$SYRUP : Review 📜

What if the fastest-growing corner of traditional finance, private credit, could be rebuilt onchain with every loan, every borrower, and every piece of collateral verifiable in real time?

Meet Maple Finance, DeFi's institutional lender. $7B+ in loans originated, a 99% repayment rate, and ~$2B+ in TVL, with institutional borrowers posting Bitcoin and Ethereum as collateral and lenders earning fixed-rate, overcollateralized yield.

Through Syrup, that institutional-grade yield is now permissionlessly available to all of DeFi.

Let's explore how Maple is bringing capital markets onchain. 👇

⚪ Maple at a Glance

Maple Finance is an onchain institutional lending marketplace that connects institutional borrowers with lenders seeking high-quality, overcollateralized yield. Unlike retail-focused DeFi, Maple applies traditional credit underwriting, active collateral management, and institutional custody (Anchorage, BitGo, Zodia) while keeping every loan and collateral position verifiable onchain.

The protocol runs two layers. Maple is the permissioned, institutional-grade marketplace for accredited allocators. Syrup is the permissionless product that opens the same yield to DeFi natives through syrupUSDC and syrupUSDT, liquid yield-bearing dollars integrated across Pendle, Balancer, Morpho, and other major protocols.

The $SYRUP token governs the ecosystem and captures value through buybacks.

Marketplace Insight: Maple sits at the intersection of three of the strongest trends in finance: the explosion of private credit as banks retreat from corporate lending, surging stablecoin adoption, and Bitcoin's acceptance as institutional collateral. CEO Sidney Powell frames the ambition as building "a new version of an Apollo or an Ares" for the onchain era. With real revenue, real loan performance, and a buyback mechanism tying protocol growth directly to the token, Maple is one of the few RWA-adjacent projects where the fundamentals are measurable rather than theoretical.

⚪ Mission

Maple's mission is to bring capital markets onchain. By combining the underwriting discipline of traditional finance with the transparency and efficiency of smart contracts, Maple aims to become the dominant institutional credit layer of DeFi, serving institutions that want capital and allocators that want high-quality yield, all on a verifiable, programmable infrastructure.

🔵 A Brief History

Maple was founded in 2019 by Sidney Powell and Joe Flanagan, who met at a commercial lending fintech and shared a background in institutional banking and debt capital markets. Powell had participated in $3B+ of corporate bond issuance and run a $200M+ bond funding program. Their original idea was to tokenize bonds, but with no market for that at the time, they pivoted Maple toward institutional lending.

The protocol launched its lending marketplace in 2021 with the MPL token, initially offering uncollateralized loans to crypto-native institutions like trading firms and market makers. The 2022 credit crisis, which hit much of crypto lending hard, pushed Maple to overhaul its risk model and move decisively to overcollateralized lending backed by large-cap assets.

In May 2024, Maple launched Syrup, a permissionless gateway that let any DeFi user access yield sourced from Maple's institutional loan book through syrupUSDC. In late 2024, following a community vote, the legacy MPL token migrated to SYRUP at a 1:100 ratio with no additional dilution, and by May 2025 the team consolidated all products under the unified Maple brand with the token as its sole asset.

October 2025 brought a pivotal tokenomics change. Governance voted to end staking emissions and shift to a buyback model, directing 25% of protocol revenue into the Syrup Strategic Fund to buy back and retire tokens. The first buyback executed in December 2025, retiring 2 million tokens using a quarter of November revenue.

2026 has tested and strengthened the protocol.

A Cayman Islands court issued an injunction blocking the syrupBTC launch over an exclusivity dispute with Core Foundation, which Maple later settled. During an April 2026 DeFi exploit involving compromised rsETH collateral, Maple confirmed no direct exposure (the asset was never approved by its Risk Committee) and exited indirect positions within 24 hours. In May 2026, Maple launched Proof of Reserves for syrupUSDC and syrupUSDT with The Network Firm, and the token expanded to Revolut's 70M+ users across the UK and EU.

🔵 Ecosystem Narrative

Maple's ecosystem is built on one principle: institutional credit discipline and DeFi transparency are not opposites, they are complementary, and combining them unlocks a category neither side could build alone.

Key dynamics include:

➛ Overcollateralized institutional lending. Maple lends to vetted institutions (trading firms, market makers, miners, family offices) with loans typically from $5M to $100M, collateralized above 100% by Bitcoin, Ethereum, and other large-cap assets, with conservative margin call and liquidation levels.

➛ Syrup as the DeFi gateway. syrupUSDC and syrupUSDT let any non-US user deposit stablecoins and earn institutional yield, packaged as liquid, composable, yield-bearing dollars usable across Pendle, Balancer, and Morpho.

➛ Active risk management. A dedicated Risk Committee approves collateral types, and the Maple Direct team actively manages loan health through real-time monitoring, margin calls, and liquidations, which is why the protocol has maintained a 99% repayment rate across $7B+ originated.

➛ Buyback flywheel. 25% of protocol revenue funds the Syrup Strategic Fund, which buys back and retires tokens, tying protocol growth directly to token scarcity. This replaced the old staking-emissions model in late 2025.

➛ Institutional custody and transparency. Collateral is held with Anchorage, BitGo, and Zodia, and Proof of Reserves through The Network Firm gives lenders independent verification that every loan is fully backed.

➛ Multi-chain and product expansion. Maple deploys where liquidity is deepest (Ethereum, Solana, with BNB Chain onboarding), and is building out products like syrupBTC to expand its addressable market.

➛ Mainstream distribution. The Revolut listing in April 2026 bridged Maple's onchain credit yield to a mainstream fintech audience of 70M+ users, a meaningful step beyond crypto-native distribution.

⚪ Token Utilities

$SYRUP is the governance and value-accrual token of the Maple ecosystem:

➛ Governance: Holders vote on protocol decisions, risk parameters,

product direction, and treasury management, including the tokenomics changes that reshaped the model.

