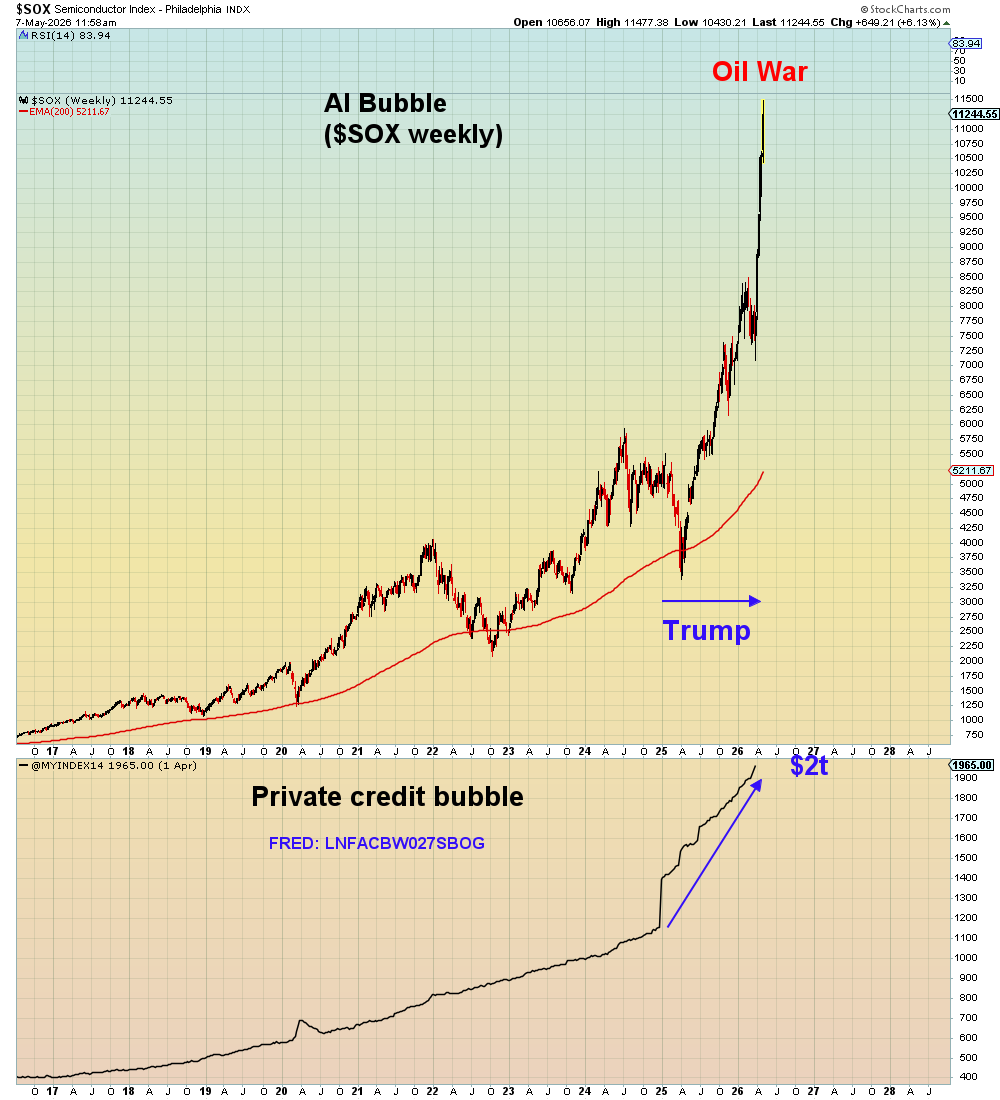

This is the chart that everyone should be watching.

If the Token Pricing rolls over, everything from the memory trade to the broader hard-ware and data-centre trade is over for this cycle imho.

The whole setup depends on this..

