HERE ARE THE 8 WORST DAYS IN THE HISTORY OF NASDAQ

1. June 5, 2026 down 1,121 points

2.Apr. 3, 2025 down 1,050 points

3. Mar. 16, 2020 down 970 points

4. Apr. 4, 2025 down 962 points

5. October 10, 2025 down 880 points

6. March 12, 2020 down 750 points

7. April 10, 2025 down 737 points

8 March 10, 2025 down 727 points

Donald Trump was president for each of these crashes!

Absolutely incredible.

ALL 7 hourly candlesticks on today's Nasdaq 100 chart were red as tech stocks fell in a literal straight-line lower.

Biggest drop since "Liberation Day."

🚨SpaceX set to IPO under the ticker $SPCX

SpaceX to begin trading June 12

🚀 THE NEW SPACE RACE IS ABOUT DATA CENTER

📈THE ANTHROPIC × SpaceX SIGNAL:

This is why every hyperscaler is moving up:

∙$AMZN → Project Kuiper

∙$GOOG → Starlink partnership + investments

∙$MSFT → Azure Space

∙Anthropic → infrastructure deals expanding into sovereign + edge compute

When SpaceX launches Starlink Direct-to-Cell and starts deploying V3 satellites with 1Tbps capacity — that’s the network layer of AI being rebuilt above the atmosphere.

The convergence is already happening:

∙Starshield (SpaceX’s classified gov division) is building dedicated DoD + intelligence constellations

∙Starlink is becoming the global low-latency backbone for AI inference at the edge

∙Lunar + LEO data centers are being prototyped (Lonestar, Axiom, Starcloud) — solar power is infinite in orbit, cooling is free in vacuum

HOW THESE 35 COMPANIES FIT THE ECOSYSTEM :

Think of the space economy as 5 layers stacked vertically — same logic as the AI stack:

LAYER 1 — RAW MATERIALS & COMPONENTS (the “semis” of space)

$HXL · $BWXT · $TDY · $HEI.A · $KULR · $ATRO · $RDW

Carbon fiber, nuclear cores, sensors, batteries, composites. Without these, nothing flies.

LAYER 2 — PRIMES & MANUFACTURERS (the + Foundry” layer)

$LHX · $LMT · $NOC · $RTX · $BA · $GE · $HON · $ESLT · $BAESY · $EADSY

Defense + aerospace giants that build the actual spacecraft, missiles, and satellite buses. Backlog, government cash flows.

LAYER 3 — LAUNCH moving (payloads to orbit)

SpaceX · $RKLB · $FLY · $SPCE

The cost of access. SpaceX has collapsed $/kg by 20x. Rocket Lab is scaling Neutron. This is the enabling layer for everything above.

LAYER 4 — DATA & CONNECTIVITY (the “cloud” layer)

$AMZN · $IRDM · $GSAT · $VSAT · $TSAT · $SATS · $SPIR · $PL · $ASTS · $SATL · $BKSY

Satellite networks. Earth observation. Direct-to-cell. This is the AWS of space — recurring revenue, subscription models, AI-ready data pipelines.

LAYER 5 — APPLICATIONS (the “AI/SaaS” layer)

$PLTR · $LDOS · $TRMB · $KTOS · $SIDU · $LUNR · $VOYG · $MNTS

Mission software, geospatial intelligence, lunar infrastructure, in-space services. Where the margin lives.

$NVDA CEO is telling you to buy energy stocks

He is literally saying demand will 1000x

Stocks positioned to benefit:

- $CEG

- $VST

- $OKLO

- $BE

- $GEV

- $IREN

“This is the best time in the history of humanity to invest in sustainable energy”

In 2025, he was early on semis and neoclouds:

- $NBIS at $22 → +600%

- $INTC at $23 → +500%

- $SNDK at $275 → +400%

- $CRWV at $40 → +200%

- $TSM at $240 → +80%

He’s not guessing. He’s showing you the roadmap.

Are you going to ignore him again?

SpaceX $SPCX is officially set to go public on June 12.

This will be the largest IPO in history, & will cause a total reprice amongst the entire space sector.