➛ Revenue-Funded Buybacks: 25% of protocol revenue flows to the Syrup Strategic Fund to buy back and retire tokens, creating deflationary pressure tied directly to protocol performance.

➛ Ecosystem Access: The token underpins the Syrup product, the gateway to permissionless institutional yield, and integrates with DeFi protocols like Balancer and Pendle.

➛ Alignment: After the October 2025 shift away from staking emissions, value accrues to holders through buybacks rather than dilutive rewards, aligning the token with sustainable revenue.

➛ Distinct from Yield Tokens: The governance token is separate from syrupUSDC and syrupUSDT, which are the yield-bearing dollar instruments, keeping governance and yield cleanly separated.

⚪ Key Features

➛ Institutional Lending Marketplace: Overcollateralized, fixed-rate loans to vetted institutions, with $7B+ originated and a 99% repayment rate.

➛ Syrup Permissionless Yield: syrupUSDC and syrupUSDT bring institutional yield to all of DeFi as liquid, composable assets.

➛ Onchain Transparency: Every loan, borrower, and collateral position is verifiable onchain, backed by Proof of Reserves via The Network Firm.

➛ Institutional Custody: Collateral held with Anchorage, BitGo, and Zodia, not self-custodied by the protocol.

➛ Active Risk Management: A Risk Committee and the Maple Direct team manage collateral health with conservative margin and liquidation levels.

➛ Revenue Buybacks: 25% of revenue retires tokens through the Syrup Strategic Fund.

➛ DeFi Composability: Deep integrations across Pendle, Balancer, and Morpho, plus mainstream reach through Revolut.

🔵 Meet the Maple Team

Maple is led by founders who came from institutional banking and debt capital markets, applying traditional credit discipline to onchain lending, backed by an engineering and product team building the infrastructure for institutional DeFi.

▶️ Core Members:

➛ Sidney Powell [ @syrupsid ] - Co-Founder & CEO | Australian entrepreneur with a background in debt capital markets and institutional banking. Participated in $3B+ of corporate bond issuance, ran a $200M+ bond funding program, and managed Treasury at a commercial lending fintech. Co-founded Maple in 2019 to bring debt capital markets onchain. Now based in Miami, leads strategy, institutional partnerships, and protocol expansion.

➛ Joe Flanagan [ @joe_defi ] - Co-Founder | Met Powell at a commercial lending fintech and co-founded Maple in 2019. Brings traditional finance and fintech experience to the protocol's lending model and operations.

➛ Matt Collum [ @fjordmatt ] - CTO | Leads engineering across Maple's core lending protocol, smart contract infrastructure, and the Syrup product stack.

➛ Ryan O'Shea [ @Ryanos_eth ] - COO | Runs operations across the Maple organization, coordinating institutional onboarding, risk processes, and go-to-market.

➛ Nayat Cheikh - Head of Product Design | Leads product design across Maple and Syrup, shaping the lender and borrower experience.

➛ Maple Direct & Risk Committee | The underwriting and risk function responsible for borrower diligence, collateral approval, and active loan management, central to the protocol's 99% repayment record.

🔵 Ratings

➛ Use Case: ★★★★✦ (4.5/5) - Maple is one of the clearest real-revenue businesses in all of crypto. $7B+ originated, a 99% repayment rate, ~$2B+ TVL, and a genuine product-market fit at the intersection of private credit, stablecoins, and Bitcoin collateral. The Syrup layer is a smart unlock, turning permissioned institutional yield into composable DeFi assets, while institutional custody and Proof of Reserves give it credibility most DeFi lenders lack. The handling of the April 2026 rsETH exploit (no direct exposure, fast exit from indirect positions) demonstrated the risk framework actually works. The 0.5-point deduction is for the inherent credit and counterparty risk of lending, the competitive pressure from other onchain credit players, and sensitivity to crypto credit cycles where a downturn could compress yields and loan demand simultaneously.

➛ Tokenomics: ★★★★ (4/5) - The October 2025 shift from staking emissions to a revenue-funded buyback model is exactly the kind of mature tokenomics evolution that aligns a token with real business performance. Directing 25% of protocol revenue into buying back and retiring tokens ties scarcity directly to protocol growth, and the first buybacks have already executed. The clean 1:100 MPL migration with no extra dilution was well handled. The 1-point deduction is for the infinite max supply structure (the buyback has to consistently outpace any emissions and unlocks to be net deflationary), the token's roughly 70% drawdown from its 2025 highs, and the reality that buyback strength depends entirely on sustained revenue, which compresses in weak credit markets.

➛ Audits: ★★★★✦ (4.5/5) - Maple has one of the strongest security profiles in DeFi, backed by a CertiK Skynet Score of 93.16 (AAA grade), one of the highest institutional ratings on the platform and on par with major L1s. The Maple-Core V2 protocol has undergone 7+ audits from top-tier firms including Spearbit/Cantina, Three Sigma, and 0xMacro, with the Syrup Router separately audited by Three Sigma. The protocol has operated lending infrastructure since 2021 through multiple market cycles, including the 2022 credit crisis, without a protocol-level smart contract exploit, and runs continuous invariant monitoring via Tenderly Web3 actions at every block with automated incident response. Proof of Reserves through The Network Firm adds independent verification that loans are fully backed, and institutional custody via Anchorage, BitGo, and Zodia reduces smart contract custody risk. The 0.5-point deduction is for the inherent credit and operational risk surface of lending (borrower default, collateral liquidity, custody integrity), which sits outside the smart contract layer, as the April 2026 rsETH episode showed even well-managed indirect exposure can introduce risk.

➛ Community: ★★★★ (4/5) - Maple has built a credible, institutionally respected community and brand, with strong exchange support (Coinbase, Upbit, and Revolut's 70M+ user base), genuine builder integrations across Pendle, Balancer, and Morpho, and a reputation as the serious institutional lender in DeFi. Sidney Powell is a visible, credible founder who communicates consistently. The 1-point deduction is that Maple's community is more institutional and yield-focused than retail-passionate, social engagement is modest relative to its TVL, and the deep token drawdown plus the syrupBTC legal episode tested holder conviction through 2026.