Thoughts from Michael Hartnett, BofA | This Is The Biggest Bubble Since The Railroads

The current AI-driven market rally resembles one of the biggest speculative bubbles in history, comparable to the Nifty Fifty or dot-com era, but investors are unlikely to aggressively sell before two catalysts occur: a major OpenAI/SpaceX-style IPO cycle and a clear Fed policy tightening shock tied to rising CPI from tariffs and inflation.

•AI mega-caps now dominate market concentration, with the “AI bubble” larger than past railroad, Japan, and dot-com bubbles by some metrics.

•Bond yields are the main warning signal: the rise in long-term yields and global cost of capital seen as dangerous for risk assets, especially leveraged consumers, private equity, housing, and emerging markets.

•Several macro stress signals are flashing: weak Asian currencies (KRW, JPY, INR, IDR), widening high-yield spreads, EM outflows, and BofA’s Bull & Bear Indicator hitting a contrarian “sell” level.

•Historically, speculative IPO waves (Alibaba, NTT, Visa, etc.) often marked medium-term market tops rather than immediate crashes.

•Current gains are very narrow (“wealth effect, not wage effect”), while equal-weight consumer stocks remain weak versus the S&P 500.

•Despite near-term bubble concerns, structurally bullish on emerging markets and commodities.

•Preferred post-bubble opportunities would be consumer stocks and smaller AI adopters/disruptors rather than dominant mega-cap AI platforms.

•Geopolitics, energy, AI competition with China, and inflation are increasingly interconnected themes shaping markets.

Zeitgeist quote: “Everyone is now convinced that equities are the best inflation hedge.”

Feedback from recent London trip, main soundbites:

•“we’re long and paranoid,”

•“wants/needs to de-escalate Iran, and stocks pop, yields drop on deal,”

•“if UK gilts find love, everything finds love,”

•“European electorate shifting decisively right, Farage in UK, Le Pen in France, and you watch the AfD in Germany will win Saxony-Anhalt in September, their first state election,”

•“the fear in bonds is nowhere near as strong as greed in equities,”

•“Warsh will be rhetorically hawkish but practically dovish over the summer,”

•“US actions in Venezuela, Ukraine, Iran, Greenland, Cuba should be viewed through single strategic lens competition with China in AI, which can only be won by securing access to critical resources.”

🦔Fortune published a piece this afternoon connecting Microsoft and Uber's AI cost overruns to token economics, with a headline that lands hard: "Microsoft reports are exposing AI's real cost problem: Using the tech is more expensive than paying human employees." Underneath those headlines, the unit economics tell the story. OpenAI is projected to lose $14 billion in 2026, spending roughly $2 for every dollar of revenue it brings in. Anthropic is in a similar position with break-even not projected until 2028. GPU rental prices for Nvidia's newest Blackwell chips jumped 48% in just two months. OpenAI's response was to close a $122 billion private funding round at an $852 billion valuation, the largest in history.

My Take

The token pricing story is really an IPO timing story. OpenAI, Anthropic, and xAI all need to go public in the next 18 to 24 months because the private market cannot keep absorbing burn rates like these indefinitely. Public markets do not accept "we will figure it out" as a line item on an S-1, they require disclosed unit economics with a credible path to profitability and a date attached. That deadline is why the price increases are happening now rather than next year. The labs need to show declining loss curves before the filings hit, and that means enterprise customers have to start covering more of the actual cost regardless of whether the productivity math holds on their end.

Every token bought over the last two years was effectively subsidized below cost by venture capital and hyperscaler cross-subsidies, and that subsidy has a hard deadline. Uber publicly admitted burning through its entire 2026 AI budget in four months, and CFOs at major enterprises are starting to flag the same pressure. The labs cannot keep losing $2 per dollar of revenue once they file public statements, so the cost transfer to customers accelerates from here. For investors, the question is not whether these companies are valuable. They clearly are. The question is who absorbs the difference between what enterprises can budget and what the models actually consume between now and 2028, and right now the answer is the hyperscalers funding the buildout. That is why I have been watching Microsoft and Amazon capex commentary more closely than the lab announcements themselves.

