$RDW 2026 하반기 리서치

수주 싹쓸이와 마진 개선, 그리고 실탄 장전

매출 폭발과 마진 정상화,펀더멘털 개선

26년 1분기 매출이 9,697만 달러로 전년 동기 대비 57.9% 올랐다. 핵심은 마진이다. 작년 4분기 9.6% 바닥 기던 매출총이익률이 1분기에 26.6%로 수직 상승했다.

저마진 계약 털어내고 사업 효율화가 먹히고 있다는 뜻이다. 현재 수주잔고만 역대급인 4억 9,810만 달러고, 2026년 연간 매출 가이던스 4.5억~5억 달러도 굳건하게 유지 중이다. 하반기 실적 방어는 이미 깔아둔 일감으로 충분하다.

우주산업 쩐의 전쟁

SSC 가 주도하는 Andromeda IDIQ 계약 벤더 14곳 중 하나로 레드와이어가 선정됐다. 원래 18억 달러짜리 프로젝트였는데, 수요 폭발로 전체 예산 한도를 60억 달러 이상으로 뚫어버린다는 공시가 떴다. 하반기 내내 VLEO및 위성 인프라 수주전에서 막강한 현금 창출원이 될 거다.

5억 달러 ATM

지난 6월 9일 자로 기존 ATM을 철회하고 최대 5억 달러 규모 신규 ATM 오퍼링을 때렸다. 주주 입장에선 피꺼솟이지만, 회사 입장에선 달 탐사, CLPS, 안드로메다 같은 대형 프로젝트 IRAD 돌리고 추가 M&A할 수 있는 '무적의 5억 달러 실탄'을 챙긴 거다. 거시 경제 흔들려도 버틸 체력은 확보했다.

끝없는 유증과 물량 부담

5월 말 스페이스X 상장 테마 등으로 26달러까지 찍었던 주가가, 6월에 저 5억 달러 ATM 공시 뜨자마자 폭포수처럼 쏟아져서 현재 7월 초 기준 11~12불대에서 놀고 있다. 시총 30억 달러도 안 되는 회사에 5억 달러짜리 매물 폭탄이 열린 거다. 하반기 내내 주가 오를 만하면 주식 찍어 팔아서 주주 가치 희석시킬 리스크가 상존한다.

만성 적자와 EPS 미스

덩치는 커지는데 흑자 전환은 멀었다. 1분기 순손실만 7,650만 달러, EPS는 -0.40달러로 월가 예상치(-0.15달러)를 시원하게 박살 냈다(Edge Autonomy 인수 관련 일회성 비용이 컸음). 당장 8월 초에 있을 Q2 실적 발표에서 잉여현금흐름 개선이나 적자 폭 축소의 가시성을 못 보여주면 시장은 더 이상 안 기다려 줄 거다.

개인적인 의견이며 매수/매도 추천이 아님.

팩트에 기반한 나의생각과 리서치를 기반으로 작성.

The American story is one of builders, explorers, innovators and dreamers.

This Fourth of July, we celebrate the spirit that continues to push boundaries, strengthen our nation and inspire what’s possible.

At Redwire, we’re proud to support the missions that protect what matters here on Earth and expand what’s possible beyond it.

Happy 250, America! 🇺🇸

반도체 기업의 엄청난 랠리는 어떻게 계속될까요?

그들의 서사를 유지하기 위해서는 '휴머노이드'가 필요합니다.

90% 마진의 HBM 사업의 놀라운 멀티플이 가장 무서워 하는 의심은 이겁니다.

바로 "이 수요가 언제 꺾이느냐"

휴머노이드는 곧바로 2027년 메모리 수요를 만들지 않는다.

하지만 휴머노이드가 만드는 건 2033년에도 메모리 수요가 존재한다는 믿음이고,

그 믿음이 2026년의 팹 착공을 정당화하며, 그 착공이 2026년의 멀티플을 지탱하게 됩니다.

메모리 기업들이 조금씩 휴머노이드 기업을 조용히 언급하는 이유입니다.

실제로 조금씩 구체화되고 있습니다.

1) Nvidia-SK하이닉스 다년 파트너십, 휴머노이드·산업 로봇용 Jetson Thor 플랫폼 메모리 공동개발

2) 삼성, 레인보우로보틱스의 최대 주주

3) 이재명 정부, 삼성·SK하이닉스 중심의 메모리 증설과 휴머노이드 상용화 가속을 1조 달러 패키지로 묶음.