🔵 Conclusion

Maple Finance is one of the most fundamentally sound businesses in crypto, full stop. It is not promising future adoption or theoretical yield. It has originated over $7 billion in loans, maintained a 99% repayment rate across multiple market cycles, and built roughly $2 billion in TVL by applying real credit underwriting to onchain lending. In a sector full of narratives, Maple has a measurable, revenue-generating operation that looks more like a private credit fund than a typical DeFi protocol.

The token has evolved to match. The shift to a revenue-funded buyback model in late 2025 ties value directly to protocol performance, and the Syrup layer extends institutional yield to all of DeFi through composable, liquid assets.

Sidney Powell and Joe Flanagan have spent over six years building this patiently, surviving the 2022 credit crisis that wiped out many peers, and positioning Maple at the convergence of private credit, stablecoins, and Bitcoin collateral.

If capital markets are moving onchain, and private credit is the fastest-growing slice of traditional finance, then Maple is the most credible institutional lender building that bridge, with the revenue, track record, and tokenomics to back it. Powell wants to build the onchain Apollo. Few crypto projects have the fundamentals to make that ambition believable. Maple actually does.

Revenue Distribution will be a bigger part of the discourse around token valuations going forward.

So I created a spreadsheet to track valuations, rev generation, and distribution (I have around 172 projects generating real cash flows)

Here are the Top 15 Protocols by Annual Holder Revenue and their respective revenue % to holders:

- $HYPE 100.0%

- $PUMP 68.3%

- $AERO 100.0%

- $SKY 37.8%

- $CAKE 63.5%

- $JUP 50.0%

- $LINK 100.0%

- $EDGE 18.7%

- $AAVE 26.1%

- $ORE 99.0%

- $RAY 64.1%

- $CVX 98.1%

- $UNI 98.0%

- $LIT 40.3%

- $PENDLE 85.4%

Full link to the doc is in the comments.

The boring DeFi tokens are becoming the most interesting ones.

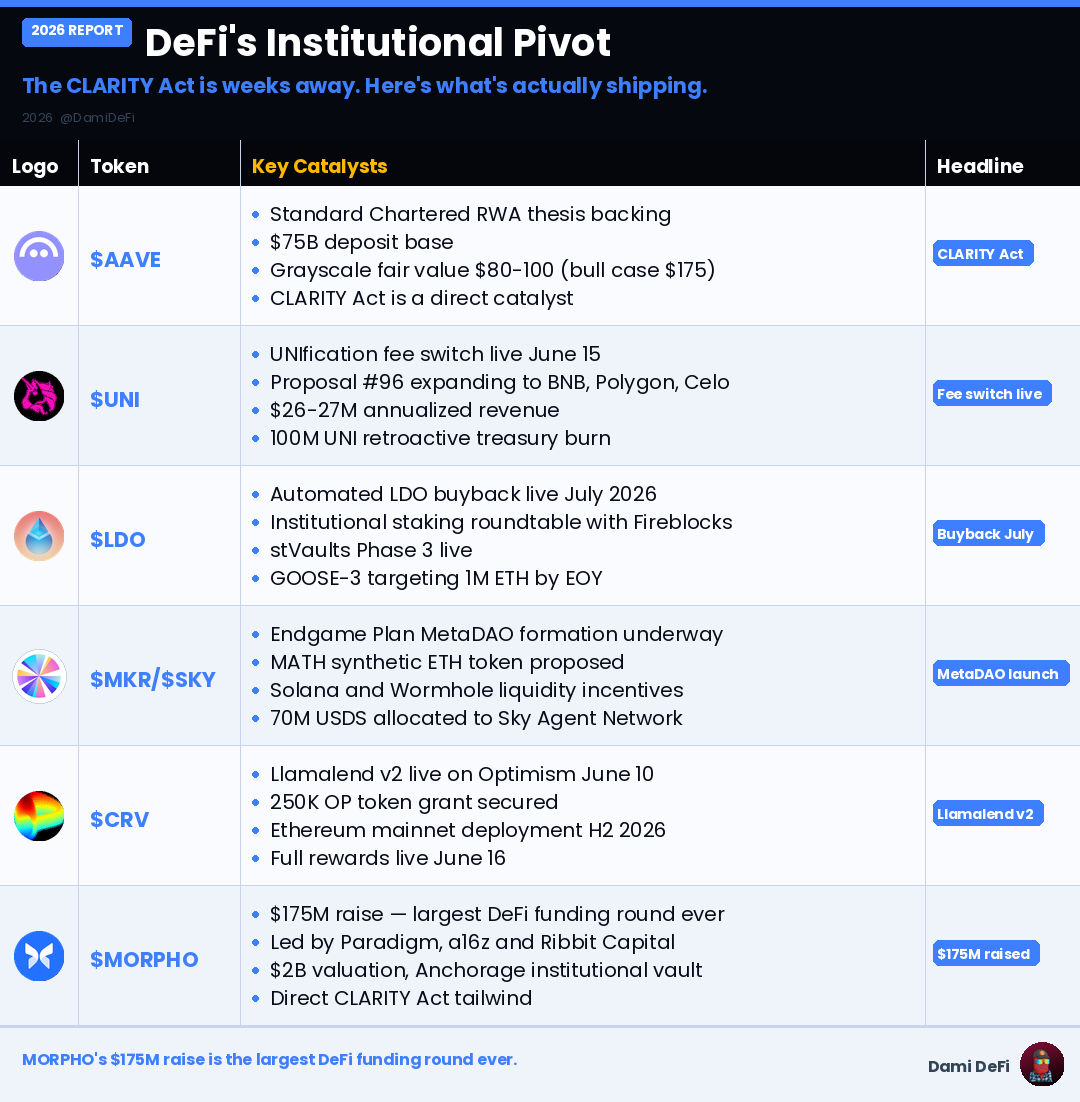

$UNI turned on its fee switch. $AAVE has $75B in deposits. $MORPHO raised $175M.