Hedgie🤗

Link: https://t.co/S2oIgUSijV

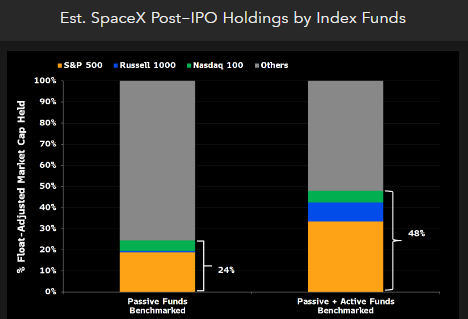

Passive S&P 500 funds could have to buy roughly 19% of public SpaceX shares within 6mo under fast-tracking framework (it would enter the index at the est 6th spot), Russell 1000 and Nasdaq 100 may buy another 5.5% within weeks of the IPO. Thrown in active MFs benchmarked to those indices and you get to HALF of SpaceX shares. Nice study from my colleague @rduboff

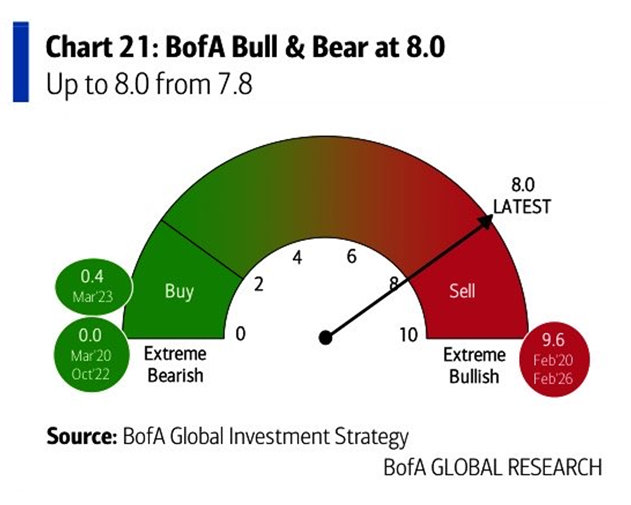

🔴BofA Bull & Bear indicator is screaming SELL again:

This metric rose to 8.0 this week, up +0.4 points, triggering a sell signal for equities for the first time since February 2026.

The indicator has surged +1.7 points over the last 4 weeks, driven by tech and emerging market debt inflows, a record monthly increase in fund manager equity allocations, and a drop in cash levels to 3.9%.

5 of the indicator's 6 components are now bullish or very bullish, with none being bearish.

Historically, there have been 17 sell signals since 2002, with global stocks averaging a loss of -2% to -3% over the following 2 to 3 months, and maximum drawdowns of -15% to -20%.

Investor euphoria is now almost everywhere.