4) Micron은 READY Robotics에 투자 중.

휴머노이드 = 로봇 한 대가 새 메모리 소비 단위

이 서사가 만들어지면 메모리 수요 곡선의 끝이 안보입니다.

이 서사가 반도체 기업 입에서 일제히 나오는 순간을 놓치지 마세요.

2026년 하반기가 중요한 시점입니다.

$RDW: NASA's Space Reactor-1 (SR-1) Freedom is humanity's first fission-powered interplanetary spacecraft.

SR-1 combines a nuclear fission reactor with the Power and Propulsion Element (PPE) originally developed for the Lunar Gateway station.

Redwire was building a pair of the most powerful Roll-Out Solar Arrays ever developed for Gateway. If this model is accurate, those same arrays appear set to be reused on the SR-1 spacecraft.

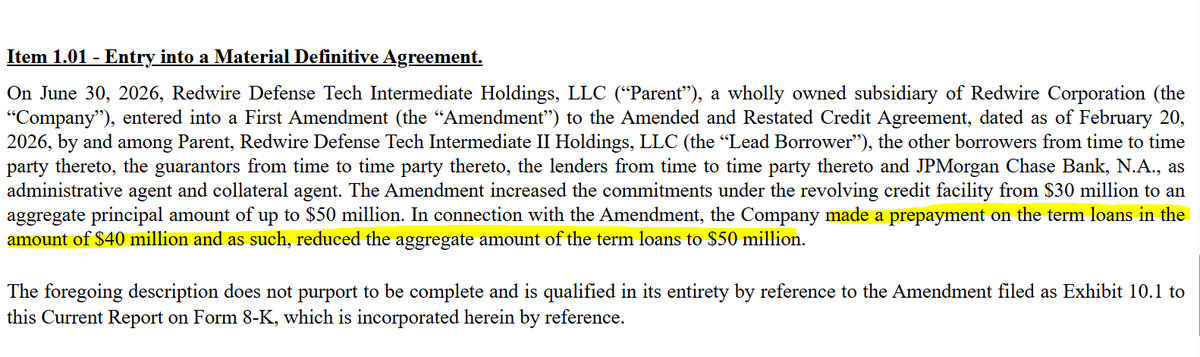

$RDW: Redwire just filed a new Form 8-K

Redwire volontarily prepaid $40M of its term loan, reducing outstanding debt from $90M to $50M and increased their revolver from $30M to $50M

Basically management chose to strenghten the balance sheet while maintaining access to liquidity.

it should improve the company's financial profile.

I bought $RKLB at $11

I bought $ASTS at $24

Today, I'm telling you $RDW is next.

If you missed the early days of the space sector,

$RDW is your time machine.

$RDW

Britain will unveil its long-delayed Defence Investment Plan on Tuesday, prioritising £5 billion of investment in drones and a focus on autonomous systems.

Redwire is preparing itself for a large delivery of VTOLs

$RDW: Be careful shorting a space company using financial metrics alone.

To be fair, they raised valid concerns about margins, reporting and the slower growth we saw last year. Those issues were real, and in my view, they're exactly why the stock is trading at a discount in the first place.

What I think they're missing is the inflection point, and they are about to find out.

Shorting one of the cheapest names in the sector after a ~50% industry wide correction, while the company is entering one of the most catalyst-rich periods in its history, is a very risky bet.

Tomorrow's NASA event, the upcoming Andromeda IDIQ awards, an accelerating M&A environment, a solid quarter for Redwire Defense after $100M in orders this quarter, VLEO moving toward its first demo mission, QKD sat production, in-space manufacturing going mainstream, ESA's budget increase, Golden Dome... just to name a few.

I could be wrong, but I wouldn't go short into that setup, at all!

아무리 계산해봐도 현재 공개된 내용만으로는 현실성이 너무 약하다.

반도체 팹은 발표문으로 짓는 게 아니다.

물과 전기가 먼저 있어야 한다.

지금 발표는 AI CAPEX 사이클이라기보다 전력·용수 로드맵이 빠진 전당대회용 공수표에 가깝다.

1. 물부터 숫자가 안 맞는다.

광주는 2022~2023년 극한 가뭄 때 시민 절수운동까지 했던 도시다.

당시 광주 하루 물 사용량은 약 50만 톤이었다.

