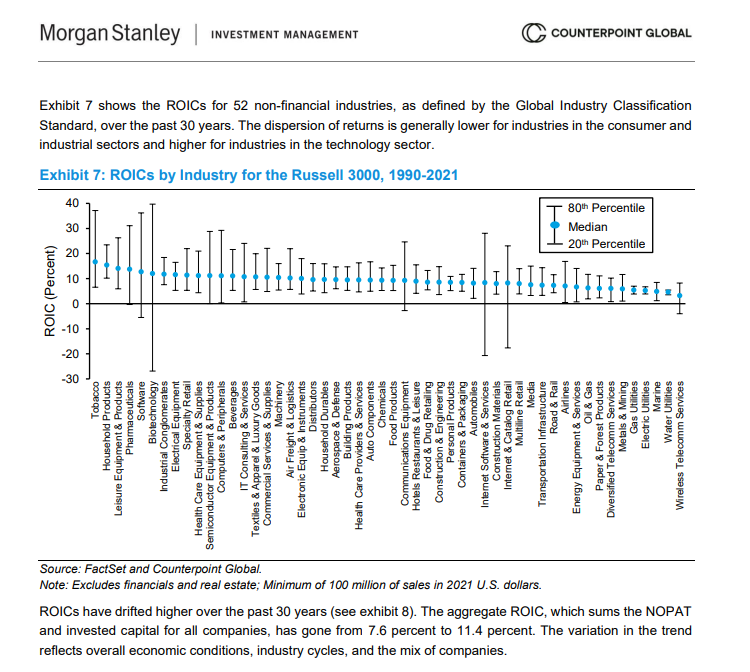

Michael Mauboussin on ROIC by industry:

"The dispersion of returns is generally lower for industries in the consumer and industrial sectors and higher for industries in the technology sector."

"A company’s ROIC is determined in part by the industry it competes in and the strategies it pursues."

MSCI EM leadership is shifting fast.

🇨🇳 China’s weight in MSCI EM has fallen from ~43% Oct’20 to ~21% post May’26 review.

AI + semiconductor tailwinds have pushed:

🇹🇼 Taiwan to ~26.5% vs 12.7% in October 2020

🇰🇷 Korea to ~21.5% vs 11.9% in October 2020

🇮🇳 India, after peaking near ~20% in Jul’24, is back to ~11%.

Interestingly, MSCI India vs MSCI EM is now near the lower band of a rising channel in place since 1996 with relative drawdowns deeper than prior cycles.