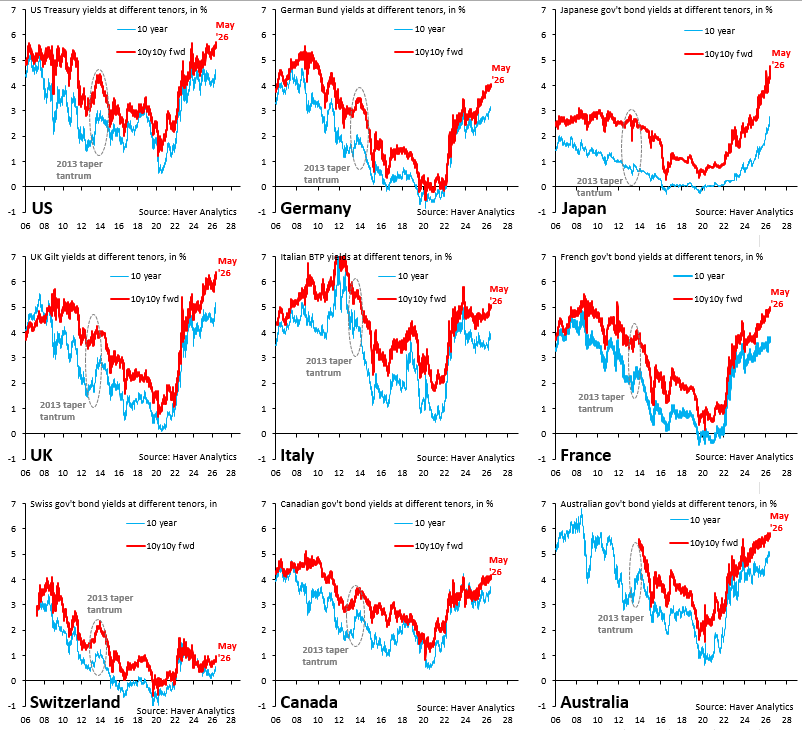

We've officially reached the "brutal" stage in the global bond market sell-off. The 10y10y forward yield (red) is making new highs all over the place. Japan's 10y10y forward has risen 30 basis points in just a few days. Even Swiss 10y10y forward is rising.

https://t.co/wLyQataCjN

🇺🇸🇨🇳

Trump left Beijing empty-handed: no agreement on Iran, no concessions on Taiwan, no H200 deal, no decision on rare earth trucks, no release of Jimmy Lai, and fewer Boeing aircraft orders than expected. Only warm words and a banquet in which Trump kept praising Xi. He came looking for leverage, and they gave him hospitality. Beautiful.

🚨🚨ALERT | SPY OPEX GAMMA DECAY | Friday May 8

Today's 2 PM snapshot showed record GEX of +$1.39B. By 4 PM, 27.9% of the gamma cushion expired.

$737.62 close. SPY rallied 2.4% this week. The gamma blanket kept thinning anyway.

Friday's weekly OPEX drained 27.9% of the gamma cushion. 1.75M gamma shares and 25.58M delta shares expired tonight. That's nearly identical to last Friday's 25.5% rolloff. Two consecutive weeks of quarter-plus gamma loss.

What survived: +4.51M net gamma. Still positive. Still suppressing. But the cushion was 6.26M this morning.

May 15 is 7 days away.

Monthly OPEX carries 24.3% of remaining gamma. 3.96M contracts. 1.10M gamma shares sitting on a single expiration. When that rolls off, 59.4% of the gamma that existed this morning is gone.

The math after May 15: surviving gamma drops to +2.54M. That's the thinnest gamma blanket since the rally started in mid-April.

The rally doesn't change the structure. Price moved higher but the options-based suppression that keeps ranges tight is decaying on schedule. Higher price with thinner gamma means the NEXT selloff, whenever it comes, has less structural resistance to fight through.

Volatility stays compressed until the cushion is gone. When it's gone, the range expands whether the move is up or down.

May 15 is the structural cliff. The calendar doesn't care about the rally.

$SPY $QQQ $VIX $SPX

Everyone knows that AI is an environmental disaster due to data center electricity and water consumption.

Everyone knows that AI is an economic disaster, because it destroys jobs AND it steals content.

Everyone knows that AI is a financial disaster due to the circular financing deals and the massive credit market issuance.

And yet, it's still the number one trade on Wall Street.

Investors are rushing to throw all of their money into an economy killing machine at the end of the cycle.

AI is where money goes to die.

Five companies are spending more money in a single year than most countries produce in a decade, on infrastructure they cannot plug in.

In Q1 2026 earnings, Amazon guided $200 billion in capital expenditure. Alphabet guided $175 to $190 billion. Meta raised its range to $125 to $145 billion. Microsoft is tracking $120 billion or more. Oracle committed $50 billion. Combined: $700 to $725 billion in 2026. In 2024, the same companies spent $200 billion. Tripled in two years. Amazon’s capex alone exceeds the entire US energy sector’s annual spending. Capital intensity has hit 57% of revenue at Oracle, 45% at Microsoft. These are no longer technology companies. They are infrastructure companies building a new physical layer of civilization on top of a grid that cannot support it.