동복댐 하루 22만 톤.

주암댐 하루 28만 톤.

이 두 축으로 도시 생활용수를 버티던 구조였다.

가뭄이 오자 광주는 영산강 비상도수, 공급망 전환, 농업용 저수지·지하수 연계, 시민 절수까지 동원했다.

그렇게 전부 끌어모은 추가 물이 하루 22만 톤 수준이었다.

이게 광주의 물 현실이다.

그런데 삼성전자 국내 반도체 사업장은 2022년 기준 하루 약 34.4만 톤의 물을 썼다.

광주가 가뭄 때 온갖 방법으로 확보한 하루 22만 톤보다 크다.

광주 시민 전체 하루 물 사용량 50만 톤의 약 69%다.

용인 반도체 클러스터 용수공급 계획은 하루 107.2만 톤 규모다.

광주 하루 물 사용량의 2.1배다.

반도체 클러스터는 공장 몇 개 짓는 사업이 아니다.

도시 하나가 쓰는 물보다 더 큰 산업용수 체계를 새로 요구하는 사업이다.

2. 물그릇으로 봐도 위험하다.

광주 주요 식수원인 동복댐 총저수용량은 약 1억 톤 수준이다.

주암댐 본댐 총저수용량은 약 4.57억 톤 수준이다.

숫자만 보면 커 보인다.

하지만 2022~2023년 가뭄 때 동복댐은 저수율 20% 아래까지 내려갔다.

남은 물이 2,000만 톤도 안 되는 수준까지 갔다.

주암댐도 저수율 20% 안팎까지 내려갔다.

이 상태에서 삼성전자 국내 반도체 하루 물 사용량 34.4만 톤은 동복댐 가뭄 잔량의 약 1.7%를 하루에 쓰는 수준이다.

용인 클러스터급 하루 107.2만 톤이면 동복댐 가뭄 잔량의 약 5%를 하루에 쓰는 수준이다.

가뭄이 오면 며칠 단위로 댐 수위가 체감되는 산업이다.

반도체는 평소 물이 아니라 최악의 가뭄 때도 끊기지 않는 물을 요구한다.

그런데 물 부족을 겪었던 지역에 팹 4기, AI 데이터센터, 협력사 산업단지까지 동시에 얹겠다는 말은 현실성부터 검증해야 한다.

3. 전기도 숫자가 안 맞는다.

2024년 전력판매량 기준으로 광주는 9.3TWh, 전북은 21.6TWh, 전남은 33.6TWh를 썼다.

광주·전북·전남을 전부 합쳐도 연간 64.5TWh다.

그런데 정부 AIDC 계획은 2029년 8.4GW, 2035년 18.4GW다.

8.4GW를 1년 24시간 돌리면 73.6TWh다.

18.4GW면 161.2TWh다.

8.4GW AI 데이터센터만 해도 호남 전체가 1년에 쓰는 전기보다 크다.

18.4GW면 호남 전체 전력사용량의 약 2.5배다.

여기에 반도체 팹 전력은 빠져 있다.

TSMC 애리조나 1단계도 약 200MW급 전력 수요가 거론된다.

200MW 팹 하나를 1년 24시간 돌리면 1.75TWh다.

팹 4기를 아주 보수적으로 800MW로 잡아도 연 7TWh다.

대형 메모리 캠퍼스급으로 1GW 팹 4기를 잡으면 연 35TWh다.

35TWh는 광주 전체 전력사용량의 약 3.8배다.

전남 전체 전력판매량 33.6TWh보다도 크다.

AIDC 8.4GW와 대형 팹 4기를 합치면 연 108.6TWh다.

호남 전체 전력사용량 64.5TWh의 약 1.7배다.

이 숫자 앞에서 “전라도에 전기 있다”는 말은 너무 가볍다.

4. 보유 전원으로 봐도 빡빡하다.

전라도권에 재생에너지가 많은 것은 맞다.

하지만 재생에너지가 많다는 말과 반도체 팹·AI 데이터센터를 24시간 무정전으로 돌린다는 말은 다르다.

공식 통계 기준 광주·전북·전남 신재생 설비 보유량은 약 11GW 수준이다.

광주 약 0.35GW.

전북 약 5.06GW.

전남 약 5.67GW.

합산 약 11GW다.

그런데 2029년 AIDC만 8.4GW다.

호남 신재생 정격용량의 약 76%다.

