This is WILD!

Goldman Sachs says Wall Street consensus 2027 hyperscaler Capex estimates are too conservative (Save this).

The consensus lands at $920 billion but Goldman thinks it could reach $1.4 trillion.

Here is how they get there.

Hyperscaler capex, the combined AI infrastructure spending of Amazon, Google, Meta, Microsoft, and Oracle went from $261 billion in 2024 to an estimated $805 billion in 2026, a 3x increase in two years.

The consensus for 2027 assumes growth decelerates sharply to just 22%, which is where Goldman pushes back.

Goldman economists compared that assumption against every major infrastructure buildout in history, railroads, highways, electrification, the internet and found they consistently consumed 2 to 3% of GDP at their peak.

At 2% of US GDP, hyperscaler capex reaches $950 billion in 2027 and at 3%, it reaches $1.25 trillion.

In the most aggressive scenario where hyperscalers deploy every dollar of operating cash flow plus the full capacity of the investment grade credit market, the number reaches $1.43 trillion.

The fourth chart is what makes the Goldman case feel earned rather than aggressive.

Hyperscalers are expected to reinvest 98% of operating cash flows directly back into capex in 2026, a ratio only ever matched during the telecom bubble of 2001.

The critical difference is that these companies are actually generating the cash flows that are being reinvested, Amazon, Google, Meta, and Microsoft combined are printing hundreds of billions in operating cash every year and putting nearly all of it back into infrastructure.

A buildout this large creates supply chain pressure and earnings volatility in the names most exposed, and Goldman is not dismissing that risk but the direction of spending is not in question, the only debate is whether 2027 comes in at $920 billion or $1.4 trillion.

The companies sitting directly in the path of that spending are the ones worth owning.

Nvidia captures the largest share of every hyperscaler capex dollar, owning 80%+ of AI training compute, and Morgan Stanley raised its 2026 capex estimate specifically because of continued Nvidia demand.

Oracle is the fastest growing capex spender among the five hyperscalers on a percentage basis up 116% from 2024 to 2027 with the smallest absolute base, giving it the most runway remaining.

CoreWeave and Nebius sit between the hyperscalers and frontier AI companies, renting GPU capacity to anyone who cannot get on the hyperscaler queue fast enough and as that capex number grows, so does their total addressable market.

Milk Road subscribers already up massively on these names, come join Milk Road Pro for our full breakdown and what other names we are watching for just a dollar.

Link below!

Vad jag vet har Sivers aldrig haft något PM med GF inom Photonics. Så egentligen är det första gången det blir officiellt. Men så klar, kunde man haft med en notis och att man varit ecosystem partners på olika sätt. Dock är det nog nedan OCI MSA partners (som inte heller nämn), som egentligen gör nyheten extra intressant.

$AMD shareholders suddenly realized most of this 5GW will go to @AMD because for $87B, it would only work for Helios Rack that have 2 EPYC Venice and 2 MI455X or 3 EPYC Venice and 1 MI455X.

And yes Subscribers already know abt this since last year.

This is confirming my thread on CPU:GPU ratio already moving to 2-3:1, where enterprises are already testing more than 10 agents. Read the linked thread to understand more.

Venice is estimated at $12,000-$15,000 per chip at highest performance SKU, 256 core)

MI455X is estimated at $35,000-$40,000.

While there is no official statement yet, but Softbank already picked AMD for many projects due to superior TCO and $0.0003-$0.0005/M Tokens.

1GW of $NVDA Rubin would be $45-$55B.

Even if 5GW in 1 campus, it would still be $180-$200B.

1GW of $AMD Helios is estimated around $30-$35B

5GW in 1 campus, with 1:1 ratio or 2:1 would be

$85-$90B

And this announcement is only $87B. The math only works for AMD chips.

Not Financial Advice! DYOR!

Per Foxconn shareholder meeting:

CPO switch products expected to begin Q3. 10K units 2026, explosive grow to next year.

Aims/expected to be #1 globally.

Anyone remember which Foxconn subsidiary handles their advanced optical work?

cough.. cough.. Shunsin (6451).

Lot of these exponentially scaling volume shipments won’t show up in balance sheet yet, but will likely soon H2.

This is called frontrunning the next supercycle.

McKinsey humanoid supply chain mapping:

Confirms that Actuators are set to be the key battleground for mass production.

Coupled with BofA analysis where Actuators = 51% total BOM.