Source: IIFL Alt Desk

Potential mean reversion setup 🤔

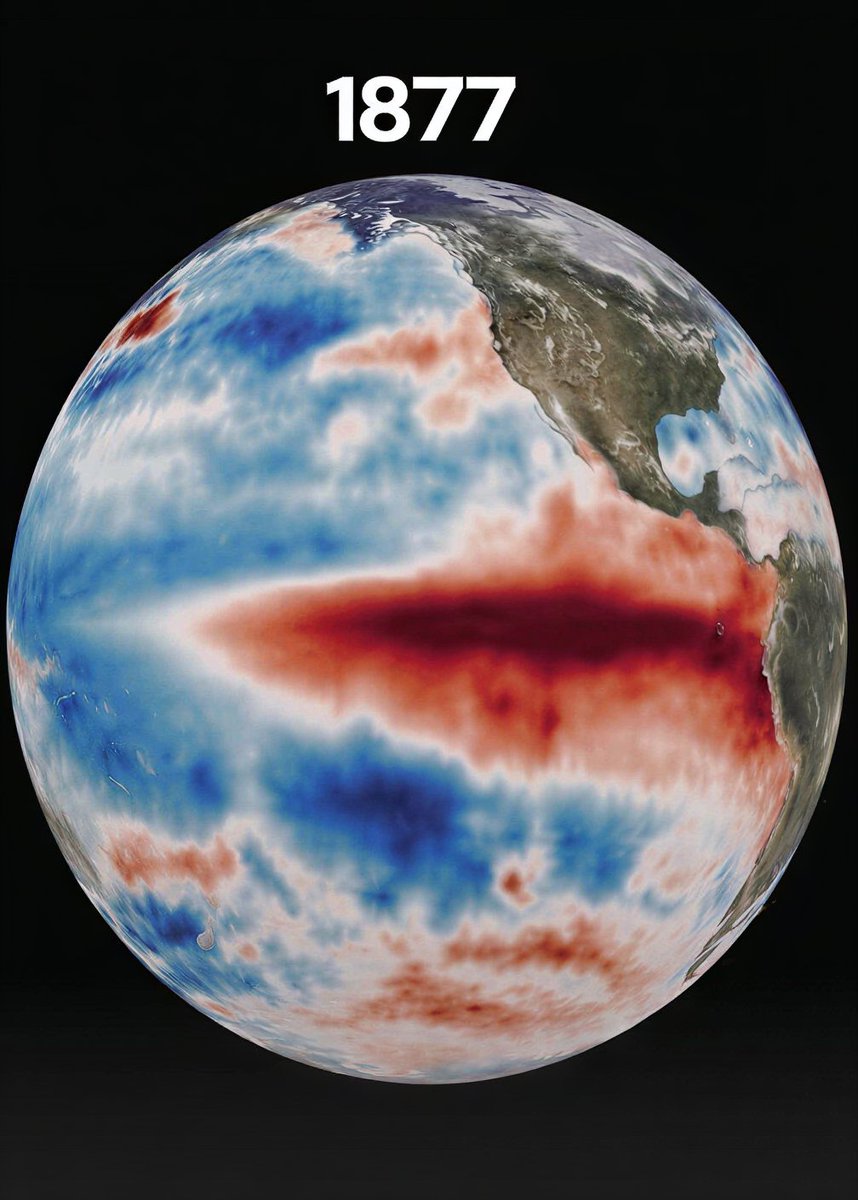

BREAKING🚨: Earth just entered intense weather cycle and could be the strongest ever recorded

The 2026 El Niño is shaping up to be the deadliest since 1877 — the year famines killed more than 50 million.

Forecasters are tracking ocean temperature spikes of 2 to 3 degrees Celsius. That's not a minor uptick. That's the signature of a once-in-150-years event.

Per LiveScience: a "Super" El Niño is now the most likely outcome by year's end. The human cost could be staggering.

EXPECTED TERMS OF US-IRAN PEACE DEAL:

1. Extension of Iran War ceasefire for another 60 days

2. Strait of Hormuz reopened for the 60-day period

3. Iran would be able to freely sell oil during the period

4. US would lift blockade on Iranian ports and unfreeze some Iranian funds

5. US would issue some sanction waivers on Iranian oil

6. Draft MOU includes statement that war between Israel and Lebanon would end

7. Negotiations would then be held regarding Iran's nuclear program

The draft MOU includes commitments from Iran to never pursue nuclear weapons, negotiate over a suspension of uranium enrichment, and removal of its highly enriched uranium, US officials told Axios.

The situation remains fluid amid the high-stakes negotiations.

