New Post out on $FEVR.LN

TLDR: Market too pessimistic on long term growth prospects, margin recovery and portfolio adaption potential. I see a ~16% IRR from today's price. Full report linked below let me know of any feedback, questions or comments on the report.

https://t.co/jpyjezGW9u

When it comes to investing in a new technology, the hard question is rarely whether that new technology will create incredible opportunities for society

Instead, the question is whether that opportunity will specifically accrue to the shareholder, or to the customer

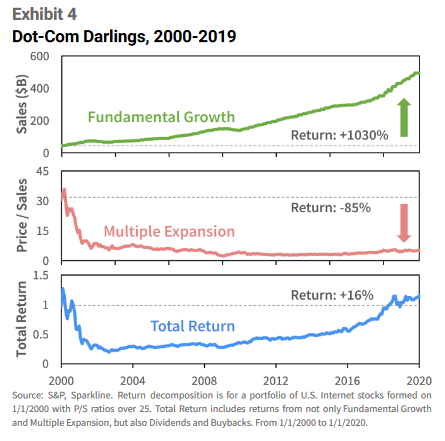

Really, really, really good chart from Sparkline Capital

Even if you grow revenue/earnings by 1000% over two decades, multiple contraction is likely to kill you if you overpay

Shouldn't come as a surprise to anyone but it just bears repeating

$NVDA

$IWG is the most mispriced business I own. If it was listed in the US, I think stock would be 2x current levels.

13x run-rate FCF isn't the lowest valuation by any means - but the cos managed partnership model has found product market fit and is starting to meaningfully inflect.

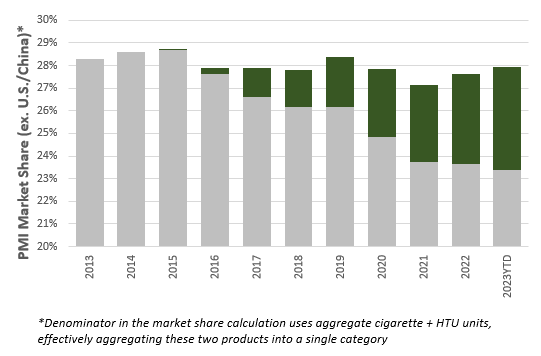

That's true, but it's also been the case for a long time, and all that's really happened so far is that their HTU share has cannibalized their ciggy share (see graph). I think they are probably moving on to a point where they'll capture combined share, but then it's a question of whether or not they'll maintain 75% share in heat-not-burn (not so sure that's sustainable, even if it does remain higher than their ciggy business) and how much the combined categories shrink (and they are shrinking still).

But ya, I take your point - not saying aggregate revenue halves in 5 years, but rather that it's hard to see how there is significant growth given all these dynamics (in particular if the excise tax spread were to narrow)

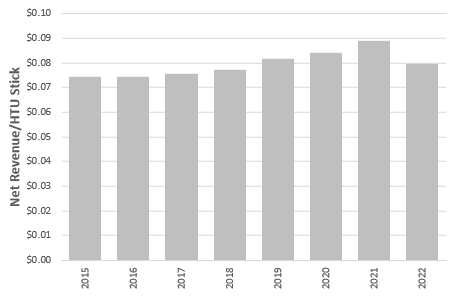

Imo it'll be hard to pass through higher excise taxes to end consumers - a big part of the strategy is to convert existing smokers to HTUs, but they are currently priced (at retail) close enough. I don't think they'd aim to price HTUS at 40% above cigs. I think that explains why net revenue per stick FELL in 2022 on the back of higher HTU excise taxes in Japan/Germany (they didn't pass through price).