A few companies have overlap in different Actuator parts like:

-> Harmonic Drive Systems (6324)

-> Nabtesco Corp (6268)

-> THK (6481)

-> Schaeffler

I'm close to picking 1-2 names for exposure.

HDS are the glaringly obvious pick though, purely from a supply chain overlap POV.

Holy mother of InP lasers.

Rosenblatt just dropped an InP supply and demand model today and the numbers are staggering.

NVIDIA asked the supply chain to scale InP laser capacity by 20x from 2025 to 2030. The vendors pushed back and agreed to 12x. Even the conservative scenario has Datacom supply still 50% behind demand exiting 2030 after a 12x increase.

12x supply increase over five years. Still not enough.

Rosenblatt explicitly calls it a non-cyclical growth industry well past 2030. The InP supply chain is structurally short for the rest of the decade.

Here is what the revenue buildout looks like by supplier across 2025 to 2030:

$LITE -- $600M in 2025 to $9B by 2030. The dominant player scaling fastest including a new InP fab acquisition in Greensboro NC converting in 2028, adding $2.5B in 2028 and $5B in 2029.

$AAOI -- $60M to $2.1B. The high-torque play. Rosenblatt sees it growing from under 5% to nearly 10% transceiver market share and entering the ultra-high-power CW laser market for CPO. Smallest base, biggest percentage runway.

$SIVE -- sits alongside as the pure-play InP laser specialist and external light source for CPO -- the chokepoint Rosenblatt's entire supply model is built around. DFB laser supply confirmed tight through Q3 2027.

$AVGO -- $550M to $4.5B. Second largest by revenue. Strong but less pure-play InP than LITE.

$COHR -- $125M to $4.3B. Rosenblatt's top near-term pick. Expects revenue acceleration and gross margin expansion from 6-inch wafer production driving 800G and 1.6T transceiver sales.

VIAV -- $53 stock, called out specifically for underappreciated bottlenecks in OCS and CPO test expertise and capacity.

Total InP Datacom market: $1.9B in 2025 to $22.75B by 2030. Nearly 12x.

Flags from the report.

$CIEN -- Rosenblatt is cautious. Side GM expectations have gotten too high and do not factor in price increases from LITE and COHR as suppliers.

$CRDO -- viewed as a niche player, not strongly relevant to the CPO optical supply chain. Expects 1.6T AECs to be weaker than the market expects.

If CPO scale-up slips beyond the current 2H27 build window, 2028 becomes a buying opportunity rather than a revenue year. Wafer supply, test and measurement, DSP, PIC, and laser capacity are all identified as potential chokepoints.

But the direction is not in question. NVIDIA is the demand signal and NVIDIA asked for 20x. The supply chain is building for 12x. The gap between those two numbers is the entire trade.

$LITE $COHR $AAOI $SIVE for the InP laser supply chain.

$IQE $AXTI $SOI for the InP epi and substrate layer underneath them.

$SOI for SiPh substrate.

Bullish Photonics

$SIVE Q1 earnings are out, this is exactly the news I was expecting from past financials and future growth.

I have been saying this for weeks. The bears are going to sell the headline. Do not be the bear.

The financials only give us a glimpse of the past.

Revenue down 22% YoY. EBITDA burning. Low on Cash at 26.6M SEK.

The stock will get hit by people who read the first line and stop.

I expected exactly this. And I am still holding every share.

The revenue miss is not a business problem. It is a timing problem.

US government shutdown delayed defense budget approvals. That revenue did not disappear, it got pushed to H2 2026. FX headwinds from a stronger SEK against USD and GBP took another chunk on top.

The underlying demand is completely intact.

Now here is the number that actually matters.

Pipeline grew 77% year to date to $799 million. On a company doing roughly 250M SEK in annual revenue. $799 million in qualified pipeline. That gap between the P&L and the pipeline is the entire thesis.

The CEO said it himself: record pipeline growth and several volume productions confirmed through 2027, driven by enormous interest in wireless beamformers and InP lasers.

We got confirmation of what we already k

Inferred:

SIVE is developing a 1.6T LRO pluggable transceiver with Jabil for AI datacenters. Jabil serves hyperscalers at a scale most companies never touch. 800G is already dominating datacenter shipments and 1.6T is the next wave. Being Jabil's laser partner for that transition is a real design win.

Goldman Sachs put the CPO TAM at $91B by 2028.

O-Net and Enablence locked in Q1. Both deep in the CPO supply chain. The right ecosystem relationships are being built right now, before the ramp.

LiDAR production confirmed for Q4 2026. Automotive first, then industrial LiDAR and autonomous robots. Two monetization verticals from one platform.