The binding constraint is no longer chips, capital, or demand. It is electricity. Microsoft disclosed an $80 billion backlog of Azure orders it cannot fulfill because the power grid cannot deliver the electricity to run them. Goldman Sachs documents a US data center capacity shortfall exceeding 11 gigawatts today, widening to 40 gigawatts by 2028. The US interconnection queue, the line of projects waiting to connect to the grid, holds 1.4 to 2.6 terawatts of pending capacity with median wait times of four to five years. Power transformer lead times have stretched to 128 weeks. The companies spending $700 billion on AI compute are building data centers faster than the grid can energize them.

The revenue is real and accelerating. Microsoft’s AI annual run rate hit $37 billion, up 123% year over year. Google Cloud surged 63% to $20 billion. AWS grew 28%, its fastest in 15 quarters. But the revenue-to-capex ratio remains below 0.3. For every dollar of AI revenue, more than three dollars of capex is deployed. The question is whether this is the early phase of a general-purpose technology cycle where returns diffuse over decades, or the largest capital misallocation in market history.

Q4 2026 earnings will be decisive. If the revenue ratio lifts above 0.3 with margin expansion and sustained 2027 guidance, the bear case collapses. If ratios compress and free cash flow stays negative, the cycle confirms as the largest overbuild since the 1990s telecom buildout.

But one trade survives both outcomes: power. If AI succeeds, electricity demand explodes for decades. If AI fails, the data centers are already built, the power purchase agreements already signed, and hundreds of billions in committed infrastructure will consume electricity regardless of whether the compute generates revenue. The GPU may depreciate. The kilowatt-hour does not.

China controls 69 to 70% of global rare earth mining and 85 to 90% of processing. The magnets inside power transformers, the components of grid infrastructure these data centers depend on, flow through Beijing. China added 543 gigawatts of generation in a single year. The United States has a 2-terawatt queue and a five-year wait. The Strait of Hormuz blockade is raising energy costs during the largest electricity demand surge in modern history. Goldman forecasts global data center power demand reaching 1,350 terawatt-hours by 2030, up 220% from 2023, with the US consuming roughly 60% of that total. That forecast assumes energy prices that no longer exist.

The screen says $700 billion in AI investment. The grid says the electricity is not there. The gap between those two numbers is the trade.

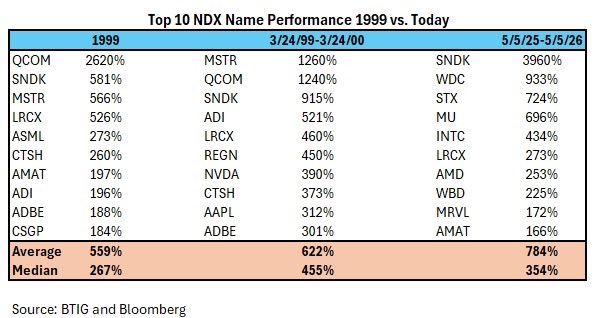

Great commentary yet again from BTIG’s Jonathan Krinsky

•Party Like It's 1999. In 1999, the best performing Nasdaq 100 stock was Qualcomm (QCOM, not rated), up 2600%. The best rolling 52-wk return for QCOM during the entire dot-com bubble was 2600%, so SNDK is beating that by 1300bps. Interestingly, the second-best stock in 1999 was SNDK up 581%.

•More Extreme. If we look at the top 10 performing NDX stocks in 1999, they were up an average of 559%. The top 10 in the year leading up to 3/24/00 were up an average of 622%. The top 10 NDX names over the last year are up an average of 784%, beating both the dot-com periods..

⚠️The AI arms race is destroying Big Tech's cash generation:

Combined free cash flow across Microsoft, Amazon, Alphabet, Meta, and Oracle peaked at ~$300 billion in late 2024 and is expected to fall to near ZERO in 2026.

As a result, free cash flow margins at Microsoft, Meta, Alphabet, and Amazon are expected to fall to ~16%, ~3%, 0% and -2%, respectively, by 2027.

Free cash flow is collapsing under the weight of ~$715 billion in combined 2026 capital expenditure, up more than +70% from 2025's already-record levels.

Free cash flow is simply the cash a company has left after paying for its operations and investments, and right now, AI spending is consuming nearly all of it.