These are the critical sectors amongst the space theme:

Satellite Communication & Operations

$ASTS ~ AST SpaceMobile

$PL ~ Planet Labs

$GSAT ~ Globalstar

$SPIR ~ Spire Global

$AMZN ~ Amazon

$VSAT ~ Viasat

Spacecraft & launch systems

$RDW ~ Redwire

$RKLB ~ RocketLab

$LMT ~ Lockheed Martin

$KTOS ~ Kratos Defense

$FLY ~ Firefly Aerospace

$LUNR ~ Intuitive Machines

Specialty Materials

$CRS ~ Carpenter Technology

$ATI ~ ATI Inc

$MTRN ~ Materion

$GLW ~ Corning

$PKE ~ Park Aerospace

Propulsion Systems & Fuel

$LIN ~ Linde

$APD ~ Air products & Chem

$NEU ~ NewMarket

Electronics & Semis

$NVDA ~ Nvidia

$AVGO ~ Broadcom

$COHR ~ Coherent

$LITE ~ Lumentum

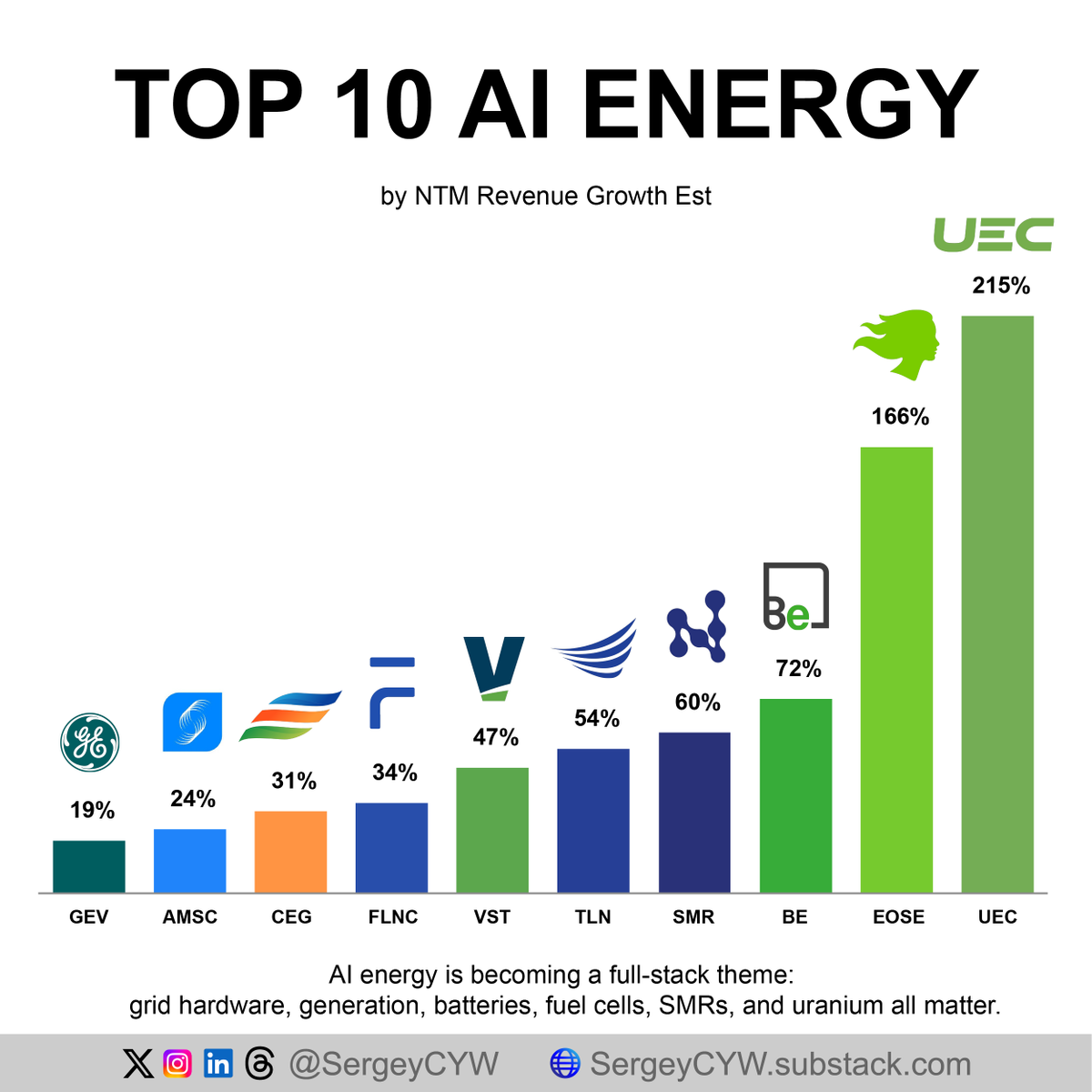

AI needs energy. From uranium to grid equipment, the power stack behind AI is becoming its own supply chain.

Data centers need GPUs. GPUs need racks. Racks need power. Power needs grid access, firm generation, storage, cooling, and fuel.

Hyperscalers are no longer only competing for compute capacity. They are competing for long-term electricity supply, faster interconnection, backup systems, and local power solutions.

