramp Network.

Create a wallet → make one transaction → earn $3 back.

Plus up to 8 USDC total in rewards waiting for you inside the app 👇

* Available for users outside EU & UK.

Follow this guy! 👇If you're a researcher and your not following this guy for his great clips, then I really don't know what to say... thanks Francisco! 👊

🚨JUST IN: AUSTRALIA PASSES FIRST CRYPTO LAW

Crypto exchanges and custody providers must now obtain AFS licenses.

The law also creates new regulated crypto platform categories and introduces rules to prevent misuse of customer funds.

Stablecoins may be global.

But the market is still overwhelmingly dollar-driven.

93% of supply is USD-denominated, while euro stablecoins are still small (~$670M), despite fast growth after MiCA.

Market structure today:

- Fiat-backed dominates (85% share) led by Tether and USD Coin

- Crypto-backed led by Dai and synthetic models like USDe

- New entrants expanding the long tail (PayPal USD, First Digital USD)

Key takeaway:

Stablecoins are growing fast.

But the real story isn’t just growth.

It’s currency concentration.

Digital dollars are scaling first.

Digital euros are trying to catch up.

Regulation may decide how balanced that future becomes.

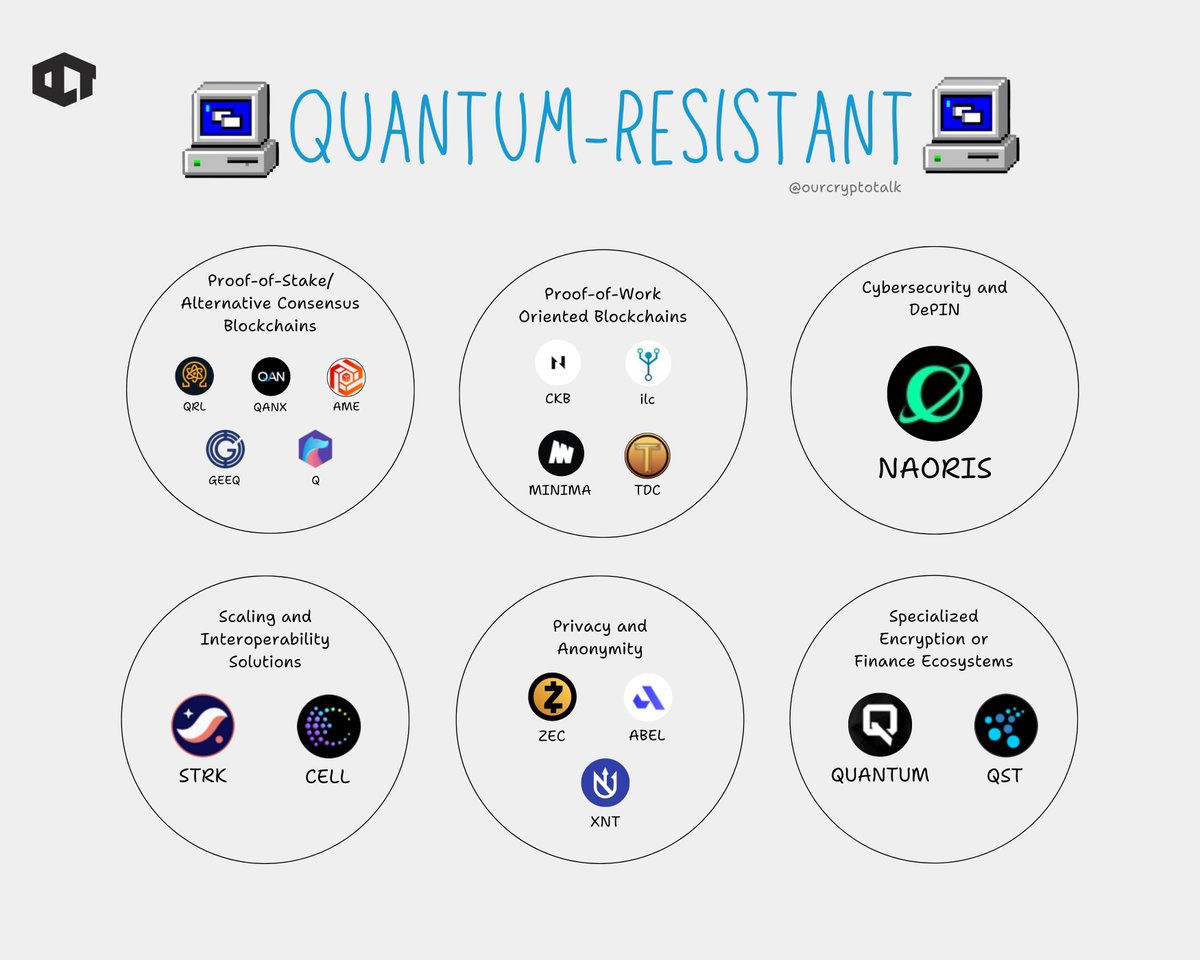

Google set a 2029 deadline to migrate all systems to post-quantum cryptography.