$AAVE: Standard Chartered RWA growth thesis, $75B deposit base, Grayscale $80-100 fair value (bull case $175), CLARITY Act catalyst, KelpDAO exploit response leadership

$UNI: UNIfication fee switch live June 15, Proposal #96 BNB/Polygon/Celo expansion, $26-27M annualized revenue, 4-5M UNI annual burn, 100M UNI retroactive treasury burn

$LDO: Automated LDO buyback live July 2026, institutional staking roundtable with Fireblocks, stVaults Phase 3 live, GOOSE-3 targeting 1M ETH by EOY, Wisp privacy product waitlist open

$MKR/ $SKY: Endgame Plan MetaDAO formation, MATH synthetic ETH token proposed, Solana and Wormhole liquidity incentives announced, 70M USDS allocated to Sky Agent Network

$CRV: Llamalend v2 live on Optimism June 10, 250K OP token grant, Ethereum mainnet deployment H2 2026, LlamaRisk auditor integration, full rewards live June 16

$MORPHO: $175M funding round (largest DeFi raise ever) led by Paradigm, a16z, Ribbit Capital, $2B valuation, Anchorage institutional vault access, fixed rate roadmap, CLARITY Act tailwind

The pattern across every protocol: fee mechanisms going live, institutional partnerships locking in, regulatory clarity approaching.

This isn't speculation anymore. This is infrastructure positioning for the next leg of institutional capital

Only a few DeFi projects do buybacks that exceed their token emissions.

In the past 90 days:

1. @HyperliquidX

• Bought back $135M worth of HYPE

• $64M HYPE was unlocked for its team

2. @chainlink

• Bought back $15M worth of LINK

• No LINK tokens were unlocked

3. @Uniswap

• Bought back $11.9M worth of UNI

• No UNI tokens were unlocked

4. @Lighter_xyz

• Bought back $6.4M worth of LIT

• No LIT tokens were unlocked (its unlocks start 1 year after TGE)

5. @JupiterExchange

• Bought back $5.7M worth of JUP

• No JUP tokens were unlocked (Jupiter passed a proposal to pause its token emissions)

6. @SkyMoney

• Bought back $3.3M worth of SKY

• No SKY tokens were unlocked (all its supply is already in circulation)

7. @Raydium

• Bought back $3M worth of RAY

• No RAY tokens were unlocked

Hyperliquid clearly dominates in terms of buybacks.

But what's great to see is that more and more projects have started to allocate a good chunk of their revenue to token buybacks.

DeFi is significantly more sustainable now than it was a few years ago.

Top 15 onchain apps by protocol revenue: $HYPE, $PUMP, $CAKE, $SKY, $JUP, $AAVE, $AERO, $WLFI, $LDO, $MET, $ETHFI, $LIT, $CARDS, $UNI, $RAY

Some of the top onchain apps by revenue have real cash flows, low overhead, and single-digit multiples, and with the CLARITY Act potentially weeks away, we believe investors are facing an attractive entry point today.

Read more from @LowBeta's latest Stack article here: https://t.co/34NkjZuPJF

New @DefiLlama dashboard is live!

This one covers the 4 spot DEXs represented in the DeFi20 Index:

@Uniswap $UNI

@AerodromeFi $AERO

@CurveFinance $CRV

@JupiterExchange $JUP

Over the past year, these 4 projects have generated:

- $1.47T in volume

-$1.49B in fees

- $289M in revenue

They also represent ~40%+ of the total market share of each of these metrics!

(The Machines & Money Portfolio owns all 4 of these tokens, plus additional $veAERO)

Protocols & their buyback % ↓

@HyperliquidX | 99% of fees

@Aster_DEX | 99% of daily platform fees

@pendle_fi | 80% of V2 yield/swap fees

@GEODNET | 80% of data revenue

@JupiterExchange | 50% of platform revenue

@PancakeSwap | varies by product, 15–23% of AMM V3 fees / 50% of Infinity revenue / 100% of Prediction revenue

@maplefinance | 25% of protocol revenue

@Raydium | 12% of trading fees

@Uniswap | ~17% of fees on active fee-switch pools

@THORSwap | 20% of revenue goes to THOR buyback and burn

@ApeBond | 50% of DEX trading fees

@MarinadeFinance | 50% of revenue

@metaplex | 50% of revenue

@Orca_so | 20% of protocol fees

@QuickSwapDEX | 10–13.33% of collected fees

@StaderLabs | 20% of quarterly revenue

Also worth tracking, but no fixed % disclosed:

@aave | fixed annual buyback budget

@Chainlink | revenue-backed LINK reserve

@sparkdotfi | protocol surplus used for buybacks

aerodrome-finance:native is the third-largest DEX on the planet by volume. Its market cap is $318M. Read those two sentences again.

THE BUSINESS

- $12.4B in DEX volume over the last 30 days — only Uniswap and PancakeSwap do more

- ~$150K/day in trading fees, and 100% of fees flow to veAERO lockers. The team keeps nothing. The purest real-yield model in DeFi.

- $454M TVL — the token trades at 0.7x the liquidity it coordinates

TOKENOMICS

- 54% of circulating supply is locked in veAERO. Voters, not flippers.

- Onchain holding data: 96% of wallets haven't moved a single coin in 30 days. Only 3.8% are actively trading. That's diamond-hand structure at the lows.

- Mission 70 emission cuts already shrinking inflation

- Holder count +23% YoY straight through a -43% drawdown

THE JULY CATALYST

The part nobody's pricing in: next month Aerodrome and Velodrome merge into one unified cross-chain DEX under AERO.

- Expands from Base to Ethereum mainnet AND Circle's Arc chain

- VELO absorbed into AERO — one token, all chains

- MEV-resistant pools + permissionless listings ship with it

The liquidity hub of Coinbase's L2 becomes a multi-chain liquidity network in ~30 days. Dated catalysts this clean are rare.