To plug the gap, hyperscalers have turned to the debt markets at an unprecedented pace, with Bank of America forecasting around $175 billion in investment-grade issuance in 2026, significantly above pre-AI cycle levels.

At the same time, share buybacks have slowed materially from 2024–2025 peaks: Meta sharply reduced repurchases in early 2026, while Alphabet, Microsoft, and Amazon have all scaled back relative to prior years.

This creates a rising risk of a broader equity market selloff, as weaker free cash flow reduces valuation support while higher debt issuance and the loss of buyback demand remove major structural buyers of US equities.

The AI buildout is being funded by debt, not profits, and the bill is only getting bigger.

🚨🚨🚨ALERT | SPY CLOSE | Friday May 1

$720.65. Shooting star on the daily. Here's what the structure and the pattern say together.

The candle: 4/5 shooting star. Long upper wick (3.62 vs 0.60 body), close in the lower 4.1% of the range. Price hit $724.37 and reversed hard into the close. The one miss: no confirmed uptrend over 3% in the prior 5 bars, which keeps it at moderate rather than strong.

The history: 33 prior shooting stars on SPY. 75.8% resulted in a decline of 2% or more. Average decline: -6.52%. Average time to max decline: 15 days. Three COVID patterns excluded.

The structure confirms the warning:

GEX dropped from +$960M at 2 PM to +$263M at the close. The gamma blanket lost 73% of its strength in the final two hours. Near-term GEX is barely positive at +$79M.

Dealers short 124.8M shares. Was 151.8M at 2 PM. Dealers sold 27M shares into the close. The engine shrank 18% in two hours.

Daily flow flipped: -15.7M shares. Was +25.2M at 2 PM. The afternoon session reversed the morning entirely.

Net premium flipped: -$185M into puts. Was +$532M at 2 PM. A $717M swing in two hours.

Composite dropped from +26.7 to -9.1. A 36-point intraday collapse. On the first day of May.

GEX flip: $713. Only 1.1% below. The thinnest cushion since the rally started.

Our read for early next week:

The shooting star says lower. The flow confirms it. The gamma confirms it. The pattern's historical average is -6.52% over 15 days. From $720.65, that targets $673-$675, right at the GEX flip zone.

We're not predicting a 6.5% decline. We're saying the pattern, the flow reversal, the gamma drain, and the dealer selling all point the same direction for the first time since the April 21 ceasefire scare.

$713 is the first test. If it breaks, $700 accelerator at -$115M is the next stop. The magnets at $725 and $730 need a headline to pull price back up. The structure won't do it alone from here.

Defensive into Monday. Let the pattern confirm or fail before adding exposure.

$SPY $QQQ $VIX

Paul Tudor Jones says the US is more dependent on equity prices than ever, and explains what a 35% correction would trigger in the economy:

"We're 252% of stock market cap to GDP. In 1929 we were 65%. In 1987 we got to ~85-90%. In 2000, 170%.

If you think about the periodicity of significant bear markets. Since 1970, we get a mean reversion about every 10 years.

Let's say mean revert to the past 25 or 30-year PE. That would be a 30, 35% decline. Well, 35% on 250% of GDP is 80, 90% of GDP.

10% of our tax revenues are capital gains, they go to zero. So you can see the budget deficit blowing up. You can see the bond market getting smoked. You can see this kind of negative self-reinforcing effect.

In the stock market, we're over-equitized as a country. We have the highest individual equity weightings in the history of the country.

And then the real problem is if you look at private equity in 2007-2008, that was about 7% of institutional portfolios. Now it's about 16% of the institutional portfolios. We're so much more illiquid than we were in 2008.

The problem is that if you buy the S&P at this current valuation, the 10-year forward return is negative when you buy the S&P with a PE of 22. That's what history shows.

So yes, the S&P is spectacular long-term, if you have a hundred-year view. But that's because that's an average of a hundred years, including times when the S&P 500 PE was 6, 7 and 8, or one third of what it is right now.

Valuation matters a lot, and the stock market's really high and it's gonna be really hard to make money from here with any kind of long-term view."