This hits crypto harder than any other industry.

$QRL $QANX $CKB $ZEC $ABEL $STRK $NAORIS etc. are already solving what they just warned the world about.

Almost every blockchain in existence, Bitcoin, Ethereum, and most altcoins, secures wallets and signs transactions using Elliptic Curve Cryptography aka ECC

It works because classical computers would take longer than the age of the universe to crack it.

Quantum computers don't play by those rules.

They use qubits, which process multiple states simultaneously.

Shor's Algorithm, a quantum-specific method, can break ECC exponentially faster than any classical machine.

A sufficiently powerful quantum computer could derive your private key from your public key.

> Drain your wallet

> Forge signatures

> Make immutable ledgers mutable.

And most of crypto has no plan. Just the same foundations quantum will eventually shatter.

But a few of them are already working on strong solutions.

━━━━━━━━━━━━━━━━━━━━

→ ZEC | @Zcash

━━━━━━━━━━━━━━━━━━━━

• Shields transactions using zk-SNARKs.

• No sender or receiver information

• Privacy quantum computing can't unravel.

━━━━━━━━━━━━━━━━━━━━

→ QRL | @QRLedger

━━━━━━━━━━━━━━━━━━━━

• Every transaction signed with XMSS,

• NIST-approved post-quantum standard.

• Not retrofitted. Built this way from block one.

━━━━━━━━━━━━━━━━━━━━

→ STRK | @Starknet

━━━━━━━━━━━━━━━━━━━━

• Settles transactions using STARK proofs.

• No elliptic curves or exposure to Shor's Algorithm.

• Quantum-resistant by design, not by patch.

━━━━━━━━━━━━━━━━━━━━

→ NAORIS | @NaorisProtocol

━━━━━━━━━━━━━━━━━━━━

• Validates every connected device in real time.

• No central server or single point of failure.

• Post-quantum security at the infrastructure level.

Your encrypted data is being stored today to be cracked tomorrow.

2029 isn't a distant deadline and it's in the next bull cycle.

Know the real ones who are building the solution to this problem.

Tether has hired KPMG as auditor and brought in PwC as it prepares for fundraising and U.S. expansion under new stablecoin regulations.

A positive step for transparency and institutional credibility across the broader crypto industry.

Fancy travelling the world? It’s not all piñas coladas and sunsets.

Digital nomad life has its challenges, including banking delays and financial stress.

Now, you can move money instantly and enjoy the journey.

@jilaryonchain explains how in this video 👇

We will soon offer crypto buy & sell services in Europe as an authorised Crypto Asset Service Provider (CASP).

Everything in one place across web + app mobile web, including a self-custodial wallet where you stay in control.

Join the waitlist👇

https://t.co/jKtvmX21Ad

There's no IP in stablecoin neobanks. Here's why I'm building one anyway.

I've been thinking about this for a while, and I think it's time to say what everyone in the space knows but nobody wants to admit: stablecoin neobanks have zero defensibility.

Every single one you see launching is the same product with a different logo. And honestly? I don't think that's a bad thing. Let me explain......

The regulatory moat that protected fintech doesn't exist here

In traditional fintech, part of the moat was regulatory. Getting a branking/psp/vasp license was hard, expensive and took big compliance resources years, millions in legal fees, and connections that most founders didn't have.

With non-custodial stablecoin wallets? None of that applies.

You're not holding user funds. You're not a money transmitter in most jurisdictions. You're just a frontend to DeFi protocols. You can launch in Argentina, Nigeria, Indonesia, or anywhere tomorrow without asking permission from anyone, at the same time.

This is honestly incredible for innovation. Users get access to dollar-linked savings without needing a US bank account. But if you're trying to build a defensible business? There's nothing stopping 50 competitors from launching the exact same thing next month.

@maxkarpis broke this down really well — the "next Revolut" story is always the same: three ex-fintech employees, crypto-native, some offshore on/off-ramp magic. But the underlying infrastructure is identical.

Every feature you can offer is a commodity.

This is the part that nobody talks about publicly.

Want to offer a stablecoin card? You're not building anything. You're calling @raincards or @gnosispay or plenty of other providers.

They handle issuance, compliance, everything. You literally just put your logo on it.