DISTRIBUTION

- Robinhood just opened AERO trading to retail

- Base MCP is live — AI agents can now route DeFi flow on Base, and agents route to the deepest liquidity

- Coinbase's entire onchain strategy runs through Base. Base's liquidity runs through Aerodrome.

TECHNICALS

- $0.335 — inside the $0.29-$0.40 accumulation band that preceded ~70% rallies in every prior extreme-fear event

- RSI(7) at 29, oversold. 23% below the 200DMA.

- Flat over 90 days while the rest of DeFi bled double digits. Quiet relative strength.

- Fib extensions at $0.62 / $0.70 — a 2x just to fill prior structure. ATH is ~7x away.

Extreme fear at 13. A top-3 DEX under a $350M cap. Half the supply locked. A chain-expansion catalyst 30 days out.

Asymmetry doesn't announce itself. It looks exactly like this.

NFA. DYOR. https://t.co/C0ll7go8lu

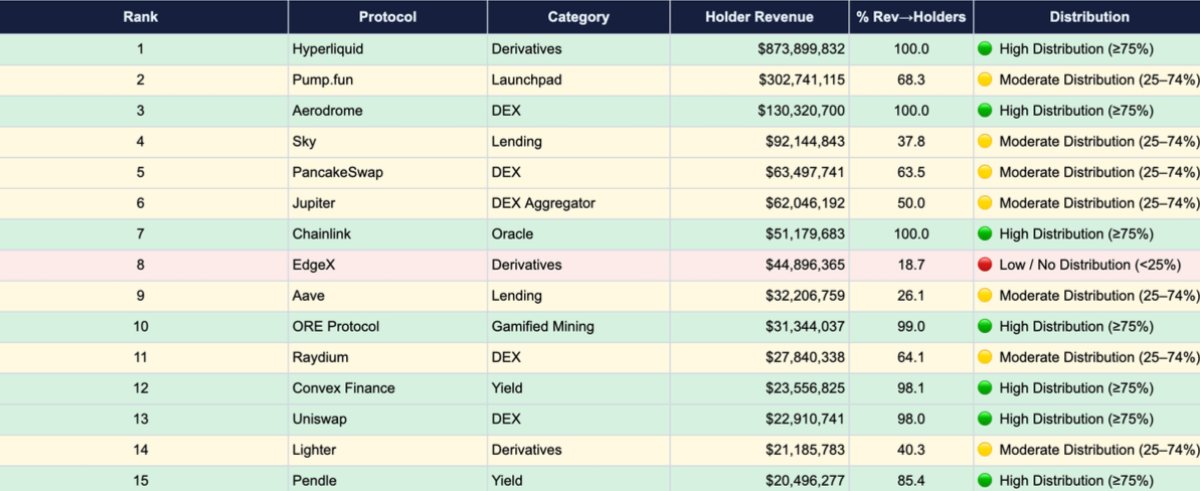

➥ five protocols. one question. how much of the fees actually reach the token.

i spent the week asking it project by project. here is the whole spectrum on one screen.

ranked by % of fees that reach holders:

[1] @pendle_fi · >100%

holder rev $28.68M on $24.93M fees. it pays holders more than it books as revenue. vePENDLE is the priority.

[2] @HyperliquidX · ~83%

holder rev $881.26M on $1.063B fees. 100% of revenue routes to HYPE. the fee machine, at scale.

[3] @ether_fi · ~5.9%

holder rev $14.05M on $239.86M fees. a real route, but thin. most fees pay restakers.

[4] @aave · ~3.4%

holder rev $32.32M on $938.2M fees. bigger dollar slice than https://t.co/w4LxVKm45m, smaller share. Safety Module pays stakers for backstopping risk.

[5] @MorphoLabs · 0%

holder rev $0 on $284.97M fees. great product. the token captures none of it.

the lesson the whole week points at:

fees measure usage. they do not measure value accrual. a protocol can print a billion in fees and route nothing to its token. another can route more than it keeps.

before you buy a token for its "revenue," check where the revenue actually goes. it is one line on DefiLlama. most people never look.

A lot of people still think of $SKY as "that old MakerDAO token with a new name."

I think that's exactly why the market is still underestimating what this ecosystem has quietly become.

While everyone is chasing the next shiny narrative, @SkyEcosystem s sitting underneath one of the largest cashflow machines in DeFi, generating $160M+ annual revenue, processing hundreds of millions in fees, and operating one of the biggest decentralized stablecoin systems in crypto.

A few things stand out to me:

> USDS has grown into a multi-billion dollar stablecoin backed by one of the deepest collateral systems in DeFi.

> Annual protocol revenue sits around $160M while the token trades at roughly 8x earnings.

> 98.9% of supply is already circulating, meaning almost no meaningful dilution risk remains.

> Spark continues absorbing liquidity across DeFi and has become a major growth engine for the ecosystem.

> Sky Agent Network introduces a completely new capital allocation layer where independent allocators compete for yield, potentially creating another demand driver for USDS and SKY.

What makes $Sky interesting isn't the stablecoin business itself.

It's the combination of stablecoin issuance, lending infrastructure, treasury management, RWA exposure, and now agent-driven capital allocation all operating inside the same economic system.

The more I dig into it, the less it feels like a lending protocol and the more it resembles a decentralized onchain bank.

Of course there are risks.

Regulation around stablecoins remains the biggest overhang, and USDS still competes against giants like USDT, USDC,..

But unlike most altcoins, $Sky isn't surviving on narrative alone.

The protocol already has users, collateral, cashflow, and one of the strongest network effects anywhere in DeFi.

If $BTC is the asset I'd rather own during uncertain markets, $Sky is probably one of the few altcoins I'd still be comfortable accumulating when sentiment gets ugly.

Massive cashflow. Minimal dilution. Strong stablecoin moat. Growing ecosystem. Real product-market fit.

Framework Rating: 4.6/5 ⭐

Protocol Quality (5/5) | Revenue (5/5) | Network Effects (4.5/5) | Token Capture (4/5) | Competitive Position (4.5/5)

At current levels, I see $SKY as one of the highest-quality DeFi assets available today. Not the fastest horse in a bull market, but probably one of the few altcoins I'd still want to hold if the market stays ugly for another 12-24 months.