Shocking stat of the day:

AI-related stocks now reflect a record 45% of the S&P 500's market cap.

This percentage has surged +20 points since November 2022, when ChatGPT was launched.

Furthermore, a record 15.4% of investment-grade debt is now tied to AI, making it the largest sector in the US credit market.

This percentage has risen +3.5 points since 2020.

This comes as AI-linked debt has nearly DOUBLED over this period to an all-time high of $1.4 trillion.

Never before has a single theme dominated both US equity and credit markets to this magnitude.

🚨 S&P 500 IS PREPARING FOR A MAJOR DROP...

The "megaphone" pattern is reaching its peak

Stages 1-5 have played out successfully ✅

Stage 6 is now setting up - downside move looks inevitable

Something big is coming soon - turn on notifs, I’ll update

![burrytracker's tweet photo. Breaking: Leopold Aschenbrenner just filed his Q1 2026 13F

Here's everything you need to know about his recent 13F

Top 10 positions:

1. VanEck Semiconductor ETF $SMH [Put] — $2.04B

2. Nvidia $NVDA [Put] — $1.57B

3. Oracle $ORCL [Put] — $1.07B

4. Broadcom $AVGO [Put] — $1.01B

5. Advanced Micro Devices $AMD [Put] — $969M

6. Bloom Energy $BE — $879M

7. SanDisk $SNDK — $724M

8. Micron $MU [Put] — $584M

9. CoreWeave $CRWV — $556M

10. Taiwan Semiconductor $TSM [Put] — $535M

New positions:

• $SMH, $NVDA, $ORCL, $AVGO, $AMD, $MU, $TSM, $ASML, $INTC, $GLW — all puts

• $MU [Call] — $422M

• $TSM [Call] — $355M

• $SNDK [Call] — $389M

Biggest adds:

• CleanSpark $CLSK: +648% shares

• Riot Platforms $RIOT: +87% shares

Biggest trims:

• CoreWeave $CRWV [Call]: -83% shares

• Bloom Energy $BE: -36% shares

Full exits:

• Intel $INTC [Call] — was $747M

• Lumentum $LITE — was $479M

• EQT Corp $EQT — was $133M

• Tower Semiconductor $TSEM — was $85M

Summary: He kept his AI infrastructure longs and opened $8.45B in new puts against tech and semiconductor](https://pbs.twimg.com/media/HImdd4AWkAAzOqm.jpg)

![burrytracker's tweet photo. Breaking: Leopold Aschenbrenner just filed his Q1 2026 13F

Here's everything you need to know about his recent 13F

Top 10 positions:

1. VanEck Semiconductor ETF $SMH [Put] — $2.04B

2. Nvidia $NVDA [Put] — $1.57B

3. Oracle $ORCL [Put] — $1.07B

4. Broadcom $AVGO [Put] — $1.01B

5. Advanced Micro Devices $AMD [Put] — $969M

6. Bloom Energy $BE — $879M

7. SanDisk $SNDK — $724M

8. Micron $MU [Put] — $584M

9. CoreWeave $CRWV — $556M

10. Taiwan Semiconductor $TSM [Put] — $535M

New positions:

• $SMH, $NVDA, $ORCL, $AVGO, $AMD, $MU, $TSM, $ASML, $INTC, $GLW — all puts

• $MU [Call] — $422M

• $TSM [Call] — $355M

• $SNDK [Call] — $389M

Biggest adds:

• CleanSpark $CLSK: +648% shares

• Riot Platforms $RIOT: +87% shares

Biggest trims:

• CoreWeave $CRWV [Call]: -83% shares

• Bloom Energy $BE: -36% shares

Full exits:

• Intel $INTC [Call] — was $747M

• Lumentum $LITE — was $479M

• EQT Corp $EQT — was $133M

• Tower Semiconductor $TSEM — was $85M

Summary: He kept his AI infrastructure longs and opened $8.45B in new puts against tech and semiconductor](https://pbs.twimg.com/media/HImdgEMXcAApr8J.jpg)