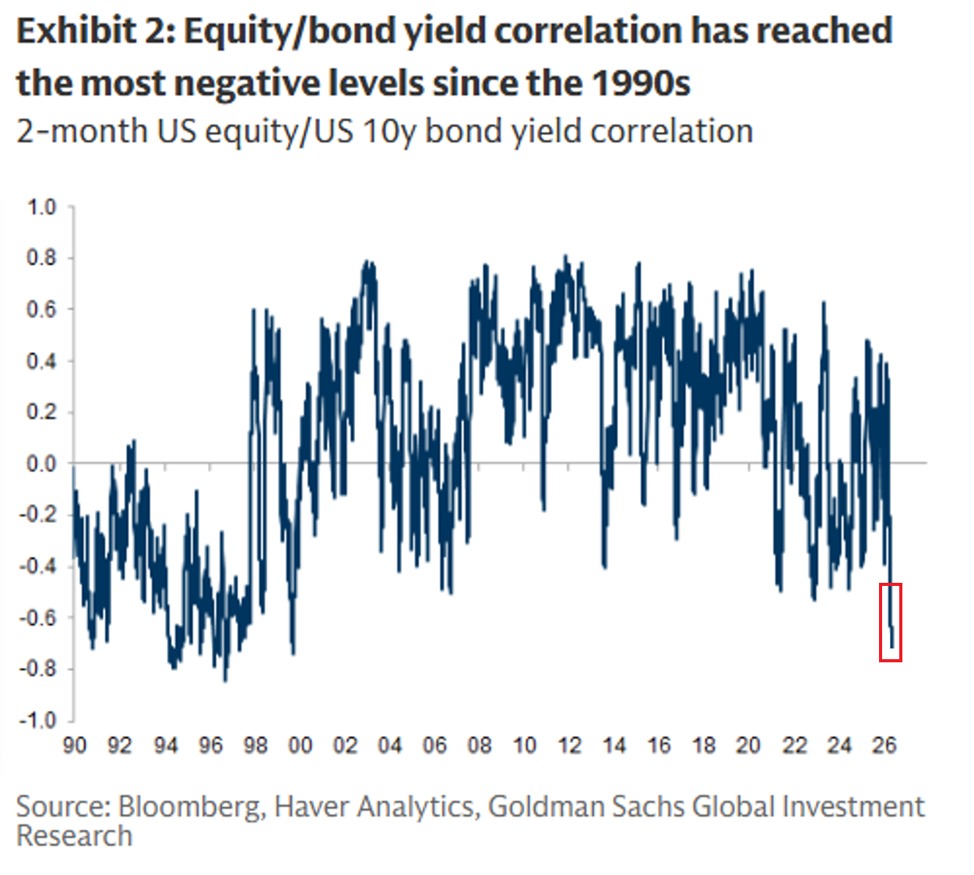

The stock-bond relationship is showing a rare pattern:

The 2-month correlation between US equities and the 10-year Treasury yield is down to -0.70, the lowest since 1999.

In other words, over the last 2 months, stocks and the 10-year Treasury yield have moved in opposite directions by the largest extent this century.

At the start of 2026, a positive correlation of 0.40 was observed, near the highest since 2023.

Additionally, the 30-day correlation is down to -0.68, also the lowest in 27 years.

Not even the 2022 bear market saw such a negative correlation, as the 10-year yield rose, driven by elevated inflation and Fed rate hikes, while stocks fell.

Bond markets are incredibly important right now.

Russia is selling its gold reserves at a rapid pace:

The Bank of Russia's gold holdings dropped -900,000 ounces in the first 4 months of 2026, to 73.9 million ounces, the lowest since February 2022.

Gold prices averaged ~$4,800 per ounce over the same period.

Therefore, if Russia sold gold at the market price, the sales are estimated to have generated ~$4.3 billion in proceeds.

Russia's central bank began reducing its gold reserves last year after the Finance Ministry liquidated gold and foreign currency assets from the National Wellbeing Fund to offset budget deficits driven by declining energy revenues.

Before the pandemic, the Bank of Russia used to be one of the world’s largest official gold buyers, taking in nearly all domestically mined output until it halted purchases in early 2020.

Russia is increasingly selling gold to raise cash.

Since the start of the war, gold has been negatively correlated to oil. Oil up, gold down. Why? Because the marginal gold buyer is not the West, it is EM Asia and Turkey.

India alone is the world’s 2nd-largest gold buyer after China, across both central banks and retail. And the Rupee hates oil spikes, let alone an oil crisis like this. High oil intensity, limited crude storage, weak FX resilience.

The mechanism is self-reinforcing: Higher oil → weaker growth -> weaker Rupee → even higher import costs (also for oil) → even weaker growth → weaker Rupee again -> repeat.

That is precisely why Modi has moved to curb gold imports. He wants to support the Rupee (industry), not the consumer (gold is a hedge for a weaker Rupee). Well, not sure consumers will like it. So this will not last forever but I doubt it will stop before 2027.

Turkey already went further and dumped reserves to support its FX. Other EM Asian countries may follow. Not just Asian, perhaps also ME countries? They are hardest hit by this crisis. Qatar & Kuwait come to mind. They have plenty of SWF reserves but the hit is big and the invoices keep coming.