Grayscale flagged five DeFi names on "value accrual."

Here's what each pays holders.

$HYPE → $781.6M

$UNI → $59.8M

$SKY → $13.4M

$MAPLE → $3.3M

$AAVE → $1.6M

Aave earned $63M. Shared $1.6M.

The case study finished last.

Despite the recent market volatility, DeFi continues to be one of the strongest sectors across crypto.

Price action comes and goes, but protocols generating consistent fees and revenue continue proving that real products with active users can survive every market cycle.

For me, sustainable cash flow remains one of the most important metrics when evaluating long-term opportunities.

Here are some of the protocols currently leading the sector:

1/ @Hyperliquid — The undisputed leader in perpetual DEX trading.

– 24h Fees: ~$2.79M

– 30d Fees: ~$82M

–30d Revenue: ~$65M

2/ @Uniswap

– 24h Fees: ~$1.48M

– 30d Fees: ~$53.72M

3/ @pumpdotfun

– 24h Fees: ~$2.06M

– 30d Fees: ~$63.57M

– 30d Revenue: ~$26M

4/ @Aave

– 24h Fees: ~$999K

– 30d Fees: ~$41.1M

5/ @LidoFinance

– 24h Fees: ~$1.14M

– 30d Fees: ~$36.81M

6/ @SkyEcosystem

– 24h Fees: ~$994K

– 30d Fees: ~$30.98M

7/ @ethena_labs

– 24h Fees: ~$3.32M

– 30d Fees: ~$18.51M

One of the fastest-growing yield protocols built around basis trading and synthetic dollars.

8/ @PancakeSwap & @AerodromeFi

Both continue processing massive trading volume while generating tens of millions of dollars in monthly fees across multiple chains.

9/ @MorphoLabs

A capital-efficient lending protocol that continues growing thanks to higher lending efficiency and increasing adoption.

10/ @Polymarket

– 24h Fees: ~$1.58M

– 30d Fees: ~$30.68M

Prediction markets continue attracting significant user activity, translating into consistently strong fee generation.

Looking across the entire sector, Hyperliquid and Pump continue dominating through exceptional fee capture, while Uniswap and Aave remain some of the strongest blue-chip DeFi protocols.

I pay much closer attention to protocols generating real fees and sustainable revenue during uncertain market conditions.

Strong fundamentals don't eliminate volatility, but they often provide a much stronger foundation than narratives alone when capital becomes more selective.

.@coinbase invested in @centrifuge and made them their Preferred Tokenization Infrastructure on @base .

The more interesting part is what’s been happening quietly in the background. Over the past few weeks, Centrifuge deployed the same assets (deJAAA and deJTRSY) across OKX/X Layer, Stellar, Morpho, and Euler — without new token launches or heavy per-chain work.

That’s how their factory model actually works in practice. The core pieces (vault logic, async redemptions, compliance) are handled once, and new chains just become another place to deploy.

Coinbase didn’t back another tokenization tool. They backed the infrastructure that lets regulated credit function inside DeFi at scale.

While a lot of people are still separating RWA and DeFi, Centrifuge is making them work together.

Still digging.

With Coinbase announcing tokenized stocks for non-US persons, here’s our map of tokenized securities models from February.

We look forward to learning more details about the structure of Coinbase’s tokenized stocks so we can add them to this graphic.

![0xchainink's tweet photo. $SYRUP : Review 📜

What if the fastest-growing corner of traditional finance, private credit, could be rebuilt onchain with every loan, every borrower, and every piece of collateral verifiable in real time?

Meet Maple Finance, DeFi's institutional lender. $7B+ in loans originated, a 99% repayment rate, and ~$2B+ in TVL, with institutional borrowers posting Bitcoin and Ethereum as collateral and lenders earning fixed-rate, overcollateralized yield.

Through Syrup, that institutional-grade yield is now permissionlessly available to all of DeFi.

Let's explore how Maple is bringing capital markets onchain. 👇

⚪ Maple at a Glance

Maple Finance is an onchain institutional lending marketplace that connects institutional borrowers with lenders seeking high-quality, overcollateralized yield. Unlike retail-focused DeFi, Maple applies traditional credit underwriting, active collateral management, and institutional custody (Anchorage, BitGo, Zodia) while keeping every loan and collateral position verifiable onchain.

The protocol runs two layers. Maple is the permissioned, institutional-grade marketplace for accredited allocators. Syrup is the permissionless product that opens the same yield to DeFi natives through syrupUSDC and syrupUSDT, liquid yield-bearing dollars integrated across Pendle, Balancer, Morpho, and other major protocols.

The $SYRUP token governs the ecosystem and captures value through buybacks.

Marketplace Insight: Maple sits at the intersection of three of the strongest trends in finance: the explosion of private credit as banks retreat from corporate lending, surging stablecoin adoption, and Bitcoin's acceptance as institutional collateral. CEO Sidney Powell frames the ambition as building "a new version of an Apollo or an Ares" for the onchain era. With real revenue, real loan performance, and a buyback mechanism tying protocol growth directly to the token, Maple is one of the few RWA-adjacent projects where the fundamentals are measurable rather than theoretical.

⚪ Mission

Maple's mission is to bring capital markets onchain. By combining the underwriting discipline of traditional finance with the transparency and efficiency of smart contracts, Maple aims to become the dominant institutional credit layer of DeFi, serving institutions that want capital and allocators that want high-quality yield, all on a verifiable, programmable infrastructure.

🔵 A Brief History

Maple was founded in 2019 by Sidney Powell and Joe Flanagan, who met at a commercial lending fintech and shared a background in institutional banking and debt capital markets. Powell had participated in $3B+ of corporate bond issuance and run a $200M+ bond funding program. Their original idea was to tokenize bonds, but with no market for that at the time, they pivoted Maple toward institutional lending.