Rain is probably powering half the crypto cards you've heard of. Teams raise $10M and announce "we're launching a card" like it's some technical achievement. It's not. It's an API integration. An easy one actually.

@paramonoww wrote extensively about this — don't be delusional thinking teams need tens of millions to launch a crypto card. They need Rain and a logo.

Want yield on deposits? You're not building a yield engine. You're plugging into @yield_xyz or @LuloApp.

The yield comes from the same DeFi protocols everyone else uses. Your "8% APY" is the same 8% APY your competitor offers because it's literally the same underlying source.

Need wallet infrastructure? @dynamic_xyz@privy_io@thirdweb will have you live in days. And their products are actually great, we been using them for years now. Account abstraction, social login, gasless transactions — all commoditized.

On/off ramps? same situation: @moonpay bridge, and more are fighting for your attention.

I could literally give you a weekend project: stitch these together, ship a landing page, and you have a "stablecoin neobank" by Monday. That's not an exaggeration. The entire stack is available off the shelf.

So what exactly is anyone building? A UI. A brand. Some copy. That's the uncomfortable truth.

So why am I building @LucaMoneyApp another stablecoin neobank?

Because the opportunity is genuinely massive, and the lack of IP actually makes it more interesting, not less.

There's $170B+ in stablecoins. Currencies across Latin America are in freefall. 70% of tech workers in Argentina want USD or crypto payments. The demand is real and desperate.

And here's what commoditized infrastructure actually means: the game isn't about who builds the best tech anymore. Everyone has access to the same tech. The game is about who captures users the fastest.

The real moat is stickiness and speed

If everyone can assemble the same legos, the winner is determined by:

Who gets to specific markets first

Who builds the strongest user habits

Who captures network effects before competitors show up

This is a land grab, not a tech race.

The team that becomes "the app Argentinians use to save in dollars" wins. Not because their yield aggregator is 0.000000003% better or their card has cooler colors and glow in the dark.

Because they got there first, built trust, and users don't switch apps that hold their savings.

People dramatically underestimate switching costs for financial products. Once someone trusts you with their money and builds a habit around your app, they're not leaving for a marginally better competitor. The moat is installed base + brand + daily habits.

Niche by niche, market by market

We're not trying to build "the global stablecoin neobank." That's a losing strategy when you have no differentiation.

We're trying to own specific user segments completely:

-The Argentine saving in USDC because the peso lost 90% in 3 years

-The Venezuelan receiving remittances from family abroad

-The freelancer getting paid by US clients who doesn't want a US bank

Win these niches one by one. Build features they specifically need. Talk to them every day. Move faster than anyone else in those corridors.

That's the playbook. Not proprietary tech. Not patents. Speed and obsession with specific users.

We're building @LucaMoneyApp with this thesis. Non-custodial stablecoin savings for Latin America. Simple, fast, focused.

I'm not going to pretend we have magical IP that nobody else can replicate. We don't. Nobody does. Our IP is how fast we are and how sticky our app is, thats it. And if we focus on this we will win.

If you're building infrastructure in this space — DM me and lets connect.

Think your bank money is safe? All you have is their promise.

Crypto completely changes the game. Discover how Self-Custody represents the ultimate power shift for your finances, granting you true ownership.

Ready for total control? Watch the video!

@jilaryonchain

🎤 Happening today at @Zebu_live!

Our CEO @przemekowalczyk will be speaking on the panel:

“From Capital to Code to Consensus: Web3’s Industrial Stack”

🕒 3:15 PM (BST)

Join the discussion on what’s shaping Web3 today – infra, innovation & more.

Don’t miss it! 🇬🇧

Big ideas at full speed on the Future of Money stage at @Zebu_live 🎤

Great to see @przemekowalczyk, CEO & Co-founder at @RampNetwork diving deep into Web3’s industrial stack ✅

We love watching and hearing our clients thrive as they tackle meaningful, industry-driving discussions like this one.

Did you know?💡 ~93% of all stablecoin market share is held by just two tokens – USDC and USDT.

That dominance has made them critical to global liquidity, from DeFi to cross-border transfers.

The next big question: will regional stablecoins or CBDCs start to chip away at that lead?

Just dropped the @RampNetwork App in the US, UK & RoW 🚀📱

Key lessons:

Don’t wait for perfect → ship it, fix it later 🛠️

Users > your opinions (they’ll tell you what sucks)

Scope creep = the devil 😈

Lab tests lie. Real users don’t.

https://t.co/weBWR8Bynk

If you’ve ever tried explaining stablecoins at a dinner table and ended up in:

1. Economics 101

2. FX markets

3. “But is it safe?”

You’re not alone. The easiest answer? It’s money that just… works.