York Space acquisition. York Space ties directly into the US Space Development Agency. Production orders described as imminent. This takes Sivers Wireless from component supplier to vertically integrated SATCOM player overnight.

Tachyon Networks expanding from 28GHz to 60GHz FWA with SIVE. A Tier-1 telecom vendor launching first products by end of 2026.

US Chips Act EW Star renewal confirmed. Microelectronics Commons Year 2 funding secured. The defense revenue that was delayed is de-risked.

Post-period they raised roughly SEK 125M via directed share issue. The cash concern is addressed. Board restructuring with new nominees explicitly framed as preparation for a Nasdaq NY dual listing.

So you have confirmed:

Jabil.

O-Net.

Tachyon.

Enablence.

York Space.

LiDAR ramp.

Defense recovery.

Nasdaq NY dual listing.

Plus those that can be inferred via supply chain mapping:

$MRVL

$APPL

All pointing at the same 12-18 month window.

Q1 numbers are the price you pay for early positioning.

The pipeline and partnerships are the reason you hold.

I’m counting on Sweden sells, America buy to scoop some juice shares at a discount.

They will sell the financials, we will buy the chock-point into the future.

Not financial advice.

In long $SIVE

$SIVE is the most compelling CPO/photonics exposure to me.

Addressing the disinformation: I haven’t sold and don’t plan to sell a single share.

I do think this ends up the next $80B+ $LITE one day from ~$2.1B.

And I personally have plans to acquire more ownership + support their M&A prospects.

I believe earnings transcripts will be strongly positive.

As in the part few months we’ve discovered:

> AlChip/Amazon private placements, which is positive for Ayar -> $SIVE implying Trainium 4 design in

> Wiwynn + Ayar CPO scale up

> $JBL 1.6T optical transceiver ramp with Sivers incoming faster than markets expected (with relatively dramatic moat + demand as much as they can produce)

> O-Net scaling up ELS efforts with $SIVE

> $YSS acquisition of $SIVE allspace lead partner, designing Sivers into Space defense primes

> New CHIPS ACT funding for $SIVE

> $POET H2 volume ramp and their new $50m -> $500m order (with $SIVE as light source)

> information discovery around $AAPL using $SIVE lasers for next gen consumer devices

> information discovery around links to Lightelligence (went public $10B+ MC) + Lightmatter as likely customers.

> Celestial volume ramp with $MRVL indicators.

> new customers working on TFLN with $SIVE like Lightium

> $AMD going with $GFS for CPO, and GFS listing sivers as one of two laser suppliers

> Ayar removing $MTSI / $LITE from their website and signaling $SIVE as primary source/sole source

> Ayar raising $500m for volume ramp (intel, Mediatek, Nvidia, amd etc)

> pluggable TAM expansion signaled from 2025 annual report

> Nasdaq listing expected soon

> MSCI small cap index / Nasdaq omx inclusion, making Blackrock, Vanguard and others passive buyers

> M&A signaled from 2025 annual report + 2 new board members that have experience in that area

> $NOK as likely customer from 2025 annual report.

> $LITE getting cw bottlenecked from EML contracts, $SIVE signaling capacity agreements in place with Win, making the a likely bottleneck owner + chokepoint in CPO sector.

All of this market research was done before earnings.

Any results is just confirmation of supply chain mapping done.

I don’t think anyone cares about former quarter revenue since $SIVE is an exceptionally compelling 2027 long, especially H2 onward.

Only thing I’m looking at are:

> TAM expansion of the overall photonics supercycle (eg. optical engine, ELS, pluggables) either from M&A or developments

> volume ramp expectations from existing companies

> Nasdaq listing timelines for more liquidity to support their M&A efforts

> any new customers signaled for CPO/Pluggables

$XFAB (photonics + power semis) is an interesting long idea at $1.28B MC, that I took positions in.

Given EU CHIPS act 2 is today as the catalyst for European photonics players.

> 800 VDC power semi exposure to $NVDA push through $NVTS + $POWI

> Silicon Photonics / CPO exposure with $NVDA as evaluation stage for high volume manufacturing (optical transceivers/switches)

> The only high-volume SiC foundry in the US.

> One of the critical MEMS foundries

> ~1.29 P/B, which was around what $SOI was sitting at when I went long. Depressed valuations due to legacy drag

> ~6.5-8.5 fwd p/e 2028 personal est.

> backstopped by Government:

- EU CHIPS act, $128M Euros

- US CHIPS act $50M PMT (department of commerce).