Here are 10 companies positioned across the AI energy stack:

$GEV — GE Vernova Market Cap: $294B | NTM Revenue Growth Est: +19%

GE Vernova is one of the key grid infrastructure names tied to AI data center expansion. Its Electrification segment booked $7.1B in Q1 orders, with a 2.5 book-to-bill ratio. More importantly, data center equipment orders reached $2.4B in one quarter, already above last year’s total. The role is clear: transformers, switchgear, and grid architecture needed to connect AI campuses to the broader power system.

$AMSC — American Superconductor Market Cap: $2.6B | NTM Revenue Growth Est: +24%

AMSC sits in the power quality and grid-stability layer. AI data centers create dense local loads, especially in constrained regions where voltage control and power resiliency matter. Its grid segment represents more than 80% of revenue, and management highlighted momentum in materials and semiconductor divisions tied to localized data center infrastructure. The company also turned free-cash-flow positive as demand for grid-stabilizing systems improved.

$CEG — Constellation Energy Market Cap: $100B | NTM Revenue Growth Est: +31%

Constellation is the large-scale nuclear baseload provider in the AI energy stack. Tech companies want 24/7 carbon-free power, and CEG owns the largest nuclear fleet in the U.S. The Calpine acquisition adds 27GW of natural gas capacity, giving the company more dispatchable supply for near-term demand. Management also increased its buyback authorization to $5B and outlined a $3.9B capex plan aimed at clean energy constraints.

$FLNC — Fluence Energy Market Cap: $2.3B | NTM Revenue Growth Est: +34%

Fluence is the battery storage layer for AI power demand. Data centers need always-on electricity, while renewables remain intermittent. FLNC delivered 2.3GWh of storage in Q1 and holds a $5.5B backlog. The more interesting piece is its active 36GWh data center pipeline, even though management has not yet converted those engagements into signed backlog. Smartstack targets high-density storage where AI campuses face space constraints.

$VST — Vistra Market Cap: $54B | NTM Revenue Growth Est: +47%

Vistra is a dispatchable power and nuclear offtake play. The company signed a 20-year agreement with Meta to deliver 2.6GW of zero-carbon nuclear power for an AI data center in Ohio. It also acquired Cogentrix for $4.7B, adding 10 gas facilities and 5.5GW of capacity. VST has also secured a 20-year nuclear power agreement with AWS, placing it directly inside the AI compute power procurement cycle.

$TLN — Talen Energy Market Cap: $17.5B | NTM Revenue Growth Est: +54%

Talen is turning nuclear generation into direct AI data center supply. Its expanded Amazon agreement locks in up to 1,920MW of nuclear power through 2042. The anchor asset is the 2.2GW Susquehanna nuclear facility, designed to support a collocated, 24/7 carbon-free data center campus. TLN is moving from merchant power exposure toward long-term contracted offtake, with management guiding to up to $1.18B in 2026 free cash flow.

$SMR — NuScale Power Market Cap: $3.5B | NTM Revenue Growth Est: +60%

NuScale represents the small modular reactor angle. AI campuses need scalable carbon-free power, but traditional nuclear projects require massive upfront capital and long timelines. SMR’s TVA and ENTRA1 partnership targets a 6GW SMR program across the seven-state TVA region. Its 12-module plant structure can scale gradually as compute clusters come online, making modular nuclear a potential fit for staged AI power demand.

$BE — Bloom Energy Market Cap: $71B | NTM Revenue Growth Est: +72%

Bloom Energy is the on-site power layer for AI campuses facing long grid interconnection delays. Its Oracle Project Jupiter agreement positions Bloom as the sole power provider for a New Mexico AI data center campus, with up to 2.45GW of solid oxide fuel cell capacity. The setup replaces planned gas turbines with a private microgrid. Management lifted 2026 revenue guidance to around $3.8B as AI data center demand reshaped the business mix.

$EOSE — Eos Energy Market Cap: $1.6B | NTM Revenue Growth Est: +166%

Eos provides zinc-based long-duration batteries for off-grid and power-constrained AI sites. Its TURBINE-X partnership targets up to 2GWh of storage across hyperscale data center projects over 36 months, pairing batteries with simple-cycle gas turbines for on-site microgrids. The MN8 Energy agreement adds 750MWh tied to solar plus 10-hour discharge batteries, aimed at round-the-clock power for high-demand industrial loads.

$UEC — Uranium Energy Market Cap: $7.1B | NTM Revenue Growth Est: +215%

UEC is the nuclear fuel exposure in the AI energy stack. AI data centers are increasing interest in nuclear baseload power, and uranium supply remains structurally tight. UEC is bringing low-cost ISR projects online in Wyoming and South Texas while keeping its order book unhedged. That structure gives direct exposure to uranium pricing if nuclear demand from utilities and hyperscalers continues to support the market.