Some of the early adopters of HTUs are closing the gap - I think Germany/Japan are now (like as of last year) taxing HTUs at 80-85% the rate of ciggies (those two countries represent ~33% of PM's HTU sales, and with the tax increase PM's net/rev per HTU was down 11% last year, and should be down a bit more this year) - if more countries follow that lead, it's a pretty big headwind to growth

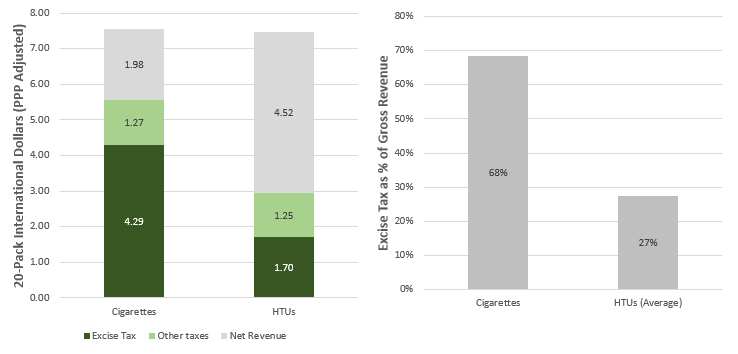

@BillBrewsterTBB 1 thing that scares me about $PM is risk that excise tax spread between cigarettes and HTUs narrows - today, net revenue/stick is ~2.5x higher for HTUs vs cigs- not because gross revenue/stick is higher, but because excise taxes are just ~40-45% of where they are for cigarettes.

(2/2) I think I have a differentiated view relative to implied expectations about the value of that smoke-free portfolio – in particular how HTU excise taxes might change. I walk through that in the piece.

(1/n) 3rd post out on $FLT today. It’s a fantastic payments success story. Ron Clarke, took this business from near bankruptcy to a successful IPO in 2010. Then compounded revenues at an 18% CAGR into 2022. Adj EPS grew at a 20% CAGR.

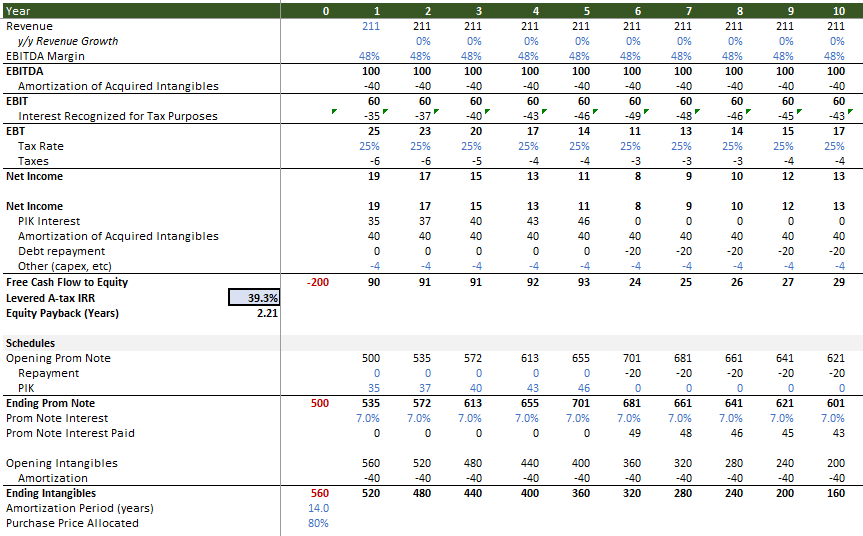

@wlep Sorry, I should say "the EBITDA we know *existed*" - that could have fallen for sure if there is lots of volume-linked rev, which is why I also ran the math assuming EBITDA fell from $100mn to $70mn

$CSU Optimal Blue deal looks wild. If that $100mn of EBITDA (T12M to Feb) is maintained, that's a levered a-tax IRR of nearly 40%. Even if EBITDA fell 30% (and never recovered) I'd get a levered a-tax IRR of 23%. Dayummmmmm

Good catch (the $211 was a guess - I took the EBITDA we know exists and just tossed on the margin I thought they were getting). Either way, I think this business has both A) recurring subscription revenue and B) volume-linked revenue, although it's not clear to me how much is tied to volume for Optimal Blue specifically