China offsets some of this through higher gold imports, but not enough, at least for now. Until the Strait of Hormuz situation stabilises, or EM Asia adjusts through demand destruction and policy responses, gold likely keeps bleeding, slowly, nothing dramatic, but bleeding.

And no, I do not think there is a quick fix for the SoH crisis. The two sides are too far apart. Weak regimes can survive longer than people expect (they had little oil exports under Trump 1.0 and survived for years). Trump has midterms ahead & is unlikely to escalate materially without political support. Without regime change, the structural issue remains.

So the oil market will likely solve this itself through painful adjustments into 2028: rerouted flows, new pipelines, permanent demand destruction, more coal, more efficiency.

For now, China is doing the heavy lifting. Chinese crude imports in May were down 45% vs February. That single-handedly balances a large part of this mess. But not indefinitely. Once China decides to normalises imports closer to baseline, or Japanese SPR drawdowns fade, Brent likely reprices higher again, ceteris paribus. Korea is another big player in the puzzle to watch.

Gold may stabilise before the full oil adjustment plays out. But I do not see much value in taking a rigid long-term view here. Too many moving parts. Mental flexibility remains key here.

We have been risk-off since week one of the war, largely because we understand commodity transmission mechanisms. If this turns into a healthy correction in quality miners, I am certainly happy to buy it as the structural gold story remains largely unchanged. I explained it in 2023/24/25 on this channel.

That is what I am watching.

YARDENI:

“.. we expect the FOMC to signal a tightening bias at the June meeting of the monetary policy-setting committee, followed by a 25bps FFR hike at the July meeting. We can't rule out more rate hikes over the rest of this year.”

@yardeni

🚨HOLY COW:

US margin debt SPIKED $83 BILLION in April, to $1.3 TRILLION, an all-time high.

Leveraged borrowing has soared $453 billion, or +53%, over the last year alone.

Margin debt now reflects 5.2% of US GDP, also an all-time record.

This exceeds any other bubble peak and the meme stock frenzy in 2021.

There has never been so much leverage in the stock market.

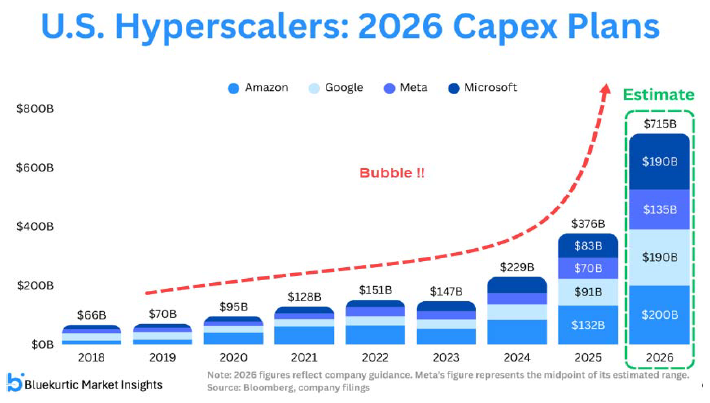

US hyperscaler capex on AI infrastructure:

- 2020: $95 billion

- 2022: $151 billion

- 2024: $229 billion

- 2025: $376 billion

- 2026 (estimate): $715 billion

That's nearly $2 billion a day. From four companies.

Either AI delivers the biggest productivity revolution since electricity, or this is the biggest mistake in corporate history.

Both possibilities are on the same chart.

Every single midterm year since 1974.

Same pattern.

1974 Ford: −35%

1978 Carter: −15%

1982 Reagan: −17%

1986 Reagan: −10%

1990 Bush: −20%

1994 Clinton: −8%

1998 Clinton: −22%

2002 Bush: −34%

2006 Bush: −8%

2010 Obama: −17%

2014 Obama: −10%

2018 Trump: −20%

2022 Biden: −27%

2026 Trump: ???

Every single one had a significant drawdown.

Every single one recovered.

The long-term chart kept going up.

The question for 2026 is not if it recovers.

The question is whether you will still be invested when it does.