The protocol launched its lending marketplace in 2021 with the MPL token, initially offering uncollateralized loans to crypto-native institutions like trading firms and market makers. The 2022 credit crisis, which hit much of crypto lending hard, pushed Maple to overhaul its risk model and move decisively to overcollateralized lending backed by large-cap assets.

In May 2024, Maple launched Syrup, a permissionless gateway that let any DeFi user access yield sourced from Maple's institutional loan book through syrupUSDC. In late 2024, following a community vote, the legacy MPL token migrated to SYRUP at a 1:100 ratio with no additional dilution, and by May 2025 the team consolidated all products under the unified Maple brand with the token as its sole asset.

October 2025 brought a pivotal tokenomics change. Governance voted to end staking emissions and shift to a buyback model, directing 25% of protocol revenue into the Syrup Strategic Fund to buy back and retire tokens. The first buyback executed in December 2025, retiring 2 million tokens using a quarter of November revenue.

2026 has tested and strengthened the protocol.

A Cayman Islands court issued an injunction blocking the syrupBTC launch over an exclusivity dispute with Core Foundation, which Maple later settled. During an April 2026 DeFi exploit involving compromised rsETH collateral, Maple confirmed no direct exposure (the asset was never approved by its Risk Committee) and exited indirect positions within 24 hours. In May 2026, Maple launched Proof of Reserves for syrupUSDC and syrupUSDT with The Network Firm, and the token expanded to Revolut's 70M+ users across the UK and EU.

🔵 Ecosystem Narrative

Maple's ecosystem is built on one principle: institutional credit discipline and DeFi transparency are not opposites, they are complementary, and combining them unlocks a category neither side could build alone.

Key dynamics include:

➛ Overcollateralized institutional lending. Maple lends to vetted institutions (trading firms, market makers, miners, family offices) with loans typically from $5M to $100M, collateralized above 100% by Bitcoin, Ethereum, and other large-cap assets, with conservative margin call and liquidation levels.

➛ Syrup as the DeFi gateway. syrupUSDC and syrupUSDT let any non-US user deposit stablecoins and earn institutional yield, packaged as liquid, composable, yield-bearing dollars usable across Pendle, Balancer, and Morpho.

➛ Active risk management. A dedicated Risk Committee approves collateral types, and the Maple Direct team actively manages loan health through real-time monitoring, margin calls, and liquidations, which is why the protocol has maintained a 99% repayment rate across $7B+ originated.

➛ Buyback flywheel. 25% of protocol revenue funds the Syrup Strategic Fund, which buys back and retires tokens, tying protocol growth directly to token scarcity. This replaced the old staking-emissions model in late 2025.

➛ Institutional custody and transparency. Collateral is held with Anchorage, BitGo, and Zodia, and Proof of Reserves through The Network Firm gives lenders independent verification that every loan is fully backed.

➛ Multi-chain and product expansion. Maple deploys where liquidity is deepest (Ethereum, Solana, with BNB Chain onboarding), and is building out products like syrupBTC to expand its addressable market.

➛ Mainstream distribution. The Revolut listing in April 2026 bridged Maple's onchain credit yield to a mainstream fintech audience of 70M+ users, a meaningful step beyond crypto-native distribution.

⚪ Token Utilities

$SYRUP is the governance and value-accrual token of the Maple ecosystem:

➛ Governance: Holders vote on protocol decisions, risk parameters,

product direction, and treasury management, including the tokenomics changes that reshaped the model.

➛ Revenue-Funded Buybacks: 25% of protocol revenue flows to the Syrup Strategic Fund to buy back and retire tokens, creating deflationary pressure tied directly to protocol performance.

➛ Ecosystem Access: The token underpins the Syrup product, the gateway to permissionless institutional yield, and integrates with DeFi protocols like Balancer and Pendle.

➛ Alignment: After the October 2025 shift away from staking emissions, value accrues to holders through buybacks rather than dilutive rewards, aligning the token with sustainable revenue.

➛ Distinct from Yield Tokens: The governance token is separate from syrupUSDC and syrupUSDT, which are the yield-bearing dollar instruments, keeping governance and yield cleanly separated.

⚪ Key Features

➛ Institutional Lending Marketplace: Overcollateralized, fixed-rate loans to vetted institutions, with $7B+ originated and a 99% repayment rate.

➛ Syrup Permissionless Yield: syrupUSDC and syrupUSDT bring institutional yield to all of DeFi as liquid, composable assets.

➛ Onchain Transparency: Every loan, borrower, and collateral position is verifiable onchain, backed by Proof of Reserves via The Network Firm.

➛ Institutional Custody: Collateral held with Anchorage, BitGo, and Zodia, not self-custodied by the protocol.

➛ Active Risk Management: A Risk Committee and the Maple Direct team manage collateral health with conservative margin and liquidation levels.

➛ Revenue Buybacks: 25% of revenue retires tokens through the Syrup Strategic Fund.

➛ DeFi Composability: Deep integrations across Pendle, Balancer, and Morpho, plus mainstream reach through Revolut.

🔵 Meet the Maple Team

Maple is led by founders who came from institutional banking and debt capital markets, applying traditional credit discipline to onchain lending, backed by an engineering and product team building the infrastructure for institutional DeFi.

▶️ Core Members:

➛ Sidney Powell [ @syrupsid ] - Co-Founder & CEO | Australian entrepreneur with a background in debt capital markets and institutional banking. Participated in $3B+ of corporate bond issuance, ran a $200M+ bond funding program, and managed Treasury at a commercial lending fintech. Co-founded Maple in 2019 to bring debt capital markets onchain. Now based in Miami, leads strategy, institutional partnerships, and protocol expansion.

➛ Joe Flanagan [ @joe_defi ] - Co-Founder | Met Powell at a commercial lending fintech and co-founded Maple in 2019. Brings traditional finance and fintech experience to the protocol's lending model and operations.

➛ Matt Collum [ @fjordmatt ] - CTO | Leads engineering across Maple's core lending protocol, smart contract infrastructure, and the Syrup product stack.

