@BertilleBayart Le programme du NFP n’est pas applicable dans son ensemble vu les résultats, les partis pro européens sont majoritaires (baisse du risque de redenomination) et le risque RN est écarté à court-terme donc plutôt positif pour le spread

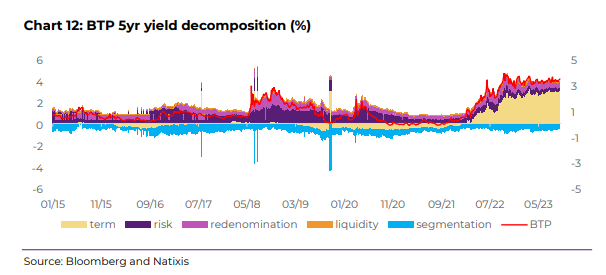

🇮🇹🇪🇺 Sovereign bond market : Italy: Is the stability of sovereign spreads sustainable for Q4-2023?

Market insight available for @NatixisResearch clients

Thread : 1/7

We’re still of the view that positive factors are still supportive for BTPs: (1) the carry is still very attractive, (2) the third tranche of the NGEU program has been validated by the European Commission, (3) net supply issuance for Q4 is negative. 6/7

@fwred Hawkish pause in September looks the smartest solution with a risk management approach and the market seems to buy this idea. Centrist speechs as Villeroy (next week) will be key ?

@zhenyuwu1990 Les hawks vont pousser là dessus à l’automne surtout si la BCE a terminé son cycle de hausse de taux. Toutefois, ce sujet du QT sur le PEPP se fera uniquement s’il n’y pas de volatilité sur les BTPs. Mais il faut quand même séparer le PEPP de l’objectif d’inflation.

On parle des implications d'un Quantitative Tightening sur le PEPP qui sera un sujet pour la fin d'année/début 2024. @NatixisResearch

👉 La BCE explore les différentes pistes pour réduire son bilan https://t.co/gyuqmxK7ch via @AgefiFrance

@joosteninvestor @RobinBrooksIIF The resilience of the spread is mainly explained by strong nominal growth at the moment (which allows for a degree of debt sustainability), strong appetite from retail investors and a relative political stability 2/2

@joosteninvestor @RobinBrooksIIF I don't necessarily agree on the illusion: the large part of the deviation from the capital key on BTPs took place in July 2022 when there was volatility on BTPs (Draghi resignation), not afterwards. 1/2