With likely more coming (just signals critical importance to Western supply chains).

So at a certain point with all the grants, they’re just getting the capex funded by the Governments.

EU CHIPS act 2 is coming out this week, and I’m gonna go ahead and guess $XFAB might get included given they were before, and this package is specifically targeting photonics.

~$1.3B MC seems compelling to me if it can pull a Soitec reversal (low p/b, very high growth segments, auto legacy drag).

As for the $NVDA silicon photonics relationships it’s under “photonixFAB”.

Markets probably missed this silicon photonics relationship (like $TSEM when I went long) with Nvidia since XFab leads this… Just under a different name.

For power semis, XFAB is named for SiC + $NVTS. In PCN-22181, $POWI explicitly names XFAB as its foundry.

Given its exposure to power semis and photonics as growth, low P/B, gov backstop (of course dyor, just sharing my personal thoughts)

Thought it personally seemed compelling.

McKinsey believes there will be bottlenecks in actuators, sensing, and perception components as robotics manufacturing ramps up

I already have a perception stock, so it may be time to move into the rest of the supply chain (although it is largely Chinese-dominated)

OpenAI and Anthropic are effectively telling the market they can't solve every problem with a generic AI coworker.

You don't pour billions into massive forward-deployed joint ventures if you think the next model release is going to take care of it.