➛ Ryan O'Shea [ @Ryanos_eth ] - COO | Runs operations across the Maple organization, coordinating institutional onboarding, risk processes, and go-to-market.

➛ Nayat Cheikh - Head of Product Design | Leads product design across Maple and Syrup, shaping the lender and borrower experience.

➛ Maple Direct & Risk Committee | The underwriting and risk function responsible for borrower diligence, collateral approval, and active loan management, central to the protocol's 99% repayment record.

🔵 Ratings

➛ Use Case: ★★★★✦ (4.5/5) - Maple is one of the clearest real-revenue businesses in all of crypto. $7B+ originated, a 99% repayment rate, ~$2B+ TVL, and a genuine product-market fit at the intersection of private credit, stablecoins, and Bitcoin collateral. The Syrup layer is a smart unlock, turning permissioned institutional yield into composable DeFi assets, while institutional custody and Proof of Reserves give it credibility most DeFi lenders lack. The handling of the April 2026 rsETH exploit (no direct exposure, fast exit from indirect positions) demonstrated the risk framework actually works. The 0.5-point deduction is for the inherent credit and counterparty risk of lending, the competitive pressure from other onchain credit players, and sensitivity to crypto credit cycles where a downturn could compress yields and loan demand simultaneously.

➛ Tokenomics: ★★★★ (4/5) - The October 2025 shift from staking emissions to a revenue-funded buyback model is exactly the kind of mature tokenomics evolution that aligns a token with real business performance. Directing 25% of protocol revenue into buying back and retiring tokens ties scarcity directly to protocol growth, and the first buybacks have already executed. The clean 1:100 MPL migration with no extra dilution was well handled. The 1-point deduction is for the infinite max supply structure (the buyback has to consistently outpace any emissions and unlocks to be net deflationary), the token's roughly 70% drawdown from its 2025 highs, and the reality that buyback strength depends entirely on sustained revenue, which compresses in weak credit markets.

➛ Audits: ★★★★✦ (4.5/5) - Maple has one of the strongest security profiles in DeFi, backed by a CertiK Skynet Score of 93.16 (AAA grade), one of the highest institutional ratings on the platform and on par with major L1s. The Maple-Core V2 protocol has undergone 7+ audits from top-tier firms including Spearbit/Cantina, Three Sigma, and 0xMacro, with the Syrup Router separately audited by Three Sigma. The protocol has operated lending infrastructure since 2021 through multiple market cycles, including the 2022 credit crisis, without a protocol-level smart contract exploit, and runs continuous invariant monitoring via Tenderly Web3 actions at every block with automated incident response. Proof of Reserves through The Network Firm adds independent verification that loans are fully backed, and institutional custody via Anchorage, BitGo, and Zodia reduces smart contract custody risk. The 0.5-point deduction is for the inherent credit and operational risk surface of lending (borrower default, collateral liquidity, custody integrity), which sits outside the smart contract layer, as the April 2026 rsETH episode showed even well-managed indirect exposure can introduce risk.

➛ Community: ★★★★ (4/5) - Maple has built a credible, institutionally respected community and brand, with strong exchange support (Coinbase, Upbit, and Revolut's 70M+ user base), genuine builder integrations across Pendle, Balancer, and Morpho, and a reputation as the serious institutional lender in DeFi. Sidney Powell is a visible, credible founder who communicates consistently. The 1-point deduction is that Maple's community is more institutional and yield-focused than retail-passionate, social engagement is modest relative to its TVL, and the deep token drawdown plus the syrupBTC legal episode tested holder conviction through 2026.

🔵 Conclusion

Maple Finance is one of the most fundamentally sound businesses in crypto, full stop. It is not promising future adoption or theoretical yield. It has originated over $7 billion in loans, maintained a 99% repayment rate across multiple market cycles, and built roughly $2 billion in TVL by applying real credit underwriting to onchain lending. In a sector full of narratives, Maple has a measurable, revenue-generating operation that looks more like a private credit fund than a typical DeFi protocol.

The token has evolved to match. The shift to a revenue-funded buyback model in late 2025 ties value directly to protocol performance, and the Syrup layer extends institutional yield to all of DeFi through composable, liquid assets.

Sidney Powell and Joe Flanagan have spent over six years building this patiently, surviving the 2022 credit crisis that wiped out many peers, and positioning Maple at the convergence of private credit, stablecoins, and Bitcoin collateral.

If capital markets are moving onchain, and private credit is the fastest-growing slice of traditional finance, then Maple is the most credible institutional lender building that bridge, with the revenue, track record, and tokenomics to back it. Powell wants to build the onchain Apollo. Few crypto projects have the fundamentals to make that ambition believable. Maple actually does.](https://pbs.twimg.com/media/HL1K_6-aUAAsZ9B.jpg)

![Capy_Research's tweet photo. ➥ five protocols. one question. how much of the fees actually reach the token.

i spent the week asking it project by project. here is the whole spectrum on one screen.

ranked by % of fees that reach holders:

[1] @pendle_fi · >100%

holder rev $28.68M on $24.93M fees. it pays holders more than it books as revenue. vePENDLE is the priority.

[2] @HyperliquidX · ~83%

holder rev $881.26M on $1.063B fees. 100% of revenue routes to HYPE. the fee machine, at scale.

[3] @ether_fi · ~5.9%

holder rev $14.05M on $239.86M fees. a real route, but thin. most fees pay restakers.

[4] @aave · ~3.4%

holder rev $32.32M on $938.2M fees. bigger dollar slice than https://t.co/w4LxVKm45m, smaller share. Safety Module pays stakers for backstopping risk.

[5] @MorphoLabs · 0%

holder rev $0 on $284.97M fees. great product. the token captures none of it.

the lesson the whole week points at:

fees measure usage. they do not measure value accrual. a protocol can print a billion in fees and route nothing to its token. another can route more than it keeps.

before you buy a token for its "revenue," check where the revenue actually goes. it is one line on DefiLlama. most people never look.](https://pbs.twimg.com/media/HLPWc1jaQAAUzmu.jpg)