2035년 AIDC 18.4GW는 호남 신재생 정격용량의 약 1.7배다.

여기에 대형 메모리 팹 4기를 4GW로 잡으면 숫자는 더 커진다.

2029년 AIDC 8.4GW + 팹 4GW = 12.4GW.

이미 호남 신재생 정격용량 11GW를 넘는다.

2035년 AIDC 18.4GW + 팹 4GW = 22.4GW.

호남 신재생 정격용량의 2배가 넘는다.

더 큰 문제는 이 11GW가 정격용량이라는 점이다.

태양광은 밤에 0이다.

풍력은 바람이 없으면 줄어든다.

반도체 팹은 멈추면 안 된다.

AI 데이터센터도 24시간 돌아가야 한다.

태양광 11GW와 원전·가스 11GW는 같은 11GW가 아니다.

반도체가 요구하는 것은 평균 전기가 아니라 끊기지 않는 전기다.

5. ESS는 해결책이 아니라 추가 비용이다.

ESS는 전기를 만드는 설비가 아니다.

전기를 잠깐 저장해서 시간을 옮기는 설비다.

800MW 팹 4기를 4시간만 버티게 해도 3.2GWh ESS가 필요하다.

국내 ESS 중앙계약시장 육지 공고 물량이 500MW, 3GWh 규모다.

즉 아주 보수적으로 잡은 팹 4기 4시간 백업만 해도 국내 대형 ESS 입찰 한 번과 비슷한 규모다.

대형 캠퍼스급 4GW로 잡으면 4시간 ESS만 16GWh다.

24시간 버퍼는 96GWh다.

3일 버퍼는 288GWh다.

이건 ESS만으로도 수십조 원이 들어갈 수 있는 영역이다.

송전망, 변전소, 계통 접속, UPS, 비상발전기, 전력품질 설비, 소방, 부지, 배터리 교체비는 전부 별도다.

6. 결론

물은 가뭄 때 시민 절수까지 했던 지역에 하루 수십만~100만 톤급 반도체 용수를 얹는 문제다.

전기는 호남 신재생 보유설비 약 11GW 지역에 AIDC 8.4GW~18.4GW와 반도체 팹 전력을 동시에 얹는 문제다.

정격용량 기준으로도 빡빡하다.

실효 공급능력 기준으로 보면 훨씬 더 어렵다.

ESS는 해결책이 아니라 비용을 더 키우는 장치다.

없는 물이 발표문에서 생기지 않는다.

없는 전기도 구호에서 생기지 않는다.

정치 테마는 발표 금액을 본다.

투자는 물그릇, 발전설비, 송전망, 인허가, 발주를 본다.

현재 공개된 숫자만 보면 이건 AI CAPEX 사이클이라기보다 전력·용수 로드맵이 빠진 전당대회용 공수표로 보는 게 맞다.

$RDW --- In June, the U.S. Missile Defense Agency (MDA) advanced the $542 billion Golden Dome next-generation national missile defense initiative. As a core aerospace & defense supplier, sell-side analysts project $RDW will phase into the program and secure initial contract awards by late 2026.

$RDW has completed development, testing and customer delivery of its flagship MANUS lunar robotic arm prototype. The system is engineered for payload handling and offloading on future crewed lunar missions, further cementing its critical tier-1 supplier status within NASA’s industrial ecosystem.

1.Pick-and-Shovel Play for Full-Spectrum Space Infrastructure

Unlike speculative launch-focused space startups that rely solely on launch vehicle narratives, Redwire specializes in foundational orbital infrastructure. Any operator targeting space access — SpaceX, Blue Origin, NASA, and U.S. military branches alike — depends on Redwire’s product suite: Roll-Out Solar Arrays (ROSA), satellite antenna systems, in-space additive manufacturing hardware, and spacecraft digital twin software. It stands as a universal critical component supplier spanning the entire space value chain.

2.Dual Growth Engines: Commercial Space + National Defense

Its latest quarterly earnings highlight a successfully diversified revenue mix. Q1 total revenue hit $97 million, split between $52.7 million from commercial space operations and $44.3 million in defense tech sales. Amid heightened global geopolitical tensions, rising defense budget allocations provide a rock-solid baseline for recurring top-line growth.