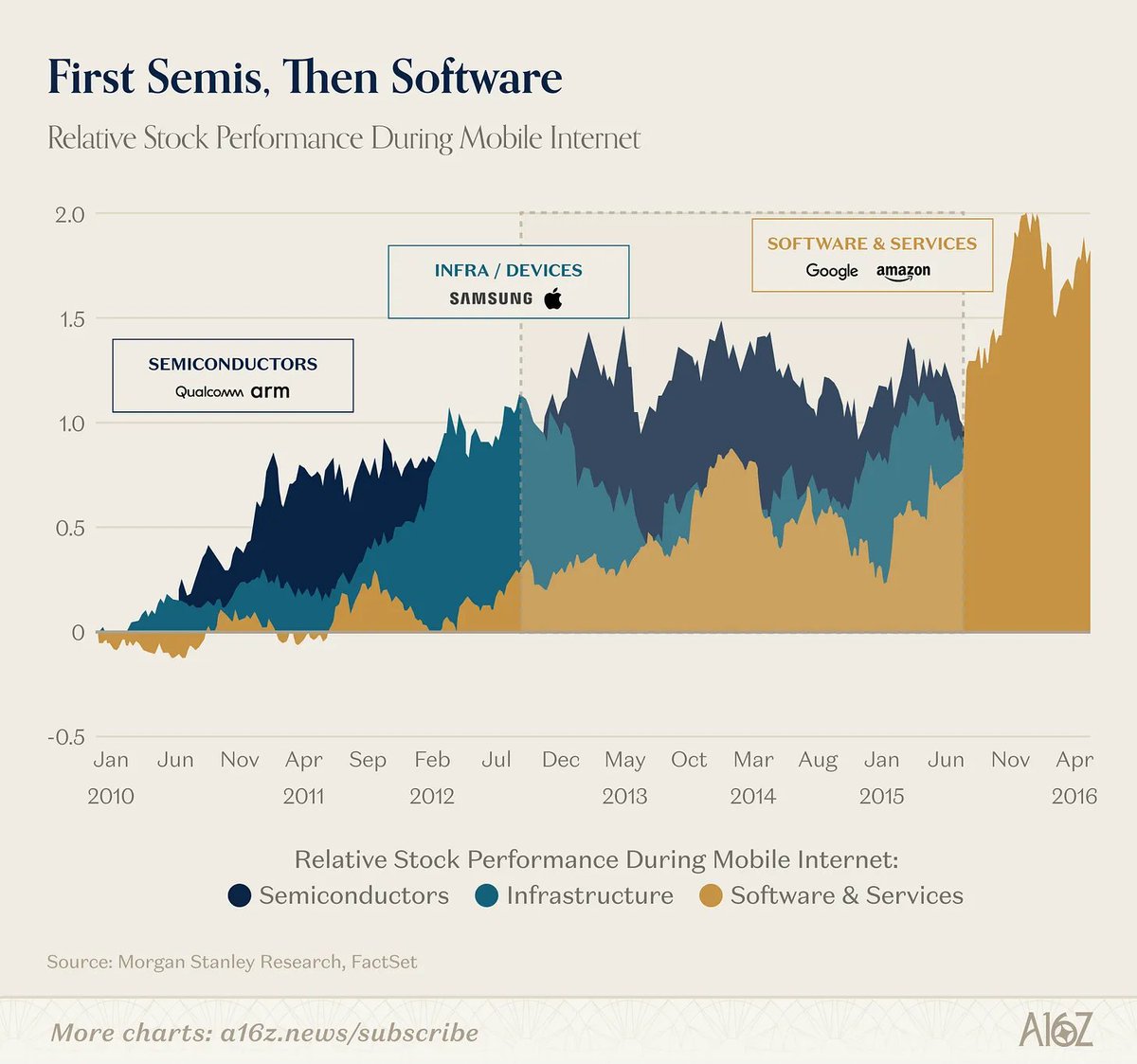

In the cloud supercycle, semis led and software followed (and you didn't need Qualcomm or ARM to tell you the value was migrating up the stack).

In AI, the infra layer itself is telling us the application layer is a separate, massive opportunity they can't fully capture.

a16z's @joeschmidtiv on why the app layer isn't dead: https://t.co/84QN5Mj9T3

Everyone with a portfolio under $100K doesn’t realize how quickly things can compound once you start making the right decisions consistently.

A lot of people think going from $100K to $1M is impossible, but surrounding yourself with smart investors, learning from the right people on X, and staying disciplined can completely change your trajectory.

My goal is to double my portfolio by year-end while minimizing risk, and after that, the sky’s the limit, the goal post is always moving.

So far, my win rate is super high and most companies I chose were home runs.

I’m sharing the entire journey here for free (and you’re always welcome to sub if you want).

Let’s create some more millionaires here.

Everyone is chasing $SIVE or looking for the next

$AEHR or $AXTI.

I think I found it… Not one. But two. Both sitting at the exact chokepoint.

This is maybe my favourite trade ideas the market hasn’t priced yet:

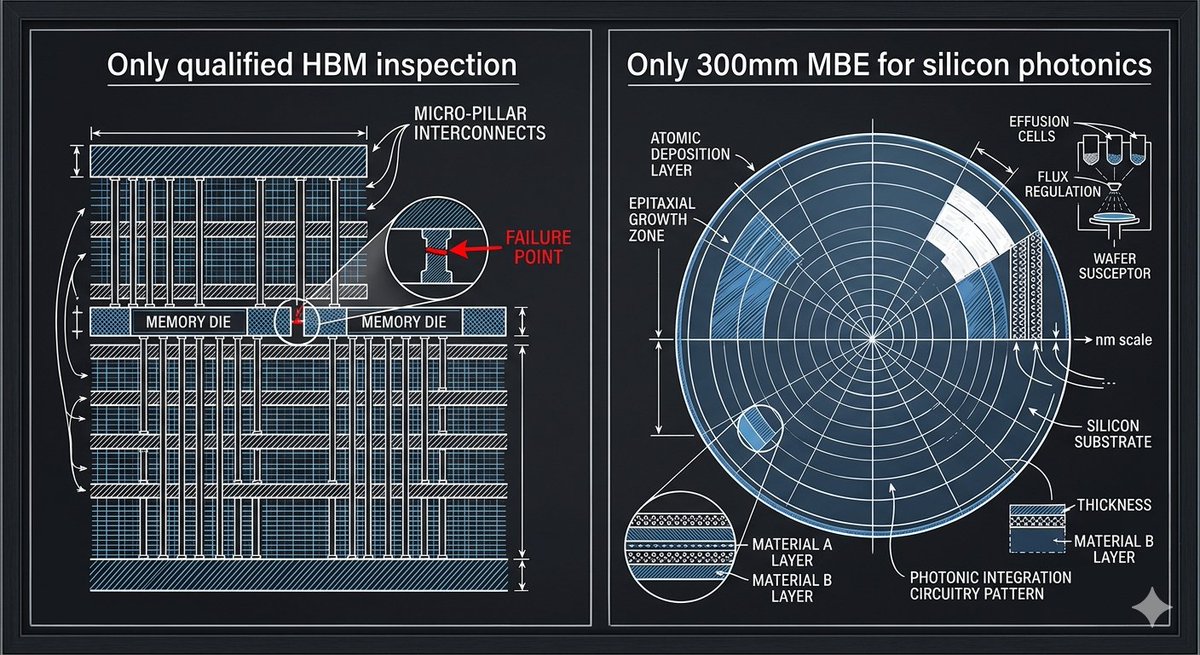

CONSTRAINT 1: HBM inspection AI chips are not a single piece of silicon.