3.Record-Setting Contract Backlog with Massive Long-Term Pipeline

$RDW ’s contracted order backlog has climbed to an all-time high of nearly $500 million, a figure that even exceeds its full-year annual revenue guidance. Meanwhile, its total prospective program pipeline tops $10 billion. Consistent on-time delivery will lock in multi-year, highly predictable revenue visibility for the firm.

Starcloud has been selected by @NASA as one of 37 companies (the only space-data center company) to advance Moon and Mars technology! 🚀 @Starcloud_

https://t.co/q3GTi0GqHC

Current thoughts 👇

$RDW and $SIDU have a solid chance of bottoming here, with tests of key moving averages this week and oversold RSI.

I understand the frustration with $RDW, and if you can't handle the volatility I'd suggest de-risking. However, I truly believe this will reward us heavily over the coming months.

I'm also happy with my $HIMS trim. I do believe this will still go to $39, however I wanted capital into $RDW so no complaints there, considering we're up over 100%.

Data centres such as $IREN $CRWV $GLXY $CIFR $KEEL $GRRR I have no real concerns about, and they'll rally sooner rather than later.

Crypto and software still want a new low, and both sectors will be generational buys once they bottom.

$ETH $BTC $MSTR $COIN $PLTR $ZETA $NOW

Quantum names such as $IONQ are testing key moving average confluence. Losing these confirms the move lower for Wave C.

China looks weak and corrective, however names such as $XPEV I'm interested in buying.

Commodities are starting to look good again, such as Palladium, which is very high on my watchlist going into next week. Remember the FOMO last time commodities rallied.

$RDDT looking primed for another breakout and still a buy here.

I'm very interested in $NKE and $LULU as safe havens for the coming years.

$DUOL will surprise many as a safe haven.

Overall a shaky but solid week, and I'm happy with my additions to $RDW near the 200DMA.

I can't name another creator publicly listing all their buys and sells, plus their largest position, for free.

As always my DMs are open, and if there's anything you'd like to see going forward please let me know.

Additionally thank you for all the kind words received this week, it truly means alot!

Have a nice weekend 🫶

레드와이어 $RDW 근황 ,방산부터 우주농업까지 폼 미쳤음

방산: 유로사토리 2026에서 소형 무인기용 정찰렌즈 '옥토퍼스 E140' 공개. 2.2kg 초경량인데 악천후 뚫고 타겟 식별 가능. ITAR 규제도 없어서 글로벌 수출길 뚫림.

우주농업: ISS 세계 최초 상업용 온실에서 '우주 야생 딸기' 재배 중. 화성 탐사 시 식량 자급자족할 생명유지시스템 뼈대 완성.

거버넌스: 주주 소송 합의로 5년간 거버넌스 개혁 돌입. 합의금은 전액 보험처리 완료. 경영 투명성 확 올려서 미 국방부/NASA 굵직한 계약 따내기 더 좋은 체질로 진화함.

단기 노이즈 방어 확실하고 장기 모멘텀 꽉 잡음. 우주·방산 복합 섹터 투자자라면 무조건 주시해야 할 타이밍.

$RDW: Space-Grown Organs Could Transform Transplantation Industry Within A Decade

Redwire and a handful of aerospace and biotech firms are advancing tissue and organ science aboard the International Space Station, pursuing experiments that aim to turn microgravity into a platform for growing complex human tissues. The work focuses on scaffolding, cell maturation and vascularization, key barriers for any future organ transplant.

Industry proponents say that, if current trajectories hold, within 10 years researchers could demonstrate the ability to grow transplantable tissues or whole organs in orbit, a development that would upend current organ donation systems.

That projection has made space-based biomanufacturing a central talking point at industry and policy meetings, framed as both a scientific milestone and a potential public-health turning point.

The implications reach beyond laboratory benches. Space-grown organs could reshape transplantation logistics, reduce reliance on donor availability and change organ procurement pathways now integral to transplant networks. Advocates also highlight the economic promise: new markets for in-orbit tissue production, manufacturing services on the ISS and downstream clinical translation on Earth.

Significant hurdles remain, rigorous clinical trials, regulatory approvals, scaling from experimental tissues to clinically safe organs, and the ethics and infrastructure of producing human tissues in space.

Still, researchers and companies pressing experiments in low Earth orbit argue the stakes justify accelerated coordination between space agencies, regulators and transplant medicine, with cautious optimism that the work could fundamentally change life on Earth and how transplantation is practiced.

https://t.co/64As6zPi23