A modern $NVDA GPU is a stack. A logic die at the bottom. Four to eight HBM memory dies bonded on top.

Each memory die connected to the next through thousands of through-silicon vias, copper pillars drilled through the chip itself.

Then that entire memory stack gets attached to the logic die through thousands more micro-pillar interconnects.

Each pillar is smaller than a human hair. One defective pillar.

One. That’s all it takes to kill a $40,000 AI GPU package.

No buffer. No workaround. The whole unit is scrap.

And here’s the constraint that makes this critical right now:

HBM supply is sold out through at least 2027. No significant new capacity comes online until late 2027. There is no spare capacity. Every die that gets made needs to reach a GPU. A defect found late in the process isn’t a minor setback, it’s a $40,000 unit written off with nothing to replace it.

So the industry doesn’t sample-inspect HBM stacks.

It performs 100% INSPECTION. Every device. Every pillar. Every generation.

As HBM advances from HBM3e to HBM4, the die gets larger, the micro-pillar density increases, and the inspection requirement becomes more complex, not less.

There is one company with qualified equipment for this job at a leading US memory manufacturer.

$COHU - Cohu Inc.

Their Neon platform performs full 6-sided optical inspection of every HBM device using proprietary AI-trained software, defect recognition trained specifically on each customer’s device architecture.

You can’t buy a competitor’s system and retrain it in a quarter. The switching cost is measured in years.

The numbers:

→ $488M cash. No dilution risk.

→ Orders up 163% year-over-year Q1 2026

→ $750M pipeline. 5 customers in active qualification.

→ HBM revenue guidance raised from $15M to $80–100M in a single year

The market is pricing this as a test equipment cycle recovery.

The correct frame: the only qualified inspection bottleneck in the HBM supply chain.

Test equipment multiple: 3–4x EV/Revenue. AI infrastructure bottleneck multiple: 7–10x.

CONSTRAINT 2: Silicon photonics fabrication Copper wires are hitting their physical limit inside AI data centers.

Moving data between GPUs at the speeds AI training requires generates heat, signal loss, and power draw that copper interconnects can no longer handle efficiently. The industry’s answer is silicon photonics, lasers built directly onto chips, transmitting data as light instead of electrons.

Co-packaged optics (CPO) embeds those lasers directly into AI switches. Forecast penetration: from near-zero today to 35% of all optical networking by 2030.

Every one of those lasers is grown using a process called molecular beam epitaxy; MBE. A process that deposits semiconductor materials one atomic layer at a time, under ultra-high vacuum, with tolerances measured in atoms.

The problem: the entire industry’s MBE infrastructure was built for 150mm and 200mm wafers. Silicon photonics runs on 300mm production lines, the same wafer size used in leading-edge logic fabs.

There was no MBE system compatible with 300mm production lines.

Until $ALRIB built one.

Meet ROSIE; Riber Oxide on Silicon Epitaxy is the first MBE platform engineered specifically for 300mm silicon photonics production lines. No other equipment company makes this.

The first two systems were ordered in 2025. ROSIE 2 the dual-chamber production version, goes into manufacturing in 2026.

This is Year 0 of the ramp. Analyst consensus price target: €6. Current price: €15+.

The gap exists because analysts are modeling Riber as a €40M scientific instruments company.

Not one single sell-side model contains ROSIE as a separate revenue line.

Silicon photonics is a $17B market by 2035. Riber’s current revenue: €40M. Market cap: €320M (~$340M USD).

If ROSIE becomes the production standard for 300mm silicon photonics the way MOCVD became the standard for LED manufacturing, the revenue trajectory and the multiple both re-rate from here.

Two constraints. Two chokepoints. One sits between every HBM die and every AI GPU that ships.

The other is the only equipment that can grow the lasers replacing copper in AI infrastructure. Both are being priced on the wrong metrics.

The market finds them eventually.

This is not financial advice. Do your own due diligence.

For full disclosure I haven’t taken a position myself, yet.

They are both on my watchlist. I'm considering adding one of them to mmy short-term portfolio.

$ALRIB looks like the most asymmetrical setup. A potential ten-bagger.

$COHU the more safe-play. 3-5X. A potential

$OUST look a like setup.

@ParadisLabs any thoughts? I can’t call out @aleabitoreddit since I’m blocked, apparently.

I'm also curious on other great investors perspective here: @moninvestor@Kaizen_Investor and @daniel_koss

-BP